The trend of ternary batteries and lithium iron phosphate is increasingly differentiated.

In November, the total output of power batteries was 28.2GWh, and the output of lithium iron phosphate batteries was 17.8GWh, accounting for 63.0%; the output of ternary batteries was 10.4GWh, accounting for 36.8%. The year-on-year growth rates of lithium iron phosphate and ternary were 229.2% vs 42.6%, respectively.

After analyzing the market this month, I will focus on the next step, the choice of different packaging routes for lithium iron phosphate technology in various companies.

2021 is a good or bad year for the battery industry.

The total output from January to November 2021 was 188.1GWh, a cumulative increase of 175.5% year-on-year, and such a high growth rate had a pull on upstream raw materials, making the price of products rise rapidly. This fact has caused a shortage of upstream raw materials and rising prices, and it is also doomed that small battery companies will need a lot of money to buy upstream materials next year, and face difficulties in dealing with downstream prices.

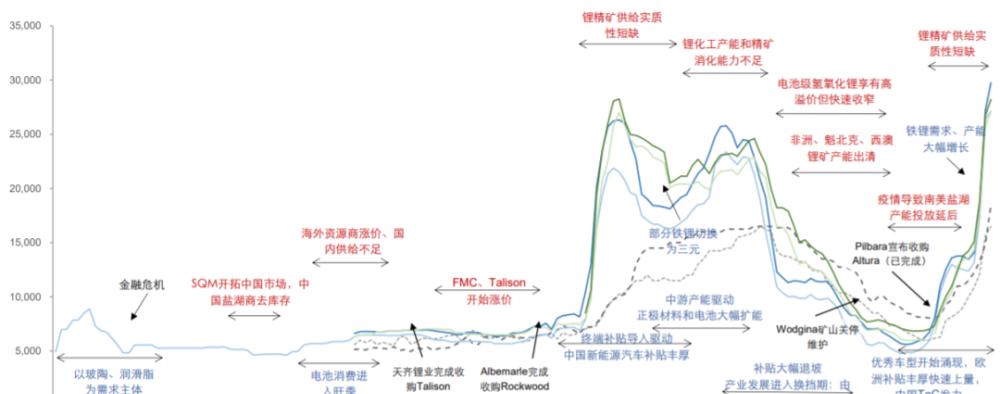

Figure 1 Minmetals Securities for 2007-2021 YTD, two rounds of lithium product prices (USD/ton) [1]

1

The overall output and installed capacity of power batteries

In November, the output of power batteries totaled 28.2GWh, an increase of 121.8% year-on-year and 12.4% month-on-month; the installed power battery volume was 20.8GWh, up 96.2% year-on-year and 35.1% month-on-month.

From the overall power production climbing situation, we can clearly see the popularity of the power battery industry.

Figure 1 The total development of the power battery industry in 2020-2021

Here we decompose the data by output and installed capacity:

The output of power batteries was 28.2GWh, and the output of ternary batteries was 10.4GWh, accounting for 36.8%, an increase of 42.6% year-on-year and 12.9% month-on-month;

The output of lithium iron phosphate batteries was 17.8GWh, accounting for 63.0%, an increase of 229.2% year-on-year and 12.0% month-on-month.

Power battery loading volume of 20.8GWh, ternary battery loading 9.2GWh, up 57.7% year-on-year, up 32.5% month-on-month; lithium iron phosphate battery loading 11.6GWh, up 145.3% year-on-year, up 37.2% month-on-month.

From the systematic point of view of these data, the current export of lithium iron phosphate is relatively small, mainly with the export of Tesla vehicles, so from this data can reflect that the subsequent ternary installed capacity in 2022 is to the top, and there is no rapid growth trend in the stage of rapid growth in demand; and the data of lithium iron phosphate is still rising.

This difference provides a forward-looking forecast of installed capacity in the following months.

Figure 2 Production and installed capacity of ternary and lithium iron in November

If you look at it from the monthly data, it is more reflective of this blowout of lithium iron phosphate demand, if we take the disturbance of Tesla's export part (export about 15,000-40,000 units, 60kWh, fluctuations of about 900MWh-2.4GWh), the actual loading of lithium iron phosphate is also increasing rapidly.

Figure 3 Production capacity of lithium iron phosphate and ternary production from January to November 2021

From the overall data point of view, the production of power batteries in 1-11 months accumulated 188.1GWh, a cumulative increase of 175.5% year-on-year.

