During the "13th Five-Year Plan" period, the vehicle purchase tax (referred to as the vehicle purchase tax) accounted for more than 65% of the central financial funds for transportation construction, which is an important source of funds for the central government's financial investment in the transportation industry. Based on the sales trend of new energy vehicles under the carbon peak target and the judgment of the adjustment trend of the future car purchase tax policy, the author analyzes the future changes of mainland car purchase tax revenue in three scenarios, indicating that in the context of the implementation of carbon peak, the car purchase tax revenue will change significantly. Especially in the high scenario, the car purchase tax revenue will decline rapidly, and it is expected that the "15th Five-Year Plan" period will be more than 40% less than the "13th Five-Year Plan"; while in the low scenario, the car purchase tax revenue will continue to decline in the long term, although there is a slight increase in the short term.

In recent years, the car purchase tax policy has been adjusted

Impact on car purchase tax revenue

The "Carbon Peak Action Plan before 2030" (hereinafter referred to as the "Action Plan") issued by the State Council puts forward the target requirement of "by 2030, the proportion of new new energy and clean energy powered transportation vehicles in that year will reach about 40%". In 2020, the proportion of new energy and clean energy vehicles in new car sales will only be about 6%, and this proportion will increase significantly in the future, which means that the consumption structure of mainland automobiles will undergo tremendous changes.

As an important means to guide automobile consumption, the adjustment direction of the automobile purchase tax and the change in the structure of automobile consumption will cause changes in the income of automobile purchase tax, which in turn will affect the financial guarantee of accelerating the construction of a transportation power. Therefore, according to the target requirements of the carbon peak work, it is necessary to make a prejudgment of the changing trend of vehicle purchase tax revenue and study the countermeasures in advance.

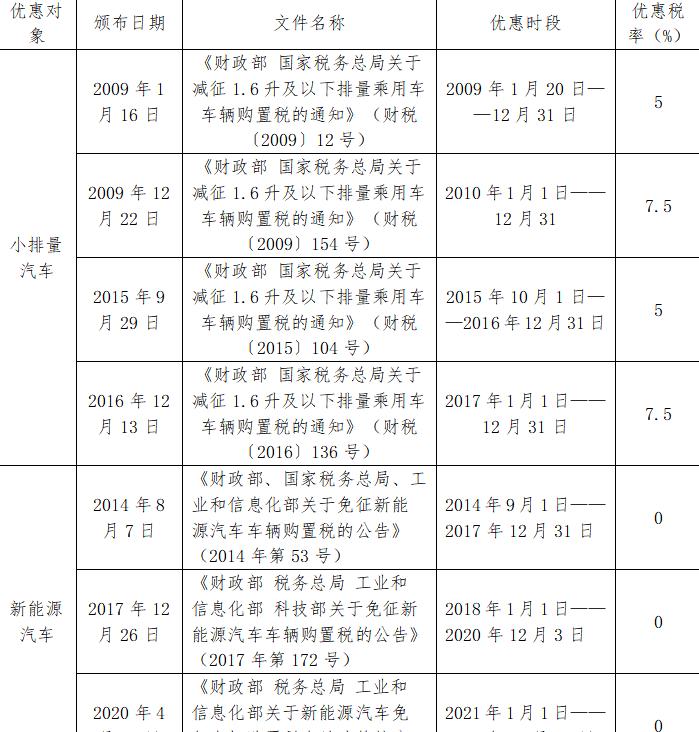

In order to encourage the consumption of small displacement passenger cars (referred to as small displacement passenger cars) and new energy vehicles under 1.6 liters, a temporary reduction policy has been implemented for these two types of cars in order to encourage the consumption of small displacement passenger cars (referred to as small displacement passenger cars) and new energy vehicles under 1.6 liters. Among them, for small-displacement passenger cars, two rounds of tax reduction were implemented from 2009 to 2010 and from 2015 to 2017, each round first reduced the tax rate to 5%, and then the tax rate was raised to 7.5% after the consumption growth of such models reached a certain scale; for new energy vehicles, it has been exempted from car purchase tax since September 1, 2014 to meet certain technical requirements.

