(Report Producer/Author: CITIC Construction Investment/Lv Juan)

First, new energy vehicles and power battery tracking

1.1 Domestic: leading the world

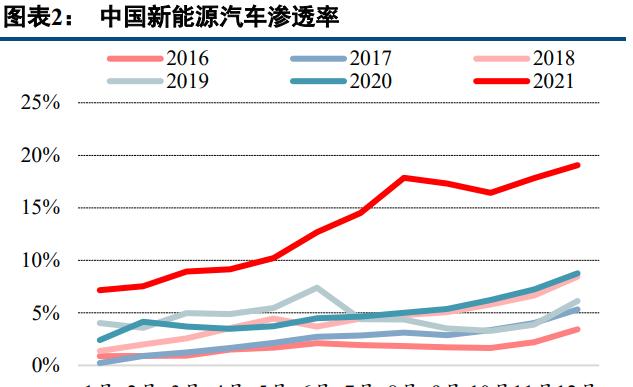

Domestic new energy vehicle production, sales and penetration rate: According to the China Association of Automobile Manufacturers, the sales of new energy vehicles in December 2021 were 498,000 units, an increase of 113.9% year-on-year. Among them, the production and sales of pure electric vehicles reached 416,000 units, an increase of 120.5% year-on-year, and the sales of plug-in hybrid vehicles were 82,000 units, an increase of 120.5% year-on-year. The penetration rate of new energy vehicles is 19.1%, of which the domestic retail penetration rate of new energy passenger cars is 22.6%.

For the whole year of 2021, domestic sales of new energy vehicles were 3.521 million units, an increase of 157.5% year-on-year, of which pure electric vehicle sales were 2.734 million units, an increase of 173.5% year-on-year, and plug-in hybrid vehicle sales were 600,000 units, an increase of 143.2% year-on-year. The penetration rate of new energy vehicles was 13.4%, an increase of 8pct year-on-year, and the domestic retail penetration rate of new energy passenger cars was 14.8%, an increase of 8pct year-on-year.

Power battery output: In December 2021, China's power battery production was 31.6GWh, an increase of 109.0% year-on-year. From January to December 2021, China's power battery production accumulated 219.7GWh, an increase of 163.4% year-on-year.

Power battery installed capacity: In December 2021, China's power battery installed capacity was 26.2GWh, an increase of 102.4% year-on-year. From January to December 2021, China's power battery installed capacity accumulated 154.5GWh, an increase of 142.8% year-on-year.

Installed capacity of power batteries by enterprise: In December 2021, the top five domestic power battery installed capacity were Catalonia Times, BYD, Zhongxin Aviation, Guoxuan Hi-Tech, LG New Energy, with installed capacity of 14.58, 3.73, 1.55, 1.42, and 0.89GWh, accounting for 55.6%, 14.2%, 5.9%, 5.4%, and 3.4% respectively. From January to December 2021, the top five domestic power battery installed capacity were CATL, BYD, Zhongxin Aviation, Guoxuan Hi-Tech and LG New Energy, with installed capacity of 80.51, 25.06, 9.05, 8.02 and 6.25GWh, accounting for 52.1%, 16.2%, 5.9%, 5.2% and 4.0% respectively.

1.2 Global: The trend toward electrification is unstoppable

From the perspective of global new energy vehicle sales: According to INSIDE EVs data, the number of new energy passenger car registrations in The world in November 2021 was 720,000 units, an increase of 72% year-on-year, a new monthly high, and the penetration rate reached 11.5%. Among them, there are about 520,000 pure electric vehicles, with a penetration rate of 8.1%, and about 200,000 plug-in hybrid vehicles, with a penetration rate of 3.4%. From January to November 2021, global sales of new energy passenger cars exceeded 5.57 million units, and the penetration rate increased to 8.1%.

