Source: United Credit

Summary of the report

In recent years, the mainland automobile market has entered a period of low- and medium-speed growth, and the characteristics of cyclical volatility have been highlighted. After three consecutive years of decline, in 2021, under the unfavorable situation of rising costs and chip shortages, the total sales volume of mainland automobiles has grown again under the drive of passenger cars, and the sales of commercial vehicles have declined; among passenger cars, new energy vehicles have grown significantly, the penetration rate has increased rapidly, and the mainland government has received good results in the cultivation of the new energy automobile industry for many years, and market demand has become an important force to promote the development of the industry.

The upstream supporting facilities of the mainland automobile industry are relatively complete, especially in the development of new energy vehicles, power batteries have a certain leading edge in the world. However, since the second half of 2020, the lack of supply of automotive chips has formed a customized contract for the production of major automakers; the mainland automotive chips have a high degree of dependence on foreign countries, and there are certain hidden dangers.

From the perspective of demand, in recent years, SUVs and high-end car preferences have been fully demonstrated in the mainland market, and with the changes in consumer groups, the market recognition of new energy vehicles that can carry the function of "smart + network connection" has increased rapidly; mainland independent brand manufacturers have gained advantages in the field of SUVs and new energy vehicles, narrowing the gap with joint ventures. The purchase demand for trucks is related to the scale of infrastructure investment and the total amount of social logistics, and the recent active fiscal policy of the mainland and the large scale of infrastructure investment are conducive to the stability of heavy truck sales; the development of the logistics industry, the implementation of policies such as road supervision are expected to maintain the growth of light truck purchase demand. Affected by the expansion of the rail transit coverage network and other factors, the mainland bus market is facing greater pressure, in recent years in a state of saturation, the future market demand mainly depends on the policy to promote the electrification of public sector vehicles, third- and fourth-tier cities public transport, growth prospects still need to wait and see.

As a capital-intensive industry, the automobile manufacturing industry has a high concentration. After the survival of the fittest since 2018, most of the bond issuers in the industry are currently head enterprises, with significant scale advantages, good overall financial performance, and generally higher credit ratings. In 2021, there was no bond default or deferral of redemption in automobile manufacturing enterprises, and the credit rating of the main body of one enterprise was downgraded; the scale of newly issued bonds was small and the coupon rate was low; the scale of existing bonds and the repayment pressure of bonds due within one year were small.

Looking ahead, in the short term, the mainland automobile manufacturing industry is expected to continue its growth trend in 2022. In the medium and long term, on the one hand, the reduction in demand growth will intensify the competition in the industry, and the living environment of weak enterprises will continue to deteriorate; on the other hand, the industry as a whole still has some room for development, and the possibility of a downward trend for many consecutive years in the future is small, and the industry as a whole is expected to operate stably, which is conducive to the credit level of most bond issuers to remain basically stable.

First, the operation of the automotive industry

In recent years, the mainland automotive industry has entered a period of low- and medium-speed growth, and the characteristics of cyclical volatility have been highlighted. After three consecutive years of decline, in 2021, the total sales volume of mainland automobiles will grow again driven by passenger cars, the production and sales of commercial vehicles have declined, and inventories have remained at a reasonable level; vehicle exports have increased significantly, and the international competitiveness of domestic enterprises has begun to appear. New energy vehicles have grown significantly, the penetration rate has increased rapidly, the new energy vehicle industry policy has received good results, and the fuel vehicle market will gradually shrink in the future and the accelerated growth of new energy vehicles will continue.

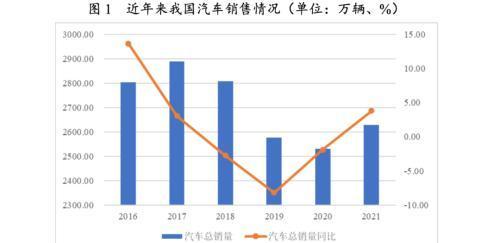

The scale of production and sales of China's automobile market has continued to rank first in the world for many years, but with the increase of automobile penetration, the sales growth rate has decreased significantly in recent years, and the characteristics of cyclical fluctuations have begun to appear. From 2018 to 2020, the total sales volume of mainland automobiles continued to decline. At the beginning of 2020, the new crown pneumonia epidemic has had an impact on the operation of all walks of life, the automobile market still continues to decline, in order to stimulate the consumption of new energy vehicles, the mainland government delayed the pace of subsidy policy decline, coupled with the good control of the epidemic in the second half of the year, the market demand for new energy vehicles began to reflect, and the decline in mainland automobile sales narrowed in 2020. In 2021, the mainland achieved automobile sales of 26.275 million units, an increase of 3.80% year-on-year, and the continuous decline in sales was reversed.

From the perspective of market segmentation, from 2018 to 2020, the trend of passenger car sales changes basically with the total sales of automobiles, showing a downward trend year by year; in 2021, passenger car sales were 21.469 million units, an increase of 6.61% year-on-year. From 2018 to 2021, commercial vehicle sales fluctuated, among which, driven by factors such as higher emission standards, stricter control and increased investment in infrastructure, commercial vehicle sales in 2020 increased by 18.69% to 5.1310 million units; and due to the early "overdraft" of sales in the previous year, in 2021, mainland commercial vehicle sales fell by 4.15% to 4.918 million units.

