Source: Securities Market Weekly

Domestic cars go to sea opportunities

The future journey of independent brand new energy vehicles is the "sea of stars" in the global market, which has become the main driving force driving the growth of automobile exports.

Affected by the new crown epidemic, chip shortages, high raw material prices and other unfavorable factors, global automakers are struggling in 2021. Analysts predict that global auto production will be reduced by 7.7 million units in 2021, and the global auto industry revenue will be reduced by more than $60 billion.

However, China's auto market has stepped out of an upward curve driven by the rise of its own brands. According to the China Association of Automobile Manufacturers, in the first 11 months of 2021, China's automobile production and sales reached 23.172 million units and 23.489 million units, respectively, an increase of 3.5% and 4.5% year-on-year. Among them, a total of 8.406 million Chinese brand passenger cars were sold, an increase of 25.1% year-on-year, and the market share reached 44.1%, up 6.4 percentage points over the same period in 2020. It is predicted that new car sales in China's auto market will reach 26.1 million units in 2021, an increase of 3.1% over the sales volume of 25.31 million units in 2020, and the situation of continuous decline for three consecutive years is expected to be reversed.

The export performance of Chinese brand cars in 2021 is outstanding, and the overall trend of volume and price rise is new.

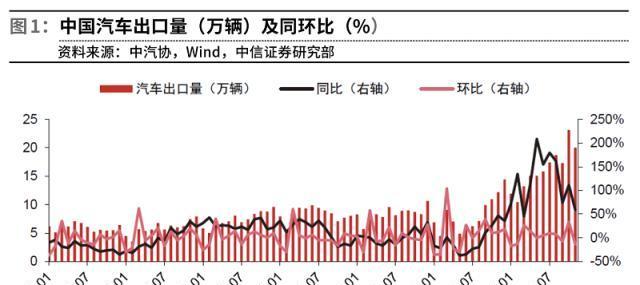

According to the latest data released by the China Association of Automobile Manufacturers, in the first 11 months of 2021, China's cumulative automobile export volume reached 1.793 million units, an increase of 1.1 times year-on-year. Among them, the export volume in November reached 200,000 units, an increase of 59.1% year-on-year. In this context, the export volume of many Chinese auto brands has increased significantly, hitting a new high. For example, from January to November 2021, SAIC Motor exported 245,000 passenger cars, exceeding the total export sales in 2020; Chery Automobile exported 237,900 units, an increase of 137.6% year-on-year; Changan Automobile exported 109,000 units, an increase of 120% year-on-year; Geely Automobile exported nearly 100,000 units, an increase of about 61% year-on-year; and Jiangqi Automobile Group exported 68,000 units, an increase of 112.8% year-on-year.

"Exports are a big growth point for China's auto market in 2021, on the one hand, due to the tight supply of other brand products caused by the overseas epidemic; on the other hand, because China's exports of auto products have improved much higher in grade than before, and the cost performance has also been further improved." Chen Shihua, deputy secretary-general of the China Association of Automobile Manufacturers, predicts that China's overall automobile export market will reach a scale of 2 million vehicles in 2021, and the export volume of automobiles will also maintain a high growth in 2022.

Chen Shihua said that in the past, it was difficult for Chinese brand fuel vehicles to be exported to developed countries, while new energy vehicles were different, and at present, China's new energy vehicles have been exported to Belgium, the United Kingdom, Germany and other countries, becoming the main driving force for the growth of Chinese brand car exports.

According to Soochow Securities, China's auto exports will continue to grow and are expected to exceed 5 million units by 2025.

Exports are growing explosively

From 2018 to 2020, China's annual automobile exports were about 1 million vehicles, but after entering 2021, exports showed explosive growth, and exports in October reached 231,000 vehicles, refreshing the single-month historical record of China's automobile exports, an increase of 33.8% month-on-month, an increase of 1.1 times year-on-year.

As for the reasons for the rapid growth of China's automobile export data in 2021, Soochow Securities believes that the first is that car companies take the initiative to promote overseas market layout, model import and joint local dealers, and accelerate development. Domestic veteran export car companies represented by MG, Chery, etc., as well as new layout car companies such as the Great Wall, have accelerated the introduction of models in overseas markets, and used their cost-effective advantages to seize the market share of Suzuki, Kia, Honda and other regions in South America, Russia, Africa and other regions. Secondly, the overseas epidemic situation is relatively serious, and the domestic benefit from the improvement of the local automobile industry supply chain has less impact and convenient export conditions. In 2021, the epidemic situation in overseas markets, especially represented by India, is more serious, which has a greater impact on the local supply chain and is conducive to the layout of the export industry of domestic car companies.

