With the onslaught of electrification, the wave of change in the global automotive industry is more turbulent than expected. At the beginning of April 2022, BYD Automobile announced that it would stop producing fuel vehicles from March 2022 and would focus on pure electric and plug-in hybrid vehicles in the future, which also marked BYD becoming the first car company in the world to officially announce the suspension of fuel vehicles, and this milestone event also means that the "electric vehicle era" or is coming.

Globally, the major car companies in Europe, the United States and Japan, which originally occupied a leading position in the field of traditional fuel vehicles, have undergone profound changes in their ideas in the past two years after experiencing a cautious wait-and-see and passive acceptance stage, and have taken the initiative to embrace this general trend, and even continue to accelerate the process of electrification, intending to regain their right to speak.

The electrification transformation and process of global car companies have accelerated again

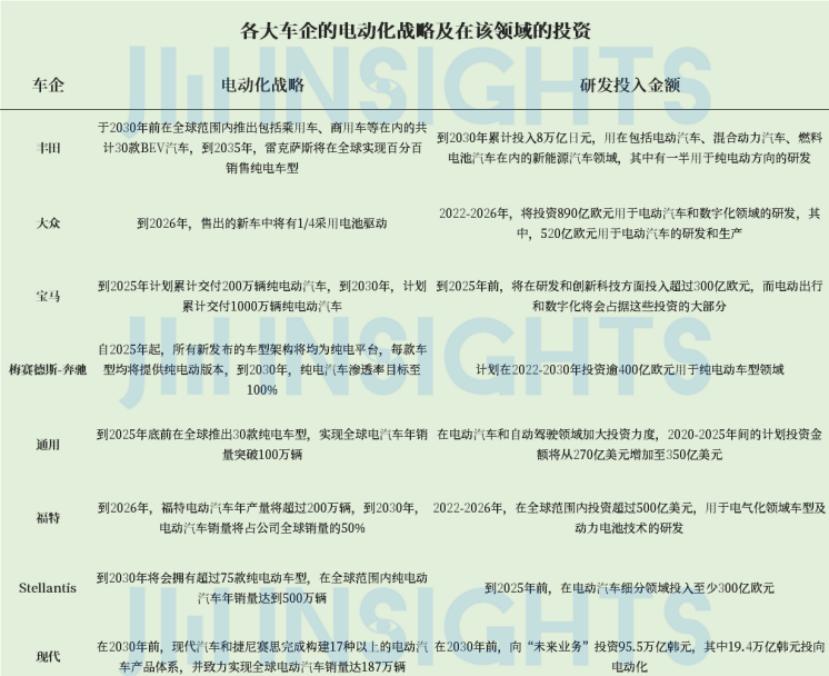

Under the trend of automobile electrification, only by following the trend can we accelerate its position in the electric vehicle market. As strong as Toyota, it is no exception, as the helmsman of Toyota Motor, Toyota Corporation President Akio Toyoda May be the most cautious car company leader for pure electric vehicles. And now, the picture suddenly turns. In December 2021, Toyota announced its latest electrification strategy, launching a total of 30 BEV (all-electric) vehicles worldwide by 2030, including passenger cars and commercial vehicles, and by 2035, Lexus will achieve 100% sales of all-electric models worldwide. To this end, Toyota plans to invest a total of 8 trillion yen by 2030 in the field of new energy vehicles, including electric vehicles, hybrid vehicles, and fuel cell vehicles, half of which will be used for research and development in the direction of pure electric.

Of course, unlike other car companies, BEV is only one of Toyota's all-round strategic options, and Volkswagen, BMW, Mercedes-Benz and other European car companies have announced electrification strategies two years earlier, and now they are accelerating the electrification process, Ford, GM and other American car companies, as well as Hyundai and other South Korean car companies are also catching up, the following figure is the electrification strategy of major car companies and their huge investment in this field.

As early as 2016, the Volkswagen Group began the electrification transformation. In December 2021, Volkswagen announced a new plan for electrification transformation, specifically, 89 billion euros will be invested in research and development in the field of electric vehicles and digitalization in 2022-2026, which will account for 56% of the group's total investment, of which 52 billion euros are used for the research and development and production of electric vehicles, 30 billion euros for software development, and it is expected that by 2026, 1/4 of the new cars sold by Volkswagen will be battery-driven.

In March 2022, the BMW Group also announced at its annual earnings report that the electrification process will be accelerated again, and more than 30 billion euros will be invested in research and development and innovation technology by 2025, and electric mobility and digitalization will account for the majority of these investments. In terms of details, in 2022, mass production and trial production of pure electric vehicle models will reach 15 models, based on the new structure of the "new generation" model will begin trial production in 2024, at the same time, with the rapid expansion of the product lineup, BMW Group is expected to increase sales of electric vehicles will also grow rapidly, by the end of 2025, BMW Group plans to deliver a total of 2 million pure electric vehicles, by 2030 plans to deliver a total of 10 million pure electric vehicles.