In terms of new energy vehicles, in 2021, the sales of new energy vehicles nationwide increased by 157.50% year-on-year to 3.521 million units, accounting for 13.40% of total vehicle sales from 5.40% in 2020. The outbreak of new energy vehicles in 2021 is the result of the care and cultivation of the mainland government for many years. As a new thing, before 2018, the mainland's new energy vehicle products were relatively single, the cost and selling price remained high, and the sales relied heavily on the purchase subsidy; due to the decline of the subsidy policy, the sales volume of new energy vehicles in the mainland declined in 2019. However, at the same time as the subsidy policy has declined, the mainland government has sacrificed the "double integral" policy stick and strongly promoted it from the supply side, making the new energy of automobile products a consensus in the industry. With Tesla's entry into China and mainstream manufacturers have laid out the new energy market, since 2020, the mainland's new energy vehicle products have been continuously enriched, coupled with the scale effect has reduced the cost of parts procurement, the price of new energy vehicles has become more and more close to the people, and the market recognition has increased rapidly. From 2019 to 2020, the driving force of new energy vehicle sales in the mainland has rapidly switched, and the explosive growth in 2021 is the embodiment of the real demand of the market.

From the perspective of inventory, since 2019, the monthly inventory of mainland automobiles has decreased significantly compared with previous years; from the perspective of inventory coefficient, in early 2020, affected by the epidemic, the inventory index has risen sharply, but with the recovery of the retail end, the inventory coefficient has fallen rapidly, and the overall operation of each month in 2021 is within the safe range, and the inventory coefficient in December is 1.43. Maintaining a low inventory factor shows to some extent that the production side and the demand side are more compatible in the product field, reducing the risk to automakers and dealers caused by the backlog of finished products.

From the perspective of import and export, since 2018, the export quantity of mainland automobiles and automobile chassis has exceeded the import quantity, and the export quantity has shown a fluctuating growth trend, and the import quantity fluctuation has decreased. In 2021, the cumulative export of mainland automobiles and automobile chassis was 2.12 million units, an increase of 96.30% year-on-year, and the number of imports was 940,000 units, an increase of 1.08% year-on-year. The increase in exports reflects the increased international competitiveness of mainland automakers.

Second, the upstream of the industry

The upstream supporting facilities of the mainland automotive industry are relatively complete, especially in the development of new energy vehicles, power batteries occupy a certain leading position in the world. However, the fluctuation of raw material prices such as steel has increased the cost control pressure of car companies; since the second half of 2020, the lack of global supply of automotive chips has formed a customized contract for the production of major automotive manufacturers; the mainland automotive chips have a high degree of dependence on foreign countries, and there are certain hidden dangers.

The automotive industry has the characteristics of "equal emphasis on materials and workers", and material cost is an important part of its product cost composition. Most of the industries involved in the upstream of the traditional automobile industry, such as steel, rubber, machinery manufacturing, instrumentation and electronic components, are relatively mature, with a high degree of marketization and sufficient production capacity, which is conducive to ensuring the supply of raw materials for the automotive industry. However, the fluctuation of raw material prices such as steel is an important factor affecting the production cost of automobiles; at the same time, in recent years, with the rise of new energy vehicles and the development of intelligent automotive products, power batteries have become an important upstream industry in the automotive industry, and the chip industry in electronic components has an increased impact on the automotive industry.

1. Steel

The production of complete vehicles and parts requires the use of cold-rolled plates, hot-rolled plates, electro-galvanized sheets and hot-dip galvanized sheets. The fluctuation of steel prices has a certain impact on the profit margins of automobile companies. The overall overcapacity of the mainland steel industry, but in recent years, the national supply-side reform, the international market iron ore and other commodity price fluctuations, etc., the overall rise in steel prices has formed a certain boost, from the beginning of 2020 to the end of 2021, steel prices as a whole showed a fluctuating upward situation.

In the first half of 2020, due to the impact of the new crown pneumonia epidemic on downstream production, steel prices fell significantly; with the gradual recovery of economic operation, steel prices continued to rise in May and December, especially in November and December. Since 2021, steel prices have shown a trend of first rising and then falling, fluctuating sharply, and the overall situation is at a historical high. Specifically, in the first quarter of 2021, affected by inflation expectations and rising costs, steel prices opened an upward trend; in the second quarter, Hebei and other places environmental protection production restrictions, superimposed downstream steel demand and speculative demand, tight supply and demand to promote steel prices to continue to rise, and rose to a historical high in May; since then, with the introduction of a series of regulatory policies and downstream demand slowdown, steel prices have declined, but the rapid rise in raw material coke prices has formed a certain support for steel prices; from October to the end of December, Coke prices have dropped significantly under government intervention, while the demand for superimposed steel has declined, and steel prices have fallen sharply, but they are still higher than the same period last year.

Overall, in 2021, the overall operating range of steel prices is at a high level in recent years, which is not conducive to the cost control of vehicle companies.

2. Power battery

The power battery industry provides important components for new energy vehicles and has become an important upstream industry for automobile supply in recent years. In 2019-2020, due to the decline of subsidy policies and the impact of the new crown pneumonia epidemic on the new energy vehicle market, the increase in the installed volume of continental power batteries was small; in 2021, the production and sales of continental power batteries increased significantly, and the annual power battery loading volume reached 154.5GWh, an increase of 142.9% year-on-year, which played an important role in supporting the explosive growth of the new energy automobile industry.

After years of development, the mainland power battery industry has occupied a leading position in the world, according to SNE Research statistics in the first three quarters of 2021 data, the global power battery loading volume, the top 10 companies accounted for about 93.6%, while Chinese companies accounted for 5 of them (NINGDE Times, BYD, Zhongxin Airlines, Guoxuan Hi-Tech and Envision AESC), the total global market share of the 5 companies is about 45.9%.