Huafu Securities said that the reasons for the explosive growth of China's automobile exports in 2021 are: China's better epidemic control, the substitution effect on overseas production; the contribution of new energy vehicle exports, according to the statistics of the China Automobile Association, the growth contribution of new energy vehicle exports is 43.3%; After many years of overseas operations, China's independent brands have greatly improved their product strength and brand.

From the perspective of export car types, passenger cars are the mainstream varieties of exports, accounting for about 3/4 of exports, accounting for a relatively stable proportion in recent years. With the accelerated penetration of new energy vehicles around the world, the export of new energy vehicles has increased significantly, accounting for about 1/4 of the first three quarters of 2021, which has been the main driving force for China's automobile exports. From the perspective of the regional structure of exports, Asia is the largest region for China's exports, but the proportion fell back, from 45% in 2018 to 33% in the first three quarters of 2021; the proportion of the European region increased significantly, from 6% in 2018 to 23%, mainly for Central and Western European countries, showing the improvement of China's car companies' product strength.

From the perspective of export car companies, the export increase contributed by independent brands accounted for 75.80%, which is the main force to promote China's automobile exports from January to September 2021, of which Chery, SAIC and Tesla have the largest increase. Soochow Securities' division of China's auto exports from January to September 2021 shows that Chery Automobile (18.8%), SAIC Passenger Vehicles (15.3%), Tesla (Shanghai) (15.0%), SAIC-GM-Wuling (8.9%), Changan Autonomous (6.9%), Geely Automobile (6.0%), Great Wall Motor (5.9%), SAIC-GM (5.3%) ranked at the top, and the cumulative increase of the eight car companies accounted for more than 80% of the total increase.

From the perspective of exporting countries, Chile, Russia, Australia and other countries have a large increase. Soochow Securities' country-level split of China's own brand exports from January to September 2021 shows that the major exporters are from Chile (18.2%), Russia (15.3%), Australia (11.8%), Egypt (7.3%), India (6.6%), Brazil (6.5%), Indonesia (6.3%), Mexico (5.1%) and the United Kingdom (4.1%).

In fact, Chinese auto brands are achieving breakthroughs in more overseas markets, ranking in many markets is also rising, and word of mouth is increasing.

According to reports, as of now, SAIC Motor Passenger Vehicles has entered the markets of 66 countries and regions, and the product penetration rate has continued to increase. From January to October 2021, SAIC Passenger Car's cumulative sales in Australia and New Zealand exceeded 35,000 units, ranking ninth in the Australian passenger car market, up 8 places from the previous year, and fifth in the South American passenger car market.

In the first 11 months of 2021, Great Wall Motors' cumulative sales in Australia and New Zealand exceeded 20,000 units, an increase of 253% year-on-year, becoming the fastest growing Chinese brand in local sales, and the Australian and New Zealand markets also became the overseas market with the largest export scale of Great Wall Motors.

Geely Automobile ushered in an explosive period in overseas markets in 2021: the first geometric C models to go to sea reached 2486 cumulative orders in the month of listing in Israel; in the Philippines, Geely Automobile's monthly sales set a new record; in Qatar, Geely Automobile's market share ranked among the top ten positions.

At the International Auto Show in Munich, Germany, which focused on the export layout of Chinese auto brands in Europe and the Asian market, Great Wall Motor exhibited popular models such as euler, a small electric vehicle that is very popular in China. Also in September, Hongqi Motor's strategic model, the pure electric intelligent SUV E-HS9, announced its export to Europe, achieving an important breakthrough in the overseas high-end new energy vehicle market. From January to November, Geely Automobile's Lynk & Co brand has delivered a total of 4,380 vehicles to European customers under the subscription model, and the shipment volume of the Lynk & Co brand exports to the European market has reached 10,702; in the second half of 2021, Lynk & Co's "Asia Pacific Plan" was launched, and Lynk & Co 01 also completed the listing in Kuwait.

Specifically, in the Chilean market, under the continuous development and accumulation of Chinese independent brand car companies, the recognition of local brands has gradually increased. From January to September 2021, the sales volume of Chinese own brands in Chile increased by 44,600 units year-on-year in the same period in 2020, and the market share increased by 6.77pct year-on-year. Among them, the independent brands with more market share increase are Chery (3.53pct) and SAIC MG (1.62pct).

Soochow Securities said that Chile is an important strategic market for Chery, and in March 2016, Chery Arrizo 5 completed its initial listing in Chile, kicking off the prelude to the global simultaneous offering. In terms of products, Chery mainly sells Tiggo series and Arrizo series in Chile; in terms of channels, Chery's agents in Chile are SK Berge, which has a deep government background, and under the cooperation of the total generation and terminal network, Chery's market share has continued to rise since 2019. SAIC's MG brand is also widely recognized in Chile, winning the best brand honor in Chile in 2020, and its market share has continued to increase since 2017.