Mercedes-Benz unveiled a new electrification strategy in July 2021, transforming from "electric first" to "full electric". To promote a comprehensive electric transition, Mercedes-Benz plans to invest more than 40 billion euros in the field of pure electric models in 2022-2030. According to the plan, in 2022, Mercedes-Benz will provide pure electric models in all market segments, 3 pure electric model architecture platforms will be released in 2025, and from 2025, all newly released model architectures will be pure electric platforms, each model will provide pure electric versions, and the penetration rate of pure electric vehicles will reach 100% by 2030.

Entering 2021, under the impetus of the US electric vehicle support policy, the sales of electric vehicles in the United States have grown strongly, and major car companies have also fully invested. In June of the same year, GM announced that it will increase its investment in electric vehicles and autonomous driving, increasing the planned investment amount from $27 billion to $35 billion in 2020-2025, and planning to launch 30 pure electric models worldwide by the end of 2025, achieving annual sales of global electric vehicles exceeding 1 million.

In May 2021, Ford officially released the Ford+ development plan, confirming the full transition to electrification, in which it is expected that by the end of 2025, Ford will invest more than $30 billion in the electrification business (including battery development), and this year Ford's electrification pace has accelerated, planning to invest more than $50 billion globally in 2022-2026 for the research and development of models and power battery technologies in the electrification field. Its goal is to produce more than 2 million electric vehicles a year by 2026, and by 2030, electric vehicle sales will account for 50% of the company's global sales.

In February 2022, stellantis Group officially announced that its goal is to achieve all vehicles sold by the Group in Europe to be pure electric models by the end of 2030, and 50% of the cars sold in the United States are pure electric models. According to the plan, by 2030, the Group will have more than 75 pure electric vehicle models, and the annual sales of pure electric vehicles will reach 5 million units worldwide. To this end, Stellantis plans to invest at least 30 billion euros in the segment of electric vehicles by 2025.

South Korean automaker Hyundai Motor Group also officially announced its medium- and long-term electrification strategy in early March this year. According to the plan, Hyundai Motor and Genises plan to complete the construction of more than 17 kinds of electric vehicle product systems by 2030, and strive to achieve global electric vehicle sales of 1.87 million units, with a market share of 7%, while ensuring that the operating profit margin of electric vehicle related departments will reach more than 10% in 2030. To this end, Hyundai Motor plans to invest 95.5 trillion won in the "future business" by 2030, of which 19.4 trillion won will be invested in electrification and 12 trillion won will be invested in software service capabilities including autonomous driving.

In 2021, global sales of new energy vehicles have reached a new high, reaching 6.75 million units, an increase of 108% year-on-year. JW Insights pointed out that judging from the electrification strategies of the above-mentioned major car companies and their huge investments in this field, global electrification will accelerate in the next three years. For now, the world's major traditional automakers are racing against time, but none have gone ashore.

Splitting up the electric vehicle business will be the trend of the times

Although the traditional car companies under the torrent of the times have a firm belief in electrification and endless strategies, Ford Motor's resolute separation of electric vehicles and fuel vehicles is still a shock to the industry. After several turns, in early March this year, Ford announced the establishment of an independently operated electric vehicle business unit Ford Model e and a fuel vehicle business unit Ford Blue, but also shared in some related technologies and practical applications to form a scale benefit to promote the continuous improvement of operational efficiency, and at the same time, together with the previously announced Ford Pro, which is responsible for commercial vehicles and related service solutions, three new business units are expected to achieve independent operation and self-financing in 2023.

Indeed, the current electrification business of traditional car companies is still small (see the data of CleanTechnica in the figure below), and it also needs blood transfusions of traditional fuel vehicle business, so the split is not an overnight thing. Taking Ford as an example, the electrification transformation has achieved initial results, but it is still in the beginning, in 2021, Ford's new energy vehicle sales in the global market are 112,000 units, accounting for only 3.01% of its total sales of 3.72 million vehicles in the world, and the only product that can really be regarded as a global electric strategic layout is Mustang Mach-E (electric pickup trucks are currently only for mass production and sales in the United States), so the industry believes that the announcement of the independent operation of the electric vehicle sector seems to be somewhat unexpectedly early.

But JW Insights believes that the move to break up the electric vehicle business may be opportune. In 2021, Tesla, which sells less than 1 million vehicles a year, will win the global car company with a market value of $1 trillion, which stimulates many established car companies with a century-old history to undergo radical changes, and splitting the business to seek structural changes may be a key step for them to achieve resistance and reimagine the future again.

Coincidentally, The Renault Group is also working on plans to split. To catch up with rivals such as Tesla and Volkswagen, Renault outlined its strategic shift for the first time in February, with Renault likely splitting its electric vehicle business and internal combustion engine business into two "separate entities" and listing its electric vehicle business separately.

Behind the launch of this change is the electrification strategy that multinational car companies urgently need to achieve quickly. JW Insights believes that the splitting of the electric/internal combustion engine business will be a major trend in recent years, in fact, not only the international OEMs, but also the domestic OEMs will also separate some new energy brands.

In November 2021, GAC Group announced that the company intends to promote the mixed ownership reform of GAC Aeon through internal asset restructuring, introduce strategic investors, achieve in-depth integration and focus on the company's pure electric new energy vehicle business, promote the independent operation of GAC Aeon, and actively seek listing at an appropriate time.

