(Report Producer/Author: CITIC Construction Investment Securities, Zhu Yue)

First, review 2021: high-quality products drive high growth, new car listing to open up the sinking market

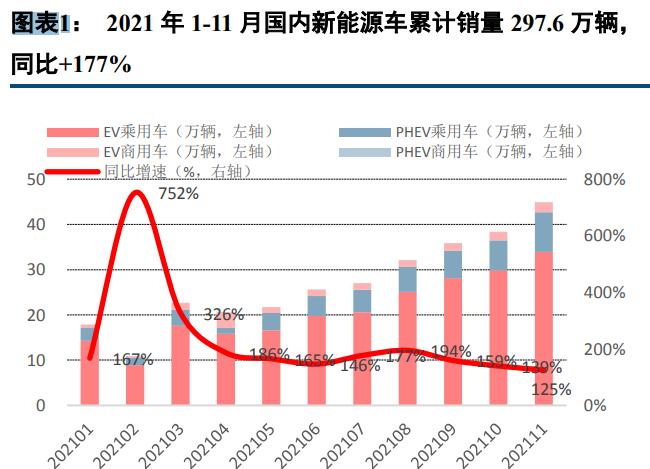

1.1, domestic: the demand for new energy vehicles has exploded, and the annual sales volume is expected to reach 3.48 million

According to the China Automobile Association, the cumulative sales of new energy vehicles in China from January to November 2021 were 2.976 million units, +177% year-on-year; of which the cumulative sales of new energy passenger vehicles were 2.825 million units, +189% year-on-year; and the sales of commercial vehicles were 152,000 units, an increase of 55% year-on-year.

In November, the domestic new energy vehicle sales were 450,000 units, and the penetration rate rose to 17.8%, of which the new energy passenger car sales were 427,000 units, the penetration rate was 19%, the commercial vehicle sales were 23,000 units, the penetration rate was 7%; the penetration rate of new energy vehicles in January to November was 12.7%, +7.9pct year-on-year, of which the passenger car penetration rate was 14.8%, +9.3pct, the commercial vehicle penetration rate was 3.4%, year-on-year +1.2pct; it is expected that the sales of new energy vehicles in December will be 505,000 units. Of these, 480,000 units were sold for passenger cars and 25,000 units for commercial vehicles.

It is estimated that domestic new energy vehicle sales will be 3.481 million units in 2021, +163% year-on-year. By model, the sales volume of new energy passenger cars was 3.305 million units, the same ratio +175%, commercial vehicles 177,000 units, +48.3% year-on-year; according to the car companies, the top three domestic new energy passenger car sales companies in 2021 were BYD, Tesla, and Shangtong Wuling, and the sales volume is expected to be 61, 49 and 450,000 units, respectively, +231%/+256%/+170% year-on-year.

The domestic Model 3/Model Y has become the main model for export. From January to November 2021, new energy vehicles exported 203,000 units, +175% year-on-year, and the domestic Model 3 and Model Y have become the main models exported. In November, 29,200 new energy passenger cars were exported, of which Model 3/Model Y/MG EZS/MG eHS were 1.75, 0.36, 0.31 and 0.25 million units, respectively.

The emergence of quality models is driving high sales in 2021. From January to November 2021, the top five models in domestic new energy passenger car sales were Wuling Hongguang MINI 345,000 units, Model Y 129,000 units, Model 3 121,000 units, Qin PLUS DM-I 94,000 units, and Han EV 77,000 units, of which Model Y and Qin PLUS DM-i were newly launched in 21 years. In November 2021, the sales of new models in China that year have reached 140,000, accounting for 38% of the sales of new energy passenger cars in that month.

1.1.1 In terms of levels, the proportion of A-class cars has increased significantly, verifying the logic of high-quality products to promote volume

Thanks to the launch of new cars and the sinking of the class, the proportion of A-class cars will increase significantly in 2021. 2021 is the first year of the rise of the domestic mid-end market for new energy vehicles, with cumulative sales of A-class new energy passenger cars reaching 849,000 units from January to November, +159% year-on-year; in November, A-class vehicles accounted for 39.3%, +14.4pct year-on-year.

