Shentucar original

Author | Zhou Jifeng

Edit | dawn

Tencent, which seems to have nothing to do with car building, recently invested in a Guangdong battery manufacturer. Huawei, which claims not to build cars, has also targeted a Beijing battery manufacturer, Weilan New Energy.

Of course, the new energy main engine factory will certainly not be absent. For example, the ideal car, which has always been known for slamming doors, smashed the 400 million yuan saved from between the teeth into a battery manufacturer - Sunwoda.

Technology companies and new energy OEMs have entered the power battery track at the same time because the industry demand is growing explosively.

According to GGII forecast, global power battery shipments will reach 1550GWh in 2025, if energy storage is included, the total global power battery and energy storage shipments in 2025 will reach 1966GWh, which is equivalent to 6.6 times the installed power battery capacity in 2021.

Huge market space and growth potential have stimulated all battery companies to run. The Ningde era is frantically expanding production, and second-tier battery manufacturers, they try to outperform their opponents and overtake in terms of capital, raw materials, production capacity, and talents.

The "fight" of the power battery track has climbed to a new level.

Start the power battery ranking war

Behind this battery-related race, there are two waves of forces.

A wave is running for simple financial investment, mainly Internet manufacturers and investment institutions.

Zhang Kai, an investor who has long been concerned about the new energy vehicle market, told Shentu: "Batteries are one of the sectors with the highest technical content and the largest value in the entire new energy vehicle industry chain, and there are equally broad markets such as energy storage, so from the perspective of the industry sector, it is a good sector." ”

When a rich Internet manufacturer encounters a profitable and imaginative target, there is no reason not to spark.

"Everyone is hoping to cast the next Ningde era." Zhang Junyi, managing partner of Oliver Laver Consulting, pointed out: "Cataline Era can achieve the same market value as Moutai and give all investment institutions great enthusiasm for investment. ”

Another wave of power is the main engine factory. For them, the battery is the heart, is the lifeblood, and the binding with the battery factory is not to make money, but out of strategic confrontation.

Dominating the electric vehicle market is the Ningde era.

"But when the store is big, it will deceive customers, especially in the battery industry." An industry insider pointed out. Especially in the past two years, the "contradiction" of tight battery supply has become particularly prominent. New energy vehicles ushered in a blowout period, there is a huge gap in the power battery, and the Ningde era can not feed all the car companies.

What really broke through the heart of the car companies was the upstream raw materials that had recently soared wildly. The price of battery-grade lithium carbonate per ton has increased 10 times in one year, and battery raw materials such as nickel, cobalt and copper have also risen significantly. This led directly to a result where battery costs soared. Ideal Auto CEO Li Xiang even complained through social media: "The increase in battery costs in the second quarter was very outrageous. ”

An industry insider pointed out: "According to common sense, battery manufacturers should work with OEMs to deal with such problems and share the cost of raw material price increases." But some head companies refuse to share, which makes the life of the OEMs more difficult. ”

As a result, more and more OEMs have been exposed to start supporting battery suppliers with two and three supplies. "Second-tier battery manufacturers finally have the opportunity to get orders at this time, although the production capacity and battery production level are not as good as the head, but the main engine factory is still willing to patiently support the training." Zhang Junyi pointed out.

For example, SAIC Signed a cooperation investment agreement with Tsingshan Industrial and built a power battery cell and system project with an annual output of 20GWh. This is also the first time that SAIC Motor has established a battery joint venture plant with a third-party company after establishing a joint venture with CATL in 2017.

Sunwoda, which has long focused on the supply of 3C consumer batteries, recently increased its capital by 2.43 billion yuan, while the leading investors have emerged as ideal and Xiaopeng affiliates, and Weilai affiliates are also among the investors.

Weilai and BYD have also raised eyebrows recently. Some time ago, photos of WEILAI CEO Li Bin accompanying BYD Chairman Wang Chuanfu to visit WEI's Hefei factory were circulated on social media.

According to media reports, Weilai and Xiaomi Automobile have signed a fixed-point agreement with BYD's Fudi Battery. For Weilai and Xiaomi, cooperating with BYD means that their competitors provide their most core components.

"If I had the choice, I would certainly not have used a battery made by another car company, which is equivalent to taking my lifeline into the hands of others, but when the enemies are united, it is enough to explain the seriousness of the situation." 」 An industry insider analyzed.

