@ Understand private admiration

Looking ahead, the size of the entire industry in the next few years is likely to move forward at an annualized doubling rate

Press and hold the image above to learn more

Source: Market Cap Watch ID: Shizhiguancha Author / Wen Yu

Two consecutive years of high-light performance makes the new energy vehicle sector expectations have basically been full, when the industry's β revenue is exhausted, the wisest approach is no longer to stud flat, but to find structural opportunities to "hunt".

For example, power exchange, an industry that has just started but directly affects the speed of electric vehicle discharge.

1

the only way

Survey data from third-party institutions show that low cost performance, low endurance, imperfect charging facilities, and long charging time are the main reasons why consumers refuse to buy electric vehicles. Among them, the problem of the energy replenishment link is particularly prominent, and nearly 40% of consumers complain that the charging of electric vehicles is too slow, and the energy supplement experience is far less than that of fuel vehicles.

To solve the problem of energy replenishment, power replacement is the only way.

Power exchange is a kind of new energy vehicle energy replenishment method, which mainly refers to the centralized storage and centralized charging of a large number of batteries through centralized charging stations, and then the battery replacement service for electric vehicles is provided centrally in the battery distribution station.

The reason why it is the only way is because the power exchange mode has advantages that other methods cannot match.

The first is the energy replenishment speed.

Even in the fast charging mode of public charging stations, it takes 30-60 minutes to complete a charge. If you take the way of replacing the battery, it takes only 3 minutes at the shortest, which is equal to the refueling speed of the fuel vehicle, which solves the problem of energy replenishment experience.

Second, changing the battery can protect the battery.

Although fast charging shortens the charging time to a certain extent, the working voltage in the fast charging mode is greater than the battery voltage, which will inevitably lead to the battery heating up too fast, and in the long run, it will bring unnecessary damage to the battery, and the way to replace the battery is completely without this concern.

Third, changing the power can reduce the initial cost of buying a car.

Power batteries are the largest cost item for electric vehicles, accounting for about 40%. In the power exchange mode, the car and electricity are separated, and consumers can use the way of renting batteries, which not only greatly reduces the burden of car purchase, but also solves the mismatch problem of battery depreciation and body depreciation.

Finally, power swapping can alleviate the electricity pressure on the grid.

When electric vehicles are widely popularized, huge electricity consumption will inevitably put pressure on the power grid, and the centralized charging method of the replacement power station can stagger the peak of electricity consumption, the principle is similar to energy storage, and it plays a role in peak regulation.

Set many advantages in one, as early as more than a decade ago, Tesla, Better place and other companies in the overseas implementation of the power exchange model, at the same time, the domestic also synchronously in the first-tier cities pilot power station. But more than a decade has passed, and the power exchange industry has always been moving forward at a crawling speed.

Until today, the entire industry has truly entered the growth period from the introduction period.

2

Everything

There are two factors restricting the popularity of power exchange, one is the industry standard, and the other is the scale of electric vehicle ownership.

Different automakers and battery manufacturers launched different calibers of products, including battery size, interface, etc., and the strange models directly affect the operational efficiency and consumer experience of power exchange.

In 2011, the State Grid tried to organize the establishment of a unified power exchange standard, but at that time, the domestic power battery industry had just started, the technology was immature, the pattern was unstable, and the difficulty of unification itself was very large. Coupled with the fact that at that time, it mainly relied on financial subsidies, and the unified standard meant that the benefits were redistributed, and in the face of the change of dominance, all parties had not reached a consensus, and finally could not be solved.

There is no unity in the superstructure, and there is no economic base.

According to GCL Energy's calculations, the investment amount of a single station in a passenger car replacement power station is about 5 million, and the investment amount of heavy truck replacement power station is even to reach the level of tens of millions. The maximum number of service times per day for a single substation is about 400, and to achieve breakeven, the utilization rate must be increased to 20%.

In other words, in order to realize the commercial operation of the replacement power station, there must be enough electric vehicle scale support, which is simply impossible to do in the early stage of the development of new energy vehicles.

The above two major problems are no longer problems.

First of all, the overall situation of the power battery industry has been preliminarily determined.

The Ningde era is an absolute leader, occupying half of the domestic market and having a unified standard foundation. On the other hand, financial subsidies have been withdrawn, and the previous profit dispute problem has also been eliminated. The standardization of power battery packs will effectively promote the popularization of electric vehicles, which is in the interests of all parties, and a consensus has been formed at the industry level.

Nor is policy wavering.

In 2020, the Government Work Report included the substation into the scope of new infrastructure for the first time, and then frequently issued official documents to establish the status and development direction of the power exchange model. On November 1 this year, GB/T40032-2021 "Electric Vehicle Replacement Safety Requirements" was officially implemented, which is the first basic universal national industry standard in the power exchange industry, which is interpreted by the market as the real inflection point of industrial development.

On the other hand, the unexpected start-up of electric vehicles has also paved the way for the commercial operation of substations.

In 2021, with the overall decline of fuel vehicles, new energy vehicles began to explode rapidly in the Chinese market. The latest data show that from January to November this year, the cumulative sales of domestic new energy vehicles reached 2.99 million units, a year-on-year increase of 166.8%.

