Written by | Wu Xue

Edit | Yang Guang

Produced | Automotive Sankei

The speed of media coverage seems to have not kept up with the capacity expansion rate of battery companies.

When we are still exploring whether the global power battery capacity will be overcapacity in 2025, battery companies have opened a new round of capacity expansion.

On December 8, the second battery day of Hive Energy, the company, which has been established for less than four years, raised its target for the Nth time - to challenge 600GWh production capacity and 450GWh shipments in 2025.

At the first battery day in 2020, its goal is to reach 40GWh in 2025.

While Hive Energy will increase its target by 10 times in one year, on the other hand, on December 8, CATL signed a cooperation and investment agreement with the Suzhou Municipal Government; on December 7, LG New Energy, which ranked second in the world, also announced that it intends to raise tens of billions of dollars to go public...

Driven by new energy vehicles, power batteries have become one of the most lively tracks this year. And like all potential, competitive tracks, involution is inevitably happening in this industry.

Capacity planning, another round of "big dry fast"

There are two "famous" rumors in the battery industry: one is that He Xiaopeng, CEO of Xiaopeng Automobile, squatted in the Ningde era for a week in order to get the battery; the other is that at least seven or more OEMs "bosses" squatted in the Ningde era every day.

Although in the end He Xiaopeng and NINGDE times both denied the rumors, the lack of battery supply can be seen.

So this year's power battery industry has a very obvious trend - expanding production capacity has become one of the main themes.

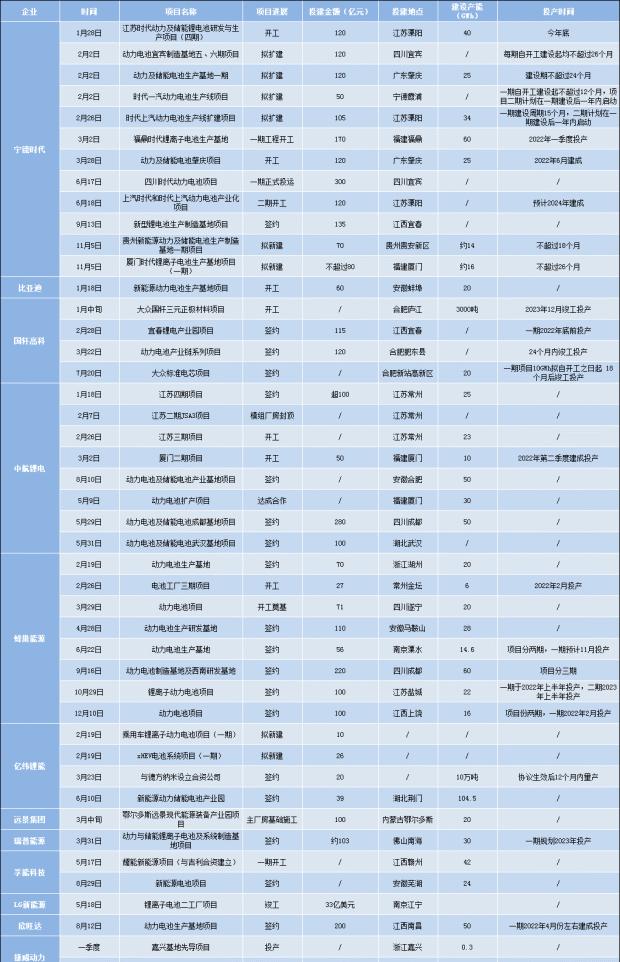

From the statistics, it is not difficult to find that from the first-line Ningde era, BYD, to the second-line Guoxuan Hi-Tech, China Innovation Airlines (AVIC lithium battery), Hive Energy, Yiwei Lithium Energy, and then to the third-line Fu Neng Technology, Ruipu Energy, Sunwoda, etc., all mainstream power battery manufacturers have opened capacity expansion this year.

