Under the slowdown of the Fed and the relatively stable performance data of Microsoft, Tesla, Meta and so on, before yesterday, the entire technology market was high morale and thriving, and it seemed to have reopened the "bull market" channel.

But yesterday, the report card handed over by the three giants of Apple, Amazon and Google at the same time pressed the pause button for the first month of 2023.

Overall, the earnings reports of the three giants were unexpectedly all "broken", and the performance of Apple, Amazon, and Google did not satisfy the market: Apple handed over its worst quarterly earnings report in nearly seven years, Amazon recorded its largest annual loss in history, and Google has fallen profits for three consecutive quarters... After the earnings report, all three companies fell as much as 4% after hours.

To a certain extent, the performance of these three giants can also reflect the trend of consumption, retail and commercial markets respectively, further revealing whether the crisis of the general environment is dissolving or continuing to worsen.

So, what information is revealed in these financial reports?

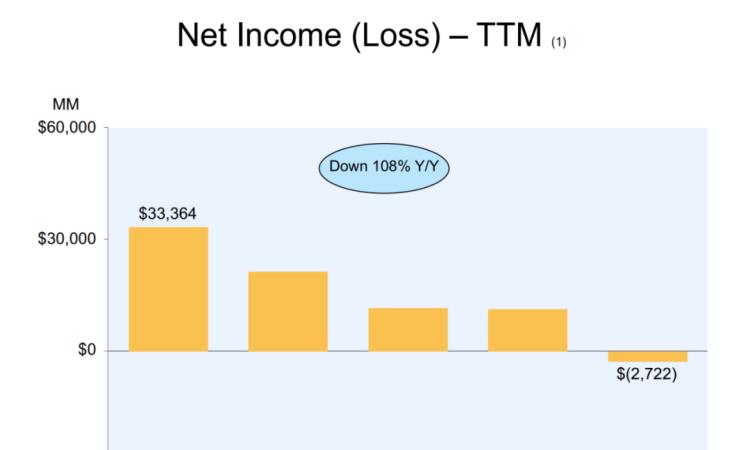

Amazon: Hit the biggest annual loss ever, "cash cow" AWS brakes

If you look at revenue alone, Amazon basically met the target this quarter. According to the financial report, Amazon's revenue in the fourth quarter was $149.2 billion, higher than the market expectation of $145.8 billion, with a year-on-year revenue growth rate of 9%, and a growth rate of 12% after excluding the impact of exchange rates, much higher than the 2% to 8% guidance formulated last quarter; Annual revenue of US$513.98 billion, exceeding the US$500 billion mark for the first time.

Although the total revenue maintained growth, Amazon's problems this time mainly appeared in the sharp decline in profits, the stagnation of sub-businesses and sluggish expectations. Amazon's net profit in the fourth quarter was $278 million, down 98% from $14.323 billion in the same period last year; Earnings per share were $0.03, compared to diluted earnings per share of $1.39 in the year-ago quarter.

Compared with previous years, Amazon's holiday season sales this year are not strong. Net sales from online stores in the fourth quarter were $64,531 million, down 2% from $66,075 million in the year-ago quarter. For the full year, Amazon posted its first full-year loss since 2014, with a net loss of $2.7 billion and the worst record since Amazon's founding in 1997.

However, it should be noted that a large part of Amazon's losses last year were also caused by the loss of investment in Rivian, which recorded a total pre-tax valuation loss of $2.3 billion, compared to $11.8 billion in the fourth quarter of 2021.

Source: Amazon Q4 earnings report

But from the perspective of the main business, Amazon is also facing challenges. The. Both e-commerce and cloud business revenue was lower than market expectations. On the one hand, the e-commerce business has stagnated, especially the slowdown in the growth rate and the continuous expansion of losses in the international region. Operating loss in North America was $200 million, international revenue decreased 8% year-over-year, and operating loss widened to $2.2 billion.

On the other hand, AWS, Amazon's "second growth curve" and the cloud business with the highest profit margin, began to grow into a slow range. AWS revenue for the quarter was just $21.4 billion, up 20% year-over-year, below expectations of $21.76 billion. Obviously, this data is difficult to satisfy the market, you know, AWS growth in the same period last year is as high as 40%.

What's more disturbing is that Amazon's expectations for the first quarter of this year are not optimistic.

At the earnings conference, Amazon said that first-quarter revenue will be between $121 billion and $126 billion, and the median estimate of the $123.5 billion cap is lower than the average estimate of $125.5 billion by analysts. In addition, because Microsoft recently said that the growth of the cloud business will gradually slow down, this also makes the market full of concerns about the growth of AWS.

Once the e-commerce business stops and the profits brought by the cloud business continue to decline, it may bring a lot of trouble to Amazon.

Google: Advertising business is challenged by third consecutive quarter of profit decline

As another big advertiser, Google did not continue the previous Meta earnings report after the momentum of the rainbow, the overall performance has shown obvious signs of weakness.

According to Google's financial report for the fourth quarter of 2022, Google's parent company Alphabet's total revenue in the quarter was $76.05 billion, a year-on-year increase of only 1%; Net profit was US$13.624 billion, down 34% year-on-year; Earnings per share were $1.05, beating expectations of $1.18 and down 31% year-over-year.

Not only are all key indicators lower than market expectations, it is worth noting that this is Google's third consecutive quarter of profit decline, and the downward trend has intensified: net profit fell by 14% in the second quarter of last year, expanded to 26.5% in the third quarter, and then exceeded 34% in this quarter.

From the data of the whole year, Google's performance has also been significantly "downgraded" compared with last year. Total revenue for the full year 2022 was $283 billion, up 10% year-over-year, but up 41% year-over-year in 2021; Operating profit in 2022 was US$74.8 billion, down nearly 5% year-over-year, compared to a 91% year-over-year increase in 2021.

