The weaknesses of Netflix's business model are undeniable, as we've pointed out for years. Fierce competition is taking market share, limiting pricing power and making it clear that Netflix can't generate anything close to the growth and profits implied by the current stock price. We expect shrinking subscribers to become the norm in the future as competition is eating away at a sizeable market share, and Netflix's continued price increases are clearly not well received.

With subscriber loss in Q1'22, and subscriber counts deteriorating further in Q222, the weakness of Netflix's business model is undeniable, as we've been pointing out for years. Although the stock is down 67% from its 52-week high, 56% from our April 2021 report and 39% from our January 2022 report, we think there is more room for the stock to go down.

Fierce competition is taking market share, limiting pricing power and making it clear that Netflix can't generate anything close to the growth and profits implied by the current stock price.

It's no surprise that users lost their lives for the first time in 10 years

Netflix lost 200,000 subscribers in the first quarter of 22 years, well below the previous estimate of 2.5 million subscribers, the company's first loss of subscribers in 10 years. More worryingly, management expects 2 million new users in the second quarter of 2022.

As we noted in our January 2022 report, we expect subscription contraction to likely become the norm in the future as competition is taking a lot of market share, and Netflix's continued price increases are clearly unpopular in such a competitive market.

We expect Netflix's market share to continue to decline as more and more competitors support their products, while deep-pocketed peers like Disney, Amazon, and Apple will continue to invest heavily in streaming.

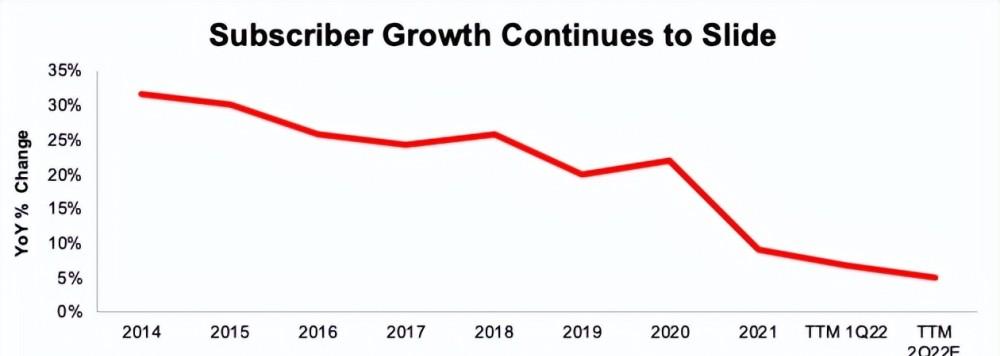

Competitive pressures have been undermining user growth for years

While Netflix plans to continue to increase its content spending "relative to previous years," it's unclear whether this is a winning strategy to boost subscriber growth. As you can see from Figure 1, in the 12 months to the first quarter of 22 years, Netflix's subscriber growth rate fell from 31% in 2014 to 7%.

According to Netflix's guidance, as of the second quarter of 22 years, Netflix's subscribers increased by only 5% year-on-year.

Figure 1: Annual user growth rate since 2014

Source from NFLX Subscriber Growth YoY Since 2014 (New Constructs, LLC)

Revenue growth follows a similar path

At its earnings conference in the first quarter of '22, Netflix acknowledged that "high household penetration, combined with competition, is creating headwinds of revenue growth." In addition, management noted, "Until recently, the huge push from COVID on streaming has obscured this prospect." "However, slower revenue growth is nothing new.

In fact, Netflix's revenue growth has fallen from 26 percent in 2014 to 15 percent as of the first quarter of 2014. Management's guidance meant a further decline in revenue growth, which was only 13% year-over-year as of the second quarter of 2022.

Figure 2: Annual revenue growth rate since 2014

Source from NFLX Revenue Growth YoY Since 2014 (New Constructs, LLC)

Advertising saves the world? Or just a worse user experience

Netflix, and co-founder and co-CEO Reed Hastings in particular, has long opposed an advertising-backed Netflix. However, this stance may change after subscribers miss and weak guidance. On the 22nd quarter earnings call, Hastings noted that the ad-backed program will be rolled out gradually over the next few years, while emphasizing that consumers can still opt for ad-free services.