Even regardless of the current size, they have almost set themselves a grand 2025 capacity target this year:

In addition to Hive Energy announcing that it will challenge 600GWh production capacity and shipments of 450GWh in 2025, some institutions have predicted that its production capacity in 2025 will be about 600GWh according to the capacity planning of the Ningde era;

BYD has news that its production capacity in 2025 may reach 430 GWh;

Guoxuan Hi-Tech said in its semi-annual report that it strives to achieve a production capacity of 300GWh in 2025;

At the strategic press conference, China Innovation Airlines made it clear that it plans to have a production capacity of 500GWh in 2025;

Liu Jincheng, chairman of Ewell Lithium Energy, bluntly said that the target for 2025 refers to the production capacity of power storage batteries of 200GWh;

Ruipu Energy's capacity plan for 2025 is 200GWh;

With the blessing of Mercedes-Benz, Fu Neng Technology also announced that the production capacity target for 2025 is expected to exceed 120GWh;

……

In this way, just these few companies, the capacity plan for 2025 is close to 3000 GWh.

In the forecast of most research institutions, the demand for power batteries will be around 1TWh in 2025. In other words, if we advance according to the current capacity plan, the overcapacity of the entire power battery industry will become inevitable.

However, in the context of the deterministic growth of downstream battery demand, every company in the middle is more willing to believe that they can fly in the wind.

As for whether they will face overcapacity, they have shown absolute confidence.

Previously, Liu Jincheng, chairman of Ewell Lithium Energy, said that in the face of this risk, enterprises need to continuously improve the quality and performance of products. Liu Jingyu, chairman of China Innovation Airlines, said bluntly, "As long as the company's technology passes, there will be no excess capacity."

When the entire industry is racing, it is inevitable that competitors will fall into a strategic situation of not advancing or retreating. In the head of the enterprise to expand the production capacity, others can only be wrapped up in the move forward. If not, there is only the end of being eliminated.

Raw material scramble, "crazy" like a land auction

At the end of October this year, Australian miner Cattlin released a set of data. Lithium concentrate, an important raw material for power batteries, reached an average price of $1650/ton in the fourth quarter, up 112% from $779/ton in the third quarter.

This is something that has never been the case before. Together with the expansion of production capacity, the "mine grabbing war" in the upstream of the power battery industry is also in full swing.

Or take lithium ore as an example. Because this raw material is highly dependent on imports, domestic battery manufacturers have gone to sea and waved banknotes to buy lithium mines overseas.

Among them, it has to be mentioned that the "Ning Lithium War" between the Ningde era and Ganfeng Lithium Industry.

When it initially planned to acquire Canadian lithium company Millennium Lithium, Ganfeng Lithium expected the transaction amount to not exceed $353 million. But who knows that in September, the Ningde era crossed a lever and raised the price to 376.8 million Canadian dollars. In the end, Ganfeng Lithium, which was not willing to give up, had to raise the price again to about 500 million Canadian dollars.

In this regard, some insiders have lamented, "Now robbing upstream lithium resources is as fierce and crazy as the previous soil auction market."

Changes in the price of lithium carbonate raw materials from 2019 to 2021

In order to obtain more upstream resources, these battery manufacturers who originally focused on manufacturing also had to start learning capital operations and investing in the industrial chain with the help of capital power to expand their right to speak in the industry.

In April this year, Hive Energy officially established Hive Capital, spending 2 billion yuan to set up two funds, growth and innovation, participating in and holding some suppliers.

Coincidentally, in September, AVIC Lithium Battery also invested in a capital company, Kaibo (Hainan) Private Equity Management Co., Ltd. The leading big brother Ningde Times has invested in the establishment of 8 private equity investment funds this year, with more than 40 foreign investments.

It can be said that the competition of power battery manufacturers today is not limited to technology and production capacity. Even enterprises that have the full advantage must be proficient in the eighteen martial arts in the entire business field.

From naming to mass production time, technical route, comprehensive inner volume

Even when naming batteries, they have to grasp the right way precisely.