The market share of independent brands in the Russian market has increased, and Soochow Securities believes that the production capacity layout of Great Wall Motors in Russia is getting better and better, and the brand recognition is constantly improving. From January to September 2021, the sales volume of Chinese independent brands in Russia increased by 37,600 units year-on-year, and the market share increased by 2.55pct year-on-year. China's independent brands with more market share increase are Chery (1.56pct) and Great Wall (0.92pct).

Among them, as the first Chinese car company to explore the Russian market, Great Wall Motors has achieved local production. In 2004, it entered the Russian market, and in 2008, it signed Theilito Company, the russian agent of Great Wall Motors, and is currently the largest Chinese automobile brand in Russia. In 2015, Great Wall Motor invested 3.33 billion yuan to set up a wholly-owned subsidiary in Tula Oblast, Russia, with a production base of 150,000 vehicles per year, mainly producing SUVs. In June 2019, the first phase of the Tula Plant with a capacity of 80,000 yuan was officially completed and put into operation, making it the first overseas wholly-owned manufacturing plant of a Chinese automobile brand.

At present, Great Wall Motors' models introduced to the Russian market include the haval F7, H5, H6, H9, H2 and Fengjun 7 with compact SUVs and lower prices. The Haval F7 is also the first car to roll off the production line at the Tula plant. In terms of price, the Haval F7 starts at 1.449 million rubles (about 123,100 yuan), which is similar to the pricing of the Hyundai ix25, but the configuration of space, power and intelligence is stronger than competitors. From January to September 2021, Great Wall Motor's main model sold in Russia was still the Haval F7, totaling 16,700 units, an increase of 124.23% year-on-year; Haval's first love performed well after it began to sell in the Russian market in July, selling 3,395 units in March.

Soochow Securities believes that the main reasons for the increase in the market share of independent brands in the Australian market include: the suspension of production of Australian local brands; the recognition of independent brands such as the Great Wall has continued to increase. From January to September 2021, the sales volume of Chinese independent brands in Australia increased by 28,900 units year-on-year, and the market share increased by 3.11pct year-on-year. The independent brands with more market share increases are SAIC MG (2.05pct) and Great Wall Motors (1.06pct).

From the perspective of export strategy, major car companies have more expectations for more and faster access to overseas markets.

According to reports, SAIC Motor plans to shift from focusing on domestic business to deepening the domestic market and expanding overseas markets during the "14th Five-Year Plan" period. Through the whole industry chain going to sea, we will reconstruct the sales structure of SAIC Motor Group, and strive to exceed 1.5 million overseas sales, accounting for 15% of the group's overall sales, and the average annual compound growth rate is expected to exceed 30%. In 2025, SAIC Motor's European sales will hit the scale of 300,000 vehicles, of which new energy vehicles account for 70% to 80%, and achieve full coverage of entry-level to mid-to-high-end products.

Jiangqi Group is also actively implementing the internationalization strategy, changing the export of a single automobile to the output of the whole industry chain. During the "14th Five-Year Plan" period, Jiangqi Group has regarded the international business as a strategic core business and upgraded it to the same status as the domestic business. To this end, Jiangqi Group has set a strategic goal of reaching 150,000 vehicles in the international market by 2025.

Chery Automobile's overseas strategy is very clear, and during the "14th Five-Year Plan" period, it will fully realize the "double 50", that is, export 500,000 vehicles per year and achieve an export profit of 5 billion yuan, which means that a quarter of Chery Automobile's sales in 2025 will be contributed by overseas markets.

Geely Automobile's external strategy is also ambitious, and its "Longwan Action" includes comprehensively promoting Geely's globalization process and realizing technology going overseas, with plans to reach 600,000 overseas sales by 2025. Geely brand will focus on the layout of Eastern Europe, the Middle East, Southeast Asia, Africa, South America and other "Belt and Road" countries, build more than 600 overseas sales outlets around the world, and enter the European and Asia-Pacific new energy vehicle markets.

As one of the new car-making forces, Xiaopeng Motors' P7 has been officially released in Norway since October 25, and the new smart flagship SUV Xiaopeng G9, which debuted at the 2021 Guangzhou Auto Show, is a model designed and developed for the global market. Xiaopeng Motors will continue to actively deploy in Norway and other European markets, and will continue to improve its sales, delivery and service systems in Sweden, Denmark and the Netherlands in the future. Gu Hongdi, vice chairman and president of Xiaopeng Motors, said that Xiaopeng Motors' long-term goal is to sell 50% abroad.

Fu Bingfeng, executive vice president and secretary general of the China Association of Automobile Manufacturers, said that in 2021, China's automobile sales are expected to exceed 26 million, new energy vehicle sales are expected to reach 3.4 million, and automobile exports are expected to exceed 2 million. The "2022 CICC Auto White Paper" also expects that in 2022, the penetration rate of new energy vehicles in the global mainstream market will exceed the critical point of 10%, new energy vehicles will enter the steep stage of the S-shaped growth curve, the export market is expected to achieve multi-fold growth, and leading independent car companies will open up double growth space.

