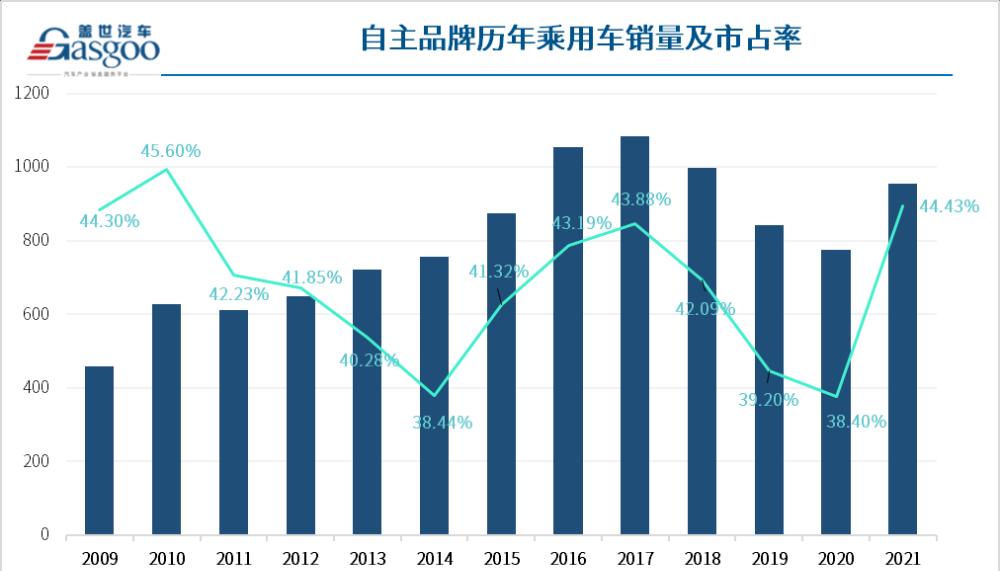

In 2021, the production and sales of mainland automobiles reached 26.082 million units and 26.275 million units, respectively, an increase of 3.4% and 3.8% year-on-year, successfully ending the downward trend of "three consecutive declines". Among them, self-owned brand passenger cars sold a total of 9.543 million units in 2021, an increase of 23.1% year-on-year, accounting for 44.4% of the total sales of passenger cars, a new high in the past decade, an increase of 6 percentage points over 2020.

Behind this, the sales of leading independent car companies such as Changan, Great Wall, and BYD have increased significantly, including the outstanding performance of the new energy sector, which is an important driving force. In addition, the continuous increase in delivery volume of new car manufacturers represented by Wei Xiaoli and others last year, as well as the surge in overseas exports, have also provided an important boost to the steady growth of the market share of autonomous passenger cars. It can be said that as the overall auto market continues to pick up, independent car companies are ushering in a highlight moment.

Image source: Gaz Cars

The new and old car-making forces have worked together, and the share of autonomy has increased significantly

Recently, various car companies have released sales data for 2021. Overall, mainstream independent passenger car brands have achieved good results, especially the head car companies, most of which have grown very strongly.

In terms of scale, last year, a total of four companies of independent passenger cars entered the million club, namely Geely, Changan, Great Wall and SAIC-GM-Wuling. Among them, Geely, although the overall sales volume did not increase significantly compared with the previous year, but in 2021, it successfully surpassed SAIC Volkswagen and squeezed into the annual passenger car company wholesale sales Top3 for the first time, second only to FAW-Volkswagen and SAIC-GM.

Changan, Great Wall and SAIC-GM-Wuling achieved sales of 1.2 million, 1,047,987 and 1,039,938 units in the passenger car segment in 2021, up 23.1%, 18.2% and 24.5% year-on-year, respectively, which can be described as the most important sales growth point of autonomous passenger cars in 2021. Among them, SAIC-GM-Wuling, GSEV (global small pure electric vehicle architecture) sales alone reached 452,238 units, a year-on-year surge of 160%, the main model Hongguang MINIEV contributed 426,452 units, the overall sales since the listing exceeded 550,000.

Chery, SAIC Passenger Car, BYD, etc., which are located in the second echelon, also performed very well. According to official statistics, in 2021, the passenger car segment of these three car companies sold 865,352 new cars, 800,767 units and 730,093 units respectively, an increase of 36.8%, 21.72% and 75.4% respectively year-on-year, which is also an important sales contribution point of the autonomous sector. It is particularly worth mentioning THAT BYD, thanks to the in-depth promotion of the electrification strategy, last year alone achieved sales of 603,783 new energy passenger cars, a sharp increase of 218.30% over the same period in 2019, so BYD once again won the 2021 domestic new energy passenger car sales championship.

In addition to the sharp red of the traditional independent passenger car sector, in the past 2021, the new car brands represented by Wei Xiaoli have contributed momentum to the increase in the market share of the independent passenger car sector with the continuous high delivery volume.