In 2021, the loading volume of power batteries in the mainland will increase significantly, and from the production side, in addition to the production lines of major battery companies and the release of production capacity, the changes in the installed structure of batteries are also important influencing factors. Due to the limitation of energy density, in 2018-2020, the mainland lithium iron phosphate battery has been marginalized, but due to bydd and other manufacturers to achieve breakthroughs in product technology, in 2021, the output of lithium iron phosphate batteries in the mainland increased by about 2.63 times year-on-year, accounting for the proportion of total power battery output rose to 57.1%, making the overall capacity utilization rate of the industry increase, and to a certain extent weakening the negative impact of the rise in cobalt prices on the entire industrial chain; the new energy vehicle mileage equipped with new lithium iron phosphate batteries increased. Sales performance is good, and technological progress has made the power lithium battery and the new energy automobile industry form a benign interaction situation.

In terms of production capacity, power batteries are emerging industries, due to the limitations of industry production capacity, industrial chain supporting factors, etc., the overall supply is in short supply at this stage. However, in the face of the continuous high prosperity of the new energy industry, the giants of the power battery industry are actively laying out production capacity. According to the relevant public information of CATL Times, China Innovation Airlines and Guoxuan Hi-Tech, before 2025, The battery production capacity of CATL is expected to reach 670GWh (its lithium-ion battery production capacity from January to September 2021 is 106.4GWh, and the lithium-ion battery production line that has been completed and put into operation has a total designed annual capacity of about 220GWh to 240GWh after completing the ramp-up of production capacity and stable operation); The production capacity of China Innovation Airlines is planned to be 200GWh in 2022 and 500GWh in 2025; and the production capacity target of Guoxuan Hi-Tech in 2025 is 300GWh (about 50GWh in 2021). In addition to the above-mentioned companies, BYD, Hive Energy, Volkswagen Group (China) and other companies are also implementing large-scale production capacity construction plans. The investment of power batteries and related industry leaders in battery production capacity and technology research and development will provide strong support for the development of the new energy automobile industry, but the scale of investment in related projects is large, and attention should be paid to the continuation of follow-up funds.

3. Automotive chips

With the application of various automation functions in automotive products, a wide variety of chips have long become important electronic components required for automobile production, especially in recent years, in the process of accelerating the development of "electric + intelligent", the demand for chips in the automotive industry has grown rapidly. However, at the same time, due to the impact of the new crown pneumonia epidemic on the normal start of some chip companies, some fabs have suffered accidents, coupled with the inaccurate forecast of demand forecasts by chip manufacturers after the change in the producer pattern in the automobile industry, as well as market speculation, hoarding and other factors, since the second half of 2020, the lack of global automotive chip supply has become prominent, and there has been a sharp rise in the price of automotive chips and the extension of the delivery cycle.

In terms of price, since the second half of 2020, the price of some chips has risen by more than 10 times; in terms of delivery cycle, according to the research report of the market analysis agency Susquehanna Financial Group, the normal delivery cycle of chip manufacturers in general years is mostly between 10 and 15 weeks, and from the second half of 2020, the delivery time of chip manufacturers has gradually lengthened, and 2021 is significantly longer than the normal year, and it is about 25 weeks by the end of the year.

Due to the small proportion of chips in the production cost of automobiles, the impact of rising chip prices on the automobile industry is still controllable, but due to the shortage of chips, most automobile manufacturers at home and abroad have been forced to reduce production in stages. From April to August 2021, mainland automobile production continued to decline month-on-month. Due to the national crackdown on market speculation and the gradual arrival of pre-orders, from September 2021, the supply of chips has eased slightly, and the output of mainland automobiles has increased month-on-month, but it still cannot fully meet the market demand. In the second half of 2021, Mainland China's automobile production was 13.513 million units, down 10.59% year-on-year, and inventory at the end of the year fell to 845,000 units from 1.019 million units at the end of the previous year.

At present, the dependence of mainland automotive chip products is very high (more than 95% need to be imported), in response to this phenomenon, the Ministry of Science and Technology, the Ministry of Industry and Information Technology, etc. have led more than 70 units to establish the "China Automotive Chip Industry Innovation Strategic Alliance" to establish an innovation ecology of China's automotive chip industry and make up for the shortcomings of the industry.

Third, the demand analysis

1. Passenger car market

Passenger cars are mainly for individual consumers, in recent years, SUVs and high-end car demand preferences have been fully reflected, and with the change of consumer group structure, the market recognition of new energy vehicles that can carry the "smart + network" function has increased rapidly. Mainland independent brand manufacturers have gained advantages in the field of SUVs and new energy vehicles, narrowing the gap with joint ventures.

From the model situation, in recent years, with the improvement of residents' living conditions, consumers have a demand for the improvement of automobile products, the target model of car purchase is gradually moving closer to large-scale and high-end, SUVs can meet the large space preferences of mainland consumers, in recent years, the proportion of passenger cars has increased year by year, SUV accounted for only 18.33% in 2013, and the proportion has increased to 47.89% in 2021. With the increase in demand for SUVs, major car companies have increased their efforts to launch SUVs, and some domestic brands have significantly improved their market competitiveness by launching cost-effective SUV products (such as the Great Wall Haval series and WEY series).

From the perspective of power sources, from 2016 to 2020, the penetration rate of new energy vehicles in the mainland has increased year by year, and in 2021, the proportion of new energy vehicle sales in total vehicle sales has increased to 13.40%, an increase of 8.00 percentage points compared with 2020. After years of development, the domestic new energy automobile industry has formed a relatively complete industrial chain, because the products can better carry the "intelligent, networked" function, more able to meet the needs of young consumer groups, new energy vehicles have become an important force to help mainland independent brand car companies "lane change and overtake".

Driven by the innovation of SUVs and new energy vehicle products, the consumer demand for domestic brand cars in the automobile market has increased significantly in recent years: in 2020 and 2021, the market share of independent automobile brands was 43.66% and 46.94%, respectively, an increase of 1.66 percentage points and 3.28 percentage points year-on-year.

