In 2021, the domestic new energy vehicle market entered a stage of explosive growth, and the annual retail sales of new energy passenger cars reached 2.989 million units, an increase of 169.1% year-on-year. From the perspective of terminal insurance, the cumulative insurance volume of new energy passenger cars in the whole year also reached about 2.894 million units, of which the cumulative insurance of new car-making brands (including Tesla, a total of 17 brands) was about 749,000 units, accounting for about 25.9%; the cumulative insurance volume of traditional car companies was about 2.145 million units, accounting for about 74.1%.

In the past year, the new forces of car manufacturing have grown very fast, and the volume brought by this is relatively large, but from the data point of view, the share of new power brands in the domestic new energy market is still small, relatively speaking, the proportion of new energy in traditional car companies is getting larger and larger. Under the trend of "3060" double carbon target, "double integral", pure electric drive route, etc., in 2021, traditional car companies launched a new energy counterattack war.

Full line layout of independent brands

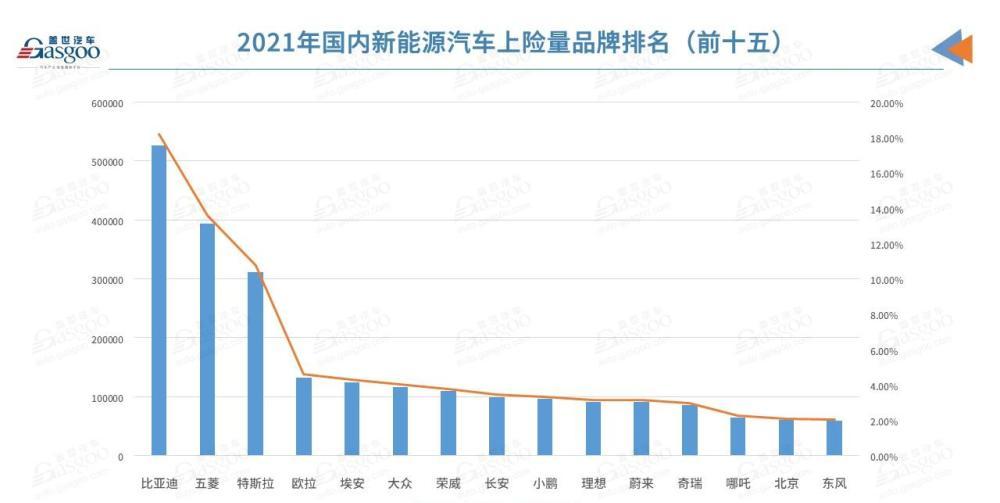

In the new energy vehicle market in 2021, independent brands can be described as the most momentum. The data shows that the domestic new energy market is ranked according to the amount of insurance on the brand, and the top fifteen brands have accumulated insurance to occupy about 81% of the market share, of which except Tesla are independent brands.

BYD is the biggest winner in the new energy market in 2021, with a cumulative insurance volume of about 526,000 vehicles in the whole year, accounting for about 18.2% of the market share, ranking first in the domestic new energy market. This achievement is due to THE CONTINUOUS expansion of BYD's pure electric and plug-in hybrid models in 2021, as well as the full replacement of blade batteries and the mass production application of super hybrid technology.

Specifically, the blade battery has greatly improved its energy density, service life and safety compared with the previous lithium iron phosphate battery, and from April 2021, BYD's full range of pure electric models will be fully equipped with blade batteries. According to the data, the first BYDHan EV equipped with blade batteries will have a cumulative insurance of about 79,000 vehicles in 2021, ranking the top of the list of pure electric models. Qin PLUS EV and BYD e2 have more than 30,000 vehicles insured throughout the year, and Qin EV, YuanPro EV, Song PLUS EV, and Dolphin have more than 20,000 vehicles insured throughout the year.

In addition, BYD's plug-in hybrid models fully equipped with DM-i super hybrid technology have further increased their market share. In the annual plug-in hybrid model insurance ranking, the first four models are from BYD, Qin PLUS DM-i, Song PLUS DM-i, Tang DM, Han DM cumulative insurance of about 223,000 vehicles, accounting for about 53.1% of the plug-in hybrid market share. It is understood that the comprehensive mileage of models equipped with DM-i super hybrid technology can exceed 1200 kilometers, and the fuel consumption is as low as 3.8L per 100 kilometers, which effectively solves the problem of high fuel consumption when plug-in hybrid models lose power in the past.

Bydie is followed by Wuling, relying on the success of Hongguang MINIEV in the micro pure electric market, Wuling new energy vehicle insurance volume reached about 393,000 vehicles, accounting for about 13.6% of the market, of which Hongguang MINIEV insured about 390,000 vehicles in the whole year, ranking first in the new energy market sales, accounting for 13.5%. Some people believe that Hongguang MINIEV has the characteristics of low price, low car cost, and can be on the road, which effectively meets the needs of consumers for daily transportation. In addition, the success of Hongguang MINIEV has also driven Chery, Euler and other brands to lay out micro pure electric products, at present, the micro pure electric market has become the battlefield of independent brands.

After Wuling, the independent brands with more than 100,000 new energy vehicles insured throughout the year include Euler, GAC Eian and Roewe. Euler has continued to expand its products around the cat series in the past year, and the brand has focused on the car purchase needs of a new generation of female users, and has also carried out a series of innovative activities such as cat picking and body opening for female users. According to the data, Euler's annual insurance reached about 133,000 vehicles, accounting for 4.6% of the new energy market. Among them, Euler Black Cat and Good Cat are the main responsibilities, and the annual insurance volume reached 68,000 and 44,000 vehicles respectively.