Power battery installed capacity: According to SNE Research data, in November 2021, cathedale, LG, BYD, Panasonic, SK On power battery installed capacity of 12.1, 5.5, 3.6, 2.9, 1.9GWh, respectively, the market share was 36.7%, 16.7%, 10.9%, 8.8%, 5.8%, an increase of 140.3%, 34.1%, 138.3%, 15.7%, 108.8%, respectively. From January to November 2021, the installed capacity of CATL, LG, Panasonic, BYD and SK On power batteries was 79.8, 51.5, 31.3, 22.5 and 14.6GWh, respectively, with market share of 31.8%, 20.5%, 12.5%, 9.0% and 5.8%, respectively, an increase of 180.1%, 90.0%, 36.5%, 192.1% and 119.3% respectively.

Second, the battery plant expansion planning tracking

2.1 CATL era expansion tracking: 836GWh is expected in 2025

On December 30, 2021, CATL announced that it intends to invest in the construction of the seventh to tenth phase of the power battery Yibin Manufacturing Base in Sanjiang New Zone, Yibin City, Sichuan Province, through its wholly-owned subsidiary Sichuan Times New Energy Technology Co., Ltd., with a total investment of no more than RMB 24 billion. According to our statistics, the planned investment scale of CATL (including joint venture) power batteries in 2025 is about 836GWh.

2.2 Honeycomb Energy Expansion Tracking: 600GWh expected in 2025

On December 8, 2021, Hive Energy held the second Battery Day conference, at which the "leading bee 600" strategy and four support strategies for 2025 were released, announcing that the company will occupy 25% of the global market share in 2025 and challenge the goal of 600GWh global production capacity (previously more than 200GWh). At the same time, a new category of short knife batteries has been launched in terms of products, and electric global short knives will be implemented in the future.

2.3 China Innovation Airlines Expansion Tracking: 500GWh is expected in 2025

On December 29, 2021, the CSRC disclosed that it had received the "Approval of Overseas Initial Public Offering of Shares (Including Ordinary Shares, Preferred Shares and Other Stocks and Derivative Forms of Stocks)" from China Innovation Aviation Technology Co., Ltd., and China Innovation Airlines will officially launch its IPO in Hong Kong. The infusion of future capital will help its expansion plans of 500GWh in 2025 and 1000GWh in 2030.

2.4 LG Expansion Tracking: 430GWh expected in 2025

On November 30, 2021, the Korean exchange said that the LG Energy Solution IPO has received preliminary approval or will be listed at the end of January 2022. The IPO raised up to $10.8 billion to support its planned capacity of 430GWh in 2025.

Third, lithium battery equipment dynamic tracking

3.1 Lithium battery equipment winning bid tracking

The large-scale expansion project of the head battery enterprise has landed, driving the growth of demand for lithium battery equipment. In 2021, the number of lithium battery production equipment bidding projects is obvious, and the new orders of related lithium battery equipment companies in the industry hit a record high. According to the disclosed bidding situation, as of January 2022, the major domestic battery companies and equipment companies announced that the amount of winning orders exceeded 20 billion yuan. As battery manufacturers continue to expand production, equipment orders will be further increased.

3.2 Equipment development trend analysis

From the overall development trend of lithium battery equipment: the degree of integration of production lines has increased, and the requirements for equipment intelligence and digitization are getting higher and higher; equipment efficiency and equipment stability are improved, the life cycle of equipment is increased and the malleability is improved; equipment components are further localized, and equipment prices are further reduced.

From the perspective of specific equipment parameters: it is expected that the specifications and efficiency of the main equipment in the middle of the front section will be greatly improved in the future, such as the coating width increased from the previous 1-1.2 meters to 1.5-1.8 meters, the winding speed from 12-16ppm to 25-32ppm, the lamination speed from 0.25s/pcs to 0.125s/pcs, and the whole line production capacity from 2GWh to 4GWh.

3.3 Tracking process changes such as lamination, series formation, 4680 cylinder, etc

3.3.1 Laminated Device Trend Update

The lamination process has advantages, and the lamination machine is the key equipment. The winding/laminating process is an important part of the battery assembly process in the production of lithium batteries, and its equipment value accounts for about 13% of the entire line of equipment, which is the core equipment of the middle process of lithium battery production. Comparatively speaking, in the production process of soft packs and square batteries, the use of laminated technology can effectively improve the energy density, cycle life and safety of lithium batteries, while reducing internal resistance and better meeting the terminal product needs of power batteries. However, the lamination process mainly faces problems such as low efficiency, complex process, poor alignment, and low yield.

