Global inflation, superimposed power battery demand soared, battery raw materials rose, once again back to the downstream of the industrial chain - the price of new energy vehicles represented by electric vehicles has risen, challenging consumer acceptance of electric vehicles, whether this emerging industry from policy-driven to market-driven nodes really come, there is still uncertainty.

The rising price tide and the turmoil in the industrial chain are just a short period of twists and turns on the road to the development of new energy vehicles, but it is also enough to throw out a lot of market participants on this crowded track. Those car companies that have deeply laid out and participated in the whole industry chain of new energy vehicles in key areas such as raw materials, batteries, and chips obviously have to tie their seat belts more firmly.

If the brands in the Chinese auto market have died out before, part of them are new brands that have not yet had time to achieve mass production, and some are niche private brands in the era of fuel vehicles, then there will be more and louder names.

Doubling year-on-year, month-on-month slashing, new energy vehicle companies have successively announced the April 2022 production and sales express report ushered in a boo. China's new energy vehicle market has suffered a double day of ice and fire.

The supply chain problems and production difficulties caused by the epidemic in April are more like a step for the new energy vehicles that have just announced price increases in March, and also a scoop of cold water for China's new energy vehicles that have been soaring since 2021.

In 2021, the production and sales of new energy vehicles in China reached 3.545 million units and 3.521 million units, respectively, an increase of about 1.6 times year-on-year, and the penetration rate of new vehicles reached 13.4%, an increase of 8 percentage points year-on-year. People are pleasantly surprised that the new energy vehicle market, which began in 2009 as a demonstration and promotion, has finally shifted from policy-driven to market-driven; and it is more expected that China's new energy automobile industry can replicate the success of the smartphone manufacturing industry and become an important pole in the global industrial chain.

The trajectory of the first quarter of 2022 reaffirms this trend. According to the data of the China Association of Automobile Manufacturers, in the first quarter of 2022, the production and sales of new energy vehicles in China reached 1.293 million units and 1.257 million units, respectively, and the production and sales of automobiles were 6.484 million units and 6.509 million units, respectively, and the penetration rate of new energy vehicles in new vehicle sales reached 19.3%, climbing to a new historical high.

According to the data from March 2022, the production and sales of new energy vehicles in China were 465,000 units and 484,000 units, respectively, and the production and sales of automobiles were 2.241 million units and 2.234 million units, respectively, and the penetration rate of new energy vehicles in the new vehicle market reached 21.8%. This figure has even exceeded the previous target set by the General Office of the State Council of China in the "New Energy Vehicle Industry Development Plan (2021-2035)" - "by 2025, the sales of new energy vehicles will reach about 20% of the total sales of new cars".

A Chinese car company, BYD, which entered the auto industry through the acquisition of Qinchuan Automobile in 2003, even without any warning, became the first car company in the world to bid farewell to fuel vehicles. They announced on April 3, 2022, that they had stopped producing and selling complete fuel vehicles from March 2022.

However, raw materials, supply chain security, and consumer market environment are the three mountains that will stand in front of new energy vehicle companies in 2022.

The development trajectory of China's new energy vehicle market cannot transcend the overall economic growth level and the global inflation level, and the elimination of car companies will be more cruel and sticky, facing the price increase of raw materials, supply chain security, global inflation, and economic growth, living, or being thrown out.

(Source: China Association of Automobile Manufacturers)

The unbearable weight behind the price increase

On April 10, 2022, WEIO announced that it would start raising prices a month later, and since then all new energy vehicle companies on sale in China have joined the price increase camp.

In the first quarter of 2022, especially since March, major car companies have intensively announced price increases for new energy models, ranging from 3,000 yuan to 30,000 yuan, and the reasons given by each company are without exception the impact of the continuous sharp rise in upstream raw material prices. If traditional car companies can still rely on fuel vehicles for blood transfusion, for new cars that generally fail to achieve positive cash flow, the "hard cost" has risen, making the gross profit margin that is difficult to raise in 2021 precarious.

