Author: Qingfeng

Editor: Liu Pengyao

Editor: Yu Mo

In the blink of an eye, the controversial new energy exclusive car insurance has been landed for a month, and its emergence has made the fiery new energy automobile industry tremble. Some people say that exclusive car insurance is a sign of the industry's complete supporting services, and some people say that this is a big test for new energy vehicles...

Let's briefly sort out the development of the matter:

On December 14 last year, the China Insurance Industry Association issued the "Exclusive Clauses for Commercial Insurance of New Energy Vehicles of the China Insurance Industry Association (Trial)".

Three days later, on December 27, the Shanghai Insurance Exchange launched the new energy vehicle insurance trading platform, and the first batch of new energy vehicle exclusive insurance products of 12 property insurance companies, including PICC Property & Casualty, Ping An Property & Casualty, and CPIC Property & Casualty, were listed.

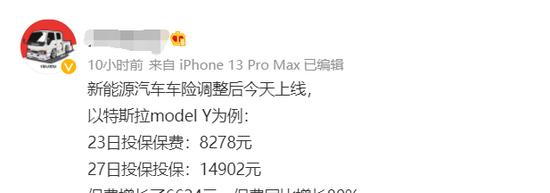

At that time, some car owners posted insurance policies on Weibo, showing that they bought Tesla Model Y, and the cost of insurance on December 23, 2021 was 8278 yuan, and after the exclusive new car insurance was launched, the premium rose to more than 14,000 yuan, an increase of up to 80%.

Since then, industry media including Xiaoxiang Morning News, Beiguo Finance, Tiantian Finance, etc. have tracked and reported, and widely disseminated through Channels such as Tencent and Sina, and the content is mainly aimed at Tesla's premium increase.

However, we cannot accurately judge the authenticity of the above news, because Tesla officials also responded through the Beijing News, Zhongxin Jingwei and other media that from the latest statistics, Tesla vehicle premiums rose by about 10%, and the premiums of high-performance models that are more concerned are within 20% from a national perspective. That said, Tesla believes that the premium increase is not so exaggerated, most of it is up about 10%.

In addition, some local new energy brands have also encountered rising premiums, but they have not stirred up waves as big as Tesla.

To sum up, the more high-end; the more expensive new energy models, the greater the increase in premiums, which can't help but make the industry bearish, thinking that it has hit the new energy vehicle market that is in the blowout period, and even more, put forward the "2022 new energy vehicles encountered an inflection point" statement.

Is it reasonable that a mere rise in premiums will cause an uproar in an industry? From all kinds of bearish emotions, it is not difficult to find that the new energy automobile industry in the blowout is not "not afraid of the sky, the ground is not afraid", on the contrary, the anxiety of the entire industry is very obvious.

Behind the price increase - trust temptation

In today's streets and alleys, the figure of new energy vehicles can be seen everywhere. A closer look reveals that they are made up of three camps:

First, the overseas car-making forces represented by Tesla occupy the high-end market by virtue of high-end brand awareness, design and technical advantages. It is worth mentioning that Tesla achieved a "dimensionality reduction blow" through the overall price reduction strategy last year, which had a great impact on local competitors.

Second, the new local car-making forces represented by Weilai, Xiaopeng and Ideal have Internet genes and have influence in the "Z generation" high-end market, especially Weilai. However, these three are homogeneous in terms of product strength, and many consumers say that it is difficult to distinguish from the appearance.

Third, the economic and practical faction represented by Wuling Hongguang mainly benefited from third-tier cities and townships, and last year it was also an Internet celebrity brand.

The new exclusive car insurance regulations that have been implemented have the greatest impact on the first two, especially making Tesla's premium rise the most. In this regard, industry insiders generally recognize the following two reasons:

First, new energy vehicles and fuel vehicles are fundamentally different, therefore, the mechanism of failure, maintenance, and claim settlement are different, and there is another set of pricing systems.

Compared with the provisions of fuel vehicle insurance, new energy vehicle insurance includes the core part of the "three electricity" system (battery and energy storage system, motor and drive system, other control systems), and also includes vehicle damage during vehicle driving, parking, charging and operation; and adds three new energy vehicle-specific additional insurance: additional external grid fault loss insurance, additional self-use charging pile loss insurance and additional self-use charging pile liability insurance.

Second, from the perspective of past experience, Tesla's claim rate and claim amount are the highest, reaching 1:1.4. Some people say that this is equivalent to charging a dollar premium to lose 1.4 yuan, so the premium price of Tesla's entire series of models has increased.

Moreover, tesla's all-aluminum integrated body can only be replaced in one piece after damage, so the amount of compensation after insurance is more expensive than other models. What's more, in recent years, there have been more reports of Tesla accidents, and the whole industry has hidden worries about its failure.

However, we have to admit the fact that Tesla's accident frequency is based on high market share. In layman's terms, the accident frequency of rare brand models on the market is definitely low.

If we speculate according to this logic, next, with the further popularization of new energy vehicles, there is a probability of occurrence in various accident situations that we have never heard of before, resulting in a prolonged claim time; the increase in costs may still lead to further increases in premiums.

This is a test of trust between consumers and brands when a new field of product enters a new market. Regarding car insurance and claims, the two sides have not established mutual recognition standards before, so that when exclusive car insurance appears, they continue to complain. After all, many car owners are using the insurance standards of oil trucks to look at the exclusive car insurance of new energy vehicles.