In particular, the three head new car brands, last year's total delivery volume exceeded 90,000, of which Xiaopeng Automobile even reached 98,155 units, close to the 100,000 mark, which is 3.6 times the delivery volume in 2020. Nezha, Weima and Zero Run, which ranked second in the company, also caught up, achieving total deliveries of 69,700, 44,200 and 43,100 units, respectively.

In contrast, joint venture brands are the opposite development trend. Affected by the continuous impact of chip shortages, rising raw material prices and repeated epidemics, sales of mainstream joint venture car companies have declined by different margins last year. For example, North and South Volkswagen, new car sales fell by more than 10% in 2021, which made the total sales of German brand passenger cars in China last year only reach 4.425 million units, with a market share of about 20.6%, down 3.3% compared with 2020.

In terms of Japanese brands, in addition to the relatively good overall performance of FAW Toyota and GAC Toyota, the sales of passenger cars of several other mainstream car companies have also declined. Correspondingly, the market share of Japanese passenger cars in China also declined last year, only 20.6%, with total sales of about 4.425 million units, the same as the Ashkenazi brand.

In terms of other factions, the total sales of passenger cars in China in 2021 for American brands will be about 2.191 million units, with a market share of 10.2%, an increase of 0.6% over 2020; the total sales of Korean brands of passenger cars will be about 730,000 units, with a market share of 3.4%, down 0.1% from the previous year. Total sales of French-brand passenger cars totaled approximately 129,000 units, representing a market share of 0.6% and an increase of 0.3%.

Traditional car companies have accelerated their transformation, and new energy vehicles have become important growth poles

Riding on the east wind of electrification development, new energy vehicles are becoming a growth pole that cannot be ignored in the autonomous sector.

Last year, the production and sales of new energy vehicles in China reached 3.545 million units and 3.521 million units, respectively, an increase of 1.6 times year-on-year. Among them, Chinese brand new energy passenger cars alone sold 2.476 million units, an increase of 1.7 times year-on-year, accounting for about 74.3% of the total sales of new energy passenger cars.

Analyzing this part of the increment, in addition to the contribution of a number of new car brands, traditional car companies are also indispensable. Under the trend of new energy tide, in the past two years, major traditional car companies have accelerated the electrification transformation, promoted core technology research, accelerated the mass production and iteration of new products, and driven the traditional independent new energy passenger vehicles to enter the outbreak period.

According to statistics, the new energy passenger car sector of many independent brands achieved triple-digit growth last year. The first to bear the brunt are BYD and SAIC-GM-Wuling, with their active layout in the field of electrification, these two companies continued to occupy the top two positions in the total sales volume of new energy manufacturers last year. In addition, the new energy passenger car sector of great wall, SAIC, GAC, Chery, Geely, Changan and other independent brands has also achieved remarkable results in 2021, of which the sales growth rate of Changan Automobile's related sectors has even reached 319%, which can be described as leading the camp of independent new energy passenger cars.

In terms of subdivision models, the production and sales of pure electric and plug-in hybrid vehicles will show a high-speed growth momentum in 2021. According to the statistics of the China Automobile Association, among the 3.334 million new energy passenger car sales last year, pure electric vehicles were 2.734 million units, an increase of 173.5% year-on-year; plug-in hybrid vehicles were 600,000 units, an increase of 143.2% year-on-year. Behind this, many traditional car companies are accelerating the hybrid layout to build a development pattern of "hybrid + pure electricity" two-wheel drive.

For example, Great Wall Motors also carries out saturation precision investment in the field of pure electricity and hybrid. In terms of pure electricity, Great Wall Motors released Dayu battery technology, and the hybrid field launched a dual-motor hybrid hybrid architecture product - lemon hybrid DHT, and has launched a number of new cars such as Macchiato DHT-PHEV and Latte DHT around the architecture. In addition, Geely, Changan, BYD, GAC, SAIC, etc. are also competing to carry out hybrid layouts and launch hybrid platforms and models.

And unlike the new energy market in previous years, which mainly relies on subsidies to pull strongly, with the continuous enhancement of independent new energy vehicle product strength, especially through the deep integration with intelligence, giving end users a completely different car experience compared with traditional fuel vehicles, the overall acceptance of pure electric passenger cars by C-end users is actually constantly improving.

According to the analysis data, the average mileage of pure electric passenger cars has increased from 253 kilometers in 2016 to more than 400 kilometers in 2021. In addition to the continuous relief of battery life anxiety, in terms of intelligent configuration, the speed of new energy vehicles is also significantly faster than that of fuel vehicles. At the beginning of 2021, Xiaopeng Automobile announced the launch of Pilot 3.0, which can realize the high-speed scene navigation auxiliary driving function, and then Weilai also announced that its latest automatic driving system NAD will be installed on the first flagship sedan ET7, and ideally launched the navigation assistance noA function at the end of 2021, which is free to users.