Taking lithium carbonate as an example, the price in January 2021 was about 30,000 yuan / ton, and rose to 500,000 yuan / ton in March 2022, an increase that exceeded most people's expectations.

The cost of batteries accounts for about 1/2 to 1/3 of the manufacturing cost of pure electric vehicles. Among the on-board battery materials, the highest cost is the cathode material, mainly lithium, nickel and cobalt and other high-priced rare metals, which account for about half of the battery cost.

With the growth of global electric vehicle sales, the number of power batteries loaded has increased, and the demand for battery materials has also increased significantly. According to data from South Korea's SNE Research, the total number of global electric vehicle batteries in the first quarter of 2019-2021 and 2022 was 118.0 GWh, 146.8 GWh, 296.8GWh and 95.1 GWh, respectively, which more than doubled year-on-year in 2021 and the first quarter of 2022.

The sales data of batteries is also basically in step with the sales data of electric vehicles. Statistics from several third-party structures show that global electric vehicle sales will approximately double to 6.5 million units year-on-year in 2021, with the Chinese market accounting for half of them. According to the Electronic Information Department of the Ministry of Industry and Information Technology of China, the output of lithium-ion power batteries in China in 2021 will be 220GWh, an increase of 165% year-on-year.

Therefore, the contradiction between supply and demand of battery materials is the most intense in China's new energy vehicle market, and even breaks the downward trend of prices brought about by the battery industry through technological upgrading and large-scale production.

Ken Brinsden, CEO of Pilbara Minerals, an Australian hard rock lithium miner, had a blunt description at a public event on March 31, 2022, "This happened because automakers were asleep at the wheel, they didn't pay attention to the raw material supply base, they were too far away... They will have to pay a high price to obtain raw materials. ”

Indeed, judging from the existing battery layout of the vehicle companies, they have mostly bound battery companies through joint ventures and equity participation, and more upstream mining companies with non-battery metal materials.

Tesla, which delivered 936,000 electric vehicles worldwide in 2021, should be the first car company to take action in the metal mine. Beginning in July 2021, it has signed a number of nickel concentrate supply agreements with a number of mineral companies such as Proni Resources, a French New Caledonia mining company, Australian mining giant BHP Billiton, Vale of Brazil, and Giga Metals, a Canadian mining company.

In January 2022, it even locked in a nickel project that will not be officially mined until 2026, us miner Talon Metals' Tamarack mine in Minnesota, which purchases no less than 75,000 tons of nickel concentrate.

In addition, Tesla's procurement contract with lithium mining companies includes: Australian lithium mining companies Core Lithium, Kidman and Piedmont Lithium, and signed a three-year purchase contract with China Ganfeng Lithium for battery-grade lithium hydroxide.

In China, Volkswagen was the first to carry out in-depth cooperation with battery raw material companies. On March 21, 2022, Volkswagen Group China signed a memorandum of understanding with Huayou Cobalt and Tsingshan Group to establish two joint ventures covering the upstream and downstream of the battery cathode material supply chain, with a view to achieving the long-term goal of reducing battery costs by 30%-50% and supporting Volkswagen's new energy vehicle growth strategy in the Chinese market.

In the United States, in mid-April 2022, General Motors signed a long-term purchase agreement with commodity company Glencore for the metal cobalt, and Ford motor also reached a preliminary agreement with the Argentine branch of Australian lithium mining company Lake Resources NL to purchase lithium.

Lithium companies are also trying to expand production capacity. Ganfeng Lithium (002460. SZ) announced on April 6, 2022, that it plans to upgrade the ore processing capacity of the Mt Marion spodumene project of the joint venture Reed Industrial Minerals Pty Ltd, from 450,000 tons/year to 600,000 tons/year by April 2022 and to 900,000 tons/year by the end of 2022.

Rising battery material prices will drive metal mining capacity expansion and investment in new projects, but in Ken Brynsden's view, this contradiction between supply and demand cannot be resolved in a short time. Because it takes only two years to build a chemical plant or car plant, but it takes five to seven years for a mine to be up and running.