The launch of new vehicles in the A-segment car market has led to a significant increase in sales. On the one hand, pure electric models have benefited from the launch of high-quality new models such as Xiaopeng P5 and Euler Good Cat; on the other hand, the sales of non-new models have also increased significantly, which reflects that mid-range EV models are gradually being accepted by the market, and the main market for new energy vehicles is gradually exploring from high-end models to mid-range models.

Hybrid model growth is mainly contributed by BYD Qin, Song two DM-i models, with low purchase costs, low fuel consumption, Qin Plus DM-i, Song Plus DM-i gradually seize the fuel vehicle market, November sales of the two models reached 1.81/1.51 million units respectively.

In 2021, the sales growth rate of B/C-class models is significantly lower than that of A-class models, on the one hand, driven by high-quality models such as Model 3 and new forces, the sales of B/C-class models in 2020 have achieved higher growth and a higher base; on the other hand, there are fewer competitive B/C new cars on the market in 2021. According to statistics, the top five B/C class new models in November retail sales were Model Y (23,100 units), NIO EC6 (0.35 million units), WM E5 (0.28 million units), BMW X3 BEV (0.28 million units), ID.6 CROZZ (0.22 million units), model Y contributed to the main increase in the B/C class new model market.

1.1.2 Looking at the city, the sinking market is gradually opening, and the consumption attributes are highlighted

In 2021, the proportion of sales in non-first-tier cities has increased significantly, especially in second- and third-tier cities, the proportion of Q1-Q3 sales has reached 35.8%, +3.3pct year-on-year, and the recognition drive is prominent. As far as B/C-class models are concerned, the sales volume of quasi-first-tier and second-tier cities in 2021Q1-Q3 totaled 52.5%, +13.9pct year-on-year, which is related to the gradual sinking of car company channels such as Tesla and new car-making forces, and the gradual improvement of charging facilities in related cities.

1.2, overseas: product + policy driven sales increased year-on-year, tram penetration rate has repeatedly reached a new high

Overall demand in Europe in 2021 will remain relatively strong and high year-on-year. From January to November 2021, the cumulative sales of new energy vehicles in Europe were 1.795 million units, the same ratio of +75%, of which the penetration rate of eight European countries continued to rise to 27% in November, the annual penetration rate reached 19.5%, and the overall penetration rate in Europe was about 14%. Affected by Tesla's delivery rhythm, it showed a trend of weakening at the beginning of the quarter and increasing at the end of the quarter. The number of registrations in Europe is expected to be 2.05 million in 2021, +61% year-on-year.

Under the influence of the lack of core in the United States, the penetration rate of trams is still increasing rapidly. From January to November 2021, the cumulative sales of new energy vehicles in the United States were 550,000 units, +96% year-on-year, although the growth rate slowed down in the second half of the year due to the lack of cores, but the upward trend of penetration rate did not change, and the penetration rate of AMERICAN trams in November was 5.6%, a record high, and the annual penetration rate reached 3.9%, an increase of 1.7pct over last year. The U.S. is expected to sell 630,000 in 2021, +90% year-on-year.

Product + policy two-wheel drive overseas sales doubled year-on-year. From January to November 2021, a total of 40 new models were listed in Europe, contributing a total of 143,000 sales net increases, accounting for 8% of the market share, of which Tesla Model Y accumulated 22,000 to maintain an absolute lead, SAIC MG HS, Volkswagen CUPRA Formentor, modern IONIQ 5 and Audi Q4 e-tron Cumulative sales exceeded 10,000, contributing a total of 80,000 pure increments. Overall, from January to November, model 3 sales were 109,000 units, a market share of 6%, and Volkswagen ID.3&4 sold a total of 110,000 units, or 6.1%.