Breakthrough? Not so easy

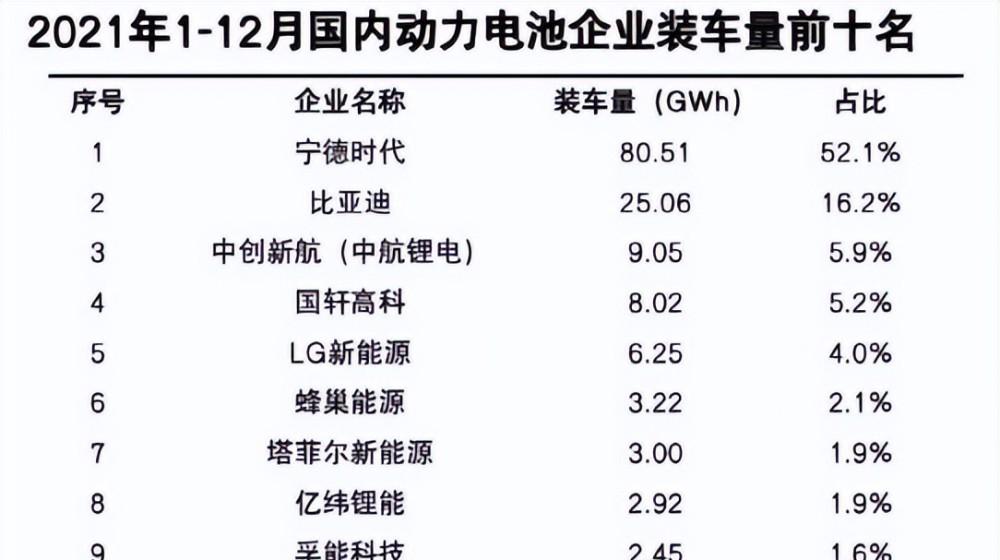

Most of the two and three supplies selected by the main engine factory are the top ten power battery companies in China in terms of installed capacity.

Despite being in the top ten, they have very little market share. For example, although China Innovation Airlines ranks third, its domestic market share is less than 6%. Some companies can only engage in the research and development of power battery systems for some unpopular models, and they cannot get orders from high-end OEMs for many years, such as Sunwoda.

They have a huge difference in strength from the Ningde era. However, the shortage of batteries and the increase in the price of raw materials have given second-tier battery manufacturers a chance to overtake in a corner.

Feng Yanjiao, a partner at CIC Insight Consulting, told Shentu: "When choosing suppliers, car companies first premise is quality and safety, but they will also consider cost performance. For example, Xiaopeng Automobile replaced its suppliers from the Ningde era to AVIC lithium batteries due to price factors. ”

An insider revealed: "The choice of Sunwoda by various OEMs is actually the honesty and trustworthiness of The boss of Sunwoda." ”

Source / China Automotive Power Battery Industry Innovation Alliance

"But it is not enough to have orders and markets from car companies, the most critical premise is to have production capacity." Zhang Junyi thinks. Zhang Kai also agrees with this view, next, the key to the power battery competition is still production capacity.

CATL currently has 15 major production bases, including 10 self-built bases of CATL times and 5 joint venture bases with car companies. These 15 production bases work overtime 24 hours a day to produce batteries, and the effective production capacity of the Ningde era in the first three quarters of 2021 reached 106GWh.

In order to catch up with the Ningde era, battery manufacturers who got orders launched a crazy production capacity war.

For example, China Innovation Airlines increased its production capacity plan at the end of last year, planning to target the production capacity of power batteries to 500GWh in 2025 and 1TWh in 2030. In order to achieve this goal, at the beginning of this year, the battery company signed an investment cooperation agreement with the People's Government of Huadu District of Guangzhou City and the People's Government of Jiangmen Municipality, which respectively planned 50GWh of production capacity.

On the evening of March 17, Sunwoda, which is involved in the investment of Wei Xiaoli and the three companies, issued an announcement that it plans to invest 8 billion yuan to build a 20GWh power battery and energy storage battery production base. Just half a month ago, Sunwoda also announced another expansion plan, through a subsidiary in Zhuhai to invest in the construction of 30GWh power battery production base, planning to invest 12 billion yuan.

There are also enterprises that go abroad to build factories. For example, Envision Power plans to build a battery factory in the United States, the site is located in Kentucky, the United States, planning a production capacity of 30GWh, can meet the needs of 500,000 500-60 degree capacity of electric vehicles.

However, production capacity does not mean that it comes and goes, on the one hand, it must have money. As a result, you can see the recent news that there are constantly power battery companies seeking to go public.

In November last year, AVIC Lithium Battery was renamed Ashinia and completed the joint-stock system transformation. In the first quarter of this year, China Innovation Airlines submitted a prospectus for an IPO of US$1.5 billion (about 9.48 billion yuan), exceeding the 5.462 billion yuan IPO of CATL four years ago. Hive Energy is also driving the IPO process.