The domestic lamination machine continues to improve and iterate, and the performance continues to improve. At present, the lamination process is mainly used in soft pack batteries, and the traditional consumer electronics leading enterprises represented by LG have a leading position in the lamination machine and the rolling machine. Some domestic head battery manufacturers such as BYD, Hive Energy, and Zhongxin Airlines have begun to use laminated equipment in the production of square batteries. The trend of downstream battery factory process replacement has forced equipment companies to actively seek technological breakthroughs in laminated equipment in view of the pain points of lamination technology. Since Q4 2020, mid-section equipment layout enterprises such as Pilot Intelligence, Kerui Technology, Yinghe Technology, Li Yuanheng, etc. have successively launched iterative products of laminated equipment from different routes.

3.3.2 Series into trend updates

The tandem formation has cost advantages, and the penetration rate will continue to increase. Chemical formation is the core process of the post-processing stage of lithium battery production, and the SEI film formed in the process has a crucial impact on the key properties such as lithium battery capacity, life and consistency. The chemical process is essentially to charge and discharge the battery cell, and the voltage and current control capabilities in the process reflect the competitiveness of the chemical equipment. At present, the more mature chemical formation technology in the industry adopts parallel mode to accurately control the voltage under constant voltage conditions, and the accuracy is relatively easy to grasp. The series route abandons the precise control of the voltage and changes to constant current charge and discharge. Relative to parallel connection, series can be achieved: charging and discharging efficiency in the power output range is increased by 15% to 30%; the number of cables is small, the cost is reduced, and the layout is convenient. Therefore, the series can help customers reduce costs and increase efficiency.

We believe that under the pressure of battery manufacturers to reduce costs, the subsequent penetration rate of tandem technology is expected to be further improved.

3.3.3 4680 Large cylindrical trend update

Battery companies accelerate the layout of large cylinders, large cylinders or large-scale replacement of small cylinders. In September 2020, Tesla released the 4680 battery, the most important feature of the 4680 compared to the traditional cylinder is that the internal structure adopts a stepless ear design, the battery cell capacity is five times that of the small cylindrical battery, which can increase the cylindrical range of the corresponding model by 16%, and the charging and discharging efficiency is 6 times higher than that of the small cylindrical battery.

Tesla 4680 Progress Tracking (quoted from Self-Aware Self-Media Zhu Yulong):

There are 4 self-supply factories that cooperate with Tesla to produce 4680s:

California, USA (development base for 4680 batteries): The first line of Tesla's development and trial.

Berlin, Germany: Planning to match the production capacity of the german factory, the production capacity is estimated to be more than 20GWh, and the actual capacity will begin to be released after Q2 2022. (Source: Future Think Tank)

Texas plant, USA: Capacity estimated at 60GWh, equipment began to enter the production line, is expected to start trial production in Q2 2022.

Pending factory.

Panasonic 4680 Progress Tracker:

In October 2021, Panasonic Battery Division CEO Kazuo Tadanobu revealed that Panasonic plans to start testing the production of new batteries at its Plant in Japan in March 2022.

In November 2021, Kazuo Tadanobu, CEO of Panasonic Battery Division, revealed that in terms of product development, the 4680 technical goals have been basically achieved and large-scale production trials will be conducted.

BAK 4680 Progress Tracker:

In 2019, BAK began the development of large-size cylindrical batteries.

In March 2021, BAK debuted the full-pole ear 4680 large cylindrical battery in China

On December 21, 2021, Dr. Lin Jian, chief scientist of BAK Battery, said at the annual meeting of Gaogong Lithium Battery that BAK Battery 46X0 series large cylinder batteries cover 80mm to 120mm, and the energy density reaches 270WH/kg, of which 4680 large cylindrical batteries are expected to be mass-produced in 2022.