New energy vehicle assist

The sudden emergence of new energy vehicles has given China's automobile industry more opportunities to win the market, and has become an important area to drive the growth of China's automobile exports. According to data from the China Association of Automobile Manufacturers, from January to November 2021, China exported 291,000 new energy vehicles, an increase of 189.9% year-on-year. Among them, 37,000 new energy vehicles were exported in November, contributing 32.9% to the growth.

According to data from the Association of Automobile Manufacturers, the top car companies in China's new energy vehicle export volume in November were SAIC Passenger Vehicles (6110 units), Great Wall Motors (426 units) and BYD (404 vehicles), and the export volume of new energy vehicles of other car companies continued to rise.

In the era of fuel vehicles, European, American, Japanese and Korean car companies started early and accumulated profound advantages in core technologies such as transmissions and engines, as well as at the brand and channel levels. Independent brands lag behind people, although after years of efforts in appearance, interior, configuration and even work materials and other aspects are not inferior, but in the driving and handling performance and other aspects of the gap makes it difficult to improve the value and reputation of independent brands, long-term snail in the low-end market. According to the statistics of Essence Securities, the ASP of independent traditional passenger cars in 2019-2021 is about 100,000 yuan, which is far lower than the 200,000 yuan of the joint venture brand, indicating the high premium of the joint venture brand.

CITIC Securities said that from fuel vehicles to new energy vehicles, the industry is undergoing several changes: First, electrification lowers the threshold for car manufacturing and attracts new participants. In addition to the existing car companies, there are currently new car-making forces, Internet companies and some traditional real estate enterprises entering the market to build cars.

Second, the supply chain of electric vehicles is more open, and the amount of value has shifted. The powertrain of traditional fuel vehicles is generally self-supplied like an engine, while the gearbox is generally stablely matched by Tier1; the supply chain of the "three electrics" (battery, motor and electronic control) system of electric vehicles is more open, which is a global supporting opportunity for Chinese suppliers.

Third, led by Tesla, the global market of electric vehicle companies has received more attention. In 2017, Tesla ranked among the top ten global car companies in terms of market capitalization for the first time (ranked eighth); in 2020, Tesla surpassed Toyota and ranked first in the global car company in terms of market capitalization; since 2020, bydir, Weilai and other electric vehicle companies have also entered the top ten in the world.

CITIC Securities said that compared with traditional fuel vehicles, electric intelligent vehicles can better meet the needs of future end users for consumption upgrades and personality highlights, and under the wave of electrification, Chinese car companies are expected to achieve "lane change overtaking". After the automobile drive system is converted from the engine + gearbox to the "three electric" system, the hardware barriers are weakened, and the software barriers such as intelligence are improved. Chinese companies will accelerate the iteration of electric smart models in 2017-2021, and have now reached the global leading level in product performance.

Anxin Securities Research Report data show that from 2009 to 2020, the penetration rate of new energy vehicles is less than 6%, China's passenger car market is basically composed of fuel vehicles, and the joint venture brands that dominate traditional cars occupy more than 50% of the market share of China's passenger car market. Among them, in 2018-2019, the macroeconomic downward pressure increased the impact on the low-end demand of the automobile market, superimposed on the purchase tax preferential policy in 2015-2017 to overdraft the independent demand in advance, and the market share of independent brands fell from 43.9% in 2017 to 38.4% in 2020.

From January to October 2021, China's cumulative sales of new energy passenger vehicles were 2.386 million units, a significant increase of 204.8% year-on-year, because independent brands accounted for a high share of 75.8% in the new energy market, so the growth of new energy sales led to an increase in the market share of independent brands from 38.4% in 2020 to 43.9%, of which the share of independent brands in the new energy market increased from 73.8% in 2020 to 75.8% in October 2021, and is expected to remain at about 76% throughout the year.

According to the data of the Association of Passenger Vehicles, the penetration rate of new energy passenger vehicles in November 2021 has reached 20%, which is significantly higher than the penetration rate of 4.2% in 2019. According to the data of compulsory traffic insurance, the penetration rate of new energy in October 2021 has exceeded 30%, reaching 32.5%, and the penetration rate of new energy in non-restricted purchase and restricted cities has increased rapidly to 14.6% and 17.7% respectively, with greater room for improvement. In addition, the proportion of new energy passenger vehicles in cities with non-restricted purchase restrictions increased from 39.4% in 2019 to 49.4% in October 2021, and it is expected that new energy passenger vehicles will continue to penetrate into cities with non-restricted purchase restrictions.