For small-displacement cars and new energy vehicles

Vehicle Purchase Tax Relief Policy

The implementation of the car purchase tax reduction policy has greatly promoted the consumption of small-displacement passenger cars and new energy vehicles. Among them, the sales volume of new cars for small-displacement passenger cars increased by more than 50% per year during the first round of preferential periods (2009 to 2010), and the average annual growth rate of the second round of preferential periods (2015-2017) also reached 9%, which was significantly higher than the growth rate of the same period without preferential years. New vehicle sales of new energy vehicles have increased by an average of about 86.4% per year since 2014, an increase of 27.6% over the growth rate from 2011 to 2013. The impact of the car purchase tax reduction policy on the vehicle purchase tax revenue mainly shows the following characteristics:

Changes in new passenger car sales of 1.6 liters or less

New energy vehicle sales

(Source: China Association of Automobile Manufacturers)

The impact of the reduction policy on the income from car purchase tax mainly depends on the proportion of sales of the reduced models

From the perspective of the implementation effect of the policy, the car purchase tax reduction policy can have an impact on the sales volume of new cars and the structure of automobile consumption, and then affect the income of car purchase tax. From 2001 to 2009, since the vast majority of cars were taxed at a rate of 10%, the revenue from the purchase tax was basically consistent with the trend of new car sales. Since the implementation of the preferential policy for small-displacement vehicles in 2009, there has been a certain difference between the change trend of car purchase tax revenue and new car sales.

National new car sales

and vehicle purchase tax income

(Source: National Bureau of Statistics, Ministry of Finance)

During the first round of preferential treatment (2009 to 2010), the growth rate of automobile sales and car purchase tax revenue increased significantly, with an average annual growth rate of 34.6% and 37.9% respectively, and the growth rate of car purchase tax was higher than that of automobile sales. The reason is that this round of concessions not only encourages consumers to buy small-displacement cars, but also stimulates the consumption of the entire automobile market, expanding the base of car purchase tax collection. After the end of the first round of concessions, the growth rate of car sales and car purchase tax has declined.

During the second round of preferential treatment (2015 to 2017), due to factors such as consumption upgrades and emission standards, automobile sales and vehicle purchase tax revenue both fell first and then rose, with an average annual growth rate of 4.4% and 6.0% respectively. The growth rate of automobile sales has not increased significantly relatively without preferential treatment, and the income from car purchase tax has suffered a certain loss. It shows that this round of tax cuts for small-displacement cars has a limited role in stimulating automobile consumption. With the reduction of the proportion of small-displacement car sales, the effect of the tax reduction policy for small-displacement vehicles has gradually declined.

Since 2018, car sales have shown a downward trend, but the revenue from car purchase tax has continued to grow. The reasons for this include the abolition of preferential tax rates for small-displacement vehicles and the increase in sales of automobile products. In general, the price sensitivity of mainland automobile consumption is relatively high, and the impact of the car purchase tax reduction policy of specific models on the purchase tax revenue mainly depends on the sales volume of its models and the proportion of sales.

The proportion of new energy vehicle sales has increased, and the impact of the reduction and exemption policy on the income from car purchase tax has accelerated

As of now, the impact of the new energy vehicle tax exemption policy on the purchase tax revenue is generally small, because the proportion of new energy vehicles in the sales volume of new cars is very small, and the highest is only 5.4% (2020). At the same time, natural gas vehicle sales in 2020 were 140,000 units, accounting for only 0.6% of the total sales of new vehicles that year.

