Following yesterday's article "The Survival Pattern of Second-line Battery Manufacturers 1 - Several Enterprises that Do Square Shells", the situation of second-line battery companies was sorted out during the New Year's holiday.

There are three typical second-tier battery companies, let's focus on it:

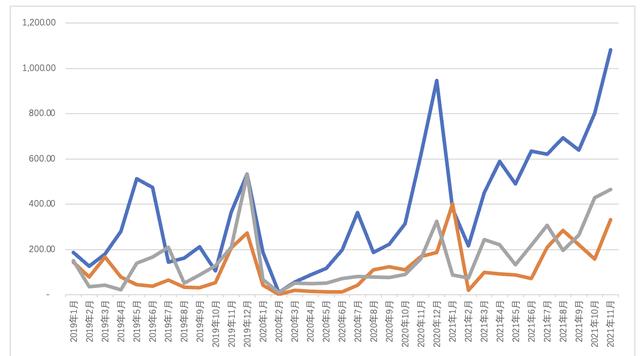

● Guoxuan Hi-Tech: 1.08GWh in November, 6.6GWh in November, the overall strategy after taking the iron lithium route is very clear

● Ewell Lithium Energy: 0.47GWh in November, 2.59GWh in November, Ewell Lithium energy covers a lot of product lines, soft packs and square shells in the power field, which somewhat limit their own quantity

● Fu Neng Technology: 0.33GWh in November, 1.98GWh in November, BAIC accounted for 20% at the beginning of the year, followed by gazing supply, but the amount still did not go up, and began to supply Mercedes-Benz BEV in November

My personal judgment is that it is too difficult for China to do the route of soft package ternary, so after this technical route does not work, the next step may be transferred to a short blade of about 600mm iron lithium, the effect will be better. Whether Guoxuan's cylindrical lithium route can be sustained may have some challenges to the battery process, especially in solving the problem of leakage.

▲Figure 1 The installation volume of several battery companies in 2019-2021

Part 1 From the distribution of customers

(1) Guoxuan Hi-Tech

Guoxuan Hi-Tech's customer structure, Figure 2 below shows it more clearly: SAIC-GM-Wuling, JAC and Chery as the basic disk, and then also did Changan, zero-run A00 level BEV.

▲Figure 2 The sub-customer trend of Guoxuan Hi-Tech's installed capacity in 2021

In terms of passenger cars, Guoxuan Hi-Tech is currently limited to low-cost A00 cars, and due to the problem of rising costs, there is a ceiling for the ability of several customers to be on the volume.

(2) Ewell lithium energy

The product line of Ewell Lithium Energy actually contains a lot of commercial vehicles (square shell lithium iron phosphate products), so the passenger car mainly includes Xiaopeng BEV and Mercedes-Benz PHEV, and overall, the next step around the soft package route is indeed to be transformed.

Later, Yiwei lithium can be transformed in the direction of high nickel cylinders, and the overall direction is OK.

▲Figure 3 The sub-customer trend of the installed capacity of Lithium Energy in 2021

(3) Fu Neng Technology

In addition to a batch of BAIC cars at the beginning of the year, the core of Fu Neng Technology revolves around the demand for GAC passenger cars; the overall demand is relatively scattered, of which, in November, there was a demand for Beijing Benz BEV, which is a relatively large follow-up point of view.

But what I want to say is, what to do with opening up new customers later? Among so many companies, Fu Neng is the only one that does not do iron lithium, and it is quite difficult to turn in the direction of energy storage or other high-safety routes.

Figure 4 The sub-customer trend of Fu Neng Technology's installed capacity in 2021

Part 2 Distinction between ternary and lithium iron

As mentioned earlier, in these several, Guoxuan Hi-Tech has made a very rapid conversion in terms of iron lithium.

At present, the figures of Guoxuan Hi-Tech Iron Lithium and Ternary are 0.537GWh (accounting for 8.1%) and 6.06GWh (91.8%), respectively. What I am more confused about is how volkswagen and Guoxuan operate, based on the square shell to do ternary or around the route of square shell iron lithium to do CTC.

▲Figure 5 The transformation of iron lithium in Guoxuan

The situation of Ewell lithium energy:

● In 2019, it is completely around lithium iron phosphate as a commercial vehicle;

● By 2020, we will start to cooperate with SK to do the soft package ternary route step by step around the ternary;

●After the original route encounters challenges in 2021, the speed of capacity expansion is not fast;

●After the demand for lithium iron phosphate rose, it was very resolutely increasing in this direction.

Figure 6 The proportion of lithium iron phosphate in the output of lithium energy

Summary: I personally think that it may be a better practice for the soft package to change the encapsulation process and switch to blade iron lithium; and on the side of the large cylinder, whether it is to do iron lithium or high nickel (which needs to be tackled by the full polar ear), there is room for development. The biggest challenge for all second-tier battery companies next year is how to control costs, or how to get raw materials.