Ewell Lithium Energy 4680 Tracking:

In September 2021, at the forum "Lithium Battery Technology and Breakthrough for Two-Wheeled Electric Vehicles", Yiwei Lithium Energy Zheng Weigong delivered a keynote speech entitled "Application of Large Cylindrical Lithium Iron Phosphate Battery on Electric Two-Wheeler", and Ewell Lithium Energy will provide full-pole ear large cylindrical lithium iron phosphate batteries for two-wheelers.

On November 5, 2021, at the opening ceremony of the Jingmen Power Energy Storage Battery Industrial Park, Liu Jincheng, chairman of Ewell Lithium Energy, said: "The large cylindrical battery project to be built in Jingmen may be the first mass production base of 4680 and 4695 batteries in the world.

Fourth, how to expect domestic lithium battery production capacity?

4.1 There may be a shortage of lithium battery production capacity in Europe and the United States

4.1.1 Europe and the United States lithium battery demand: 827GWh under the neutral assumption of 2025

4.1.1.1 Power Battery Demand: 747GWh under the 2025 Neutral Assumption

Hypothesis (neutral):

From 2022 to 2025, European car sales will increase by 2% per year, the penetration rate of new energy vehicles will reach 30% in 2025, and the number of bicycles will increase from 60kWh in 2021 to 68kWh in 2025.

From 2022 to 2025, total U.S. car sales will increase by 2% per year, the penetration rate of new energy vehicles will reach 25% in 2025, and the number of bicycles will increase from 60kWh in 2021 to 68kWh.

Conclusion: The installed power battery demand in Europe and the United States in 2025 will be 410 and 337GWh, respectively, totaling 747GWh.

Analysis of the sensitivity of the installed capacity of power batteries in Europe:

Under pessimistic assumptions: if the penetration rate of new energy vehicles in Europe reaches 30% in 2025, and the power of EV passenger car bicycles reaches 60kWh, then the corresponding power battery installed capacity is 327GWh.

Under the neutral assumption: If the penetration rate of new energy vehicles in Europe reaches 35% in 2025, and the power of EV passenger car bicycles reaches 65kWh, then the corresponding power battery installed capacity is 410GWh.

Optimistic assumptions: If the penetration rate of new energy vehicles in Europe reaches 40% in 2025, and the power of EV passenger car bicycles reaches 70kWh, then the corresponding power battery installed capacity is 502GWh.

Sensitivity analysis of installed capacity of power batteries in the United States:

Under the pessimistic assumption: if the penetration rate of new energy vehicles in the United States reaches 25% in 2025, and the power of EV passenger car bicycles reaches 60kWh, then the corresponding power battery installed capacity is 260GWh.

Under the neutral assumption: If the penetration rate of new energy vehicles in the United States reaches 30% in 2025, and the power of EV passenger car bicycles reaches 65kWh, then the corresponding power battery installed capacity is 337GWh.

Optimistic assumptions: If the penetration rate of new energy vehicles in the United States reaches 35% in 2025, and the power of EV passenger car bicycles reaches 70kWh, then the corresponding power battery installed capacity is 422GWh.

Europe and the United States power battery installed capacity sensitivity measurement summary:

Under the pessimistic assumption: 587GWh; under the neutral hypothesis: 747GWh; under the optimistic assumption: 924GWh.

4.1.1.3 Two-wheelers, power tools, etc.: 20GWh in 2025

Two-wheelers, power tools and other products are produced less in Europe and the United States, most of them rely on imports, we estimate that these products in the local region in 2025 the demand for batteries is about 20GWh.

4.1.1.4 Lithium battery demand summary: 827GWh under the 2025 neutral assumption

Summarizing the above calculations, the pessimistic, neutral and optimistic assumptions of 2025 European and American lithium battery demand are 667GWh, 827GWh and 1004GWh, respectively.

4.1.2 European and American lithium battery production capacity judgment: 547GWh in 2025

2025 European and American lithium battery production capacity judgment: According to Benchmark Mineral Intelligence forecast, in 2025, the local lithium battery production in Europe and the United States will be 323GWh and 224GWh, respectively, totaling 547GWh.