With the launch of various pure electric and hybrid platforms, the decline in the cost of new energy vehicles, the improvement of product strength and continuous marketing promotion, new energy passenger vehicles are expected to usher in a period of rapid growth. Combined with the development of pure electric and hybrid platforms of various car companies and the rhythm of new car launches, Essence Securities expects that the penetration rate of new energy passenger cars is expected to reach 48.3% in 2025, and the sales volume of new energy passenger cars is expected to reach 12.62 million units, with an annual compound growth rate of CAGR of about 41%. The independent brand is expected to maintain its leading edge in the new energy market - in 2025, the market share is expected to reach 78.2%, and the overall automobile market share is also expected to increase to 65%.

Under the wave of global electrification, Chinese car companies have laid out overseas and practiced the "going out" strategy.

Europe is the main market for China's electric vehicle exports, according to the Ministry of Commerce, about 64% of China's exports of new energy vehicles in 2020 will be exported to six European countries (Belgium, Britain, Germany, Norway, the Netherlands, Sweden). As early as 2018 and 2019, SAIC Maxus & MG, Chery Exed and other models were successfully exported to Europe. Since 2020, more and more brands and models in China are accelerating their going global, and traditional car companies such as Great Wall and BYD, and new power car companies such as Xiaopeng and Weilai have achieved sea with their high-quality products.

CITIC Securities said that the threshold for entering the European auto market is WVTA (full name Whole Vehicle Type Approval), which is the EU vehicle form certification, involving a total of 43 vehicle test items such as motor vehicle noise, mileage, crash safety, pedestrian protection, etc., and the indicators are higher than the domestic regulatory requirements. In addition, high-volume access requires an annual plant review and the completion of all testing projects. WVTA is one of the most stringent automotive certification systems in the world, and only certified automotive products can be sold in the EU market, and any EU member state must accept the results of this certification. WVTA's strict certification standards have brought certain barriers to entry for Chinese car companies in the short term, after most of China's new energy vehicle companies chose Norway outside the "European Union" as the first stop at sea, which may not be able to fully meet the consideration of WVTA in the short term.

In December 2017, BAIC Group's mid-to-high-end electric vehicle brand LITE officially obtained the EU vehicle WVTA certification, which is the first two-door two-seat pure electric vehicle in China to obtain a European export pass. Subsequently, Chinese brand electric vehicle models such as Aichi U5, Xiaopeng P7, Weilai ES8, etc., with solid product strength have successively passed the strict WVTA certification, and these models are expected to be mass-produced and sold in all countries in the European Union in the future, opening up a larger market space.

CITIC Securities believes that Europe is only the first step to go to sea, and the future journey of China's own brand new energy vehicles is the "sea of stars" in the global market.

At the moment when the global energy revolution is vigorously advancing, the power structure in the automotive field is also undergoing profound changes, the trend of electrification, intelligence and networking of the automotive industry in the past century is unstoppable, and the baton of Chinese cars going to sea is passing from traditional fuel vehicles to new energy vehicles. For the first time, Chinese car companies and overseas car companies stand on the same starting line of the new "track" of electric vehicles, and Chinese car companies have a first-mover advantage and are expected to usher in the opportunity to overtake in curves. In the medium and long term, China has a huge population base and market, leading overseas electrification of local supply chains, high-speed iteration of intelligent electric vehicle products, Chinese electric vehicle companies are expected to take Europe as the starting point, open the "era of great navigation" of new energy vehicles, open up a larger global market space.

Soochow Securities expects domestic passenger car exports to continue to grow to 1.84 million units in 2022, an increase of 22.4% year-on-year, and is expected to exceed 5 million units in the long run to 2025. In the future, the key areas of domestic passenger car exports include the Southeast Asian market, the South American market, the Eastern European market and the South Asian market, and the main increase comes from the great wall, Geely, Chery, SAIC MG, etc. In the corresponding regions, the introduction of models and the acceleration of production capacity are accelerated.

Huafu Securities said that in the era of intelligent electric vehicles, the advantages of China's independent brands in technology, product strength, brand, supply chain resources and talent levels have gradually emerged, and they have rapidly improved in the domestic market; in overseas markets, in the face of traditional car companies with slower transformation of new energy such as Japan and South Korea, with the accelerated penetration of new energy vehicles, it is expected to further seize market share and become the main source of China's automobile demand. Exports of 1.98 million units are expected in 2021, an increase of 99.1% year-on-year; after 2022, steady growth is resumed, with a CAGR of 8% in 2022-2025.

From cycle to growth

In addition to providing Opportunities for China's own brand car companies to overtake in curves, the new energy vehicle track will also significantly improve their profitability, and the investment in vehicle stocks is expected to shift to a long-term sustained high growth driver.

