BYD and Ningde Times are the two giants of new energy vehicles in China. In 2021, BYD's new energy vehicle sales ranked first in the country, the domestic power battery installed capacity ranked second, the establishment of Fordy battery to open the power battery supply business, in the new energy vehicle industry chain layout formed a significant synergy effect; the domestic power battery installed capacity in the Ningde era with a market share of 52% ranked first, through investment, acquisition and other ways to actively layout the upstream and downstream of the industrial chain, in addition to vertical vertical integration of the battery industry chain, NINGDE era also takes the battery as the core, Horizontal layout has also begun in the fields of three electric and complete vehicles.

In this issue of intelligent internal reference, we recommend the report of Tianfeng Securities "Comparative Study of the Two Giants of New Energy Vehicles: BYD vs Ningde Era", which comprehensively compares the two giants of new energy vehicles, BYD and Ningde Era, from the aspects of business, revenue and profit.

Source Tianfeng Securities

Original title:

"Comparative Study of the Two Giants of New Energy Vehicles: BYD vs Ningde Era"

Author: Yute

First, the battery double giant who has been deeply cultivated for many years

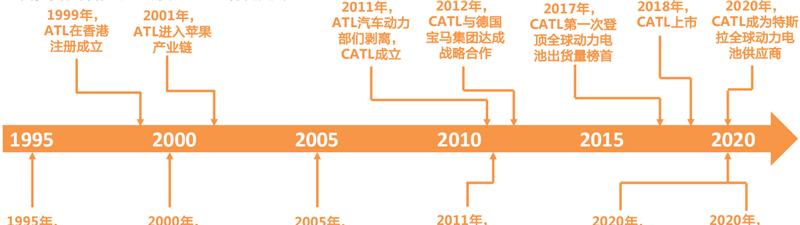

Ningde Times and BYD have been deeply engaged in the field of lithium-ion batteries for many years, and the new energy technology co., Ltd. (ATL) and BYD that have been spun off from NINGDE Times have bright performances in the field of consumer lithium-ion batteries. New Energy Technology Co., Ltd. (ATL) was established in 1999, lithium-ion batteries entered the Apple industry chain in 2001, power battery business divested in 2011 to establish NINGDE Times, and Ningde Times was listed in 2018.

BYD was established in 1995, lithium-ion batteries entered motorola's supply chain in 2000, the first LFP power battery was developed in 2005, BYD was listed in 2011, and Fordy Battery Company was established in 2020 to open the power battery battery supply business.

▲The development process of ningde era and BYD's power battery business

CATL: The senior management team is a young team with high-quality educational background, rich background and management experience related to the new energy industry, and can play a decisive role in corporate strategy formulation and management to help enterprises develop in the future.

BYD: In the management, Chairman Wang Chuanfu, executives Lian Yubo, Liu Huanming, Ren Lin, Yang Dongsheng, etc. are senior engineers, and the management team with rich technical background is fully compatible with the company's competitive advantage, which can lead the company to continuously lead the industry through leading technological innovation and achieve competitive advantage.

▲The management team of the Ningde era

▲BYD's management team

In terms of business, BYD's business content is broader, including automotive, electronics, secondary batteries and other main businesses, and its power battery and other businesses are moving from self-supply to external supply. BYD's business layout covers the fields of electronics, automobiles, new energy and rail transit, and is committed to building a zero-emission new energy overall solution from energy acquisition, storage, and application. From the perspective of 2020 report revenue, BYD's main business is automobiles, mobile phone parts and assembly and secondary battery business.

In 2020, BYD established five Fordi subsidiaries, Including Fordy Battery, Fordi Power, Fordi Vision, Fordi Technology, and Fordi Mould (Fordi Precision), to further accelerate the external supply business of new energy core components and broaden growth space.

▲The proportion of BYD's business revenue in 2020

CATL is the world's leading power battery system provider, focusing on the research and development, production and sales of new energy vehicle power battery systems and energy storage systems, and is committed to providing first-class solutions for global new energy applications. From the perspective of revenue in the 2020 annual report, the main business of catheter era is power battery systems, energy storage systems and battery materials, which are closely related to batteries.

With the rapid development of the new energy automobile industry, CATL has also entered the downstream vehicle field through investment and equity participation, such as investing in Avita, Extreme Krypton, Nezha and other automobile brands.

▲The proportion of business revenue in the Ningde era in 2020

From the perspective of operating income: BYD's overall revenue scale is large, and it has benefited from the rapid development of new energy vehicles in 2020; the overall revenue scale of the Ningde era has maintained a relatively rapid growth trend, which also benefits from the increase in demand for new energy vehicles, and the revenue in 2021Q3 has increased significantly year-on-year.

