2021 has come to an end, looking back at this year, the car market can be said to be ups and downs, wonderful, the birth of a lot of "hot words", on the one hand, the car market suffered a cold snap, the overall sales of cars declined, "missing core" and "pre-sale" became the "periphery" of the epidemic; on the other hand, electrification is vibrant, "new energy vehicle penetration" continues to increase, "battery" is popular, "Huawei concept" triggered a capital frenzy to spawn the new car 2.0 era.

These annual hot words have accompanied us through 2021, experienced the cold and warm of the car market, and left a mixed report card. Looking back again, which hot word represents the 2021 rim, which hot word is impressive, and which hot word has the most far-reaching impact? To this end, this article has reorganized these annual hot words, summarizing the past with readers and meeting the future.

"Missing core":

There has been some relief, but it will continue

A small chip, but induced a major "earthquake" in the industry. The wave of "lack of core" that broke out at the end of 2020 is still affecting the development of the automobile market, and in 2021, it will become the "black swan" of the "black swan" that affects the development of the automobile industry under the "black swan" of the epidemic. Chen Shihua, deputy secretary-general of the China Association of Automobile Manufacturers, analyzed that the shortage of chips has led to a reduction of 1.3 million to 1.4 million vehicles in China's auto market this year.

There are many reasons for "lack of core", on the one hand, although cars generally use basic chips, but the use is very large, a traditional fuel car uses about 40-150 kinds of chips, the use of new energy vehicles is higher, basically 4-5 times that of traditional fuel vehicles, so the automotive chip supply chain requirements are very high; on the other hand, the outbreak of the global epidemic has led to a direct reduction of 40% in the international chip industry, and there is a serious supply shortage, especially the Malaysian epidemic situation has even led to the sudden supply of individual varieties of chips.

In the face of the problem of "lack of core", various automakers can be said to have exhausted their methods. The leaders of automobile manufacturers do not hesitate to fly and squat in the factory, just to be able to get the chip at the first time. Even so, the lack of core still plagues enterprises, and the industry even derives the ideal "first delivery and then reloading" model. Audi also had to equip the new car with only one remote control key, and then deliver a second remote control key to the user after the production capacity was restored.

Automakers are looking for ways to use general-purpose chips, such as Tesla, Volkswagen and Nissan, to ensure supply flexibility by replacing custom chips with general-purpose chips. GM plans to reduce diversity by 95 percent by consolidating semiconductors currently in use into three product groups. Stelantis also plans to jointly develop four new semiconductor product lines with Foxconn to replace 80% of chip demand.

In addition to using general-purpose chips, some companies are also trying to develop their own chips. Taking Geely as an example, while using the global layout scheduling resources to supply chips, it also began to directly manufacture chips, and recently announced China's first 7nm process vehicle specification SOC chip developed by Core Qing Technology, which is expected to achieve mass production in the third quarter of 2022.

For traditional or long-established car brands, they can have special channels to solve chips, such as returning from overseas chips, or producing chips themselves, but for new car-making forces, there is only one solution, that is, to order chips from suppliers. He Xiaopeng, chairman and CEO of Xiaopeng Motors, even shouted helplessly, "Whoever can give me the chip, I will invite him to drink more." ”

Although the shortage of chips has been alleviated at present, and major car companies are also actively "self-help", the "lack of cores" may continue to accompany the development of the automobile industry in the form of "normal" in the next two years. According to data from the Korea Automotive Research Institute, the cumulative orders for semiconductors in major cars around the world exceed the semiconductor production capacity next year by as much as 30%, and automotive semiconductor companies are accepting orders in 2023. The average lead time after an order in the semiconductor industry also increased from 22.9 weeks in October this year to 23.3 weeks a month later.