Source: Google's fourth quarter earnings report

From the perspective of sub-business, Google's performance this time is also mediocre, or even lower than expected. Among them, the most important advertising business situation is not optimistic, with total revenue falling 3.6% to $59.04 billion in the fourth quarter, lower than the market's expectation of $60.64 billion.

Revenue from YouTube ads fell nearly 8% to $7.96 billion, well below the estimate of $8.25 billion. Since last year, the YouTube sector has faced a proliferation of rival platforms, including TikTok, Reels and others, making Youtube's outlook foggy.

Outside of the advertising business, Google Cloud's performance was generally unsatisfactory, recording revenue of $7.315 billion, a loss that narrowed sharply by about 50% from the same period last year to $480 million. But the 32 percent growth rate is also the slowest since the company began disclosing revenue figures for the division.

In addition, the "other bet" business, including Waymo, DeepMind, venture capital fund Google Capital, is still not improving, and although revenue has increased to $226 million, the operating loss has widened from $1.45 billion last year to $1.63 billion, and it is still in the process of burning money like crazy.

It is worth noting that at this earnings conference, Google made it clear that "we are embarking on an important journey to redesign the cost structure in a lasting way." "It sends the same signal as Meta to further reduce costs and streamline the structure. In recent months, Google has shut down its internal incubation experiment Area 120 and streaming game platform Stadia, while laying off 12,000 employees at 6% of its total workforce.

In addition, Google is responding to questions about how to deal with the challenges posed by the rise of ChatCPT. Google said that it is stepping up its AI strategy at the company level and will soon launch the latest products on the search function. So we should see ChatGPT competitors emerge soon.

The latest news is that Google has reportedly invested $300 million in artificial intelligence company Anthropic in response to Microsoft's recent continued bet on OpenAI. Founded in 2021, Anthropic also focuses on AI language models, and has an intelligent chatbot called Claude, but it has not yet been launched to the masses. This chatbot battle may be Google's focus next.

Apple: Worst earnings report in 7 years, profit plunged 12%

In terms of consumer retail, it is not only Amazon that has been affected, but also "big brother" Apple.

In the past year, Apple's performance has been relatively stable in the face of a general decline of more than 50% in the technology market, and it has barely delivered earnings reports that reassured the market in previous quarters. But at the end of the year, Apple still failed to withstand the pressure, and quarterly revenue fell for the first time since 2019, recording the largest annual quarterly revenue decline since September 2016; Net profit fell 12%, the first time in nearly seven years that profit fell short of expectations.

Source: From the Internet

Overall, Apple's results this quarter are almost all off the mark:

Operating income: $117.15 billion, market expectation of $121.1 billion, down 5.49% year-over-yearEarnings per share: $1.88, market expectation of $1.94, down 10.9% year-over-year iPhone revenue: $65.78 billion, market expectation of $68.29 billion, down 8.17% year-over-year Mac revenue: $7.74 billion, market expectation of $9.63 billion, down 28.66% year-over-year iPad revenue: $9.4 billion, market expectation $7.76 billion, up 29.66% year-over-yearRevenue from other products: $13.48 billion, down 8.3% year-over-year to $15.23 billion, down $20.77 billion versus $20.67 billion expected

It can be seen that except for iPad and service revenue higher than market expectations, all other key indicators are lower than expected and have fallen sharply. Among them, the sales revenue of the iPhone that attracted the most attention from the market was much lower than the market expectation, which also confirmed that the iPhone 14 series is Apple's worst new product performance in the past.

For this eye-popping earnings report, Cook also gave the following explanation: First, because of the strengthening of the dollar exchange rate, he said that if the exchange rate impact is removed, Apple has actually grown in most markets this quarter. Second, there were problems in the supply chain of the iPhone 14 Pro and iPhone 14 Pro Max last quarter, resulting in a decline in production, emphasizing that the current production capacity of the iPhone has returned to a level that is satisfactory to the company. Third, the overall downturn in the consumer electronics market has put additional pressure on the company.

But Cook also said that the current production capacity of the iPhone has returned to a satisfactory level. At the same time, it was disclosed that including iPhone, Mac, Apple Watch and other products, there are now 2 billion active devices, an increase of more than 200 million over the same period last year, many consumers switched from Android to Apple, and many consumers bought Apple Watch for the first time.

Apple still did not provide specific performance guidance for the next quarter, but CFO Luca Maestri said that the overall trend in the first quarter of this year will be similar to the previous quarter, but the most important iPhone sales will pick up this quarter.

Judging by the recent performance of some chipmakers and other computer suppliers, the current global demand for smartphones and PCs is still slowing. The analysis believes that in the current environment, including Apple, the entire consumer electronics industry may continue to be in a period of slow or no growth.

We are

Yesterday's in-depth article

As mentioned in the book, 2022 is a rare "water reversal" year for "Big Brother" Apple. Throughout last year, Apple encountered the new iPhone 14 and 14plus encountered the Waterloo of product positioning, and downstream manufacturers were forced to cut orders continuously; The two major innovation projects of MR and automotive were postponed, and many senior executives left intensively; The stock price fell by $1 trillion at one point, and Cook and other executives collectively cut their salaries... Apple, the anchor of the technology circle, is now showing signs of instability.

Judging from the current situation of the three giants, it is clear that the entire technology industry has not yet reached the time for a full recovery. It is foreseeable that in 2023, the trend of technology giants reducing costs and increasing efficiency, open source and reducing costs will continue.

Note: The cover image is from Pexels, and the copyright belongs to the original author. If you do not agree to the use, please contact us as soon as possible and we will delete it immediately