4.1.3 European and American battery installed capacity gap judgment: 389GWh under the neutral assumption of 2025

Assuming that the capacity utilization rate of local battery factories in Europe and the United States is 80%, then the installed capacity that can be covered is 437GWh, and there is a clear capacity gap. According to our calculations above:

Under the pessimistic assumption: Europe and the United States in 2025 lithium battery installed demand is 667GWh, then there is a 229GWh installed capacity gap that needs to rely on imports;

Under the neutral assumption: Europe and the United States in 2025 lithium battery installed demand is 827GWh, then there is an installed capacity gap of 389GWh that needs to rely on imports;

Under optimistic assumptions: The installed demand for lithium batteries in Europe and the United States in 2025 is 1004GWh, and the installed capacity gap of 566GWh needs to rely on imports. (Source: Future Think Tank)

4.2 Domestic lithium battery production capacity judgment

4.2.1 Domestic lithium battery demand forecast: 750GWh under the 2025 neutral assumption

4.2.1.1 Power Battery: 645GWh under the 2025 neutral assumption

Passenger car sales increased 10% year-over-year in 2021 and 3% yoy-y annually from 2022 to 2025. The penetration rate of new energy passenger cars increased from 13.8% in 2021 to 40.8% in 2025, of which the penetration rate of EV passenger cars increased from 82% in 2021 to 90% in 2025; the power of EV passenger car bicycles increased from 50kWh in 2021 to 62kWh in 2025; the power consumption of PHEV passenger car bicycles remained unchanged.

Commercial vehicle sales will decline 5% year-on-year in 2021 and 3% year-on-year from 2022 to 2025. The penetration rate of new energy commercial vehicles increased from 3.2% in 2021 to 9.2% in 2025. Among the new energy commercial vehicles, the growth mainly comes from EV special vehicles, EV buses and PHEV buses maintaining a slight growth trend; the bicycle carrying capacity of EV special vehicles has increased from 70kWh in 2021 to 90kWh in 2025.

Conclusion: Under the neutral assumption, China's installed power battery capacity demand in 2025 is 645GWh.

Sensitivity measurement for domestic new energy vehicle penetration rate and bicycle power:

Under the pessimistic assumption: if the penetration rate of new energy vehicles reaches 35.8% in 2025, and the power of EV passenger car bicycles reaches 58kWh, then the corresponding power battery installed capacity is 541GWh.

Under the neutral assumption: If the penetration rate of new energy vehicles reaches 40.8% in 2025 and the power of EV passenger car bicycles reaches 62kWh, then the corresponding power battery installed capacity is 645GWh.

Optimistic assumptions: If the penetration rate of new energy vehicles reaches 45.8% in 2025 and the power of EV passenger car bicycles reaches 66kWh, then the corresponding power battery installed capacity is 759GWh.

4.2.1.2 Energy Storage: 35GWh in 2025

Assumptions: According to CNESA's conservative forecast, the average annual growth rate of domestic energy storage installed capacity from 2021 to 2025 is CAGR57.4%, and the cumulative installed capacity in 2025 will reach 35.52GW. Without disruptive technologies by 2025, lithium/sodium-ion batteries will account for 95% of electrochemical energy storage in 2025.

Conclusion: It is estimated that the new installed capacity of domestic energy storage in 2025 will be 35GWh.

4.2.1.3 Two-wheelers, electric hand tools, etc.: 70GWh in 2025

We estimate that the demand for batteries for two-wheelers in 2025 will be 30GWh, 30GWh for power tools, and 10GWh for others, for a total of 70GWh.

4.2.1.4 Lithium Battery Demand Summary: 750GWh under the 2025 Neutral Assumption

Summarizing the above calculations, the pessimistic, neutral and optimistic assumptions of China's lithium battery demand in 2025 will be 646GWh, 750GWh and 864GWh respectively.