In the first 11 months, the penetration rate of domestic new energy passenger cars soared from 5.8% last year to 15%, more than doubling in less than a year. What is more noteworthy is that the current month-on-month data still maintains a high level, and in the single month of November, the penetration rate of domestic new energy passenger cars is as high as 20%.

From the perspective of industrial economics, the penetration trajectory of a new product shows the characteristics of an S-shaped curve, according to the popularity process of Electric Vehicles in Norway, when the penetration rate crosses the 10% threshold, it will increase at a high slope. With this as a yardstick, the domestic electric vehicle market has entered a period of high-speed release.

As the most effective way to replenish energy, the outbreak of power exchange cannot be stopped.

3

Annualized doubled

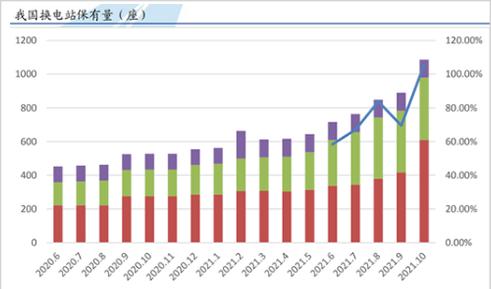

As of October this year, a total of 1,086 substations have been built in China, although the total number is not large, but it is a year-on-year doubling growth rate.

Looking ahead, the entire industry will most likely continue to move forward at an annualized doubling rate in the next few years.

According to data from Orient Securities, by 2025, the number of domestic power replacement models is expected to reach about 5 million; by 2030, this number is expected to be close to 40 million.

On this basis, by 2025, about 22,000 substations will be landed. At that time, the size of the entire equipment market will reach 70 billion, the operating market size is expected to reach 263.1 billion, and the CAGR (compound annual growth rate) from 2021 to 2025 will exceed 100%.

The power exchange equipment will take the lead with the landing of the power station replacement plan, and when the popularity of the power exchange mode increases, the space for the power exchange operation market will gradually open. The order of the development of the two major markets is also the order of investment layout, just as the "hype" logic of 5G is to advance downwards in accordance with the industrial chain.

Let's start with the equipment market.

The most certain opportunity among A-share listed companies is Shandong Weida.

In 2017, Shandong Weida and NIO jointly funded the establishment of Kunshan Swopu, which is the only supplier of NIO's second-generation replacement power station, and has begun to increase its volume, since April this year, Weilai's second-generation replacement power station has come from Kunshan Swopu.

Looking ahead, Weilai plans to build 4,000 substations in 2025, with the current scale, there is still 8 times the room for growth, and the gross profit margin is more than 1 billion. Shandong Weida holds 44% of the shares of Kunshan Swopu, just considering the customer of Weilai, Shandong Weida can get more than 440 million gross profits from Kunshan Swopu, for comparison, the total gross profit of Shandong Weida in 2020 is only 540 million.

Also entering the harvest period is Hanchuan Intelligence, a listed company on the Science and Technology Innovation Board.

As a first-mover power exchange equipment manufacturer, Hanchuan Intelligent announced this year that it has developed a prototype of power exchange equipment and has been recognized by many customers. Technology is the company's biggest attraction and competitiveness, including the identification accuracy of equipment, transmission stability and assembly speed, Hanchuan Intelligent is the industry's leading level.

Compared with the equipment market, the operating market is competing for deer, and the overall situation is undecided.

At present, the head participants are mainly three enterprises: Aodong New Energy, Weilai and Hangzhou Botan. In terms of market share, as of October this year, Aodong accounted for 56% of the total market, Weilai accounted for 34%, and Hangzhou Botan accounted for 10%.

▲The picture is taken from AVIC Securities

Now does not represent the future, a large number of powerful enterprises are stepping up the layout of the power station, and in the end there are roughly two factions that can really achieve things: automakers and "national teams".

In the field of OEMs, Dongfeng, BAIC, Changan, SAIC, Geely and other enterprises have successively announced the increase in power exchange; at the "national team" level, giants such as the State Grid, state power investment, and Sinopec have issued plans to build more than 4,000 charging and replacing power stations during the "14th Five-Year Plan" period.

The landing of a new technology will inevitably be accompanied by the proliferation of capital, but the evolutionary rhythm of the whole process must be carried out strictly according to logic.

Reviewing the development process of smart phones, when the market sales reached 200 million, the stock price of the entire "fruit chain" was basically climbing upwards, but after crossing the 200 million hurdle, the β income disappeared, and the internal differentiation began to be obvious. There is still room for valuable growth in areas where technology continues to improve, while the rest of the tracks are mostly stagnant.

In view of the past, although new energy vehicles have not yet reached the bottleneck point of volume, it is expected to be enough in advance, and the overall room for the plate to rise is getting smaller and smaller. In the future, the focus of funds will focus on the two major links of technology value-added and cleaning up industrial bottlenecks.

The so-called industrial bottleneck means that if the field does not break through, then the entire industry will not be able to continue to develop. As a just-needed support for new energy vehicles, the just-started power exchange market is a bottleneck link.

The properties of the substation are similar to the current gas stations, and the current number of domestic gas stations is about 110,000. In the long run, even after 2025, the replacement market still has a lot of room for growth, and the visibility of the industry is extremely high.

![Doubling the annualization! Another super outlet for new energy[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)