"Pre-Sale":

Orders are placed first, then produced, and chip reserves are effectively allocated

Affected by the shortage of chips, the car market has borne a lot of pressure this year. The data disclosed by the Federation of Automobile Manufacturers shows that the capacity utilization rate of the automotive industry continued to decline, and remained at about 71% in the third quarter of the third quarter when the core was seriously missing. Therefore, in order to maintain profitability, automobile manufacturers can only prioritize the production of high-profit models, which also leads to the extension of the pick-up cycle of most models of the terminal to about one month, and the longest or even wait for more than half a year.

Production capacity declined, or even stopped production, and automakers rarely fell into the dilemma of "no car to sell" at the terminal, resulting in a sharp decline in sales. According to the Association of Passenger Vehicles, retail sales in the passenger car market were about 1.816 million units in November this year, down 12.7% year-on-year.

This abnormal "short supply" has also quietly changed the sales model of car companies and the purchase habits of consumers. Many of the new cars on the market this year have been changed to "pre-sale": order first, then produce. When will the car be delivered? and other notifications. There are even cases where the Kr 2021 deliverable order is sold out in June, accepting the 2022 order.

Not only new cars, but also hot-selling models that have already been launched have resumed "pre-sale" and adopted "order-based production": orders are placed first, and then scheduled. "Now it's all order-based sales, ordering, scheduling, producing, and delivering." Dealer said.

Pre-sales are a traditional marketing tool and are not new. Industry insiders pointed out that the previous pre-sale was a test of the product sales prospects of enterprises in order to increase the exposure of brand products. Today's "pre-sale" model of order-based production, on the one hand, can help enterprises to consolidate order data and adjust products on this basis. Especially in the context of the current chip shortage and the inconvenience of new car scheduling, enterprises can understand the needs of consumers in advance through pre-sales, allocate valuable chip reserves in a targeted manner, and reduce inventory waste.

On the other hand, consumers gradually accept the "pre-sale" model, which is also a sign of the gradual maturity of China's automobile consumption, indicating that consumers have a clearer understanding of their own needs and can calmly choose a car for themselves. The implementation of pre-sales also gives consumers more time to consider needs, analyze products, and make scientific decisions.

The shortage of automotive chips, the market into a special period of "supply determines demand", the industry has called for many years of "sales to determine production" did not expect to be realized in such a market environment.

New energy penetration rate increase:

The industry ushered in a rapid upward inflection point

Chip shortages are still stubborn, but the electric trend is unstoppable. 2021 is the first year of the "14th Five-Year Plan", under the guidance of the "double carbon" goal of "achieving carbon peak by 2030 and carbon neutrality by 2060", major auto companies have responded, sounding the clarion call for the explosive growth of new energy vehicles.

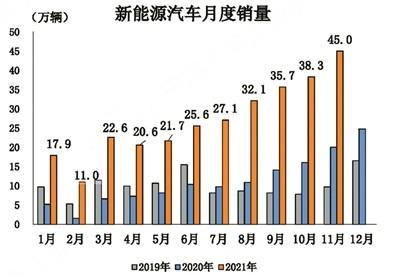

According to data from the China Automobile Association, from January to November this year, the cumulative sales of new energy vehicles in China have exceeded the annual expectations, reaching 2.99 million units, an increase of 1.7 times year-on-year. At the same time, the market penetration rate of new energy vehicles has also increased from 5.4% at the beginning of this year to 12.7%. It is worth mentioning that in November this year, the penetration rate of domestic new energy vehicles reached 17.8%, higher than that of the whole year, of which the market penetration rate of new energy passenger vehicles was close to 20%, reaching 19.5%.

Generally speaking, the penetration rate is at 10%-15%, which is the inflection point of the rapid rise of the industry, and after the penetration rate of China's new energy market exceeds 10%, the speed of market penetration will be very fast. The China Automobile Association predicts that in 2021, China's new energy vehicle sales will reach 3.4 million units, an increase of 1.5 times year-on-year. For the development trend of the domestic new energy vehicle market next year, the China Automobile Association also gave an optimistic expectation of 5 million vehicles sold, an increase of 47% year-on-year.