New energy vehicles and natural gas vehicles

The proportion of new car sales changes

In order to achieve the goal of "the proportion of new energy vehicles and clean energy vehicles in the sales of new vehicles will increase to about 40% by 2030", the Action Plan proposes to promote measures such as more widely promoting new energy vehicles, electrified replacement of urban public service vehicles, and the promotion of electricity, hydrogen fuel, and liquefied natural gas power for heavy freight vehicles. In recent years, the impact of the new energy vehicle purchase subsidy policy on the sales of new energy vehicles is very significant, but the impact is mainly short-term. Comprehensive judgment, by 2030, new energy vehicles will become the main force to achieve the 40% target, its proportion will be much higher than that of clean energy vehicles such as liquefied natural gas vehicles, with the rapid increase in sales and proportion of new energy vehicles, the impact of preferential tax policies for this model on vehicle purchase tax revenue will accelerate.

Quarterly sales of new energy vehicles

Schematic diagram of the relationship with subsidy decline

(Source: CICC Research Department)

Three scenario predictions:

Overall, car purchase tax revenue showed a downward trend

The impact of the Carbon Peak action on car purchase tax revenue mainly depends on the trend of automobile sales and the adjustment of related tax policies such as car purchase tax.

From the perspective of automobile sales, considering the future development trend of per capita income, second-hand car trading, motor vehicle scrapping, new crown pneumonia epidemic, sharing economy and other factors, it is expected that from the current to 2030, there is still some room for growth in mainland automobile sales, of which the growth rate of new energy vehicles will be significantly higher than the growth rate of total automobile sales. According to the preliminary calculation of the statistics department, the sales growth rate of new energy vehicles will accelerate in 2021, accounting for more than 13% of new car sales, an increase of 7 percentage points over 2020. At the same time, considering the willingness of relevant ministries and commissions to introduce policies and further increase the promotion of new energy vehicles, it is expected that by 2030, the sales volume of new energy vehicles may exceed the target of 40%.

From the perspective of the direction of the adjustment of the car purchase tax policy, although it is not clear whether the current car purchase tax exemption policy will continue after the expiration of the end of 2022, as the ownership of new energy vehicles reaches a certain level, the car purchase tax exemption policy for the purpose of promoting the consumption of the model will also face gradual adjustment and withdrawal. At the same time, the "Proposal of the Central Committee of the Communist Party of China on Formulating the Fourteenth Five-Year Plan for National Economic and Social Development and the Long-term Goals for the Year 2035" proposes to "promote the transformation of consumer goods such as automobiles from purchase management to use management", which may reduce the tax on the purchase link and increase the tax in the use link in the future.

Based on the sales trend of new energy vehicles under the carbon peak target and the judgment of the adjustment trend of the future car purchase tax policy, the future changes in mainland vehicle purchase tax revenue are analyzed in three scenarios:

Low scenario. The proportion of new energy vehicles in new car sales has increased at a faster rate, reaching 40% in 2030. The current new energy vehicle tax exemption policy will be cancelled after the expiration of the policy, and will be halved, that is, from 2023, a 5% tax rate will be applied to eligible new energy vehicles. Subsidies for new energy vehicles have declined, fuel vehicle scrapping and elimination have remained unchanged.

Medium scenario. The proportion of new energy vehicles in new car sales has increased rapidly, reaching 40% in 2027 and 50% in 2030. The current new energy vehicle purchase tax exemption policy is cancelled after the proportion of new energy vehicle sales reaches 40%, and is changed to halving the levy, that is, from 2028, the 5% tax rate will be applied to eligible new energy vehicles. The subsidies for new energy vehicles have declined, and the scrapping and elimination of fuel vehicles have remained unchanged, and consumers have been guided to choose new energy vehicles through the implementation of policies and measures such as reducing the cost of using new energy vehicles and increasing the cost of using fuel vehicles.