From January to November 2021, a total of 18 new models were listed in the United States, contributing a total of 76,000 pure sales increments, with a market share of 14%, of which Jeep Wrangler, Volkswagen ID.4, and Mustang Mach-E had average monthly sales of 4.5K, 1.7K and 2.2K, with a total cumulative contribution of 60,000 increments, which was the main force in the new models listed. Superimposed biden government charging pile supporting facilities construction, new new energy vehicle subsidies and other policy plans, driving the US sales in 2021 to double year-on-year. (Source: Future Think Tank)

Second, the 2022 model outlook: the domestic market blossoms at many points, and pure electricity emerges in the European and American markets

2.1 Domestic market: a large number of mid-to-high-end models are listed, and there should be no doubt about the annual sales of more than 5.5 million

According to our incomplete statistics, it is expected that at least 37 new electric models will be listed in the domestic market from mid-2021 to 2022. Compared with 2021, a large number of high-quality models will be launched in the mid-range and high-end markets in 2022, and the domestic new energy vehicle market will usher in a comprehensive prosperity.

2.1.1 Mid-range market: product richness and intelligent configuration improvement

The highlights of the new mid-range pure electric models are mainly reflected in intelligence, cost performance and personalization. Since the second half of 2021, the 100,000-200,000 yuan pure electric models represented by the Xiaopeng P5, BYD Haiyang series, the Great Wall Euler series, and the zero-run C11 have been listed, which is expected to further activate the mid-range pure tram market.

(1) Intelligent: L3 level automatic driving has gradually penetrated into 100,000-200,000 yuan models. Xiaopeng P5, zero-run C11, Lightning Cat three new models all support L3 level automatic driving, the number of supporting perception hardware is also significantly higher than the previous model of the same level of intelligent driving, Xiaopeng P5 (550P/600P version) model is equipped with 2 laser radar, is the first model equipped with lidar below 200,000 yuan (of which, the 550P version is priced at 199,900 yuan).

Xiaopeng P5: The world's first mass-produced lidar smart car, creating a "23-hour intelligent third space". P5 is another masterpiece of Xiaopeng in the mid-end market after the G3, positioned as an A-class smart car for the home market, with a price of 157,900-22.39 million yuan after subsidies.

In terms of intelligent driving, the P5 is the world's first mass-produced lidar smart car, high-end model 550P/600P equipped with dual lidar, the farthest detection distance is up to 150 meters, the ranging accuracy is centimeter-level; the XPILOT3.5 automatic driving assistance system is adopted, equipped with 13 high-definition cameras, 5 millimeter-wave radar, 12 ultrasonic sensors, 2 vehicle-level lidar, a total of 32 sensors.

In terms of intelligent cockpit, P5 applies the latest Xmart OS 3.0 system, the industry's first "full-scene voice", supports continuous dialogue, visible speaking, dual-tone zone recognition and other high-end functions, equipped with high-definition 15.6-inch suspension touch screen, 12.3-inch full LCD instrument. In addition, P5 creates a "23-hour smart third space", which can provide optional cabin accessories such as sleep sets, movie sets, and car gourmet smart refrigerators to meet the other personalized needs of car owners.

(2) Cost-effective: Compared with the same level of fuel vehicles, the cost performance is prominent.

In terms of performance, on the one hand, the new generation of pure electric platform is more simple in internal structure, pure electric models compared with the same level of fuel models "wheelbase / body length" is lower, the cockpit space is larger; on the other hand, the noise and vibration emitted by the motor when running is much smaller than the engine, and the smoothness and quietness of pure electric vehicle driving are significantly better.

In terms of cost, thanks to the rapid popularization of lithium iron phosphate batteries in mid-range models driven by CTP, blade batteries and other technologies, and the reduction of production costs after the upgrade of the pure electric platform, many new models of pure electricity in the 100,000-200,000 yuan section have achieved parity with fuel vehicles or even better performance, and zero-run C11 is a typical representative. Considering the advantages of the green card and the cost of electricity consumption is much lower than the cost of fuel consumption, the cost performance of mid-range pure electric models is prominent.