According to this calculation, the market penetration rate of new energy vehicles in China will be about 18% next year, and this penetration rate is very close to the goal of "20% penetration rate of new energy vehicle sales in 2025" proposed in China's "New Energy Vehicle Industry Development Plan". Some people in the industry believe that the 20% penetration target proposed in the above development plan is expected to be achieved ahead of schedule next year.

Whether it is to achieve the "double carbon" goal, or optimistic about the prospect of rapid increase in sales and penetration rates of new energy vehicles in 2021, more and more brands have joined the new energy vehicle industry. During the Guangzhou Auto Show alone, 241 new energy models were exhibited, of which 88 were exhibited by international brands.

Luxury brands, in particular, are electrifying "ALL IN". In 2021, BMW, Mercedes-Benz and Audi respectively launched the BMW i series, EQ series and Audi etron series; Volvo and Cadillac unveiled new pure electric products, and Jaguar Land Rover, Lexus and Lincoln seized the hybrid market. Ultra-luxury also began to "electrocute", Lotus, one of the world's three major supercars, exhibited the hall-of-the-art pure electric supercar Evija in China, Bentley also launched the First Flying Spur Plug-in Hybrid Edition in China, introducing a selection of materials in line with the concept of sustainable development.

At the same time, other international brands are also speeding up the electrification "counterattack", volkswagen ID series listed a number of models, Toyota released the "TOYOTA bZ" brand, Honda released the "e: N" pure electric brand, Nissan e-POWER technology into China, the first Chinese model Nissan e-POWER Xuanyi listed...

In addition to the introduction of electrification technologies and products by luxury brands and joint venture brands, independent brands that entered the electrification game earlier began to enter a new stage, that is, the launch of a new high-end electric vehicle brand born from traditional car companies. BAIC ARCFOX Polar Fox, Dongfeng Lantu, SAIC Zhiji and Feifan Automobile, Changan Avita, Geely Krypton, Great Wall Salon...

In addition, the new forces of car manufacturing continue to march forward, and the delivery volume continues to break through. In November, weilai, Xiaopeng, ideal, Nezha, zero-run, weima six new car-making forces delivered a total of about 60,600 new cars, accounting for about 16.04% of the domestic new energy passenger car market. Among them, the delivery volume of Xiaopeng, Ideal, Weilai and Nezha 4 new car-making forces has exceeded 10,000 vehicles.

battery:

A hundred flowers bloom and usher in the spring of development

The rapid development of new energy vehicles has also made the battery industry usher in "spring". According to the data released by the China Automotive Power Battery Industry Innovation Alliance, from January to November this year, the cumulative loading volume of power batteries in China was 128.3GWh, an increase of 153.1% year-on-year.

While the loading volume continues to increase, the industrial structure is also constantly optimized. The power battery industry is moving from the early multi-point decentralized layout to the head enterprises. The "Blue Book of Power Batteries" shows that in 2009, after The demonstration and promotion of new energy vehicles was carried out in China, there were more than 230 power battery manufacturers in the country. After years of development, the market share of the top ten enterprises in China's power battery has reached 91.9%, and the loading volume from January to November this year has reached 118.06GWh.

In the face of the power battery market with huge potential, automakers have also begun to lay out the battery field and harvest the power battery market. For example, GAC Aean released a magazine battery to achieve the ternary lithium battery package of needle can not catch fire; BYD's pure electric vehicle model is fully equipped with blade batteries to seize the lithium iron phosphate technology market; Beiqi Blue Valley recently announced the completion of the development of the second generation of solid-state batteries, battery system bench test verification and vehicle mounting verification, to seize the solid-state battery market.

In particular, the solid-state battery market has also attracted traditional multinational car giants such as Mercedes-Benz, BMW, Ford, and Toyota. BMW Group plans to start testing and integration of solid-state battery prototypes next year, Mercedes-Benz plans to start testing solid-state battery prototypes in 2022, Volkswagen Group announced that it will use solid-state batteries in 2025; Ford will start testing products next year, Toyota plans to achieve continuous and stable production of all-solid-state batteries by 2030, and Nissan Plans to launch electric models equipped with all-solid-state batteries by fiscal 2028.