High scenario. The proportion of new energy vehicles in new car sales has accelerated, reaching 60% in 2030. Implement a package of policies to strengthen carbon reduction, including measures such as strengthening the management of vehicle use and accelerating the scrapping of fuel vehicles. Extend the implementation period of the vehicle purchase tax exemption policy for new energy vehicles to the end of 2030. At the same time, the technical requirements for tax exemption for new energy vehicles will be further improved to promote their technological progress, and the resulting increase in the cost of automobile production will be solved by other policy measures such as increasing subsidies, so that the price of new energy vehicles can meet market expectations.

2021-2030 in each scenario

Analysis of national vehicle purchase tax revenues

The results show that under the low scenario, the vehicle purchase tax revenue will decline from 2021 to 2022, rebound in 2023, and continue to decline slowly since then, reaching about 331.5 billion yuan in 2030, which is about 6% lower than in 2020. Under this scenario, the car purchase tax revenue of the "14th Five-Year Plan" and the "15th Five-Year Plan" is about 1,835 billion yuan and 1,758 billion yuan, respectively.

Forecast of revenue from car sales tax for different scenarios

(Unit: 100 million yuan)

In the medium scenario, the vehicle purchase tax revenue shows a trend of "first falling and then increasing and then falling" between 2021 and 2030. Among them, between 2021 and 2025, it will decline at a relatively fast rate, and in 2028, due to the proportion of new energy vehicle sales reaching 40%, the cancellation of new energy vehicle tax exemption policies has seen a sudden increase, and since then it has continued to decline, but the decline rate has slowed down. In 2030, it will be about 289 billion yuan, which is about 18% less than in 2020. Under this scenario, the car purchase tax revenue of the "14th Five-Year Plan" and the "15th Five-Year Plan" is about 1,630 billion yuan and 1,405 billion yuan, respectively.

Under the high scenario, the vehicle purchase tax revenue will continue to decrease, falling to about 134 billion yuan by 2030, about 62% less than in 2020. Under this scenario, the car purchase tax revenue of the "14th Five-Year Plan" and the "15th Five-Year Plan" is about 1,578 billion yuan and 966 billion yuan respectively.

It can be seen that in the context of the implementation of carbon peaking, the revenue of car purchase tax will change significantly. In all three scenarios, car purchase tax revenue is generally on a downward trend between 2021 and 2030. Especially in the high scenario, the revenue of car purchase tax will decline rapidly, and the "15th Five-Year Plan" period will be more than 40% lower than that of the "13th Five-Year Plan". Under the low scenario, although the car purchase tax revenue has a slight increase in the short term, it will continue to decline in the long run, and its short-term growth level depends on the year and magnitude of the increase in the new energy vehicle tax rate.

Strengthen the monitoring of changes in vehicle purchase tax funds

Make a variety of scenario response plans

During the "13th Five-Year Plan" period, the national finance at all levels invested a total of 7.5 trillion yuan in the field of transportation in five years, forming a fixed asset investment of more than 16 trillion yuan. Among them, the car purchase tax fund accounts for more than 65% of the central financial funds for transportation construction, which is an important source of funds for the central government's financial investment in the transportation industry. It is estimated that the investment effect of the national transportation fixed assets driven by the car purchase tax is about 1:6, which plays a vital role in completing the task of transportation planning and construction, stabilizing the effective investment in transportation, and supporting the sustainable development of the transportation industry. Although the vehicle purchase tax reform measures have not yet been introduced, its reform trend is closely related to the ability to guarantee funds for the development of the transportation industry. The transportation department should take the initiative to participate in the decision-making of relevant tax policies such as the car purchase tax, and on the basis of tracking and evaluating the public financial funding needs and guarantee capabilities of transportation, comprehensively promote reform and adjustment strategies to ensure the construction of a stable source of funds for accelerating the construction of a transportation power.