Anxin Securities said that excluding the impact of license value, pure electric vehicles are more expensive and better sold than the fuel version of the same configuration, indicating that compared with fuel vehicles, consumers' willingness to pay more to electric vehicles is higher, and pure electric platform models have the advantages of leapfrog cost reduction and easier platformization, and the cost is expected to be lower than that of fuel vehicles at the same level, so the profitability of electric vehicles is expected to significantly exceed that of fuel vehicles.

Compared with traditional fuel vehicles, pure electric platform models have the advantages of leapfrogging cost reduction and easier platformization. Compared with traditional fuel vehicles, pure electric platform models do not need to consider the position layout of engines, gearboxes, transmission shafts and other components, the body structure is more flexible, and the space utilization rate is higher, so the body size of pure electric vehicles with wheelbase (space) is shorter, the overall material cost is smaller, and the cost of cross-level is realized.

In addition, compared with traditional fuel vehicles, pure electric vehicles in addition to the traditional fuel vehicle chassis required for horizontal design, engine layout, etc., the battery and motor into the chassis architecture, according to the body size, endurance needs to change the battery capacity size, so as to design different sizes, wheelbase and endurance of the model. Therefore, compared with traditional fuel vehicles, the parts of electric vehicles are more generalized, and the difficulty of platformization is relatively lower.

Thanks to the advantages of cross-level cost reduction and easier platformization, the cost of electric vehicles is expected to be lower than that of the same level of fuel vehicles. Taking the BYD e-platform 3.0 seal as an example, the seal is positioned as a medium-sized car, the size is similar to the compact car Qin PLUS EV, and the cost of the two bicycles is expected to be roughly equal. Essence Securities estimates that the gross profit margin of Qin PLUS EV is about 20%-25%, considering the pure electric vehicle subsidy of 18,000 yuan and dealer rebate of 10%, the bicycle cost of Qin PLUS EV is about 117,000-125,000 yuan. Compared with the Camry of the same class of fuel vehicles, BYD Seals have a similar wheelbase (longer), but the size is smaller than the former, and the cost of the bicycle is expected to be significantly lower than the latter.

Since consumers are more willing to pay more for electric vehicles, and pure electric platform models are lower than fuel vehicles, the profitability of electric vehicles is expected to significantly exceed that of fuel vehicles. Anxin Securities still takes BYD Seal as an example, based on its model positioning, it is expected that the price of seals after subsidies will be 150,000-200,000 yuan, and its bicycle cost is about the same as that of Qin PLUS EV (117,000-125,000 yuan). Considering that the pure electric vehicle subsidy will decline by 30% in 2022, assuming that the dealer rebate is 10%, it is discussed in two situations: assuming that the average selling price of seals after subsidies is 170,000 yuan, it is estimated that the gross profit margin of seals is expected to reach 25%-30%; assuming that the average selling price of seals after subsidies is 190,000 yuan, it is estimated that the gross profit margin of seals is expected to reach 33%-37%. The mainstream joint venture brands such as Beijing Benz, BMW Brilliance, Dongfeng Honda, and Dongfeng Nissan have a net profit margin of 10%-15% over the years, and the gross profit margin is expected to be 20%-30%, so the profitability of pure electric vehicles is expected to significantly exceed that of fuel vehicles.

Anxin Securities said that in the era of fuel vehicles, great wall motors with high profitability in vehicle companies in the past 10 years had an average gross profit margin of 22.6%, an average net profit margin of 9.4%, and a net profit margin of only about 5% in 2017-2020. In addition, the gross profit margin of Great Wall Motor pickup trucks is higher than that of fuel passenger cars, so the actual gross profit margin of the company's passenger cars is slightly lower than the overall gross profit margin. Due to the low overall profitability of vehicle companies over the years, investment in auto stocks is often driven by extremely short product cycles. In the era of electric vehicles, in the next five years, with the accelerated growth of electric vehicle sales of vehicle companies, the gross profit margin level will continue to increase, and it is expected to reach about 25%-37% (in the third quarter of 2021, Tesla's vehicle gross profit margin has increased to 30.5%, and the ideal car has increased to 23.3%), and the net profit margin is expected to reach more than 10%, bringing significant performance flexibility, and the investment in vehicle stocks is expected to turn to a long-term sustained high growth drive.

The rise of autonomous accessories

The wave of electric intelligence provides an opportunity for Chinese enterprises to catch up with foreign car companies, and the development path and final form of electric intelligent vehicles have not yet been finalized, independent brands seize the opportunity to actively enter the game, high-end new energy vehicle brands accelerate the establishment, and high-end new energy vehicles are intensively listed. In 2022, independent brands such as BYD, GAC E-An, SAIC R Automobile, etc., new forces such as Ideal, Xiaopeng, Weilai, WM, etc., will launch high-end new energy vehicles, based on their differentiated advantages in space, endurance, fast charging, intelligence, etc., Anxin Securities expects that in 2022, more than 200,000 yuan of new energy passenger cars are expected to exceed 1.91 million, achieving 60%-70% growth.