JW Insights believes that splitting is a good choice, and it has three major benefits:

First, OEMs may seek new growth points through this wave of opportunities for rapid penetration of new energy.

Second, the valuation of traditional fuel vehicle companies and new energy vehicle companies in the capital market is very different, for example, although the sales volume of new energy vehicle companies like Tesla is only a fraction of that of traditional car companies, new energy vehicles represent the future, and these new energy vehicle companies are indeed at the forefront of intelligence, so their valuations are far more than traditional car companies, in this case, traditional car companies will split their business is more conducive to financing and accelerate the development of their new business.

Finally, due to the uniqueness of technology, new energy vehicles can be strongly bound to intelligent networking, especially automatic driving and some ecosystems, so under the general trend of software-defined cars, the organizational structure and process system of traditional OEMs, including procurement systems, research and development systems, and agility need to be redefined. The traditional organizational structure can not meet such needs, so it is necessary to independently come out of a company, independent brand operation, independent research and development, independent consumer docking, and even independent sales, using new retail, direct sales and other ways.

The construction of a mature electric vehicle supply chain has a long way to go

Of course, it is also necessary to face the development process of electrification, and the supply chain still faces many challenges and problems, one of which is the power battery supply chain. Power batteries are the most costly part of electric vehicles, so they have always been the "Achilles heel" on the road to the development of electric vehicles. At present, the development of new energy vehicles is too fast, the demand for batteries is rising, but the production capacity is obviously insufficient, so the price of raw materials has continued to rise since 2021. Today, the prices of rare metals such as lithium, nickel and cobalt have soared to multi-year highs.

For example, in March 2022, the data of Xinzhu lithium battery shows that battery-grade lithium carbonate (an important raw material for power batteries) has risen to more than 520,000 yuan per ton, while in 2020, the price of battery-grade lithium carbonate was only 38,000 / ton at a low level, and rose to 50,000 yuan / ton in January 2021, which can be seen to have doubled by more than 10 times.

On the other hand, the epidemic, the Russian-Ukrainian conflict and other geopolitical escalations will also exacerbate the original supply chain pressure, "All in electrification" road to add "black swan", global automakers on the road to electrification transformation more "step by step".

Since 2022, nearly dozens of car companies have announced the "price increase" of their new energy models, the following chart only lists some of the new energy vehicle companies/brands that have increased their prices since March 2022, and the main reason for their increase in the price of electric vehicles refers to the crazy rise in the price of raw materials for power batteries.

As for when the price falls, JW Insights believes that it depends on "when supply and demand are balanced". From the demand side, as mentioned above, the process of global electrification is still accelerating, so the demand for power batteries will double. Global automakers are scrambling to reserve key raw materials for electric vehicle batteries, and supply agreements are constantly being "bound" to upstream manufacturers of raw materials, but the construction of production capacity requires cycles, and most of them will not be put into production until after 2023.

For example, Australian lithium miner Core Lithium said the first lithium ore is expected to start production in the fourth quarter of 2022 under the terms of the contract, with supplies scheduled to begin supplying to Tesla in the second half of 2023. Liontown Resources, another Australian lithium miner, also said that under the agreement, starting in 2024, Tesla will purchase 100,000 dry metric tons of spodumene concentrate in the first year.

JW Insights believes that from the supply and demand level, global lithium supply is difficult to alleviate in the past two years. Battery costs increase, coupled with the full cancellation of subsidies in 2023, the market price of domestic electric vehicles may be difficult to decline. The same is true of the foreign electric vehicle market. More critically, the rising cost of raw materials and energy in the supply chain will also bring greater pressure to the electrification transformation of car companies.

It is worth vigilance that some analysts believe that the price increase will affect the acceptance of electric vehicles, and consumers are resistant to overpaying for electric vehicles. They argue that it will take longer than expected for automakers to achieve cost parity between electric vehicles and conventional fuel vehicles, and more critically, any factor that increases costs will affect or even hinder the acceptance of electric vehicles.

But so far, ev consumers have not stopped. According to EV-volumes forecasts, global electric vehicle sales grew by nearly 120% in the first quarter of 2022. Despite soaring prices, buyers around the world are still lining up to buy electric cars this year, which also upends the traditional automotive industry's view for many years that EV sales will only explode after the cost of batteries falls.

Bloomberg New Energy Finance (BNEF) also expects that in June this year, the world will move towards an important milestone in the popularization of electric vehicles, when 20 million electric vehicles will be on the road, in the second half of 2022, the global electric vehicles will increase by nearly 1 million per month, calculating that about every 3 seconds to add a new one, by the end of 2022, it is expected that more than 26 million electric vehicles will be on the road worldwide.

In view of this, JW Insights believes that in the development and growth of the industry itself and the external ups and downs, although there is a long way to go, the electric vehicle supply chain needs to be further improved and consolidated, and the power battery supply chain is only one of them. In the future, more control over the supply chain could help automakers maximize their protection from rising prices and component shortages. (Proofreading/Sami)