Strengthen the assessment of public financial guarantee capacity of transportation

Judging from the previous revenue and expenditure of car purchase tax, during the "Thirteenth Five-Year Plan" period, after deducting other expenditures approved by the Ministry of Finance, about 86% of the income was transferred to local governments to support the development of local highways and waterways. If this proportion is maintained unchanged, from the above three scenarios, the overall vehicle purchase tax expenditure capacity will show a downward trend from 2021 to 2030, especially under the condition of high scenarios, the expenditure capacity of the "15th Five-Year Plan" period of the car purchase tax will be reduced by about 40% compared with the "13th Five-Year Plan".

Different scenarios get off the car purchase tax

Spending capacity projections for transportation

According to the estimation of the deployment of transportation power and the construction of the national comprehensive three-dimensional transportation network, the scale of investment in transportation fixed assets in the "14th Five-Year Plan" period will still maintain a certain growth rate compared with the "13th Five-Year Plan" period. At the same time, under the current downward pressure of the economy, the "stabilizer" role of transportation fixed asset investment is still important, such as the first three quarters of 2021, transportation fixed asset investment completed 2.56 trillion yuan, an increase of 2% year-on-year, effectively hedging the downward trend of the economy. In addition, due to the intensification of the contradiction between grass-roots fiscal revenue and expenditure in recent years and the increasingly prominent problem of insufficient local financial resources, the central investment represented by the ability to spend on vehicle purchase tax is also more important for the driving role played by the completion of fixed asset investment. Therefore, judging from the forecast, the expenditure capacity of the car purchase tax in the "14th Five-Year Plan" period has shown insufficient growth potential, which will increase the expenditure pressure of the central and local finances.

During the "Fifteenth Five-Year Plan" period, the ability to collect revenue from car purchase tax is closely related to different policy choices, there is a high uncertainty, once the high scenario model appears, it will inevitably bring about fundamental changes in the structure and capacity of central transportation investment, and directly affect the scale and capacity of local supporting and social financing, so it is difficult to ensure the construction of a transportation power and the construction of a national comprehensive three-dimensional transportation network. Therefore, it is necessary to strengthen the monitoring of changes in vehicle purchase tax funds, timely assess its impact on the public financial security capacity of transportation development, and make a response plan for various scenarios.

Coordinate and promote the reform of vehicle purchase tax and related policy formulation

The first is the preferential tax policy for the purchase of new energy vehicles. In 2021, the Announcement on Adjusting the Technical Requirements for New Energy Vehicles Exempted from Vehicle Purchase Tax will reduce the pure electric driving range of plug-in (including range extended) hybrid passenger vehicles from 50 kilometers to 43 kilometers, which means that the technical threshold for obtaining tax exemption status has been reduced to a certain extent. If the car purchase tax reduction and exemption policy for new energy vehicles is adjusted in the future, on the one hand, the role of promoting the technological progress of the new energy automobile industry should be fully considered, on the other hand, the formulation of the policy should also fully consider the needs of the central financial funds for transportation construction, and do a good job in matching the adjustment strength and adjustment rhythm.

The second is the adjustment of the basic tax rate of the car purchase tax. If the focus of automobile consumption management in the mainland is gradually shifted from the purchase link to the use link in the future, when reducing the tax burden of the purchase link, how to adjust the tax rate of the car purchase tax should be fully considered whether the car purchase tax income after the tax rate change can meet the needs of the central financial fund guarantee for transportation construction.

The third is the design of the tax reform plan, including the car purchase tax. In the consumption tax reform, if the car purchase tax and the automobile consumption tax are integrated, it will have a subversive impact on the car purchase tax revenue, and the associated transportation central financial fund guarantee channels should also be adjusted simultaneously. If there is no other alternative source of funds for transportation construction, it is necessary to build a central financial expenditure channel for transportation construction from the consolidated automobile consumption tax revenue.

Author | Huang Liya Cui Min Ma Yanjun Yang Wenyin

Unit | Planning and Research Institute of the Ministry of Transport

Edit | Li ning

Audit | Lian Meng

Producer | Sun Yingli