In the future, with the improvement of residents' living standards, the demand for automobiles will show a diversified trend. "Post-80s" and "post-90s" have become the main group of car buyers, the young group's purchase decision-making behavior shallow characteristics are obvious, the decision-making cycle is shortened, and more attention is paid to the appearance of modeling, high-tech configuration and fun experience; in addition, with the increase of female car buyers, creating models that are more in line with women's aesthetic and use needs has also become the growth point of car companies. From the supply side, many intelligent electric vehicle models of many car companies have been listed, forming a situation in which independent brands are leading and foreign car companies are gradually keeping up, and market competition is becoming increasingly fierce. The intelligent configuration of car companies represented by Tesla and new forces has introduced new ones, built product selling points and brand elements with "intelligence", and quickly occupied consumer cognition in the new energy market. From the demand side, consumer choices are becoming more and more abundant, the concept of intelligent driving is becoming more and more deeply rooted in the minds of end consumers, and the richness and completion of intelligent functions have become an important reference factor for car purchases.

The goal of the development of new energy vehicles in the mainland's "New Energy Vehicle Industry Development Plan (2021-2035)" is that by 2025, the sales volume of new energy vehicles will account for 20% of the total sales of new vehicles. Judging from the new situation and market response of new energy vehicles in 2021, this goal is expected to be achieved ahead of schedule in 2022. In the future, the automotive market is expected to show low-speed growth and cyclical fluctuations in the total number of automobile purchases, while the demand for new energy vehicles continues to rise.

2. Commercial vehicle market

(1) Truck market

As a production tool, the purchase demand for trucks in mainland China is greatly correlated with the scale of infrastructure investment, the total amount of social logistics and the vehicle renewal cycle. Recently, the mainland's active fiscal policy and large scale of infrastructure investment are conducive to the stability of heavy truck sales; the development of the logistics industry, the implementation of policies such as road supervision is expected to maintain growth in the purchase demand for light trucks.

In recent years, heavy trucks (heavy trucks) and light trucks (light trucks) have been the main varieties of the mainland truck market. In 2021, due to the wait-and-see caused by the Ministry of Industry and Information Technology's deliberations on adjusting the light truck management policy, as well as the early overdraft of heavy truck sales in the previous year, mainland truck sales decreased by 8.5% year-on-year to 4.288 million units, of which heavy-duty truck sales decreased by 13.8% year-on-year to 1.395 million units, but still increased by 18.8% compared with 2019; light truck sales decreased by 4.0% year-on-year to 2.110 million units, an increase of 12.0% over 2019; medium-sized and mini truck sales accounted for a small proportion, which had little impact on the industry as a whole.

The demand for heavy trucks mainly depends on the scale of infrastructure investment and vehicle renewal in the mainland, which has a strong cyclicality. In 2020, due to the acceleration of the National III emission standard trucks and the imminent implementation of the China VI emission standard, the sales volume of heavy-duty trucks in the mainland hit a record high (1.623 million units), and under the circumstance of early sales overdraft in the previous year, the sales of heavy trucks in the mainland in 2021 were 1.395 million units, which is still a historical high level. In the fourth quarter of 2021, the mainland's GDP growth rate has dropped to 4%, in the case of increasing downward pressure on the economy, the mainland's fiscal policy is expected to be more active in 2022, and the construction of infrastructure and affordable housing is expected to accelerate, which is conducive to the stability of heavy truck sales.

In terms of light trucks, in recent years, the sales of light trucks in the mainland have been better, mainly due to the development of e-commerce, live streaming and community group buying, which has boosted logistics demand. In the future, with the improvement of people's living standards, the demand for fresh agricultural products in society will grow steadily, the development of fresh e-commerce has put forward higher requirements for the quality and timeliness of transportation, and the demand for light trucks in the logistics industry is expected to further increase; at the same time, the implementation of the policy of light trucks and the gradual upgrading of emission standards will also stimulate the sales of light trucks. In the next 3 to 5 years, the demand for light trucks in mainland China is expected to maintain growth.

(2) Bus market

Affected by the expansion of the rail transit coverage network and other factors, the mainland bus market is facing greater pressure, in recent years in a state of saturation, the future market demand mainly depends on the policy to promote the electrification of public sector vehicles, third- and fourth-tier cities public transport, growth prospects still need to wait and see.

Mainland bus sales peaked in 2014 due to the expansion of the coverage of the high-speed rail network and the increase in the mileage of urban subways on the highway and urban passenger transport industry. After six consecutive years of decline, in 2021, the mainland bus market picked up, with annual sales of 505,000 units, an increase of 12.6% year-on-year and 7.2% over 2019.

From the perspective of subdivided models, in 2021, the sales volume of large buses in the mainland decreased by 15.4% year-on-year to 48,000 units, accounting for 3.2 percentage points to 9.5% compared with the previous year; the sales volume of medium-sized buses was 3.1% to 46,000 units lower than that of the previous year, and the sales volume of light buses decreased by 1.4 percentage points to 9.1% compared with the previous year; the sales volume of light buses increased by 19.4% year-on-year to 411,000 units, and the sales volume accounted for 4.6 percentage points higher than that of the previous year to 81.4%. In recent years, the demand for mainland buses has tended to be lightweight, and the trend of declining the proportion of large and medium-sized buses and rising proportion of light buses is still continuing.

From the perspective of total market demand, the mainland bus market will continue to bear the pressure of the expansion of rail transit coverage and the popularity of family cars and online ride-hailing in the future, and the future market will mainly rely on the support of renewal demand.