The cumulative output of ternary batteries was 82.4GWh, accounting for 43.8%, an increase of 106.1% year-on-year; the cumulative output of lithium iron phosphate batteries was 105.3GWh, accounting for 56.0%, an increase of 275.7% year-on-year.

From January to November, the installed power battery volume accumulated 128.3GWh, an increase of 153.1% year-on-year. The cumulative loading volume of ternary batteries was 63.3GWh, accounting for 49.3%, up 92.5% year-on-year; the cumulative loading of lithium iron phosphate batteries was 64.8GWh, accounting for 50.5%, up 270.3% year-on-year.

From this point of view, the proportion of lithium iron phosphate in the output is a priority response to market changes. From this point of view, the proportion of lithium iron in 2022 can increase the overall passenger car share to 70%, or even to 80%.

2

Power battery installed distribution

From the two charts of November and January-November to see the overall use, the largest amount of use in November or to go to pure electric passenger cars, installed capacity of 16.18GWh, accounting for 77.7%; with the amount of plug-in hybrid, the amount of battery use in November also reached 1.613GWh, fully reflecting the growth rate of this market segment, and also maintained a growth rate of 47.7% month-on-month.

From this point of view, the traditional bus market that uses lithium iron phosphate batteries is only 7.662GWh, and a large amount of lithium iron phosphate will be used in the passenger car market in the future.

Table 1 Where the power battery goes

Figure 4 The installed capacity of the power battery in November and January-November, the longitudinal axis unit is GWh

3

Lithium iron phosphate "eight immortals across the sea"

At present, lithium iron phosphate has become the mainstream design trend, and the current packaging form of lithium iron phosphate by major battery companies is as follows:

CATL era: mainly take two routes, in the passenger car to follow the original VDA 148 width, 220 width and Tesla custom width; and then through the electric bicycle demand inside the long cylindrical battery cell to do A00 level vehicles. Of these two routes, the former is to reuse all the production lines, and the latter is to be compatible with low capacity, reducing the investment in the production line.

BYD: Whether it is the battery of the EV blade and the blade module battery of the PHEV, BYD's current All in lithium iron phosphate Chinese battery companies, from the perspective of the packaging situation of passenger cars, the blade battery is centered on lamination technology, and then packaged in the form of a square shell package (which may use some aluminum-plastic film internally).

Guoxuan: Guoxuan began to do low-cost battery solutions in cylindrical lithium iron phosphate very early, and the biggest challenge of this technical route lies in the stability of quality, because the logic of a single lithium iron phosphate made of 15Ah poses a challenge to the quality system of the battery factory itself, especially in terms of welding. If lithium iron phosphate is not solved in the leakage link, in fact, safety is difficult to be guaranteed.

Hive Energy: On the most recent Hive Battery Day, they introduced a technical route to switch the entire series to short blades. I think this length of design, on the one hand, increases the universality of the application, but also takes into account the current technical process. This path can have some breakthroughs in product energy density and yield.

AVIC Lithium Battery: The One Stop battery of AVIC Lithium Battery is also a blade mode that switches from the original VDA route to laminated, that is, the original three companies that make square shell batteries have disembarked from VDA and transferred to the square shell lamination process.

I think that in 2022, with the white-hot competition of lithium iron phosphate, these lithium iron phosphate companies will carry out very fierce competition, of course, the advantages of the Ningde era are still very large. From the perspective of the breakthrough of The Fordy battery in 2021, there will be some changes in 2022, especially many automotive companies have begun to fully adopt lithium iron phosphate, which is objectively affected by the Ningde era, which has a decisive advantage in the middle nickel ternary.

Figure 5 Different packaging forms of lithium iron phosphate by major domestic enterprises

Summary: Power batteries will continue to differentiate into high nickel and lithium iron phosphate in 2022. In 2022, we will see that most companies will increase the proportion of lithium iron phosphate. This is due to the current cost structure, which will also narrow the gap in the material system of domestic first-line and second-line battery companies. The biggest gap between the previous Ningde era and other battery companies is in the electrochemical system.

bibliography:

1. Lithium Series 22: The Milestone of Europe's Lithium Resource Strategy - Eichmann, France, restarted the construction of salt lakes in Argentina

--END--