Zero-run C11: "Cross-level fully equipped with pure electric SUVs" to create the ultimate cost performance. Zero-run C11 is positioned as a B-class pure electric SUV, priced at 159,800-19.98 million yuan after subsidies. At the beginning of the listing, Zero-Run Automobile defined the C11 as a "cross-level fully equipped pure electric SUV" with excellent hardware configuration. Power performance: The dual-motor version has a maximum output of 400 kW, a maximum torque of 720 N·m, and a maximum acceleration time of 4.8 s; the NEDC cruising range is up to 610 km. Intelligent: The C11 enables intelligent assisted driving close to L3. The whole series is equipped with two self-developed Lingxin 01 intelligent driving chips, with a single computing power of 4.2TOPS, which is significantly better than the mainstream Mobileye EyeQ4 2.5TOPS hash rate; equipped with 10 high-definition cameras, 5 millimeter-wave radars, and 12 ultrasonic sensors. Since its launch at the end of September, C11 sales have continued to climb, with 7,005 C11 orders in November, and cumulative orders reaching 18,113 units.

(3) Personalization: Differentiated positioning to tap market segments. The competitiveness of the product is reflected in the cognition of the consumer group, with the continuous promotion of the product, the car company began to conduct in-depth research and accurate positioning of the user, Xiaopeng P5 mainly focuses on family users; BYD Ocean Series and GAC Aion Y mainly attack young groups; the Great Wall Euler Cat series focuses on the female market, catering to the demands of female car owners in appearance and function.

BYD Ocean series models focus on young people, benchmarking the Cat series of the Great Wall Euler. The first model, Dolphin, was officially launched at the end of August. Dolphin is the first model launched based on the e-platform 3.0, positioned as an A0-class BEV, priced at 9.38-12.18 million yuan after subsidies, and the cruising range includes 301/401/405km three gears. In terms of design, the design concept of "marine aesthetics" is adopted; although it is an A0-class model, its wheelbase is up to 2.7m, and the interior space is significantly more spacious than other A0-class and even some A-class cars. In terms of power performance, the maximum power is 70/130kW, and the power consumption of 100 kilometers is 10.3kWh. Since its launch, Dolphin sales have climbed month by month, with retail sales increasing to 8,800 units in November. In 2022, the Ocean Series will also feature seals, sea lions, and seagulls. Official seals are defined as sharp sports, sea lions as spacious and comfortable, seagulls as flexible and free, and the model matrix continues to improve.

Great Wall Euler is positioned as "the world's most women's car brand", which is suitable for women's aesthetics and needs in both appearance and function. In 2022, The Great City Euler is expected to release three models of lightning cat, ballet cat and punk cat, and we expect that the model will cover the A0-B class, and the main price segment is expected to be 15-20 million yuan.

Ballet Cat: Similar in appearance to Volkswagen's early Beetles, with distinct retro colors and an L2+ level assisted driving system. Deliveries are expected in the first half of 2022.

Lightning Cat: Positioned as a 200,000 yuan pure electric coupe, the price is expected to be about 200,000 yuan. The appearance is strongly modern, and it is also equipped with frameless doors and electric lifting tails; equipped with L3+ level auxiliary driving system; in terms of power performance, the Lightning Cat is equipped with dual motors, zero hundred acceleration time can reach 3.5s, and the comprehensive cruising range of NEDC can reach up to 700km. Deliveries are expected in the second quarter of 2022.

Punk cat: adopts the design concept of "classic restoration aesthetics", and adopts a simple retro body curvature and coherent and feminine body curves on the outside; the interior adopts a yacht-style design, integrated through the large screen, central control panel suspension wireless charging and suspension reading lights, which are expected to be released in the second quarter of 2022.