▲The operating income of Ningde Times and BYD (unit: 100 million yuan) and the year-on-year growth rate

From the overall profitability point of view: the sales gross profit margin of the Ningde era generally maintained a high level, maintaining above 27%; BYD due to the wide range of business, there is a certain degree of fluctuation in the sales profit margin. From the perspective of profitability of sub-businesses: the gross profit margin of each business of the Ningde era is at a relatively high level, the power battery remains above 25%, the battery material remains above 20%, and in the past two years, with the development of the energy storage business, its gross profit margin has also been greatly improved; IND's various businesses, mobile phone components and assembly business due to oem, the gross profit margin is about 10%, the gross profit margin of the automobile business is about 20%, and the gross profit margin of the secondary battery has improved in the past two years, with the expansion of the blade battery supply business, It is expected to contribute to BYD's profitability in the future.

▲Revenue and profitability of various businesses of CATL

▲Revenue and profitability of BYD's various businesses

From the perspective of profit margin: the sales gross profit margin of the Ningde era has generally declined, but it has remained above 27%, and the net profit margin on sales after 2018 can basically remain stable and the profitability is better; BYD has a certain degree of fluctuation in the sales profit margin due to the wide range of business, and with the rapid growth of the new energy vehicle business, the future profitability can be expected.

Power battery business: The gross profit margin of the power battery business of the Ningde era has always been higher than 25%, the gross profit margin of the lithium-ion battery business of Ewell Lithium Energy has reached more than 20% since 2019, and the gross profit margin of BYD's secondary battery business in 2020 has also exceeded 20%. With the expansion of blade battery supply business, BYD will form a second growth curve, according to our forecast will contribute 15 billion and 40 billion yuan in revenue in 2022 and 2023, and if estimated at 20% gross margin, it will contribute 3 billion and 8 billion operating profits.

▲The sales profit margin of NINGDE times and BYD

▲The profit margin of the battery business of NINGDE Times, Ewell Lithium Energy and BYD

From the perspective of net profit attributable to the mother: the profitability of the Ningde era has always been strong and relatively stable; since the new energy vehicle field is still in a period of rapid development, we believe that BYD's vehicle business has not yet fully realized profitability.

▲The net profit attributable to the mother of NINGDE Times and BYD (unit: 100 million yuan) and the year-on-year growth rate

Both CATL and BYD pay more attention to research and development, and continue to invest a lot of R & D funds, which is conducive to continuously building product competitiveness advantages and ensuring the sustainable development of the company. In the past three years, the investment in R&D expenses of the NINGDE era has increased year by year, and it is significantly higher than that of other battery companies. BYD's R&D investment costs are higher than in the Ningde era, but not only for its battery business, but also for its automotive, electronics and other businesses.

▲Investment in research and development of various battery companies

Second, the power battery, who is a brother?

In terms of technology, the Ningde era put forward six major concepts of high specific energy, long life, ultra-fast charging, true safety, self-control temperature control and intelligent management. The performance indicators of the battery have reached the industry-leading level: the battery density reaches 330Wh/kg, the life expectancy is up to 16 years or 2 million kilometers, and the ultra-fast charge can achieve 80% charge in 5 minutes.

In addition, catheter era has started the industrialization layout of sodium-ion batteries, and will form a basic industrial chain in 2023, and lay out next-generation batteries such as cobalt-free batteries, all-solid-state batteries, rare metal batteries, 4680 large cylindrical batteries and emerging technologies in the industry.

▲Six cutting-edge technologies in the Ningde era

In 2021, CATL released the first generation of sodium-ion batteries: the energy density of the cell cell is 160Wh/kg, and through the application of technologies such as anodeless metal batteries, the next generation of products can reach 200Wh/kg; the charge at room temperature for 15 minutes reaches 80%, with fast charging capacity; -20 °C low temperature environment, more than 90% discharge retention rate; system integration efficiency can reach more than 80%; excellent thermal stability, exceeding the safety requirements of the national power battery strong standard. Overall, the energy density of the first generation of sodium-ion batteries is slightly lower than that of the current lithium iron phosphate batteries, but it has obvious advantages in terms of low temperature performance and fast charging, which is especially suitable for high-power application scenarios in alpine regions.

In addition, CATL also proposed the AB battery solution: the sodium-ion battery and the lithium-ion battery integrated mixing and sharing, according to a certain proportion and arrangement of mixing and integration, through the BMS algorithm for the balanced control of different battery systems, not only to make up for the sodium-ion battery at this stage of the energy density shortcomings, but also to play its high power, low temperature performance advantages. Based on this system structure innovation, we will expand more application scenarios for lithium-sodium battery systems.