Behind the high sales growth, independent brands are redefining the form of automotive products. Essence Securities believes that with the growth of independent high-end new energy vehicle sales, the market share of China's independent brands is expected to surpass joint ventures and foreign investment in 2022, and it is expected to reach 65% in 2025, and independent brands are redefining the form of automobile products. Among them, independent brand new energy vehicles have the following characteristics.

High-speed iteration of products: In the era of traditional fuel vehicles, the update iteration speed of automobiles is slow, and the conventional replacement cycle is about 5 years; in the era of electric intelligence, the technology and products are high-speed iteration, and the update cycle is shortened to about 1-2 years.

Extremely rich configuration: electric intelligent vehicle development time is relatively short, consumers for luxury new energy vehicles have not yet a clear concept, independent car companies seize the opportunity to create high-end brands through stacking configurations, to create differences to improve cost performance to attract users, the main configuration includes intelligent, personalized interior and exterior, air suspension, etc.

Intelligent: Intelligent driving, the current conventional anti-collision warning, ACC adaptive cruise, AEB emergency braking and other functions have become standard in domestic high-end models, independent brands for higher-level intelligent driving enthusiasm more than joint ventures and luxury brands, for example, in 2022, the independent high-end models listed in support L4 automatic driving accounted for nearly half, while joint ventures and luxury brands are few; smart cockpits, tesla, Weilai, Xiaopeng, The new forces of car-making represented by ideals and so on have made smart cockpits popular, and multi-screen, voice interaction, etc. have become the common trend of major car companies to develop intelligent cockpits.

Personalized lights: At present, there are very few models equipped with DLP pixel lights in the world, and the independent brands mainly include Gaohe and SAIC Zhiji L7. Among them, Gaohe HiPhi X is equipped with DLP pixel lights for the first time, surpassing Porsche Taycan in September sales; the second model, HiPhi Z, also uses ISD intelligent interaction design, and the bicycle value is much higher than that of traditional lights.

Air suspension: Air suspension has a high unit price, and has been installed in luxury cars priced at more than 500,000 yuan in the past, with a penetration rate of less than 1%. In recent years, independent high-end brands such as Weilai, Hongqi, Extreme Krypton and Lantu have increased air suspension in order to create high-end and differentiation, and the price of configuration models has dropped to 350,000-400,000 yuan.

Interior: Independent high-end brand interior exquisite workmanship, style has its own advantages, whether it is science fiction or comfort, are in line with the positioning of high-end new energy vehicles, deeply loved by consumers, is expected to lead the trend.

Anxin Securities said that with the strong rise of independent vehicles, Chinese brands have gradually redefined the form of automotive products, and the corresponding domestic auto parts companies are expected to usher in rapid growth.

China's independent parts and components enterprises have institutional advantages and strong enterprising spirit. According to Wind, there are 150 A-share auto parts companies in China, of which private enterprises account for 75.8%, far exceeding the 36.36% of A-share private vehicle companies, which has obvious advantages over the system of vehicle companies.

For independent car companies, there are many advantages in using domestic parts and components enterprises, such as strong bargaining power, ability to ensure supply, fast response speed, etc., so the probability of cooperation between domestic brand vehicle manufacturers and independent parts manufacturers is higher.

Strong bargaining power: independent car companies and foreign parts and components enterprises cooperation is mostly at a low level, usually foreign parts and components enterprises are stronger, if you choose domestic parts and components companies as suppliers, independent car companies can have stronger bargaining power and higher priority.

Guarantee supply: In 2021, the automotive industry is shrouded in a haze of lack of cores, production capacity restricts sales, and the sales growth rate of independent brands is always stronger than that of joint venture brands, mainly independent brands choose domestic parts and components enterprises, product supply is more abundant, supply methods are more flexible, and the industrial chain is resilient.

Fast response speed: the pace of fuel vehicle development is relatively stable, basically an average of 1-2 cars per year, new energy vehicles from the early annual release of 1 car increase year by year, the pace of development accelerated. Independent parts and components enterprises R & D institutions are located in China, the production base is close to the car company, the R & D service response is fast and convenient to support the supply, and the foreign R & D network coverage is wide, to meet the needs of car companies need to go through the R & D process is complex. In short, Chinese parts and components enterprises have a faster response speed and are more able to adapt to the faster development rhythm of new energy vehicles.

In terms of exports, Essence Securities believes that it is easier to export parts than complete vehicles. Overseas markets are vast, but the added value of the whole vehicle is high, there is a possibility of trade protection, the value of parts is low, the difficulty of export is smaller, and it is easier to achieve globalization.