Supply and demand contradictions, inflation, the battery industry has already made worse, coupled with geopolitics, the Russian-Ukrainian conflict since February 2022, making about 1/10 of the world's Russian nickel mine full of uncertainty, metal nickel prices have risen by about 2 times year-on-year. Under the superposition of three major factors, the price of battery metal materials fluctuated sharply and soared.

Although some car companies and battery manufacturers have turned to battery recycling or tried other battery materials, they mostly stay in the laboratory and small-scale trial production stage, which is far from formal commercialization.

The contradiction between supply and demand needs time to ease. The rise in raw material prices not only breaks the downward trend of battery prices, but also affects the growth rate of electric vehicles.

For car companies, the binding of battery materials also affects their vehicle costs, profits, and future market competitiveness to a certain extent. Because for most consumers, the price of electric vehicles is an important weight that affects their purchase balance.

Perspective on the consumption structure of new energy vehicles

In March, when car companies announced price increases, sales of new energy vehicles were in the dust. In March 2022, the top-selling sedan and SUV brands in the Chinese market were all electric vehicles, namely Wuling Hongguangmin and Model Y.

In the annual sales ranking in 2021, the performance of new energy vehicles is also remarkable: among the top ten brands in terms of car sales, Wuling Hongguang Mini is second, close to 500,000 vehicles, Model3 is fifth, with sales of more than 300,000 vehicles; among the top ten SUV brands in terms of sales, Model Y ranks fifth and sells about 200,000 vehicles.

Does this mean that new energy vehicles have won the hearts of consumers and entered the market-driven stage? Judging from the existing consumption structure of new energy vehicles in China, it may not be enough.

As of the end of March 2022, There were 8.915 million new energy vehicles in China, of which about half were commercial vehicles, online ride-hailing vehicles, and cars going to the countryside (4.21 million units).

According to statistics from China's Ministry of Public Security, as of the end of March 2022, there were 307 million cars in the country, of which 8.915 million were new energy vehicles, accounting for 2.90% of the total number of vehicles.

These nearly 9 million new energy vehicles can be roughly divided into two parts: commercial vehicles (mainly including buses and trucks), and passenger cars (taxis, online ride-hailing cars, private cars).

China's electric vehicle market originated in 2009 by the Ministry of Science and Technology, the Ministry of Finance, the Development and Reform Commission, and the Ministry of Industry and Information Technology jointly promoted the "Ten Cities and Thousand Vehicles" project, that is, 10 pilot cities are developed every year, and each city promotes 1,000 new energy vehicles, and demonstrates operations in the fields of public transportation, taxi, public affairs, municipal administration, and postal services. Commercial vehicles are an important category for the promotion and application of new energy vehicles in China.

According to the China Automobile Association, in the seven years from 2015 to March 2022, the sales volume of new energy commercial vehicles was about 1.15 million; new energy passenger vehicles were also divided into 2B and 2C: the 2B market represented by taxis, online car-hailing and car rental, and the private consumer market (rural and urban).

According to the statistics of the national online ride-hailing regulatory information exchange platform, as of the end of March 2021, a total of 267 online ride-hailing platform companies in China have obtained business licenses for online ride-hailing platforms, and a total of 1.634 million online ride-hailing vehicle transportation certificates have been issued in various places. According to the conditions of the previous transportation certificate for online ride-hailing vehicles in various places, the vast majority of these vehicles are new energy vehicles.

In addition to the Didi platform, many of the 267 online ride-hailing platform companies are led by vehicle companies, and the main operating vehicles are mostly car companies' own brands. Geely Automobile's Cao Cao Travel, GAC Group's Ruqi Travel, FAW Dongfeng Changan's T3 Travel, SAIC Group's Xiangdao Travel, Xiaopeng Automobile's Youpeng Travel, WM Motor's Dayan Travel, etc.

The self-built travel brands of car companies are not only the demonstration operation and performance verification of car companies, but also the purpose of brand promotion, and even shoulder the beautiful vision of car companies transforming from hardware manufacturers to travel service providers. Their most direct effect is to drive the overall sales of China's new energy vehicle market.