Although BYD has covered ternary batteries and lithium iron phosphate batteries in its products, since the company launched the first lithium iron phosphate power battery in 2005, it has been adhering to the deep ploughing of the field of lithium iron phosphate batteries, and has continued to promote the progress of the LFP battery industry for many years. In 2020, the company launched blade battery technology and equipped a full range of models, with long endurance, high stability, high safety of the technical advantages.

The blade battery adopts the long cell lithium iron phosphate scheme, the cell is flat designed, and the moduleless technology is used to form a battery pack, which can greatly improve the group efficiency of the battery cell. Compared with traditional lithium iron phosphate batteries, the discharge rate of blade batteries is greatly improved, the charging cycle life exceeds 4500 times, the life span is up to 8 years and 1.2 million kilometers, the cost can be saved by 30%, and the battery volume is 50% higher than the energy density.

The blade battery is safe and can be tested by needle prick. The test showed that after acupuncture, there was no open flame, no smoke, and the surface temperature was only 30-60 ° C. CTP technology of the Ningde era: On the basis of the unchanged cost of the battery cell, the NINGDE era uses CTP technology to achieve system cost reduction and strong battery compatibility; and the CTP solution is combined with the NCM battery, which performs well in energy density and low temperature performance.

BYD's blade battery technology: BYD's lithium iron phosphate blade battery is independently designed and developed, with perfect intellectual property rights, strong technological innovation, excellent performance in safety, durability and economy; but its battery cell length is long, and there are certain challenges and difficulties in design, manufacturing and application.

▲Comparison between CTP scheme and BYD blade battery scheme in the Ningde era

CATL and BYD ranked first and second in the installed capacity of domestic power batteries, and their market share was significantly higher than that of other manufacturers. According to the data of the Power Battery Industry Alliance, the total domestic installed capacity of NINGDE Times and BYD in 2021 will reach 80.51GWh and 25.06GWh respectively.

In 2021, the monthly installed capacity of the Ningde era accounted for the lowest 43.9%, the highest was 56.5%, and the annual market share in 2021 was 52.1%; BYD's monthly installed capacity accounted for the lowest 12.5%, the highest reached 20.4%, and the annual market share in 2021 was 16.2%.

▲ In 2021, the monthly installed capacity of domestic power batteries (unit GWh) and proportion of NINGDE times and BYD

▲The proportion of domestic power battery installed capacity in 2021

At present, the planned production capacity of the self-built production base of CATL has exceeded 650GWh. In addition, CATL has also established joint ventures with FAW, Geely, GAC, SAIC and Dongfeng, and the capacity planning of the joint venture battery is also more than 140GWh.

At present, bydir's announced total production capacity plan has reached 300GWh. According to the previous plan, BYD's total production capacity in 2021 and 2022 can reach 75GWh and 100GWh respectively, while only Wuwei Fudi, Yancheng Fudi, Jinan Fudi, Shaoxing Fudi, Chuzhou Fudi and other companies established in 2021 will add about 90GWh of production capacity to BYD. According to Shaanxi Daily, in December 2021, BYD had a 20GWh hybrid special blade battery project in Xi'an put into production.

▲Capacity planning in the Ningde era

▲BYD's production capacity planning

CATL actively lays out the upstream and downstream of the industrial chain through investment, acquisition, etc., and ensures production capacity and profit margins through the integration of the industrial chain. In addition to in-depth cooperation with upstream suppliers, CATL has a layout in the upstream minerals, cathode materials, electrolytes and equipment, and downstream vehicles.

BYD's current layout in the new energy automobile industry has run through the upstream, middle, downstream and aftermarkets of the industry, initially constituting a closed loop of the industrial chain and forming a synergy effect. As the leader of new energy vehicles, BYD's downstream demand is guaranteed, and the integration ability of the upstream industrial chain needs to be continuously accumulated.

▲The layout of the battery industry chain in the Ningde era

▲BYD's battery industry chain layout

The upstream material supply chain system of CATL and BYD is both quantitative and qualitative. The upstream material supply chain contains multiple suppliers, which can strengthen the voice of suppliers while increasing the quality and stability of their own suppliers.

Cataline Era fully covers the mainstream car companies and customers in the market, and also has both quantity and quality. Customers include mainstream independent brands, mainstream foreign brands, new car manufacturing forces and mainstream commercial vehicle brands, etc., with excellent quality and dispersion, laying a solid foundation for their sustained and rapid development. Ningde era not only has many customer groups, but also accounts for a large proportion of supply among high-quality customers, and in 2020, the supply of Cataline times to Geely, Great Wall, Weilai, Xiaopeng, Ideal and other car companies accounts for more than 60%.