4.2.2 Major lithium battery enterprises in the domestic production capacity planning: more than 3072GWh in 2025

The main lithium battery companies in 2025 in the domestic capacity expansion plan (including joint ventures): Ningde 822GWh, Hive 550 GWh, Zhongxin Airlines 500 GWh, BYD 425 GWh, Yiwei Lithium Energy 250 GWh, Guoxuan 300 GWh, Fu Neng 100 GWh, Sunwoda 100 GWh, LG (Nanjing) 110 GWh, a total of 3072 GWh.

Why are the head companies increasing their capacity expansion?

Horse racing. The penetration of new energy vehicles has accelerated, the supply and demand of power batteries is tight, and various companies are racing to seize more incremental markets, behind which is the ability to quickly put into production.

Based on the domestic, supply global. If domestic enterprises go to Europe and the United States to build factories, there are problems such as high investment costs, high policy risks, and imperfect industrial chain support. Instead of going to sea, it is better to base itself on the domestic market and supply the world. Therefore, enterprises will leave a capacity margin for the export market when making capacity planning.

How to evaluate bottom-up capacity planning?

We believe that the domestic production capacity planning of more than 3072GWh in 2025 is relatively optimistic. According to the above calculations, under the optimistic situation, the total demand for lithium batteries in China, the United States and Europe in 2025 is 1822GWh, which is lower than the plan. In addition, from a policy point of view, the "Lithium-ion Battery Industry Specification Conditions (2021 Version)" has improved the battery parameter indicators for some new capacity expansion, while maintaining the actual output of the previous year when the enterprise declared the actual output of the previous year is not less than 50% of the actual production capacity of the same year. Therefore, the policy may serve as an anchor to regulate the supply and demand relationship of the industry and prevent enterprises from over-investing ahead of time. Therefore, the production capacity that is truly implemented in China in 2025 may have to be discounted on the basis of the plan.

4.2.3 Judging the desirable production capacity of lithium batteries from the perspective of demand

We believe that the domestic lithium battery demand in 2025 superimposed on the installed capacity gap in Europe and the United States will constitute the desirable production capacity of domestic lithium batteries.

Under the pessimistic assumption: in 2025, the domestic installed capacity demand is 646GWh, the installed capacity gap in Europe and the United States is 229GWh, assuming that the capacity utilization rate is 60%, corresponding to the desirable capacity of 1459GWh;

Under the neutral assumption: the domestic installed capacity demand in 2025 is 750GWh, the installed capacity gap in Europe and the United States is 389GWh, the assumed capacity utilization rate is 60%, and the corresponding desirable capacity is 1899GWh;

Optimistic assumptions: in 2025, the domestic installed capacity demand is 864GWh, the installed capacity gap in Europe and the United States is 566GWh, and the assumed capacity utilization rate is 60%, corresponding to the desirable capacity of 2384GWh.

In addition: it must be emphasized that our current calculations have limitations, and the needs of niche markets in Southeast Asia, Australia and South America are not considered for the time being, and the electrification breakthroughs in these segments will drive the overall revision of our calculation results.

Fifth, lithium battery equipment demand expectations

By the end of 2021, the effective production capacity of domestic lithium batteries is about 250GWh, so we estimate that under pessimistic, neutral and optimistic calculations, the domestic lithium battery equipment demand in 2022-2025 will be 2134GWh, 1649GWh and 1209GWh respectively.

In addition, with the enhancement of the competitiveness of domestic lithium battery equipment, we have seen the logic of the equipment going to sea, bringing incremental demand. We have seen that domestic lithium battery equipment has begun to enter the supply chain of Japanese, South Korean, European and American power battery companies, such as Hangke Technology occupies an important share in the back-end equipment of LG and SK, and the pilot intelligence can enter LG, Northvolt, ACC and so on. We believe that in 2023 and beyond, the expansion of production capacity of European and American battery companies will accelerate, and it is expected to purchase domestic equipment on a larger scale, and enterprises with the logic of going to sea can obtain better growth.

(This article is for informational purposes only and does not represent any of our investment advice.) For usage information, see the original report. )

Featured report source: [Future Think Tank].