Under the current technical conditions, buses are more suitable for electrification than passenger cars and trucks. Mainland China's "New Energy Vehicle Industry Development Plan (2021-2035)" proposes that by 2035, public domain vehicles should be fully electrified, and from 2021, the national ecological civilization pilot zone and key areas of air pollution prevention and control of public domain vehicles will be updated, and the proportion of new energy vehicles will not be less than 80%. In addition, during the "13th Five-Year Plan" period, many local governments have introduced new energy bus renewal plans, the electrification of public transport vehicles in Shenzhen, Beijing, Shanghai and Guangzhou has been basically completed, and the electrification of public transport in third- and fourth-tier cities is accelerating. During the "14th Five-Year Plan" period, the new energy replacement of public vehicles will form a certain support for the bus market; and the electrification of buses in third- and fourth-tier cities will, to a certain extent, increase the demand for medium and large buses.

Fourth, the analysis of policy trends and their impact

1. The central government and relevant ministries and commissions have repeatedly issued policies or made statements to stabilize and expand automobile consumption

On January 5, 2021, the Ministry of Commerce and 12 other departments jointly issued the "Notice on Several Measures to Promote the Release of Rural Consumption Potential by Boosting Key Consumption of Bulk Consumption", which requires the release of automobile consumption potential, encourages relevant cities to optimize purchase restriction measures, and increases the number plate indicators; carries out a new round of cars going to the countryside and replacing old with new, encourages qualified areas to purchase passenger cars with a displacement of 3.5 tons and below, 1.6 liters and below, and subsidizes residents to eliminate National III and below emission standard cars and buy new cars. On March 5, 2021, Premier Li Keqiang of the State Council proposed in the "Government Work Report" that "we must continue to stabilize and expand consumption" and "steadily increase bulk consumption such as automobiles and home appliances". On July 30, 2021, the meeting of the Politburo of the Central Committee clearly proposed to tap the potential of the domestic market and support the accelerated development of new energy vehicles. On August 20, 2021, the relevant person in charge of the Ministry of Industry and Information Technology said that the Ministry of Industry and Information Technology will promote the cancellation of car purchase restrictions in various places, encourage local governments to introduce more preferential policies for real money and silver, and promote the transformation of automobiles from purchase management to use management.

Comments: The development of the automobile industry has a huge impact on the national economy. Due to the consumption capacity of residents and the effect of population agglomeration, the current important market for mainland automobile sales is still mainly concentrated in cities, while some large and medium-sized cities have implemented automobile purchase restriction policies in recent years due to the limited carrying capacity of road traffic, forming a customized contract for automobile consumption. Since 2021, many central ministries and commissions, the State Council and even the Political Bureau of the Central Committee have issued relevant policies or put forward guiding suggestions, which will help stimulate the demand for automobiles in rural and small and medium-sized cities, and promote the adjustment of purchase restriction policies (especially for new energy vehicles) in some qualified large and medium-sized cities, thereby promoting the recovery of the automobile market.

2. The joint venture share ratio of passenger car companies has been fully liberalized

On 27 December 2021, the National Development and Reform Commission and the Ministry of Commerce (MOFCOM) issued the Special Administrative Measures for Foreign Investment Access (Negative List) (2021 Edition), which, from 1 January 2022, will abolish the restriction on foreign ownership in passenger car manufacturing and the restriction that "the same foreign investor can establish two or less joint ventures in China to produce similar vehicle products".

Comments: The liberalization of the joint venture share ratio of automobile enterprises has experienced a transition period of nearly 4 years. Due to the strong brand premium ability of the joint venture car companies and the large sales volume of the whole vehicle, until the first three quarters of 2021, the investment in the joint venture is still an important source of profit for many large state-owned automobile groups in the mainland, and if the shareholding ratio of the relevant state-owned enterprises in the joint venture is diluted, it will lead to a decline in their profits; in addition, the market is also worried that after the full liberalization of investment, the independent brand cars will be more directly impacted.

However, since the second half of 2020, the transformation of the global automotive industry has accelerated, the penetration rate of new energy vehicles in the mainland automobile market has increased rapidly, and local enterprises have achieved certain competitive advantages in the new energy vehicle market. At the same time, after years of cooperation, some joint ventures have formed a situation of "foreign-led technology and products, Chinese-led product localization and marketing", especially in cooperation with local governments and understanding of market demand, joint ventures often need the support of Chinese shareholders. As of the end of 2021, except for BMW Brilliance, major joint ventures have not yet announced the news that foreign shareholders have requested to increase their shareholding ratio. Whether the foreign shareholders increase the shareholding ratio and the specific increase, there is a certain "game" and "balance" space. Overall, the impact of the liberalization of the foreign equity ratio on the mainland automobile industry and the impact on the shareholders of the relevant Chinese participation (control) shares will be lower than expected.

3. The "big stick" of the "double points" policy is further approaching

In June 2021, the Ministry of Industry and Information Technology announced the annual report on the average fuel consumption of passenger car enterprises and the implementation of new energy vehicle credits in 2020. According to the public data, in 2020, the positive integral of domestic new energy vehicles was 4.37 million points and the negative integral was 1.0655 million points; the positive integral of average fuel consumption was 4.3674 million points, and the negative integral was 11.7143 million points. Among the 137 passenger car manufacturers/importers, 93 companies did not meet the average fuel consumption standards; the non-compliant enterprises included FAW-Volkswagen Co., Ltd., SAIC-General Automobile Co., Ltd., Zhejiang Haoqing Automobile Manufacturing Co., Ltd., SAIC Volkswagen Co., Ltd., Zhejiang Geely Automobile Co., Ltd., Chongqing Changan Automobile Co., Ltd., Beijing Benz Automobile Co., Ltd., China FAW Group Co., Ltd., Chery Automobile Co., Ltd. and Dongfeng Motor Co., Ltd.