While ad-backed services may help a business's revenue growth, consumers largely dislike ad-backed streaming platforms. A survey of U.S. adults conducted by Morning Consult in October 2021 found:

44% think there are too many ads on streaming services

64% consider targeted advertising to be intrusive

69% believe that streaming ads are repetitive

79% of people were bothered by this experience

Time will tell if consumers will flock to ad-powered Netflix, but the data shows that this will immediately create a worse experience.

Revenue and user growth are not the only issues

Netflix faces a series of challenges to turn a money-burning business into a money-making business and justify its stock price expectations. Below, we will briefly summarize these challenges. You can find out more details in our January 2022 report.

Netflix's first-mover advantage is gone

The streaming market currently has at least 15 service companies with more than 10 million users, and many of these competitors, such as Disney, Amazon, YouTube, Apple, Paramount, and HBO Max, have at least one of the following two key advantages:

Subsidize profitable businesses for low-cost streaming services

A catalog of content owned by a company, not licensed from someone else

With so many low-cost alternatives, it's hard to raise prices

We previously underestimated Netflix's ability to raise prices, but now that the competition in the market is fierce, our arguments are just as expected. Netflix's forecast for Q22 subscriber losses suggests that with so many low-priced alternatives available, the recent price increase may have reached the upper limit that consumers are willing to pay. As you can see from Figure 3, Netflix now charges more than other mainstream streaming services. For reference, we used Netflix's "Standard" plan as well as the competitor's equivalent package in Figure 3.

Figure 3: Monthly charges for streaming services in the United States

Image source from Netflix Price Vs Competition (New Constructs, LLC)

There can be no growth and cash flow

After achieving a positive FCF in 2020, Netflix returned to the money-burning modalities and generated $2.8 billion in FCF in 2021. Since 2014, Netflix has consumed $16.6 billion in free cash flow. See Figure 4.

Figure 4: Netflix's cumulative free cash flow since 2014

Image source from Netflix Cash Burn Since 2014 (New Constructs, LLC)

Considering that Netflix has only one source of revenue — subscription fees , while competitors like Disney make money from content through theme parks, merchandise, cruise ships, and more, Netflix's cash consumption is likely to continue. Competitors such as Apple and Comcast/NBC Universal receive cash flow from other businesses that can fund content production and reduce the profit margins of streaming services.

Huge red flags: User growth is down despite rising content spending

Netflix's free cash flow was positive in 2020 for the first time since 2010. But the positive FCF came almost entirely from Netflix cutting back on content spending during the COVID-19 pandemic. Netflix is unable to generate positive free cash flow and increase content spending.

In the past, we've found a strong relationship between content spending and subscriber growth. So, it seems worth it to spend the money. As of yesterday's earnings report, we saw that relationship broken.

As Figure 5 shows, Netflix's subscriber growth is still down year-over-year even after a significant increase in content spending in 2021 and surpasses TTM. Given the competitive, content-driven nature of the streaming business, insufficient user growth is a huge red flag. Investing billions of dollars in content isn't enough to fend off competition, and even if you invest heavily in content, new users won't emerge.

Figure 5: User growth and changes in content spending: 2014

图源来自Netflix Subscriber Growth YoY vs Content Spend YoY Change Since 2014 (New Constructs, LLC)

The lack of live content limits user growth

Netflix has historically not ventured into live sports, and that position seems unlikely to change. Co-CEO Reed Hastings said Netflix will require exclusivity that sports leagues don't offer in mid-2021 to "provide a secure deal for our customers." For consumers who need to include live content as part of their streaming needs, Netflix is either not optional or must purchase it as a complementary service to competitors.

Meanwhile, Disney, Amazon, CBS, NBC, and Fox (all of which have their own streaming platforms) are securing access to more and more live content, especially the NFL and NHL, which has given them access to very popular content that Netflix can't match. Recently, Apple began playing "Friday Baseball Night," and it was reported that Apple was about to reach an agreement with the National Football League (NFL), which would only strengthen the live streaming service.

