On February 13, Ford Motor announced that it will invest USD 3.5 billion to build a lithium iron phosphate battery plant in Michigan, USA. Some U.S. politicians are not very happy. Because it is provided by CATL with relevant technology and services.

This is a new attempt by Chinese enterprises to go overseas. Ford says it is in a "very global market" and believes newly produced batteries are eligible for subsidies under the Inflation Reduction Act. But resistance remains. Tens of billions of dollars have been announced for domestically made renewable energy, batteries and electric vehicles, many of which are under lengthy scrutiny. Microvast, a publicly listed company founded in Houston in 2006, plans to build a battery factory in Tennessee, and the subsidy qualification has received preliminary approval from the U.S. Department of Energy, but it has been subject to due diligence due on suspicion of having subsidiaries in China.

Globalization is torn apart, and countries are fighting among them. The technology of the Ningde era going to sea is only one of the epitomes. The global supply chain has entered a period of great divergence and restructuring, and in the process, Chinese entrepreneurs, investors and entrepreneurs have begun to make major adjustments.

In 2022, the United States imported more goods from Southeast Asia than China. Containers shipped from ASEAN to the United States increased by 20% compared with last year, and from China by 20% less. Chinese investment in U.S. innovation and entrepreneurship has come under greater scrutiny, with about 4 percent of transactions involving Chinese investors in the U.S. market but 15 percent filed with the Committee on Foreign Investment in the United States (CFIUS).

China is a beneficiary of globalization and still needs it. Now, facing global technology regulation and supply chain reshaping, China is accelerating its global expansion and promoting the spread of innovation around the world around its own technology accumulation, production capacity advantages and supply chain experience. Going out is no longer the export of products, but more about talents going abroad, capital going abroad, and production capacity going abroad.

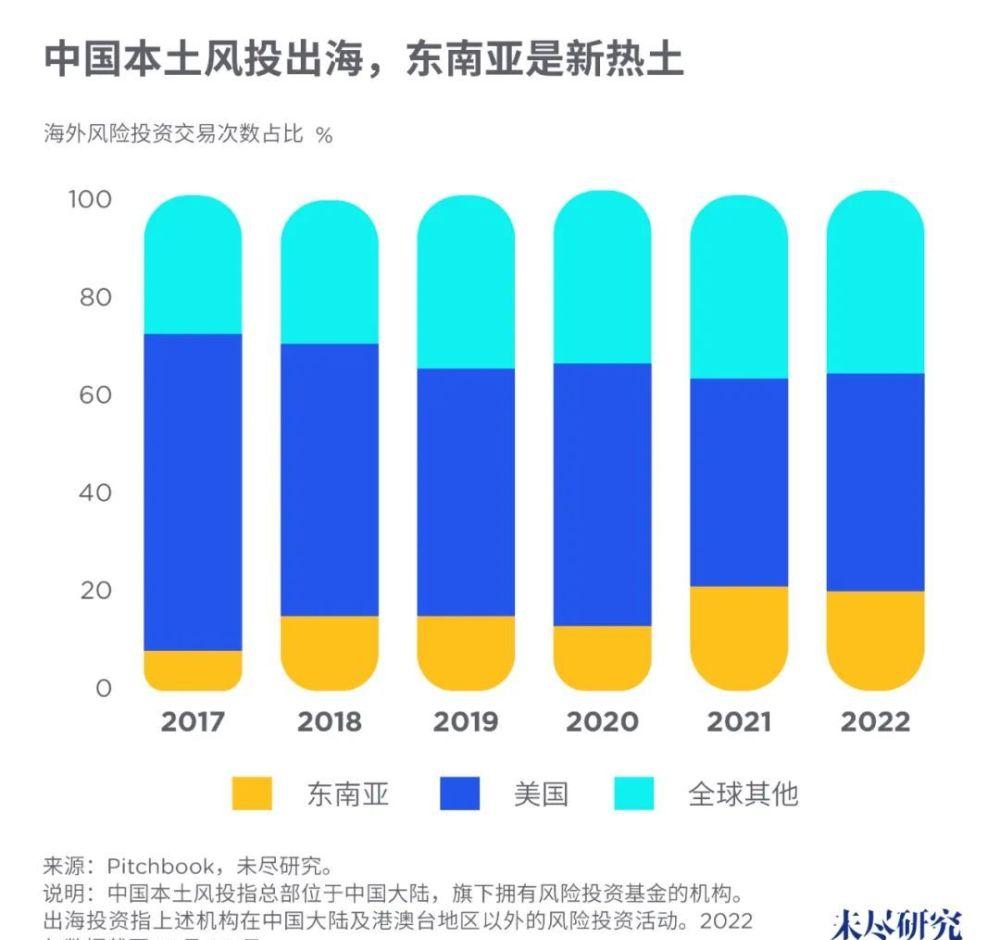

The most important stop is Southeast Asia. In 2022, Singapore became a high-frequency word on the lips of Chinese entrepreneurs and investors. Some VCs began to open Southeast Asia offices to recruit talent. Some of the new funds are designed to go overseas. In recent years, local Chinese VCs have accounted for an increasing proportion of overseas investment in Southeast Asian startups, and the United States has gradually fallen to about 50%.