After all, the capacity of the 2B market represented by buses, taxis and online ride-hailing is limited, and it is becoming increasingly saturated in the early policy promotion. For example, in Shenzhen, China, the electrification of public transportation was achieved in 2017, the full electrification of cruise taxis in 2018, the full electrification of online ride-hailing and sanitation vehicles in 2020, plus electric mud trucks, commercial vehicles and new energy vehicles in the field of public transportation, while the number of cars in Shenzhen exceeded 3 million in the same period.

The real development of new energy vehicles depends on the private consumer market, and the rural market has to be mentioned here. From the second half of 2020 to the end of 2021, "cars going to the countryside" has brought about 1.428 million units of sales to new energy vehicles.

"In order to promote the promotion and application of new energy vehicles in rural areas, guide the upgrading of rural residents' travel modes, and help the construction of beautiful villages and the strategy of rural revitalization", in the second half of 2020, the three ministries and commissions of the Ministry of Industry and Information Technology, the Ministry of Agriculture and Rural Affairs, and the Ministry of Commerce jointly launched the new energy vehicle to the countryside; in 2021, the joint sponsoring unit added the National Energy Administration, and also added "supporting the realization of carbon peaks and carbon neutrality goals".

According to data from the Ministry of Industry and Information Technology, about 360,000 new energy vehicles will be sold in the second half of 2020. This accounts for 26% of the total sales of 1.367 million new energy vehicles in 2020, and a total of 1.068 million new energy vehicles will be completed in 2021. This accounts for more than 30% of the total sales of new energy vehicles in 2021 of 3.521 million units, and the number and proportion are higher than in 2020.

An important condition for new energy vehicles to go to the countryside is that the price range of the declared models is basically the same as the price consumption range of rural consumers for automobile products. The two car activities in the countryside between 2020 and 2021 are based on the initiative of enterprises to make profits, and local governments will provide financial subsidies to rural consumers. This means that the price of the rural model can not be too high, the profit will not be too high, to a large extent, the profit is exchanged for sales, or in other words, the price for the volume.

Judging from the best-selling cars and SUVs in the Chinese market in March 2022, the price of the Wuling Hongguang mini terminal is more than 30,000 yuan, and the Price of the Model Y terminal is more than 300,000 yuan, which represent the two poles of new energy vehicle consumption.

As mentioned earlier, the manufacturing cost of electric vehicles, about 1/2-1/3 is the cost of the battery, even in the rear vehicle use link, the same level of vehicle, driving the same number of kilometers, the required electricity bill is much cheaper than the fuel cost, but the premise is that consumers have to pay a higher price in the car purchase link.

This was once regarded as an obstacle for new energy vehicles to enter the private consumption market, and it was also an important reason for reducing consumer purchase costs through national and local financial subsidies in the early stage of the promotion and application of new energy vehicles.

The same car purchase budget, in the face of the same price of fuel vehicles and electric vehicles, the cost of late use of electric vehicles is lower, coupled with vehicle purchase tax reductions, license fee reductions in restricted cities, parking, right of way and other policy preferences, which is also an important factor for some consumers to actively choose electric vehicles, for this reason, they can accept the range anxiety of electric vehicles, the shortness of charging facilities.

On the production enterprise side, the Ministry of Industry and Information Technology began to implement the "double integration" policy in 2018 ("Measures for the Parallel Management of Average Fuel Consumption of Passenger Car Enterprises and New Energy Vehicle Credit"), and some car companies also have the incentive to sell relatively cheap micro-electric vehicles.

None of this is the result of a truly complete market competition.

Just like the evolution from feature phones to smart phones, consumers put down their security concerns and embrace the richer functions of smart phones, and are willing to start from thousands of yuan machines to choose high-end products of more than three thousand yuan to pay higher prices for better functions. New energy vehicles really win with comprehensive performance and economy, so that consumers still need to work hard to pay for the sense of technology, trend and comfort that new energy vehicles have painstakingly created.