Netflix's current valuation means that the number of subscribers will double

We used the reverse discounted cash flow model and found that expectations for Netflix's future cash flow looked overly optimistic given the above competitive challenges and guidance from a further slowdown in subscriber growth. To justify Netflix's current share price of $220 per share, the company must:

Maintained its 5-year average NOPAT margin of 12%[1] and

Income will grow at a compound rate of 13% per annum through 2027, assuming that in 2022-2023, revenue will grow at a general estimate and 12% per annum thereafter (equivalent to a 2022 revenue estimate)

In this case, Netflix's implied revenue through 2027 is $59.5 billion, 44 times that of Fox Corp's TTM revenue and 2.1 times that of Paramount Global's TTM, which is 2.1 times that of Paramount Global and Warner Bros. Discovery) TTM revenue combined 1.5 times, 82% of Disney's TTM revenue.

To generate this level of revenue and meet the expectations implied by its share price, Netflix needs to:

335 million users, an average of $14.78 per month

424 million users, an average of $11.67 per month

$14.78 was the average monthly earnings per member in the U.S. and Canada in the 22nd quarter. However, Netflix's subscriber growth is mainly coming from international markets, where per capita subscriber revenue is much lower. The overall (U.S. and international) average monthly revenue per user is $11.67 in 2021. At that price, Netflix would need to double its subscriber base to more than 424 million to justify its share price.

In this case, Netflix hinted at $7.1 billion in 2027, 3.6 times more than Fox's 2019 NOPAT, Paramount Global's 2019 NOPAT 1.9 times, Paramount Global inc. and Warner Bros.'s discovery company's 2019 NOPAT combined, and Disney's 2019 NOPAT combined at 1.1 times.

Figure 6 compares Netflix's implied NOPAT in 2027 with the 2019 NOPAT of other content producers.[2]

Figure 6: Netflix's 2019 NOPAT and implied 2027 NOPAT vs. content producers

Source from NFLX DCF Implied NOPAT vs Peers (New Constructs, LLC)

If the profit margin drops to the historical average for streaming, there will be a loss of nearly 50%.

The negative impact would be even greater if Netflix's profit margins fell further due to competitive pressures and spending on content creation and/or user acquisition increased. Specifically, if we assume:

Netflix's NOPAT margin fell to 9% (unchanged from the average since 2014)

By 2027, Netflix's revenue will grow at a compound rate of 10% per year (equivalent to the annual revenue growth rate of the second quarter of 2022, as directed by management).

The stock is currently worth only $121 per share, down 45%. In this case, Netflix's revenue in 2027 would be $51.3 billion, which means that Netflix has 289 million subscribers (at the current average monthly rent in the U.S. and Canada), or 367 million subscribers (at an average of $11.67 per user per month). For reference, Netflix had 222 million subscribers at the end of Q22.

In this case, Netflix's $51.3 billion implied revenue is Fox Corp. TTM revenue is 3.8 times higher than Paramount Global's TTM revenue and paramount Global's TTM revenue is paramount Universal and Warner Bros. Discovery) TTM revenue combined is 1.3 times that of Disney TTM revenue, which is 70% of Disney's TTM revenue.

Netflix hinted that in this case, NOPAT would be 2.3 times more of Fox's 2019 NOPAT, 1.2 times of Paramount Global's 2019 OF's NOPAT, 70% of Paramount Global and Warner Bros. Discovery's 2019 NOPAT, and 43% of Disney's 2019 NOPAT.

Figure 7 compares the company's historical revenue and implied NOPAT in the above cases to illustrate expectations for Netflix's share price. For reference, we also include Paramount Global inc. and Warner Bros. Discovery.

Figure 7: Netflix's history of NOPAT vs. DCF implies NOPAT

Source from NFLX DCF Implied NOPAT (New Constructs, LLC)

Maybe overly optimistic

The scenario above assumes that, according to our DCF model, Netflix's investment capital changes by 14% of revenue each year (H1 2021). For example, since 2014, Netflix's investment capital has grown at a compound interest rate of 40% per year, and changes in investment capital as an average of 26% of revenue.

In the above projections, it is more likely that spending will need to be much higher to achieve growth, but we use this lower assumption to emphasize the risks of valuation of this stock.

This article was originally published on April 20, 2022.

Disclosure: David Trina, Kyle Gusk II and Matt Schuler will not be paid for writing any particular stock, style, or theme.

[1] Suppose that as costs rise from epidemic lows, nopat margins fall to near historical margins. For example, Netflix expects operating margins to fall from 21% in 2021 to 19%-20%.

Considering the impact on the global economy in 2020 and 2021 and other business units of these peers, we used 2019 NOPAT in this analysis to analyze each company's profitability before covid-19.