The advantages of low purchase cost and low fuel consumption of plug-in and hybrid models are significant, and intelligent equipment is superimposed to accelerate the replacement of fuel vehicles. In 2021, BYD launched two A-class PHEV models, Qin Plus DM-i and Song Plus DM-i, which have gradually replaced the A-class fuel vehicle market with low acquisition cost and low fuel consumption. In 2022, BYD, Great Wall, Changan, Chery and other manufacturers will launch a number of 100,000-200,000 yuan PHEV models to seize the fuel vehicle market.

2.1.2 High-end market: the hardware configuration has been greatly upgraded, and long-endurance and fast charging dominate battery technology

Compared with 2021, in 2022, the domestic high-end electric vehicle market will have a large number of high-quality models listed, in addition to the new car-making forces represented by Wei Xiaoli continue to promote, independent brands, joint venture brands have made great efforts. The outstanding features of high-end electric vehicle models in 2022 are mainly reflected in:

In terms of intelligent hardware configuration, lidar has gradually become the standard of high-end models, and the chip computing power has been greatly improved compared with the previous generation model

In terms of automatic driving chips, NVIDIA's new generation of automatic driving chips Drive Orin is gradually popularized, and WEI's ET7, ET5, and WM M7 are all equipped with 4 Orin chips to achieve the ultra-high computing power of 1016TOPS. In terms of sensors, on the one hand, the number has increased compared with the previous generation model, and on the other hand, the number of laser radar has gradually become popular. WEILAI ET7, ET5, Xiaopeng G9, WM M7, BAIC Jihu Alpha S (Huawei Hi Version), Great Wall Salon Mech Dragon and other models are equipped with lidar, and the Great Wall Salon Mech Dragon is even equipped with 4 laser radars.

Battery innovation has pushed the cruising range to 1000km, and the popularity of fast charging has improved charging efficiency

Battery innovation to promote the mileage to 1000km forward, WEILAI ET7, ET5, Zhiji L7, GAC Aion LX PLUS have launched a version with a range of more than 1000km: ET7, ET5's 1000km version of the model are equipped with semi-solid-state batteries, Zhiji L7 high-end version, Aion LX PLUS batteries using silicon-doped lithium technology, by improving the specific capacity of the negative electrode to improve energy density. The penetration rate of high-voltage platforms has increased, and fast charging has gradually become popular, and Xiaopeng G9, Jihu Alpha S (Huawei HI Version), and Great Wall Salon Mech Dragon can achieve charging efficiency of 195km/10min, 200km/5min, and 401km/10min respectively.

From the perspective of car companies, 2022 is a big year for new forces, and the competitiveness of products has been qualitatively improved compared with the previous generation of models. In 2022, all new force car companies have obvious breakthroughs in high-end models: WEILAI launched the car ET7 and ET5 for the first time, and ET5 directly hit the 250,000 yuan + volume market; Xiaopeng, Weima and Nezha all launched flagship models to promote brand positioning. Overall, this round of new models compared with the previous generation of models in terms of power performance, endurance, intelligent driving and other aspects have been significantly improved, lidar, ultra-long endurance, 200km/ 5min fast charging is a prominent point of view.

Independent brands: High-end brands of new energy have been launched, and technology companies have empowered and improved intelligent experiences. Since 2021, a number of independent new energy high-end brands such as Shangqi Zhiji, Geely Extreme Krypton, BAIC Jihu, Dongfeng Lantu and so on have been launched one after another, regarding electric vehicles as a powerful grasp of brand upwards. In addition, SAIC motor joined hands with Alibaba and Zhangjiang Hi-Tech to build SAIC Zhiji, BAIC motor and Huawei to build Alpha S (Hi version), and huawei to build Cilis to improve intelligent performance.