The toughest war

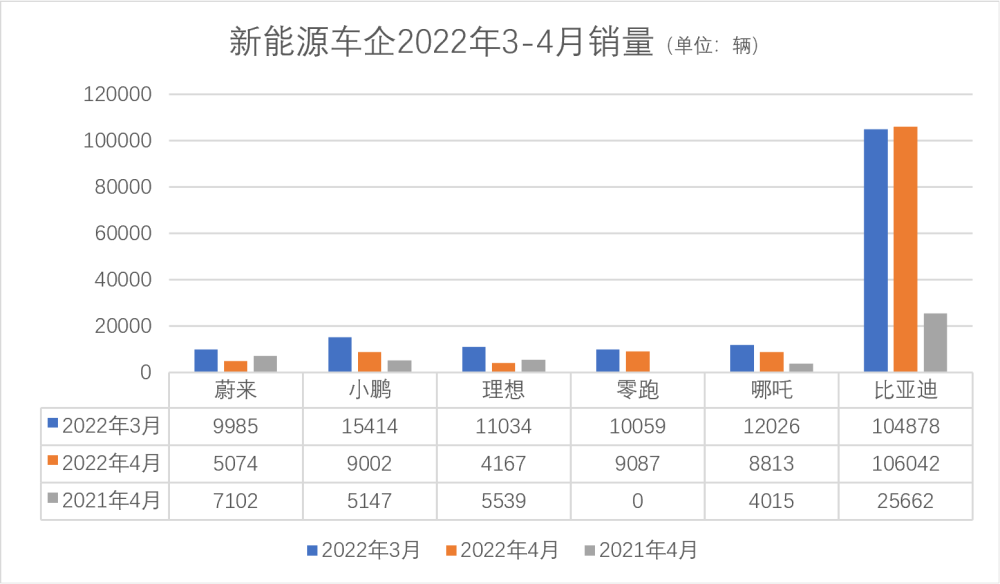

Judging from the April 2022 production and sales express report released by car companies, BYD, which prefers "vertical integration", is the only new energy vehicle company that has slightly increased month-on-month.

Since the end of March, due to the impact of the epidemic, the Yangtze River Delta automobile supply chain has been broken, and the production of many car companies has been restricted, which is the most direct reason for the decline in April sales. At present, the market generally predicts that the full recovery of the automotive supply chain is likely to be until the end of May or even June.

Car companies are suffering because of production difficulties, and the weakness of the sales side should not be underestimated. Behind the high sales of some car companies in March, it is not excluded that some of them have advanced future orders because of price increase forecasts.

On March 22, 2022, Tesla's Berlin factory opened, and someone asked at the scene, when will Tesla go to South America or other markets? Musk's answer is that it will go, but the challenge for Tesla at the moment is that the order volume far exceeds the production.

This is really an answer that makes individuals envious and jealous. Insufficient orders are the daily routine of most new energy vehicle companies at present; overcapacity is the trouble they are facing or will face.

In the case of 600733, the annual report discloses that its sales volume in 2021 is 26,127 units, but the production is only 6,369 units, and the extra 20,000 vehicles are mainly from 2020 and earlier (2021 production is only more than 13,000 units).

Beiqi Blue Valley currently has three plants with a planned design capacity of 520,000 units and a production capacity of 260,000 units in 2021, with an actual capacity utilization rate of 0.08%, 0% and 8.32% respectively.

If the planned production capacity of pure new energy vehicle companies represented by Beiqi Blue Valley is only part of China's new energy vehicle production capacity, then with the traditional car companies that are moving in the direction of new energy, overcapacity is inevitable. Great Wall Motor (601633) admitted in its 2021 annual report that its new energy products are currently produced in line with traditional vehicles, sharing production capacity and implementing flexible production.

Beiqi Blue Valley's production capacity planning is not aggressive, its sales in 2019 were 150,000 vehicles, and since 2013, it has won the sales championship of pure electric vehicles in China for seven consecutive years. Previously, its main sales were supported by online car-hailing, official cars, taxis, etc., after all, the market capacity was limited, and the competitiveness of products was first seen in the private car market.