Before the emergence of BYD's blade battery, people's cognition of the power battery category still mostly stayed on ternary lithium batteries and lithium iron phosphate batteries.

After BYD's blade battery was well known for its technical strength and simple image, the naming of the power battery even began to roll inward.

GAC's magazine battery and the Great Wall's Dayu battery

From the sodium-ion battery of the Ningde era to the short knife battery of hive energy, even car companies have come to join in the fun. GAC's magazine battery, the Great Wall's Dayu battery, Lantu's amber battery, Zhiji's silicon-doped lithium battery...

Some of these are new names brought about by new technologies, and some are trying to wrap up their selling points with simple and memorable names so that people can quickly remember them.

As a result, today's power battery industry has also become like the automotive industry, "a good name is not a panacea, but no good name is a must."

Even this kind of marketing roll continues to be the first to mass-produce solid-state batteries.

In recent years, solid-state batteries have been increasingly recognized as next-generation battery technology solutions that can disrupt the entire automotive industry. Therefore, in order to attract the attention of consumers, battery companies and car companies have recently begun to announce the mass production time of solid-state batteries to the outside world.

And the first person in this is Weilai.

At the end of last year, NIO released a 150kWh solid-state battery on NIO Day, saying that the solid-state battery can achieve ultra-high energy density of 360Wh/kg. The NIO ET7 sedan with the battery pack will have a range of more than 1,000 kilometers, and the product is scheduled to be delivered in the fourth quarter of 2022.

However, after the release of this news, it attracted many questions. Many practitioners said that according to the current technology, solid-state batteries cannot be mass-produced for electric vehicles on a large scale. Zeng Yuqun, chairman of the Ningde times, even admitted that in 3 to 5 years, what can be done in the car is not an all-solid-state battery.

Whether Weilai will be punched in the face or will prove himself, and it is up to time. However, in order to enhance the competitiveness of their own new energy models, some domestic and foreign car companies not only cooperate with battery suppliers in joint ventures, but also personally develop their own battery technology and self-built battery factories.

Earlier, Zeng Qinghong, chairman of GAC Group, had mentioned that "the global automotive industry has already started a battery talent battle, and GAC dug up some core talents of LG, Samsung, and Japanese Yuasa battery manufacturers five years ago."

Through independent research and development in recent years, GAC has indeed made good progress in overspeed batteries and sponge silicon anode chip batteries. However, while constantly challenging the difficult liquid lithium battery technology, in order to increase the future chips, many car companies are also taking a diversified battery path. Taking GAC Group as an example, according to Zeng Qinghong, they will accelerate the development of hydrogen fuel cells and solid-state batteries in the future.

Write at the end

Not long ago, SNE Research, a South Korean market research institute, released the global power battery installed capacity ranking for October 2021 and January-October.

The data shows that in the top 10, Chinese companies occupy 6 seats. At the same time, CATL dominates with a market share of 34.2%, far surpassing South Korea's three giants LG New Energy, SK Innovation, Samsung SDI, and Japan's Panasonic.

However, in recent days, Ouyang Minggao, an academician of the Chinese Academy of Sciences and vice chairman of the China Electric Vehicle Hundred Association, said in an interview that although China is currently in an absolute leading position in the supply of automotive power batteries, in the field of solid-state batteries, it will take at least five years for China to catch up with Japan.

For domestic battery companies, in addition to competing with each other, don't forget to look up and look farther ahead.

* Some information references:

Cast in the network "The innermost track in the history of the real, 350 billion yuan was thrown in half a year, and 7 bosses were rumored to be "squatting and taking goods""

Time Weekly "Immortal Fight! Ningde era, Ganfeng lithium industry overseas snapped up lithium ore, as crazy as the previous soil auction"

autocarweekly "The hardest level to do batteries is to name"

CBN "Car companies pile up to bet on solid-state batteries, what are the chances of winning this technical route?" 》

![2021 power battery installed capacity TOP10 analysis: Ning Wang's triple anxiety Honeycomb entered the list for the first time[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)