2.2, European and American markets: pure electric models emerge, pickup trucks are expected to become a new addition to the US market

2.2.1 U.S. market: large models account for a high proportion, electric pickup trucks emerge

The new models in the US market this round are mainly B-class and above models, with higher battery. According to incomplete statistics, from 2021H2 to 2022, at least 30 new electric models will be listed in the European and American markets. From the perspective of model structure, the Chinese and European markets are concentrated in the A-C class car market, and the distribution of models at various levels is more balanced; while the US market is dominated by B-class and above models, and even a number of D-class models, with higher bicycles.

The power performance of the pickup truck is strong, the energy consumption is high, and the electric pickup truck has more than 100kWh of power. Pickup truck is a major model of the US automobile market, accounting for nearly 20% of the total sales, its main features are: cockpit space and rear box loading space is large, can withstand a large load; strong power performance, suitable for a variety of road conditions, therefore, pickup truck energy consumption is larger, electric pickup truck with more than 100kWh power. Previously, the US market has been lacking in high-quality electric pickups.

2022 will be the year of the outbreak of the ELECTRIC pickup truck market in the United States, which is expected to become a new growth point in sales and drive further improvement of the carrying power. From 2021H2, there will be a number of pure electric pickup truck models in the US market: 1) Rivian R1T: The first electric pickup truck in the United States, 336 units have been delivered by the end of November 2021, and it is expected to start in 2022. 2) Ford F-150 Lightning: More than 130,000 units were scheduled for September ($100 deposit), and then Ford increased the model's 2024 production target from 40,000 to 80,000, indicating that the scheduled volume exceeded the company's expectations, and mass production is expected in 2022H1. 3) Tesla Cybertruck: As of August, the Cybertruck is scheduled to reach 1.26 million units, and mass production is expected to be completed by the end of 2022 and delivered in 2023.

2.2.2 European market: This round of new model cycle is mainly pure electric models, and the carrying power will be significantly improved

A new round of high-quality pure electric models has begun to be launched, and the carrying power will be significantly improved. At present, PHEV accounts for a relatively high proportion of the sales structure of european new energy vehicles, and in October, European PHEV sales accounted for 39% of the total sales of new energy vehicles, on the one hand, because PHEV is a transitional model, it is an important means for European automakers to meet the short-term carbon emission assessment; on the other hand, a considerable number of pure electric models have been developed based on oil-to-electricity platforms, whether it is endurance or power performance is weak. Since 2021H2, with the launch of a large number of high-quality pure electric models based on pure electric platforms, it is expected to drive sales and bicycles with double liters of electricity. (Source: Future Think Tank)

Third, 2022 sales outlook: China's steady growth, overseas volume, the global electric wave trend is firm

3.1, domestic subsidies throughout the whole year of 2022, conservatively expected the industry to increase 62% year-on-year

3.1.1 Policy side: The subsidy threshold requirements remain unchanged, and the subsidy time runs throughout the year

On the domestic side, the policy side of the 2022 new energy vehicle subsidy end threshold requirements remain unchanged, the amount of 30% decline, subsidy time exceeded the limit of 2 million vehicles, throughout the whole year of 2022. On December 31, the Ministry of Finance and other four departments issued the "Notice on the Financial Subsidy Policy for the Promotion and Application of New Energy Vehicles in 2022", clarifying that the framework and threshold requirements of the new energy vehicle technical indicator system in 2022 will remain unchanged, and the subsidy standard for new energy vehicles in 2022 will be reduced by 30% on the basis of 2021; urban buses, road passenger transport, rental (including online car-hailing), sanitation, urban logistics distribution, postal express, civil aviation airports and vehicles in the official field of party and government organs, the subsidy standard is in 2021 The annual decline is 20%. For C-end consumer cars, the maximum bicycle subsidy was reduced from 18,000 yuan to 12,600 yuan, and the bicycle was reduced by 5,400 yuan. The notice clearly changed to December 31, 2022 as the end date of the subsidy, which also indicates that the scale of the subsidy will be lifted from the original expected 2 million vehicles to the whole year, and it is initially expected to double the financial subsidy. We expect that in addition to considering factors such as industrial development planning, market sales trends and the smooth transition of enterprises, the state is also a kind of burden reduction for car companies under the upward pressure of raw materials.