Of course, the major power battery companies that have taken the lead in enjoying the market dividend have not posed as a stable Diaoyutai, but have opened the road to expansion. According to incomplete statistics, power battery companies such as CATL, BYD, Ewell Lithium Energy, and Hive Energy have announced that the new production capacity in the next 5 years will exceed 2TWh, which is about 20 times the loading volume this year.

The heat of the battery market has also allowed the battery industry to gain unprecedented capital support. Among them, Ningde Times (300750.SZ), Yiwei Lithium Energy (300014.SZ), Guoxuan Hi-Tech (002074.SZ), Xinwanda (300207.SZ) and other individual stocks, all gained more than 40% during the year. Among them, especially in the Ningde era, the growth was the most rapid. According to the data, the stock price of CATL has risen from about 300 yuan at the beginning of the year to a maximum of 692 yuan, and the market value has soared all the way to 1.6 trillion yuan, an increase of nearly 1 times compared with the beginning of 2021. In addition, the upstream and downstream industries of power batteries such as lithium ore, lithium battery positive and negative electrodes, lithium battery electrolyte and other sectors rose by more than 100% during the year.

"Huawei Concept":

Capital frenzy spawned the new car 2.0 era

The "mania" of the capital market not only appears in the field of batteries, but also in the field of car manufacturing.

Although Huawei has publicly stated eight times in the past three years that it "does not build cars", every action of Huawei has affected the direction of capital. Especially when Huawei participates in the automotive industry as a supplier or partner, the listed companies behind the brands of Xilix, ARCFOX Pole Fox and Avita Technology (formerly Changan Weilai), Xiaokang Shares, Beiqi Blue Valley, and Changan Automobile have become three famous "Huawei concept stocks", attracting the influx of many capital.

According to the data, after the cooperation with Huawei was reached, the stock prices and market value of Xiaokang Shares, Beiqi Blue Valley and Changan Automobile have risen sharply, and even many times, of which the increase in Xiaokang shares is the most obvious. According to statistics, Xiaokang shares, from about 15 yuan per share at the beginning of the year, rose to 83.83 yuan, and the market value also soared from about 20 billion yuan to a maximum of 101.519 billion yuan, a five-fold increase.

After a year of fermentation, the "Huawei Concept" has made new progress in recent days. Xilix announced the launch of its first model, the Q&I M5, a brand of AITO, which will be equipped with Huawei's Hongmeng system. Polar Fox Alpha S Huawei HI Edition has been delivered in small quantities. The Huawei concept is being implemented to implement software-defined cars.

Compared with the capital hype Huawei concept, the layout of technology companies is more direct. 360 Group invested in Nezha, Skyworth released the first pure electric SUV, Baidu joined hands with Geely to form Jidu Automobile, Xiaomi and Didi directly announced the car, the founder of Xiaoniu Electric entered the new energy vehicle market, and capital is grabbing the "big cake" in a diversified way.

With the entry of a number of Internet technology companies, the first batch of new car-making forces represented by Weilai and Xiaopeng have the potential to become a "front wave". Xiaomi, Baidu and other companies lurking as investors have directly entered the market to build cars, bringing different business models. More importantly, new energy vehicles have been upgraded from "the direction of automobile industry development" to a chess piece in the big chess game of "carbon peak", and in such a major policy background change, the new forces of car manufacturing will also enter the 2.0 era.

Summarizing the past is to make a better departure. 2021 can be said to have ended, this year, the automotive industry experienced the "lack of core" production trough, encountered no car to sell dilemma, but also ushered in the explosive growth of new energy vehicles and batteries, attracted more capital and technology companies new players to enter, a variety of factors together to boost, China's auto market is bursting with new vitality.

Text/Wen Chong