There are many reasons to go to Nanyang. Many institutions that originally invested in Internet companies have hit hard technology investment barriers, domestic traffic dividends are disappearing, and entertainment, education and financial technology have encountered policy restrictions.

Southeast Asia is different, where there is new traffic, there is new media, which leads to new transactions. Southeast Asia has 10% of the world's population, 480 million active Internet users, and a per capita GDP growth rate of about 4 times the world average. TikTokShop expanded its business to six Southeast Asian countries this year. Singapore not only has top international universities, but is also reforming its visa policy to compete for innovative talent from around the world. Many Chinese entrepreneurs are looking for opportunities there, some previously working in the internet industry in Chinese mainland, others who have just studied abroad.

Some Chinese investors and entrepreneurs have followed cryptocurrency, blockchain and Web3 all the way to Nanyang. Southeast Asia has become an ideal market to validate the technology and serve consumers. There are currently more than 600 crypto or blockchain companies headquartered in Southeast Asia, with many founders with Chinese backgrounds. Chinese VCs are willing to bet on them. In the past two years, four of the top 10 local Chinese VCs leading the most investments in Southeast Asian startups have been new faces investing in crypto or blockchain.

In addition, Chinese venture capital firms are also eyeing fintech and e-commerce in the Southeast Asian market. When it comes to Chinese innovation in Southeast Asia, SHEIN and Shopee are mentioned. Their supply chain is in China and the market is overseas. Unlike the early business model of going overseas to copy China, today's cross-border e-commerce is more localized, and even deliberately downplays its own Chinese background. The Southeast Asian market is not a single whole, and the global configuration pays more attention to local conditions; The market is smaller, and the team is more motivated to expand into other markets. Many overseas entrepreneurs are also making a big fuss about the supply chain that takes China as the origin and spreads to the world. The Middle East Logistics iMile founded by the Chinese serves the Chinese cross-border e-commerce represented by SHEIN.

China's mature production capacity is also shifting to Southeast Asia. In the era of globalization, both direct investment in China and Chinese outbound investment have achieved rapid growth. However, as the global industrial chain gradually shifts from focusing on efficiency to taking into account security, the capital "flowing into China" and "investing by China" is also changing.

In 2012, FDI inflows to China were four times the level of China's OFDI. By 2021, the balance was tilted in favor of China's outward foreign direct investment, surpassing foreign direct investment. The Asia-Pacific region absorbs half of China's overseas direct investment. Southeast Asia is an important emerging market.

China is the world's factory, but it does not mean that all links need to be completed in China. Driven by costs, production capacity such as the textile industry has actively migrated to Southeast Asia. European and American countries' concerns about the supply chain being too concentrated in China have also made Chinese consumer electronics companies in the overseas giant industrial chain go out together. They are mostly labour-intensive, low- and medium-value-added sectors.

The Apple industry chain is accelerating its relocation. The number of production bases in the Chinese mainland of Apple's supply chain dropped from 47% in 2019 to 41% in 2020 and only 36% in 2021. The United States and Southeast Asia were the biggest winners, with the share of Apple production sites in these economies rising by more than 3% each.

The trend of supply chain migration continues. JPMorgan expects about 25 percent of Apple's products, including Mac PCs, iPads, Apple Watch and AirPods, to be made outside of China by 2025, up from 5 percent today.

But don't worry too much about this "de-Sinicization". Foundry companies such as Luxshare Precision are increasingly setting up production bases in Southeast Asia. Made in Vietnam, the core is still made in China. Just as the United States has always suspected that PV imports from Vietnam are still made in China. JPMorgan Chase believes that as the production capacity of Chinese companies goes overseas, the importance of Chinese companies in Apple's supply chain will rise against the trend, and by 2025, the iPhone manufactured by Chinese mainland companies will rise to more than 20%, more than 4 times that of today. The cycle of learning and innovating in manufacturing remains in the hands of Chinese companies.

China's advanced manufacturing is also going global. China dominates all links of the global electric vehicle industry chain, refining about 70% of the world's nickel and cobalt, 40% of copper, 60% of lithium, producing 70% of cathodes, 85% of anodes, more than 60% of separators and electrolytes, and more than 3/4 of the electric vehicle battery production capacity. This is a huge production capacity that is difficult to fully absorb in China's local market, and it must be oriented towards globalization.

Chinese power battery maker CATL, which has put into operation in countries such as Hungary, is the country's largest ever greenfield investment, exceeding the sum of other competitors. In addition, several battery separator film companies and battery material companies in China have announced production plans in Hungary. Hungary is now one of the global power battery manufacturing centers, close to the European automotive industry base. Envision Power has not only invested in and expanded power battery projects in Europe, North America and Japan, but also established zero-carbon industrial parks in the local areas to promote the green transformation of economy and industry.

Chinese enterprises represented by new energy have gone overseas and begun to build a more resilient global supply chain configuration. CATL is also exploring with local partners the possibility of establishing a battery material factory, hoping to tie it more deeply with globalization.

In the restructuring of global supply chains, some companies see opportunities for import substitution at home, while others see new opportunities to access foreign markets.