Under the guidance of these new consumer trends, consumers' quality and brand satisfaction with new energy vehicles are also continuously improving, driving the transformation of the new energy vehicle market from policy acceleration to deep market-oriented competition. According to the ministry of public security traffic insurance data, in the past 12 months, the domestic new energy passenger car terminal sales (insurance volume) was 481,100 units, an increase of 113.11% year-on-year, of which the rental market sales of 61,400 vehicles, accounting for 12.8%; private market sales of 371,000 vehicles, accounting for 77.1%. In the first 11 months of 2021, private users in the new energy vehicle market accounted for as much as 78%, and C-end users pulled significantly.

Future growth can be expected, and 2022 is expected to continue to soar

In the past for a long time, joint venture brands have been in a dominant position in the market, but with the deepening of the "four modernizations" reform represented by intelligence and electrification, independent brands have begun to usher in a new round of development opportunities, and the substantial increase in sales volume and market share of independent plates in 2021 is a good proof.

Next, with the gradual alleviation of external factors such as chip shortage and the new crown epidemic, and the continuous consolidation of product strength and brand power by independent brands internally, the market share of independent brands is expected to further increase. According to Ping An Securities forecast data, China's automobile sales are expected to reach 28 million units in 2022, an increase of 6.6% year-on-year, of which new energy vehicles are expected to reach 5.1 million units. In the long run, the annual sales of mainland automobiles are expected to reach 40 million units, and the share of independent brands is expected to reach 60% to 70%.

Perhaps at present, this forecast is slightly radical, but it is undeniable that the overall competitiveness of independent brands is indeed continuing to improve. And for the future growth, everyone is also full of confidence, which can be glimpsed from the 2022 sales targets released by major car companies recently.

According to Geely's previous announcement, its board of directors has set a sales target of 1.65 million units in 2022 (including Lynk & Co brand cars), an increase of about 24% from the total sales achieved in 2021. If Geely can successfully complete the goal, according to the current market trend, it is likely to go further on the list of car companies.

Image source: Geely Auto

Focusing on intelligence and electrification, Geely is continuing to build a hard-core "science and technology ecosystem" to help achieve the goal of double carbon. To this end, Geely has successively carried out layouts in the fields of new energy technology, on-board chips, Internet of Vehicles, and automatic driving, and has made overall efforts in the fields of passenger cars, commercial vehicles, and shared travel, exploring diversified new energy technologies such as pure electricity, hybrid, methanol, and power exchange to further enhance the overall competitiveness.

BYD was exposed to lock in sales targets of 1.2 million vehicles in 2022, a 64.4% increase compared with the overall sales in 2021, of which 600,000 were pure electric models and 500,000-600,000 plug-in hybrid models were expected. Considering that in 2022, BYD will have a number of new models such as Han DM-i, Yuan PLUS and destroyer on the market, while the blade battery production capacity continues to increase, coupled with the continuous improvement of the external new energy vehicle consumption environment, BYD is also stable for this goal.

Also full of confidence for 2022 is the red flag. In 2021, Hongqi's total sales reached 300,600 vehicles, an increase of 50% year-on-year, ranking first in the growth rate of high-end luxury brands. It is precisely with this "confidence" that in 2022, Hongqi proposed a sales target of 50% on the basis of last year's total sales, that is, 450,000 to 500,000 vehicles.

In fact, not only is the development trend in the domestic market good, but also the global perspective, the voice of independent car companies is also increasing. Over the past few years, China's auto exports have been hovering around 1 million units, with the best year reaching 1.041 million units in 2018. However, in the past 2021, China's automobile exports reached 2.015 million units, breaking through the 2 million mark for the first time, doubling the year-on-year increase in 2020; passenger car exports totaled 1.614 million units, an increase of 110.5% year-on-year.

Among them, the export performance of new energy vehicles was particularly eye-catching, reaching 310,000 units, an increase of 304.6% year-on-year. Specific to new energy passenger vehicles, the total export volume in 2021 was 296,000 units, an increase of 329.5% year-on-year.

As far as car companies are concerned, independent brands such as SAIC, Chery, Great Wall, Changan, Dongfeng, and Geely have achieved good performance. According to the sales report, SAIC Motor's overseas sales in 2021 were 697,000 units, exports were 598,000 units, and overseas bases produced and sold 99,000 units, an increase of 78.9% year-on-year. Among them, saicel passenger car exports reached 290,000 units in the whole year, an increase of 68% year-on-year. Other car companies, most of the export growth rate has also reached triple digits, the future is expected to further growth.

At present, a new round of scientific and technological revolution represented by intelligence and electrification is gradually entering the deep water area, although there are many uncertainties in it, but it has also brought many new development opportunities to the industry. In particular, autonomous car companies are opening up a new round of competition by actively embracing smart electric vehicles. It can be said that the best era of independent car companies is coming.