In 2021, the dust has settled. The power battery market has experienced a year of soaring.

A few days ago, the Power Battery Innovation Alliance released the monthly data of power batteries in December 2021:

December: 31.6 GWh production, 35.5 GWh sales, installed capacity of 26.2 GWh

2021: Production of 219.7GWh, sales volume of 186.0GWh, installed capacity of 154.5GWh

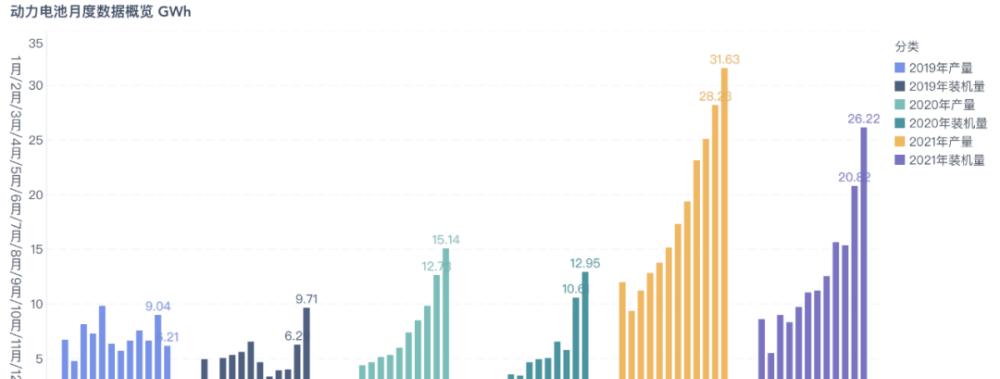

The following figure can make everyone intuitively see - in 2020 and 2019, the power battery is still in a sideways state, and in 2021, the demand for power batteries has suddenly exploded.

In 2021, the output of power batteries exceeded 219.7GWh, an increase of 163.4% year-on-year. Among them, the ternary did not break through 100GWh, but it was also at a high level of 93.9GWh; the production of lithium iron phosphate batteries accumulated 125.4GWh, accounting for 57.1%, an increase of 262.9% year-on-year. Lithium iron phosphate presses through the ternary battery and is very clear and unambiguous.

Figure 1 Comparison of china's power battery situation in three years

1

Overview of market specifications

1) The main line of demand

In December, the demand for single-month vehicles was 1.82GWh for plug-in hybrid passenger cars, 4.43GWh for pure electric commercial vehicles (2.04GWh for pure electric buses and 2.39GWh for pure electric trucks), and pure electric passenger cars were still far ahead of 19.86GWh.

Figure 2 Where are China's power batteries used in December?

From the perspective of the whole year of 2021, pure electric passenger cars use 121.73GWh batteries, accounting for 78.7%, while pure electric buses, pure electric special vehicles and plug-in hybrid passenger cars each have an annual demand of 10-12GWh, which can be said that the power battery field is highly concentrated in the passenger car market. This objectively confirms that this round of demand is the growth of C-end new energy vehicle demand. The size of the C-end market is many times that of the B-end market. As the penetration rate further increases, the gap between 2C and 2B will continue to widen.

Figure 3 In the 2021 market, the pure electric passenger car market based on personal consumption is the main demand

2) The situation of the power battery supplier

With the further agglomeration of suppliers, there are only 58 power battery companies left in China by the end of 2021.

In December 2021, the market shares of the top 3, top 5 and top 10 power battery companies were 75.8%, 84.5% and 93.4%, respectively. From the annual point of view, the top 3, top 5 and top 10 power battery companies have power battery loading capacity of 114.6GWh, 128.9GWh and 142.5GWh respectively, with a market share of 74.2%, 83.4% and 92.3%.

But look at the following chart is more intuitive: the Ningde era accounts for more than 52%, BYD's market share is 16%, and AVIC lithium battery is 6%. The accumulation effect of this market is still very thorough and obvious.

Figure 4 The situation of various suppliers of power batteries in China in 2021

3) Penetration of lithium iron in December

In December, the total load of ternary batteries was 11.1GWh, an increase of 84.7% year-on-year; the total loading of lithium iron phosphate batteries was 15.1GWh, an increase of 118.5%. The installed capacity of lithium iron phosphate is rapidly exceeding ternary. From the perspective of various automobile companies, who is the vanguard?

The following is a classification from the matching of vehicle models, judging from the vehicles delivered in December, Tesla, BYD and Wuling have very rapid lithium iron (more than 75%), followed by Changan and Euler (more than 40%). Most of the other automotive companies are still in the planning stage, mainly limited by the production capacity of lithium iron phosphate and the switching speed of the whole vehicle.

Figure 5 China in December by vehicle power battery type

Tesla is the fastest in the application of lithium iron phosphate, as shown in the chart below, which accounts for the vast majority of new cars.

According to estimates of nearly 60,000 units, Tesla used a 3.6GWh iron lithium battery. And Nio uses the latest lithium iron phosphate and ternary composite technology, and the 75kWh ternary composite battery probably accounts for more than half of the total number of NIO. Xiaopeng has not yet been able to effectively get enough lithium iron phosphate production capacity, so most of them are currently around ternary batteries. Zero ran inside the T03 and got a lot of iron lithium batteries, so the speed of iron lithiumization is also relatively fast.

Figure 6 Progress of lithium iron in major new car manufacturers

2

The evolution of technology and the pattern of demand

If you want to deeply understand the technical trends in 2022, you must also carefully compare the actual situation of lithium iron phosphate and ternary battery systems.

According to the data, most of the current lithium iron phosphate battery system energy density is below 140Wh/kg, and there is still some gap between the energy density and ternary batteries.

It is also said that the gap in the energy density of the whole package of lithium iron phosphate and ternary batteries before did exist. The energy density of some ternary batteries has exceeded 200Wh/kg, and they are heading for higher data. In the era when subsidies are more important, energy density is indeed very important, but subsidies have begun to slowly be ignored for a long time.

Figure 7 Pattern of energy density of battery system

In December 2021, the battery system of lithium iron phosphate can support the range of pure electric vehicles covering a range of 600 kilometers.

Ternary battery systems do have some advantages in terms of energy density, but the biggest problem is that the comprehensive comparison is in the ascendant. Pure electric vehicles armed with ternary batteries can achieve an endurance of 700 kilometers, but they basically rely on battery products of about 100kWh. There is no subsidy within 20kwh and the iron-lithium ratio, and the cost is very uncomfortable. Ternary batteries are densely packed around 300 km, 400 km, 500 km and 600 km.

In the PK of the core parameters, lithium iron phosphate currently occupies an advantage in safety and cost, and the mileage of supporting electric vehicles can meet the needs of consumers. With the intensification of cost pressure in 2022, car companies need to switch lithium iron phosphate on a large scale in order to deal with cost problems more effectively.

Figure 8 Lithium iron phosphate and ternary respectively cover the range range

In 2022, possible technological changes can be seen including:

1) Ternary high-end batteries, the first generation of fast-charging batteries based on 2C has begun to be launched, which is the first distinction between high-end in 2022

2) The fast charging speed of lithium iron is also improving, according to the current situation, 2C lithium iron phosphate batteries will also be gradually promoted in 2022

3) In 2022, second-tier battery companies that previously developed around ternary will begin to launch their own lithium iron phosphate products

The safety problems brought about since 2017 have plagued China's electric vehicle industry for a long time, so in 2021 lithium iron phosphate staged a Jedi reversal. However, from the perspective of product characteristics, I personally still feel that the ternary technology route has the potential for long-term evolution.

——END——