Comments: As of the end of 2021, the "Measures for the Parallel Management of Average Fuel Consumption of Passenger Car Enterprises and New Energy Vehicle Credits" (hereinafter referred to as the "Double Credit Policy") has been in effect for 4 years, and the Ministry of Industry and Information Technology has announced the results of the "Double Integral" assessment of passenger car enterprises five times. According to the "double point policy", if the car company does not meet the point requirements, it will be subject to penalties such as suspension of the declaration and production of high fuel consumption products; before the negative points are offset, its fuel consumption products that do not meet the standards will not be included in the model announcement.

Up to now, the Ministry of Industry and Information Technology has not taken punitive measures against enterprises that do not meet the points standard, and the "policy stick" has not been dropped, but the vast majority of traditional car companies have felt great pressure. In 2020, FAW-Volkswagen and other traditional vehicle companies have accumulated more negative points, and the positive points generated by the mainland passenger car industry are much lower than the negative points, and the shortage of positive points will raise the price of points, forcing traditional car companies to develop and produce new energy models, and promote the development of the domestic new energy vehicle market.

4. The State Council, the Ministry of Industry and Information Technology, the National Development and Reform Commission and other departments support the construction of supporting systems such as charging, power exchange, and waste battery utilization of new energy vehicles

On March 5, 2021, Premier Li Keqiang proposed in the "Government Work Report" to "increase parking lots, charging piles, substations and other facilities to accelerate the construction of a power battery recycling system"; on May 20, 2021, the National Development and Reform Commission and the Energy Administration issued the "Implementation Opinions on Further Improving the Service Guarantee Capacity of Charging and Swapping Infrastructure (Draft for Comments)", indicating that it is necessary to accelerate the construction and installation of charging facilities in residential communities and improve the charging and replacement guarantee capabilities in urban and rural areas. Strengthen the research and development and application of new technologies such as vehicle network interaction, strengthen the operation and maintenance of charging and replacing facilities and network services, do a good job in supporting power grid construction and power supply services, strengthen quality and safety supervision, and increase fiscal and taxation financial support; on October 28, 2021, the Ministry of Industry and Information Technology issued the "Notice on Launching the Pilot Work on the Application of new Energy Vehicle Power Exchange Mode", and decided to start the pilot work of the application of new energy vehicle power exchange mode, including 11 cities including Beijing, Chongqing, Nanjing and Wuhan.

On July 7, 2021, the National Development and Reform Commission issued the "14th Five-Year Plan for the Development of circular economy", which clarified 11 key projects and actions, including the construction of urban waste material recycling system, the recycling and quality improvement of waste electricity products and the recycling of waste power batteries. On August 19, 2021, the Ministry of Industry and Information Technology and the Ministry of Ecology and Environment and other five ministries and commissions jointly issued the "Administrative Measures for the Cascade Utilization of New Energy Vehicle Power Batteries", encouraging cascade utilization enterprises to cooperate with enterprises such as new energy vehicle production, power battery production and scrapped motor vehicle recycling and dismantling, strengthen information sharing, use existing recycling channels, efficiently recycle waste power batteries for cascade utilization, and encourage power battery manufacturers to participate in waste power battery recycling and cascade utilization.

Comments: Insufficient charging equipment is one of the important factors restricting the development of new energy vehicles, the State Council has listed the construction of charging piles as one of the "new infrastructure" projects, the premier mentioned the construction of charging and replacing facilities in the government work report for 2 consecutive years, the Development and Reform Commission, the Ministry of Industry and Information Technology and other departments have also carried out corresponding policy follow-up, and the relevant policies have been gradually reflected in local planning. The problem of insufficient total number of charging facilities and unreasonable distribution is expected to be gradually solved.

Continental power batteries have entered a centralized end-of-life period, and the amount of decommissioning is expected to reach about 116GWh (about 800,000 tons) by 2025. Waste power lithium batteries have great harm to the environment, but also have great resource utilization value, but mainland vehicle power lithium batteries do not have a national recycling network. Power battery recycling and cascade utilization can maximize the use value of decommissioned power batteries and reduce the environmental pollution of heavy metals. Only by establishing a sound power battery recycling system can the mainland new energy automobile industry become a truly green industry and go far.

5. The new regulations of "blue card light truck" landed

On January 12, 2022, five months after soliciting comments, the Ministry of Industry and Information Technology and the Ministry of Public Security jointly issued the Notice on Further Strengthening the Production and Registration Management of Light Trucks and Small and Micro Passenger Vehicles (hereinafter referred to as the "Notice"), and issued relevant technical specifications. The Notice regulates and unifies a number of indicators registered as light trucks, requiring that products in production that do not meet the technical specifications should stop production from March 1, 2022, and proposing that manufacturers who violate the rules should bear criminal liability.

Comments: "Blue card light card" refers to trucks that can use white number plates (blue cards) on a blue background, and its biggest advantage over "yellow card" cars is that they have the right of way to the central urban area. In 2019, in order to activate the vitality of urban distribution, the Ministry of Transport cancelled the relevant qualification requirements and significantly lowered the entry threshold for the operation of blue-brand light trucks. However, due to the fact that the production and manufacture of light trucks in the mainland and market access management, registration and right-of-way management, operation management belong to different departments, different departments according to different standards, there has been a phenomenon of some products being on the blue card and "large tons and small standards", and some commercial vehicle companies even take overload capacity (actual carrying capacity exceeds the nominal carrying capacity) as the competitiveness of products, which has adversely affected the order of the freight market and road traffic safety. The "Notice" and related technical specifications make specific provisions on a number of technical indicators for light trucks, and are jointly issued by the Ministry of Industry and Information Technology and the Ministry of Public Security, which will help regulate light truck products, prevent unfair competition, and reduce the risk of production enterprises; at the same time, the new regulations reduce the single vehicle capacity of compliant products, which will bring about an increase in the demand for light truck purchases.