In addition to self-supply, BYD is opening up its external supply business through Fordy batteries. At present, it has begun to supply blade batteries to Ford, FAW and other car companies, and has supported HEV models such as Haval H6 and Weipai latte of the Great Wall. In addition, it has also cooperated with Toyota to jointly develop power batteries and pure electric cars. The gradual release of blade battery production capacity and the gradual expansion of the external supply business will create a second growth curve for the company.

▲2020 CATL TOP10 customer analysis

In the automotive industry, BYD is the leader of new energy vehicles in China. It has built a traditional fuel, hybrid, pure electric vehicle all-engine all-power product system, and the sales of new energy vehicles have ranked first in China for 8 consecutive years, and it is the first Chinese brand to enter the "Millions Club".

In terms of technical routes, BYD pure electric and hybrid two-wheel drive, Pure electric launch of e3.0 platform, hybrid launch of DM-i and DM-p two sets of systems, leading technology, strong product force; in terms of brand network, BYD ocean network and Dynasty network go hand in hand, the model cycle is upward, the market share is steadily improving; in terms of market positioning, BYD deep ploughing the mass market below 200,000 yuan, through the hot-selling model Han to achieve the expansion of more than 200,000 high-end market, and will launch more than 500,000 high-end brands, further open the price ceiling.

BYD has a comprehensive industrial chain layout in the new energy automobile industry, ranging from battery raw materials to three-electric system to vehicle design and manufacturing to battery recycling and automobile services, forming a complete industrial chain closed loop and forming a significant synergy effect.

BYD's abundant new energy models and strong terminal demand have driven the market share of key components in the midstream. Taking November 2021 as an example, the company's new energy vehicle market share ranked first in China, the market share of Midstream Fudi Battery in the power battery cell (Cell) ranked second in China, and the market share of other core components of the three electric core components such as battery packs, electric drive systems, motors, and electronic controls ranked first in China.

The company's layout in the middle and upstream of the industrial chain can provide supply chain support for the rapid growth of the company's sales volume, and can reduce costs and improve the competitiveness and profitability of terminal products.

In addition to the vertical vertical integration of the battery industry chain, the Ningde era takes the battery as the core and has also begun a horizontal layout in the fields of three electric and complete vehicles. In 2017, it invested in the establishment of CATL Motors; in 2021, CATL plans to set up a joint venture company in the field of electric drive control systems, and the general manager of the joint venture company, Jiang Yong, is the former vice president of Huichuan Technology; when announcing the CTC technology route, Zeng Yuqun, chairman of CATL Times, introduced that CTC technology will not only rearrange the battery, but also include power components including motors, electronic controls, DC/DC, OBC and so on In the future, CTC technology will further optimize power distribution and reduce energy consumption through intelligent power domain controllers; in terms of vehicles, CATL will cooperate with Changan and Huawei to build Avita Automobile, invest in Geely's Extreme Kr Automobile, and invest in Hezhong New Energy.

The energy storage business of the Ningde era has performed well, forming a second growth curve for the company. CATL provides energy storage solutions in a variety of scenarios such as power generation side energy storage, grid side energy storage and electricity side energy storage. From the perspective of financial data, from 2020, the revenue of the energy storage system business and the proportion of the business in the company's revenue have risen rapidly, and the gross profit margin is higher than 35%, and the rapid growth of the energy storage system business will form a second growth curve for the company.

BYD's energy storage business has spread to more than 100 cities in 23 countries around the world, with cumulative global sales of more than 700MWh. BYD has taken the lead in developing a business model of "optical storage integration" in the field of new energy, aiming to break through the bottleneck of traditional photovoltaic power generation and make it meet more diversified market demand. Relying on advanced iron battery technology, it meets the needs of energy storage, peak shaving and valley filling, peak shaving and frequency regulation, and promotes renewable energy power generation supporting and power auxiliary services。

Che Dongxi believes that power lithium batteries are an important branch of China's new energy industry chain and an important part of new energy vehicles. At present, the two giants of China's power lithium batteries are Ningde Times and BYD. BYD has grown into the world's second largest rechargeable battery manufacturer in 2003, and successfully produced lithium iron phosphate power batteries in 2005; Ningde times, as a rising star, has achieved the world's first installed power lithium battery capacity in seven years, and the installed power battery capacity has exceeded 50% of the national market share. Although CATL is leading in market share, the momentum of BYD's battery business looks more fierce.