U.S. market: In 2021, the United States has passed the "U.S. Clean Energy Bill" proposal and Biden's $1.75 trillion stimulus bill, while stimulating the U.S. new energy market, it is more focused on supporting U.S. car companies, such as adding an additional $2,500 to the maximum tax credit for electric vehicles produced by union members or car companies with union representatives, relaxing the 200,000-dollar tax reduction limit for automobile manufacturers, which is good for Tesla, General Motors and other car companies that have withdrawn due to sales exceeding 200,000 tax relief.

European market: According to EVsales, Volkswagen, Renault, Mercedes-Benz, Tesla, BMW and Volvo account for half of the European new energy passenger car market from January to October 2021. On the one hand, Europe is the base camp of German and French auto giants, and is currently transforming to electrification, there is a mass base and market share in Europe, coupled with Tesla's hot sales in the European market, independent vehicles out of the sea competition; on the other hand, Europe and the domestic natural geographical environment is different, consumer demand for electric vehicles may not be consistent, there are differences between domestic and foreign markets. Therefore, there may be certain challenges for independent brands to go overseas in Europe.

In summary, under the background of the rise of independent brands and the gradual acquisition of the right to define the form of automotive products, independent parts and components enterprises with mechanism advantages, globalization advantages, cost-effective advantages, supply chain and response speed advantages are expected to benefit significantly.

Anxin Securities said that in the era of fuel vehicles, parts giants are mainly overseas enterprises, China's auto industry started late, and independent parts companies have weak technical accumulation in core components such as engines and gearboxes, and the gap with foreign investment is large. Therefore, in the era of traditional fuel vehicles, mainstream auto parts companies are concentrated in Europe, the United States, Japan and South Korea. According to the top 100 global auto parts suppliers released by Automotive News over the years, the United States, Japan and Germany have always accounted for two-thirds of the list in 2013-2021, and only 1 Chinese auto parts dealer has been shortlisted in 2012-2013, increased to 2 in 2014-2016, increased from 5 to 7 in 2017-2020, and increased to 9 in 2021, but it is still less.

In the era of electric intelligence, the subdivision parts giant is expected to reconstruct the automobile supply chain from China's electric intelligence. On the one hand, the "three electric" system replaces the traditional three major parts, the technical barriers and first-mover advantages of foreign suppliers in the era of fuel vehicles disappear, the new components of electric intelligence release new supply opportunities, and domestic suppliers stand on the same running line with foreign capital; on the other hand, in the era of fuel vehicles, the supply chain is relatively closed, the car giants and the core components suppliers such as engines and transmissions are deeply bound for a long time, electric intelligence gradually opens the closed supply chain, and the supporting convergence of the core "three electricity" systems, such as the most closed Japanese system.

Essence Securities believes that in the subdivision of auto parts, high-quality domestic suppliers are expected to take advantage of the rise. On the one hand, China took the lead in issuing a series of favorable policies such as new energy subsidies to support the development of electric intelligent vehicles, in addition, Tesla entered China, new forces such as car manufacturing forces have been established; on the other hand, electric intelligent vehicles are in the early stage of development, car companies are more inclined to choose R & D services to respond quickly, develop highly flexible, high degree of cooperation suppliers, independent suppliers have more advantages than foreign capital, so electric, intelligent, interior and exterior and other subdivision of the track of high-quality domestic suppliers to take advantage of the rise.

At the same time, global OEMs are facing multiple pressures such as sales, research and development and supply, and Chinese parts suppliers are facing opportunities abroad. From the perspective of the global environment, since 2018, global automobile sales have declined, and OEMs have increased investment in research and development in order to seize the opportunity of electric intelligence, and the demand for cost reduction of OEMs under double pressure is strong; in 2020, the outbreak of the epidemic, the bankruptcy of overseas parts and components enterprises occurs frequently, and the stability of the supply chain has become another important factor for OEMs to choose suppliers, so OEMs are looking for suppliers with high cost performance and stable supply on a global scale, and high-quality Chinese parts suppliers are expected to start an overseas journey.

Essence Securities believes that in the future, the subdivision parts giant is expected to come from China. From the perspective of the external environment, the sales of new energy vehicles in 2025 are expected to reach 12.62 million units, with the growth of independent vehicle sales and the transfer of product definition rights, independent parts and components companies are expected to achieve high growth; global car companies are expected to reduce costs and supply stable demand is stronger, high-quality independent suppliers are expected to accelerate the process of globalization; from their own point of view, independent parts and components enterprises are enterprising, have served the world's largest auto market accumulation advantages (cost, industrial chain, supply capacity) and the quality of not losing foreign investment, China's high-quality subdivided track parts suppliers are expected to enter the global supply chain and grow into a global parts giant.