V. Credit status of enterprises in the industry

Due to the capital-intensive characteristics of the industry, the credit rating of the issuers of existing bonds in the automobile manufacturing industry is generally higher. In 2021, there was no bond default or deferral in the automobile manufacturing industry, and the credit rating of the main body of one enterprise was downgraded; the scale of newly issued bonds was small and the coupon rate was low; the scale of existing bonds and the repayment pressure of bonds due within one year were small.

1. Changes in the credit rating of bond-issuing enterprises in the industry

In 2021, one of the issuers of existing bonds in the automotive manufacturing industry [1] (Chongqing Xiaokang Industrial Group Co., Ltd.) was downgraded (from AA to AA-, with a stable outlook).

By the end of 2021, among the existing bond issuers in the automobile manufacturing industry, there are 15 enterprises with effective entity credit ratings, and from the perspective of the distribution of credit ratings of entities, there are 11 enterprises with AAA credit ratings, 3 AA+ enterprises, and 1 AA-enterprise. At present, the overall credit rating of bond-issuing enterprises in the automobile manufacturing industry is relatively high, which is mainly determined by the capital-intensive characteristics of the industry, and is also the result of the elimination of some weak enterprises in market competition in recent years.

2. Redemption of bonds due to enterprises in the industry

In 2021, in the automobile manufacturing industry, a total of 10 companies' 25-issue bonds were redeemed/resold at maturity (excluding ultra-short-term financing bonds issued and matured in the current year), with a total principal amount of 31.085 billion yuan, and there was no default or delay in payment. The details are shown in the following table.

3. Bond issuance and current existing bonds of enterprises in the industry in 2021

In 2021, a total of 3 of the existing bond issuers in the automobile manufacturing industry issued 5 bonds (excluding the ultra-short-term financing bonds that have been redeemed in the current period), with a total issuance scale of 10 billion yuan. Since the issuer and the credit rating of the bonds are both AAA, the highest interest rate of the issuance is 3.97%, which is at a low level.

By the end of 2021, there will be 15 existing bond issuers in the automobile manufacturing industry, with a total of 71 existing bonds, and the total bond balance will be 116.148 billion yuan. Among the 15 issuers, the bond balances of Beijing New Energy Automobile Co., Ltd. and Beijing Automotive Group Co., Ltd. are equivalent to 57.45% and 27.06% of their net assets at the end of 2020, respectively, and the balance of existing bonds of the remaining 13 issuers is below 15% of the net assets at the end of 2020. Compared with the larger net assets, the overall bond repayment pressure of the automobile manufacturing industry is not large.

As of the end of 2021, among the existing bonds in the automobile manufacturing industry, the principal amount of bonds that mature before the end of 2022 (or face the option of resale) is 48.467 billion yuan, and the pressure of centralized bond repayment in the next year is not large.

Fifth, the financial performance of bond-issuing enterprises

In this paper, based on the arithmetic average of the financial indicators of the sample enterprises, United Credit analyzes the changes in the financial indicators of bond issuers in the industry since 2020.

According to wind data, as of the end of 2021, there are 15 existing bond issuers in mainland automobile manufacturing enterprises (see Table 3 for details), because beijing new energy automobile co., ltd. has fluctuated too much since 2020, and United Credit has not included it in the sample; among the remaining 14 companies, because Dongfeng Motor Group Co., Ltd. has not released the third quarter report of 2021, United Credit is in the analysis of the data of bond issuers from January to September 2021 and the end of September 2021. It was excluded (the relevant data compared to it also used 13 samples).

1. Asset composition

Since 2020, the total assets of bond-issuing enterprises in the automobile manufacturing industry have maintained growth, and the scale of assets has been large; the proportion of monetary funds is relatively high, the control of accounts receivable is better, and non-current assets such as long-term equity investment and fixed assets have not changed much.

In 2020, the decline in mainland automobile production and sales narrowed, the market picked up in an all-round way in the second half of the year, and the sample enterprises increased their overall asset scale through profit accumulation and debt increase. By the end of 2020, the average total assets of the sample enterprises increased by 10.46% over the end of the previous year. From the perspective of several key subjects, the average value of monetary funds increased by 16.81% and the proportion increased by 0.87 percentage points, mainly due to the relatively strong market enterprises in the industrial chain, and the sales settlement method was beneficial to itself; correspondingly, the average increase in accounts receivable was very small, and the proportion fell by 0.42 percentage points. Inventory increased by 14.93%, mainly due to the increase in raw material prices, the increase in orders in the second half of the year, and the increase in stockpiling of sample enterprises. The average value of fixed assets increased by 5.14%, which was related to the upgrading of production lines of sample enterprises and investment in new energy vehicle-related projects; the proportion of fixed assets decreased slightly.

As of the end of September 2021, the average total assets of the sample enterprises increased by 3.89% from the beginning of the year to 269.626 billion yuan, and the average asset size was very large. Among them, the average value of accounts receivable increased by 9.71% compared with the beginning of the year, which was lower than the increase in income scale (see Table 5), which was basically reasonable; monetary funds increased by 5.92% compared with the beginning of the year, accounting for 16.35%, indicating that the liquidity of sample enterprises continued to improve.

2. Profitability

Since 2020, the investment income of bond-issuing enterprises in the automobile manufacturing industry has been basically stable; the expansion of income scale and the enhancement of the profitability of the main business have driven the growth of profits.

There are many Sino-foreign joint ventures or joint ventures in the mainland automotive industry, and for many years, investment income has been an important source of profits for several large automobile groups; in 2020, the overall change in the investment income of sample enterprises is very small.