Another key to capacity expansion is talent. The alliance between OEMs and battery manufacturers actually requires these second-line battery manufacturers to produce high-performance batteries. However, there is a gap between second-line battery manufacturers and first-line battery manufacturers in terms of manufacturing capacity and consistency level.

The best way to bridge the gap is to recruit great talent. "The researchers who come out of the research institute understand technology, but they have no experience in engineering, and most of the talents with engineering experience come from head battery companies, such as Ningde Times, BYD... Some people only know the trick if they've done it. Zhang Junyi pointed out.

In the battery industry in 2022, it is not an easy task to dig the foot of the wall.

Faced with challenges from all sides, the Ningde era, as the defender, has long launched the "anti-encirclement and suppression". In order to intercept talents, CATL formulated a strict non-compete agreement.

From 2018 to 2019, nine former employees joined two affiliated companies of NINGDE Era rival Honeycomb Energy, Baoding Yixin and Wuxi Tianhong. In the end, the 9 employees were sued by CATL, and each was awarded a non-compete liquidated damages of up to 1 million yuan.

There are also media reports, many employees revealed that the non-compete agreement of the Ningde era is as high as more than 30 pages, including almost all upstream and downstream companies in the battery industry. Once you leave your job, there are only two choices - "either go to the joint venture company of the Ningde era, or change careers".

Is new technology the future?

At present, lithium batteries are the mainstream power batteries.

The point in which it went from laboratory to commercialization was 1991. But this year, 31 years later, lithium-ion battery technology still has not seen a revolutionary breakthrough.

Tesla co-founder Marc Tarpenning once pointed out that lithium battery technology has entered a period of relative stagnation: "When we started Tesla in 2003, the battery was good enough. But it has been 19 years, and we still haven't made a qualitative leap in battery capacity, which is 7%-8% per year. ”

In order to solve the problems of lithium batteries, a variety of emerging battery technologies have emerged on the market. These battery companies, which specialize in emerging battery technologies, have also gained the favor of capital.

For example, Weilan New Energy, which specializes in hybrid solid-state batteries and all-solid-state batteries, stands behind Xiaomi, Huawei, IDG Capital, and Weilai. Huawei's investment company took a stake in sodium-ion battery developer Zhongke Hai sodium, becoming the third largest shareholder of the latter. Zhongke Hai sodium mainly focuses on the development of sodium-ion batteries.

Investors are trying to bet on the future and future of the power battery industry in these emerging battery manufacturers. "After all, the battery industry has a characteristic, and every iteration of battery technology will give birth to great companies." Zhang Junyi analyzed.

But whether it is a solid-state battery or a sodium-ion battery, the technology is in the early stage of research and development, and it is not realistic to expect them to mass-produce and install vehicles in the short term. Zhang Kai believes: "At present, there are many emerging technology routes for batteries, but not every one of them can run out. The gap between the technical route of the battery is still relatively large. ”

He predicted that pure solid-state batteries, especially the sulfide route, actually landed on the mass production cycle is relatively long, and the mass production of sodium batteries will be relatively fast, but sodium batteries are more suitable for lead-acid battery substitution, as a power battery is actually not suitable.

"Around 2025 will be the peak of conventional power batteries, after which the market will be further subdivided, high-energy density solid-state batteries will also begin to gradually stand in the high-end market, in addition, such as low-temperature performance of strong all-climate batteries and fast-charging batteries will have corresponding market segment demand." Zhang Kai thinks.

But before the arrival of revolutionary battery technology, this power battery market battle is not yet a foregone conclusion.

What is visible to the naked eye is that the power battery manufacturers that have been supported have indeed run. For example, in 2018, China Innovation Airlines ranked ninth in the top ten, but in the latest ranking in 2021, China Innovation Airlines has ranked third.

"Everyone may have the opportunity to become a head battery manufacturer." Zhang Junyi concluded: "But if you want to overtake successfully in curves, this requires battery manufacturers to have no short board in all aspects such as technology, capital, customers, supply chain, cost control capabilities and risk resistance capabilities, but the long board must be prominent." ”

Feng Yanjiao gave an example, taking the supply chain as an example, raw materials are the main cost of lithium-ion power batteries, and the current head manufacturers benefit from the scale effect and the profit margin is higher. If you want to overtake in curves, second-tier battery manufacturers need to achieve cost advantages and scale effects by strengthening the layout of core materials.

However, everyone has the opportunity to become a first-line battery company, but is it possible to surpass the Ningde era? Many people in the industry have given a negative answer. "It's a winner-take-all industry, and to completely disrupt it, it will take a technological breakthrough and more than a decade." Zhang Junyi said.

*The caption image is from Visual China, and the picture in the text is from pexels. At the request of the interviewee, Zhang Kai is a pseudonym in the article.