In the final analysis, the overall technology, performance, marketing, service and other aspects of new energy vehicles are still in the exploratory stage, and the price sensitivity of all parties is high.

The continuation of industry anxiety - real knife competition

In the midst of the spit, car owners successfully transmitted their premium anxiety to the new energy vehicle brand.

In order to offset everyone's wavering desire to buy due to premiums, some brands that focus on high-end styles have responded in advance.

For example, at the brand event at the end of last year, a local car-making new force specifically explained the exclusive car insurance: first promised that the premium adjustment of the brand's models was not large, and then said that it would continue to pay attention to the subsequent price changes.

This commitment is tantamount to giving price-sensitive consumers a "reassuring pill". Specifically, the brand has launched a related "service portfolio" that includes three additional insurances added to the exclusive car insurance (external grid fault loss insurance, self-use charging pile loss insurance and self-use charging pile liability insurance).

How wonderful is this response? Not necessarily, it looks more like subsidizing car owners out of their own pockets, trying to maintain their hard-won market position. As for the future? It is also unclear and can only be observed with caution.

This practice is not unique, and many new local car-making forces have similar countermeasures.

Such a real knife competition is because the new local car-making forces are in a competitive situation, and the leaders are worried that a new exclusive car insurance policy will break the situation; the laggards hope to take advantage of this to overturn.

It is speculated that these new car-making forces will maintain subsidies based on exclusive car insurance for a period of time.

In the final analysis, the entire new energy automobile industry, especially the local car-making forces, has been in a state of anxiety. Before today's "premium anxiety," they also experienced "mileage anxiety," "charging anxiety," and "safety anxiety."

Specifically, "mileage anxiety" and "charging anxiety" originate from the product technical problems encountered in the application and promotion process of new energy vehicles, which are mainly reflected in the short battery mileage, long charging time, and difficult to find charging piles, which have always plagued car owners and become the biggest obstacle to the popularity of new energy vehicles.

To this end, car companies have invested a lot of real money and silver to improve the level of endurance, and some head forces have begun to build their own charging piles, or develop new power exchange technologies, just to improve the driving experience of car owners. Of course, this kind of investment is often in the order of 100 million yuan, which increases the financial burden of car companies. Looking at the new energy vehicle companies that have been listed, all of them are in a state of loss.

However, judging from last year's market feedback, new energy vehicles have another "safety anxiety". Last year, there were a number of battery fires and burning accidents, which also caused casualties. Although the causes of accidents involve various aspects, industry experts mostly point to the battery itself and the design of the vehicle.

If you can't control your own accident problems and reduce maintenance costs, the premium of new energy vehicles (especially high-end models) is difficult to reduce, and car companies have to continue to invest in subsidies.

On the contrary, Tesla, which has achieved a "dimensionality reduction strike", has not deliberately taken subsidy measures. Presumably, it needs to verify how well the market is sticking to the shock of rising premiums.

The conjecture of exclusive car insurance - the industry game

Let's understand this problem from the perspective of insurance business.

Based on the large investment of car companies, the current high-end new energy vehicles are equipped with many high-intelligence devices, and insurance companies lack knowledgeable talents in this regard. Once an accident occurs, it is more troublesome to settle the claim and determine the loss. It is reported that insurance companies set insurance rates and service standards based on data, including driving behavior data and vehicle attribute data. At present, the relevant prices of new energy vehicles and underwriting claim data resources have not been obtained by insurance companies, which is not conducive to premium calculation.

"You see this car, a body of radar, how do we determine the loss?" An insurance practitioner pointed to a new new energy vehicle and said helplessly.

Due to the weakness of the profession, the cost of maintenance claims for new energy vehicles has been dominated by car companies, so that insurance companies have always been in a passive situation.

Shenwan Hongyuan report data shows that the current loss rate of new energy vehicle insurance is close to 85% on average, and the industry is facing greater underwriting loss pressure. Insurers do not have the ability to strike a balance between service and profitability at this stage.

More seriously, the overall premium of car insurance has been reduced. According to the operation of the insurance industry in the first four months of 2021 released by the website of the Banking and Insurance Regulatory Commission, the growth rate of automobile insurance premiums fell by 6.86% year-on-year, accounting for 50.16%, and the entire insurance industry was in a state of loss.

Therefore, the launch of new energy exclusive car insurance is a necessary measure for the insurance industry to maintain the healthy development of its own business, and it is also one of the means to launch checks and balances on the new energy automobile industry.

From another point of view, the rise in premiums that overrides the heads of car owners is the price of the orderly integration of the new energy automobile industry and the insurance industry. New energy vehicle companies choose to subsidize car owners and take the initiative to pay for this cost, which makes sense from the truth, after all, the new energy industry is in a hot track, and the ability to attract hot money is stronger.

New energy exclusive car insurance was launched for a full month, and the effect has not yet been immediate. Next, based on the accumulation of data from both sides, insurance companies will have more resources at their disposal.

For consumers, the emergence of checks and balances is always a good thing, at least it can force new energy vehicle companies to stabilize product performance and minimize accidents caused by their own problems. (Text/Zhiton Qingfeng)