In terms of main business, in 2020, mainland automobile sales have decreased, but the proportion of sales of medium and high-priced models has increased, and the average sales revenue of sample enterprises has increased by 2.99% year-on-year; from the perspective of the "adjusted operating profit margin" that reflects the profitability of the main business of the enterprise, the average value of this indicator has declined in 2020, mainly due to the decline in the indicator of individual smaller operating scale enterprises (such as Xiaokang shares) in the sample enterprises, and the adjusted operating profit margin of other enterprises has generally improved. In 2020, the total profit of the sample enterprises increased slightly year-on-year, mainly from the contribution of the main business.

In the first three quarters of 2021, although the mainland automotive industry is facing strong market demand, production is constrained by factors such as "lack of core". Under the influence of the above factors, the average sales revenue and total profit of the sample enterprises increased by 12.04% and 16.06% respectively year-on-year.

3. Capital structure and debt servicing indicators

The scale of the owner's equity of the automobile manufacturing enterprise is large, the overall debt burden is at a reasonable level, and the profits and cash flows obtained from continuous operation and investment have a strong ability to cover the debt.

As of the end of 2020, the average equity of the owners of the sample enterprises increased by 7.54% from the end of the previous year, and the average value of all debt increased by 14.84% from the end of the previous year, affected by the average debt capitalization ratio of all debt increased by 1.57 percentage points. In 2020, the short-term debt growth rate of the sample enterprises was less than the increase in all debt, indicating that the maturity structure of the new debt was more reasonable.

In 2020, the average of the "(Net Cash Flow from Operating Activities + Cash Receipts from Investment Income)/Short-term Debt" indicator of the sample enterprises was raised to 0.69 (times) and the average value of the "EBITDA/Total Debt" indicator was increased to 0.56 (times), reflecting the overall strong ability of the sample enterprises to cover the debt by operating, investment profits and cash flows.

As of the end of September 2021, the average equity of the owners of the sample enterprises increased by 10.32% from the end of the previous year to 104.275 billion yuan, which is a large scale; the average value of all debt increased by 4.01% over the end of the previous year, the average of the total debt capitalization ratio decreased slightly to 35.41%, and the overall debt burden was in a reasonable range.

Seventh, the industry outlook view

The mainland automobile manufacturing industry will show the characteristics of medium and low speed growth and cyclical fluctuations for a long time. In the short term, due to the unmet part of the purchase demand in 2021, the industry is more likely to continue to grow in 2022; the penetration rate of new energy vehicles in the passenger car field will still increase rapidly, the heavy trucks in the commercial vehicle field are expected to remain basically stable, there is a certain growth space for light trucks, and the prospect of the bus market is uncertain. In the medium and long term, on the one hand, the reduction in demand growth will intensify the competition in the industry, and the living environment of weak enterprises will continue to deteriorate; on the other hand, the industry as a whole still has some room for development, and the possibility of downward prosperity for several consecutive years in the future is small, from a long-term cycle perspective, the industry as a whole is expected to operate stably, which is conducive to the credit level of most existing bond issuers to remain basically stable.

At present, the demand for automotive products in the mainland market has entered a period of low- and medium-speed growth, and the operation of the automotive industry mainly shows the characteristics of cyclical fluctuations. Since the second half of 2020, the mainland automobile market has entered an upward cycle, but due to the short-term impact of chips and other factors, the growth of automobile production and sales in 2021 is not significant, and there are still some consumer demand that has not been met, leaving a certain space for sales growth in 2022.

In terms of passenger cars, the Chinese base is large, there is still a certain gap between the automobile penetration rate and developed countries, the future urbanization, the improvement of residents' income levels, and the stimulation of the demand for renewal of rich new energy vehicle products will help the mainland automobile consumption to remain stable for a long time; after years of policy guidance, the mainland new energy passenger cars have entered the outbreak period, the improvement of product strength makes it more able to meet the needs of new consumer groups, and the penetration rate will continue to increase rapidly in the next few years. Mainland independent brands have achieved a certain first-mover advantage in the field of new energy vehicles, and the increase in the penetration rate of new energy vehicles will benefit local auto companies even more.

In terms of commercial vehicles, the purchase demand for trucks is greatly correlated with the scale of infrastructure investment and the total amount of social logistics. At present, the downward pressure on the mainland economy is large, and the state has launched a proactive fiscal policy and expanded the scale of infrastructure investment, which is conducive to the stability of heavy truck sales in 2022; while the development of the logistics industry, road supervision and upgrading of emission standards and other policies are expected to continue to grow the demand for light truck purchases. The mainland bus market is affected by factors such as the expansion of the rail transit coverage network, and in recent years, it is facing great pressure and is in a saturated state, and the future market demand mainly depends on the electrification of public sector vehicles and public transportation in third- and fourth-tier cities driven by policies, and the market situation remains to be seen.

As a capital-intensive industry, the automobile manufacturing industry has a high concentration. After the survival of the fittest since 2018, most of the bond issuers in the industry are currently head enterprises, with significant scale advantages, good overall financial performance, and generally higher credit ratings. Looking forward to the future, on the one hand, because the total demand for mainland automobiles has left the high growth stage, the future industry competition will be more intense, if there are problems in product development, supply chain management and other aspects, enterprises will face the situation of being eliminated by the market, weak capital strength, poor R & D and supply chain management capabilities, the living environment will continue to deteriorate. On the other hand, the mainland automobile market still has some room for development, although there will be cyclical fluctuations in the future, but the possibility of declining the prosperity for several consecutive years is small; from a long-term perspective, the industry as a whole is expected to operate stably, which is conducive to the basic stability of the operating conditions and credit levels of most of the surviving bond issuers.

[1] refers to enterprises whose main business is the manufacture and sale of gasoline, diesel and new energy vehicles, and more than 50% of the total operating income or profit comes from automobile manufacturing business.

[2] The change in absolute quantity refers to the proportion of the difference between the two sides of the comparison, and the change of the relative index refers to the difference between the two sides of the comparison that directly subtracts; the same is the same below.