3.1.2 Model end: The centralized listing of new cars drives the downstream volume

The new force Tesla production capacity expansion export increased, Weilai, Ideal, Xiaopeng new car centralized listing; traditional car companies Extreme Kr, Zhiji, Xilisi high-end brands in the first year of the first year; Volkswagen, Mercedes-Benz, BMW, GM and other joint venture brand pure electric platform volume, driving industry resonance. With more than 20 new models on the market in 2022, we expect to sell more than 5.6 million new energy vehicles in 2022, +62% month-on-month.

3.2, European and American subsidies and regulatory resonance, mainstream car companies transform and release

3.2.1 European German and French subsidies are postponed, and carbon emission pressures continue

In Europe, the subsidy policies in Germany and France have been postponed, which is good for sales growth in 2022. In Germany, in the union agreement submitted by the new federal government in November, it was stated that the validity of the innovation bonus (3000 euros) will be extended from the end of 2021 to the end of 2022, on the basis of the environmental bonus (6000 euros), the innovation bonus (3000 euros) will continue to take effect next year. In France, at the end of October, the French government announced that the current new energy vehicle subsidy policy is extended from the end of 2021 to June 30, 2022, and the implementation of the slope reduction plan is postponed, that is, the maximum subsidy of 6,000 euros for bicycles will continue to take effect before the middle of next year.

The downward pressure on emissions is relatively large, and the supply side of the car companies tram launches spare no effort. In 2019, the European Union set a carbon emission requirement of 95g CO2/km for newly registered passenger cars, which has not been fully met in all countries. In Germany, under the NEDC calculation method, carbon emissions have gradually declined, but still exceeded the target by nearly 10g/km; in France, under the WLTP algorithm, the carbon emissions of newly registered vehicles in November fell to 101.2g/km, -0.8g/km month-on-month, and this year has reached the 2021 carbon emission target five times, but it still needs to be maintained to complete the annual target.

3.2.2 US policy + model two-wheel drive, sales in 2022 continue to double year-on-year

Biden government bicycles are expected to take effect in 2022 for up to $12,500 in tax credits, and the extension of subsidies will not affect the annual release. The concentrated listing of electric pickup models such as the Ford F-150 Lightning and Rivian R1T will drive the outbreak of sales in the US electric pickup truck market. Policy + model two-wheel drive U.S. sales in 2022 will increase year-on-year, and it is expected to maintain a trend of more than doubling year-on-year.

3.3, the world opened the electric wave, 2021-2025 CAGR > 36%

Looking forward to 2022, we expect global new energy vehicle sales to reach 9.61 million units, by model, passenger car sales of 9.36 million units, commercial vehicle sales of 250,000 units; from the penetration rate, the global penetration rate of 21 years is expected to be 8%, of which China's overall penetration rate is ahead of Europe and the United States, reaching 15%; it is expected that in 2022, the global penetration rate of the three places will resonate with 12%; from the perspective of model structure, the launch of hybrid models such as China's DM-i will drive the hybrid proportion to increase by 2pct in 2022. However, with the large number of pure electric platform models in Europe and the United States, it is expected that the proportion of global hybrids will drop by 2pct to 28%.

In the long run, the world has opened a wave of electric power, the trend is firm, and the space is huge. In 2025, global new energy vehicle sales are expected to reach 21.08 million units, with a compound growth rate of 36%. Among them, China has the largest volume, reaching 7.55 million vehicles; the United States has the highest growth rate, with a compound growth rate of 63%.

