I am writing a battery monthly report for Dianguan, first picking some preliminary conclusions to do some discussion, and then I will publish a complete analysis article of the comparative system.

What I see is that as the application of lithium iron phosphate becomes more and more widespread, overall, the competitiveness of ternary is really weakening. From another point of view, there are some vehicle companies whose battery cell choices have begun to gradually differentiate, let's look at Xiaopeng, Eian, Euler and Tesla specifically.

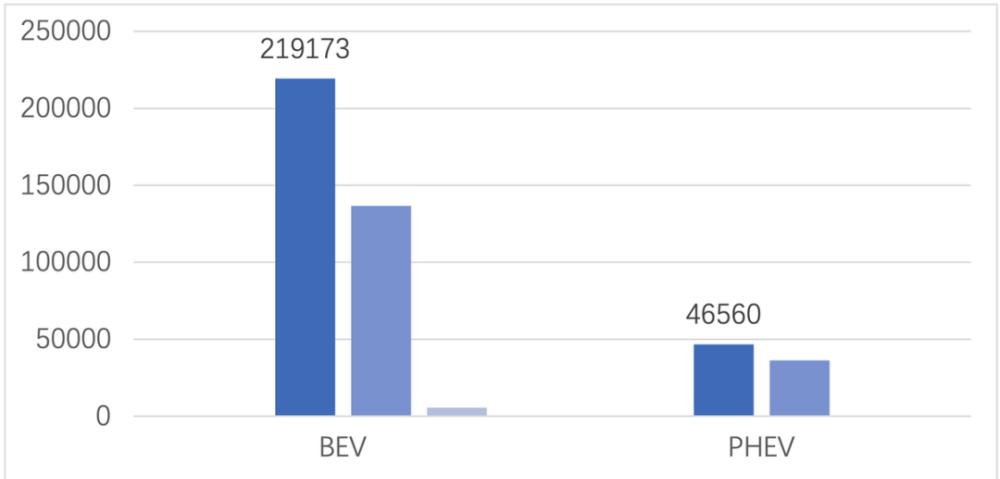

Figure 1. At present, the proportion of different types of batteries in March

From the attribute point of view, Chinese car companies and Tesla are holding the banner of lithium iron phosphate, and Japanese, Korean and German car companies are not ready. BYD and Tesla have single-handedly pushed the re-popularization of lithium iron phosphate in China to a very high speed.

Figure 2. The speed of iron lithiumization of different car companies

Part 1 The process of lithium iron phosphate

From the perspective of traditional car companies, BYD is the first to fully and completely lithium iron phosphate, and with the follow-up Iteration of Han DM to DM-i, the use of ternary batteries is basically invisible. In the A00 field, Wuling, Chery and Changan are all using lithium iron phosphate batteries as low-cost solutions. The Geely in the main A-class car has not yet moved, and we will analyze Trumpchi and Euler in the follow-up analysis.

Figure 3. Lithium iron of traditional independent brands

In the new forces, in addition to Tesla, Zero Run, Xiaopeng and Weilai are all rapidly advancing lithium iron phosphate.

Figure 4. The iron lithiumization of new forces

I understand the difference in cost this way, before the price difference between iron lithium and ternary is about 1 mao / Wh, with the price increase of more than 30%, with iron lithium to replace the high voltage system of nickel 55 cells, from the cost point of view there is still a certain advantage. With the transmission of car prices to the consumer market, the demand for lithium iron phosphate is still faster than that of medium nickel ternary. And from the perspective of new force car companies, the 400-500 km of ternary does not actually reflect the characteristics of ternary.

Table 1. Battery situation of new power car companies

So at present, Sanyuan can only develop models that are more than 600 kilometers, and this space is indeed a bit narrow.

Part 2 Several key enterprises

(1) Tesla

Tesla's situation is relatively simple, only 11,000 units of three yuan, accounting for 17%.

Figure 5. Tesla's battery supply (March)

(2) Xiaopeng

Xiaopeng's situation, from the Ningde era to switch a lot, it is precisely because of three cars, two chemical systems and three suppliers, resulting in more types of electricity.

Figure 6. Xiao Peng's case

Looking at the following table, Comrade Anlong has to manage so many products well, and it really takes a lot of effort.

Figure 7. Xiaopeng's battery selection

Summary: Let's write here first, and the detailed analysis can be followed by the interpretation of electric vehicle observers. At present, we are still in silence, and the second article can also be casually looked at.