In the past year, GAC Aeon has also accumulated more than 100,000 vehicles, reaching 124,000 vehicles. GAC Aeon's market performance is mainly supported by two vehicles, the AION S and AION Y, which have 71,000 and 31,000 vehicles in the whole year.

Compared with the above brands, Roewe and BYD rely on pure electric plus plug-in hybrid two legs, relying on pure electric matrix such as Kelaiwei and plug-in matrix such as eRX5 PLUS, Roewe New Energy has about 109,000 vehicles insured in the whole year, accounting for about 3.8% of the market share.

On the whole, the reason why independent brands have made great progress in the field of new energy in the past year is mainly because independent brands have released more core technologies and products, pure electric and plug-in hybrid products in the two-line investment layout, and these products have met the user's just needs to a certain extent. In addition, independent brands have achieved many innovative ways at the marketing level, such as community, user co-creation and other models have begun to "roll" from independent brands. In addition, independent brands are also gathering in the field of high-end new energy, and mainstream brands such as Great Wall, BYD, Dongfeng, and SAIC are already in the layout.

Traditional luxury brands differentiate in the field of new energy

In 2021, in the case of independent brand new energy in full swing, the performance of traditional luxury brands and joint venture brands in the field of new energy is slightly inferior, but mainstream brands have actually made great progress in the past year.

First of all, among the traditional luxury brands, BMW's achievements in the domestic new energy market are obvious to all. According to the data, BMW's annual insurance volume of new energy vehicles in China is about 47,000 vehicles, accounting for 1.6% of the market, which has far surpassed Mercedes-Benz and Audi. Mercedes-Benz and Audi were insured for 11,500 and 11,200 vehicles respectively, with a market share of about 0.4%, so the performance of "BBA" in the domestic new energy field has opened up.

BMW is mainly driven by the two-way layout of the pure electric BMW iX3 and the plug-in hybrid version of the BMW 5 Series, which have reached 22,000 and 23,000 units respectively in the past year. Some people believe that BMW's market performance is not unrelated to its official reduction of iX3 models. BMW had reduced the price of the BMW iX3 by 70,000 yuan in January 2021, and the price of its leading model was adjusted to 399,900 yuan. According to the insurance data, the monthly insurance volume of iX3 increased month by month after the official decline, from 100 vehicles per month to 1,000 vehicles, and nearly 4,000 vehicles in a single month in December.

BMW is in front, mercedes-benz is not weak. At the Guangzhou Auto Show in 2021, Mercedes-Benz listed two models, EQA and EQB, priced at 365,800 yuan and 437,800 yuan respectively, and formed a Mercedes-Benz pure electric matrix with EQC. In addition, the Mercedes-Benz plug-in hybrid matrix has Mercedes-Benz E-Class and GLE, but the overall risk situation of these two models throughout the year is not yet prominent.

Audi in the field of new energy in 2021 is mainly supported by e-tron and Q2L e-tron, of which the highly concerned e-tron has 1406 vehicles in the whole year, and the Q2L e-tron with a lower price is 4645 vehicles. In December 2021, Audi continued to increase the Q2L e-tron offensive, listing a new Q2L e-tron, the new model compared to the old model in the battery life increased by 23%, further enhance the product strength.

Compared with "BBA", lexus, Cadillac, Volvo and other brands in the second echelon of traditional luxury brands will have fewer actions in the field of new energy in 2021, and the layout of products is also relatively small. In November 2021, Cadillac announced the opening of pre-sale of its first pure electric model in China, the LYRIQ, which is pre-priced at 439,700 yuan and will begin delivery by the first owners in April this year. From this point of view, in the next two years, in the new energy market of more than 400,000 levels, not only will independent high-end brands be assembled, but also traditional luxury brands such as "BBA" and Cadillac will also respond.

The layout of new energy for joint venture brands is relatively slow

In the domestic new energy market, the overall volume of joint venture brands is relatively small, and in the ranking of new energy brands, only Volkswagen brands have rushed into the top ten. In 2021, the Volkswagen brand will have about 117,000 new energy vehicles in China, with a market share of 4.0%.

In the past year, Volkswagen ID.series models expanded, on the basis of Volkswagen ID.4 CROZZ, ID.4X, in 2021 Volkswagen also launched ID.6 CROZZ, ID.6X, ID.3 and other models in China, of which ID.4 CROZZ, ID.4X annual insurance reached 21,000, 20,000 vehicles, the last three models are still in a climbing state, and the annual insurance of each model is not more than 10,000.

After Volkswagen, the joint venture brands are relatively high in line with Sihao, Buick and Toyota. Among them, Sihao has about 35,000 insurance units in 2021, and its brand model E10X is a small car sold from 39,900 yuan, and the annual insurance volume of the car has reached 29,000 units.

Buick, Toyota and Honda have great advantages in the field of fuel vehicles, but they have not yet fully developed in the new energy market. Buick has two pure electric models on sale in 2021, Micro Blue 6 and Micro Blue 7 and Micro Blue 6 PHEV, with a total of about 25,000 vehicles in the whole year, and Toyota has only 21,000 vehicles in the whole year with a matrix of pure electric plus plug-in hybrid models. In addition, brands such as Beijing Hyundai, Chevrolet, Citroen and other brands did not exceed 4,000 new energy insurance vehicles in the whole year.

From the above point of view, although the joint venture brands are in full swing in the fuel vehicle market, their performance in the new energy market is far from the same. Some analysts believe that the reason why the market share of the joint venture brand in the domestic new energy market is low is mainly due to the system and process of the joint venture company, which is relatively low in efficiency and flexibility, which in turn leads to a slower speed of product launch and iteration, while the independent brand has a faster product launch and iteration speed in the past two years, coupled with the self-developed technology has been on the car, and the overall layout of the independent brand in the domestic new energy market is faster than that of the joint venture brand.