Quarterly, it is expected that the global quarterly sales in 2022 will be 177, 221, 249, 2.89 million, at the beginning of the year by the domestic Spring Festival, overseas New Year's Day and other long holidays, -15% month-on-month, in the second quarter, if the US policy is implemented, superimposed on the domestic new car listing, French subsidies rushed, it is expected to bring a strong growth of 25% month-on-month. From the perspective of penetration rate, benefiting from the continuous introduction of new energy models and driven by market awareness, it is expected that the quarterly change of penetration rate will continue the trend of rapid improvement in the 21-year quarter, from 10% to 14%, and the annual penetration rate will reach 12%.

Fourth, lithium battery outlook: iron lithium, high nickel drive industry growth

4.1 Total demand for lithium batteries in 2022 will reach 803GWh, CAGR 35.8% from 2021 to 2025

4.1.1 In 2022, the procurement demand for electric vehicle batteries was 533GWh, a year-on-year growth rate of +62%

The curtain of global electrification is opened, and it is expected that the global electric vehicle lithium battery installed capacity will be 274GWh in 2021, of which 246GWh for passenger cars and 28GWh for commercial vehicles, and the procurement demand after superimposed installed redundancy and channel inventory will reach 329GWh; the procurement demand for electric vehicle batteries in 2022 will be 533GWh, a year-on-year growth rate of +62%; the global electric vehicle lithium battery procurement demand will be 1367GWh in 2025, and the CAGR will be 42.7% from 2021 to 2025, which is higher than the growth rate of electric vehicle sales 6.9pct。

From the perspective of bicycle carrying electricity, due to the proportion of models below A class in China reaching 37%, the charging capacity of pure electric models has stabilized at 47-49 degrees since 2019, without significant improvement; overseas in the pickup truck, pure electric new platform models continue to drive, bicycles with electricity from 2021 to climb faster.

From the overall demand of the industry, it is expected that the battery demand for small power, consumer lithium battery, power system energy storage, and communication energy storage in 2022 will be 78, 95, 81, and 16GWh, corresponding to a year-on-year growth rate of 23%, 7%, 60% and 50%, and the total global lithium demand for superimposed electric vehicle demand will be 803GWh.

4.2 Iron lithium, high nickel ternary continue to squeeze the nickel space

With the launch of iron-lithium versions such as Tesla Model 3, Model Y and Xiaopeng P7, domestic electric vehicles have sunk and increased their cost performance, opening up sales space, driving the proportion of iron lithium in 21 years to more than 48%; overseas Tesla NCM8 series and Tesla NCA have driven the rapid increase in the proportion of high nickel, and the proportion of high nickel in 2022 is more than 25%.

From the perspective of battery proportion, ternary and lithium iron share together squeeze the share of LCO and LMO, consumption, communication energy storage, small power transformation LFP and ternary as the trend; from the year-on-year growth rate, it is expected that in 2022, iron lithium growth rate of 59%, more than three yuan 7pct.

In terms of the growth rate of subdivisions, the growth rate of high nickel in 21-23 years reached 115%, 83% and 61%, followed by the growth rate of lithium iron and lithium was 82%, 59% and 38%, which was faster than the year-on-year growth rate of total demand for lithium batteries, and was the two most worthy of investment.

Fifth, investment strategy

In terms of material requirements, ternary for LFP, the demand for lithium carbonate is higher, while the demand for diaphragms, negative electrodes, electrolytes, etc. is less, but the quality requirements are higher.

From the demand for the four major materials, considering the impact of the battery's pass rate and industry inventory, we estimate that the global demand for the positive electrode in 2022 will be 2.13 million tons, of which the demand for LFP, ternary and LCO will be 90, 85 and 380,000 tons respectively; the demand for the negative electrode is 1.2 million tons, and we estimate that the demand for artificial graphite, natural graphite and silicon carbon will be 68, 49 and 30,000 tons, respectively; the demand for electrolyte is 950,000 tons; and the demand for diaphragm is 15.1 billion square meters.

(This article is for informational purposes only and does not represent any of our investment advice.) For usage information, see the original report. )

Featured report source: [Future Think Tank].