According to the Ministry of Public Security, China's car ownership in 2019 was 260 million, and private cars exceeded 200 million for the first time to reach 207 million, and the number of private cars has not been updated in the following two years. At the same time, car ownership in big cities is expanding, doubling the number of cities with more than 1 million cars in just seven years from 2015 to 2021.

(Source: Ministry of Public Security.) Note: The number of private cars has not been disclosed after 2020. )

(Source: Ministry of Public Security)

As of March 2022, 79 cities in China had more than 1 million cars. Roughly estimated, they own about 148 million cars, close to half of China's car ownership.

In these congested cities, car purchase restrictions and traffic restrictions have also become the norm. On April 25, 2022, the General Office of the State Council of the People's Republic of China issued the Opinions on Further Releasing Consumption Potential and Promoting the Sustained Recovery of Consumption, which clearly states that it is necessary to steadily increase bulk consumption such as automobiles, and all regions must not add new car purchase restriction measures, gradually increase the number of automobile incremental indicators in areas that have implemented purchase restrictions, relax the qualification restrictions for car buyers, encourage the gradual cancellation of automobile purchase restrictions according to local conditions, and promote the transformation of automobiles and other consumer goods from purchase management to use management.

In order to tap the potential of the market, major car companies have spared no effort, and the sales outlets have sunk again and again. How much incremental can the relaxation of purchase restrictions in cities bring?

In fact, as early as before the epidemic in 2020, in the process of shifting from the incremental market to the stock market, the growth rate of Private Cars in China has begun to slow down. As a bulk durable consumer goods, automobiles have a certain use cycle, and changes in the economic environment will shorten or lengthen the replacement cycle accordingly. Price increases, inflation, and economic situations are all likely to increase people's wait-and-see and wait-and-see cycles. Not only fuel vehicles, but also new energy vehicles.

According to the National Bureau of Statistics, the total retail sales of consumer goods in the first quarter of 2022 108659 billion yuan, an increase of 3.3% year-on-year, and the same period of automobiles -0.3%; in March 2022, the total retail sales of social consumer goods increased by -3.5% year-on-year, while the year-on-year decline in automobiles was as high as 7.5%.

In the traditional peak sales season of the consumer electronics market, there has been a downward trend. According to IDC's data on China's smartphone market in the first quarter of 2022, the total shipment volume was 74.2 million units, down 14.1% year-on-year. In the same period, although the overall sales volume of automobiles increased slightly by 0.20% year-on-year, the decline in sales in April was a foregone conclusion, and new energy vehicles were no exception.

Since 2009, China has become the world's largest single automobile market for 13 consecutive years; since 2015, it has been the world's largest new energy vehicle market for seven consecutive years, and it is naturally an important market that international car companies must compete for. This blue ocean, which once bypassed the competition of foreign brands, is about to usher in a fierce rival this summer.

Before Tesla entered China, China's new energy vehicle market has always been the home of Chinese brand cars, and foreign/joint venture brand new energy vehicles more often only appear on the auto show booth, only hear the sound of stairs, and 2022 will usher in a group of real "downstairs people".

Starting from 2021, under the requirements of various countries on emissions and environmental protection, major car companies around the world have successively announced their timetable for withdrawing from fuel vehicles and fully electrifying. At the end of April 2022, in order to show its determination to develop the electric vehicle business, General Motors of the United States even announced that it would link the long-term compensation of executives to the company's electric vehicle target.

At the end of April 2022, Toyota motor launched the pre-sale of the first pure electric SUV in China. Including GAC Toyota, FAW Toyota, Dongfeng Honda, GAC Honda, Dongfeng Nissan, FAW-Volkswagen, Beijing Hyundai, SAIC-GM Cadillac and other joint venture car companies, at least 8 electric vehicles will be listed in 2022 to participate in the competition of China's new energy vehicle market.

At four o'clock, the weather is urgent, and the wind brings heat in one night. Zotye Automobile, which once hung up China's first electric vehicle license plate, the Ranger, Byton, Singularity that could not be really born... All have disappeared from public view.

The fiercest survival battle in China's new energy vehicle market has just begun.

Southern Weekend researcher Li Yizhi