Text | Hickory Rust-free bowl

After a period of introduction to the upgraded version of Apple TV that most people don't pay attention to, and even want to fast-forward, as usual, Cook, wearing a blue hoodie, quickly cut to the right topic of this Apple spring product launch.

To sum up, this conference has mixed feelings.

Previously, based on the breaking news of major media, Apple is likely to launch a new iPhone SE, a new iPad Air and a new Mac at this spring conference.

After the press conference, the new can be divided into three categories: reasonable, a little unexpected and unexpected.

Reasonable new -

Regarding the new color of the iPhone 13 - green, the official translation is "Cangling Green", and some netizens commented that it was "Leek Green".

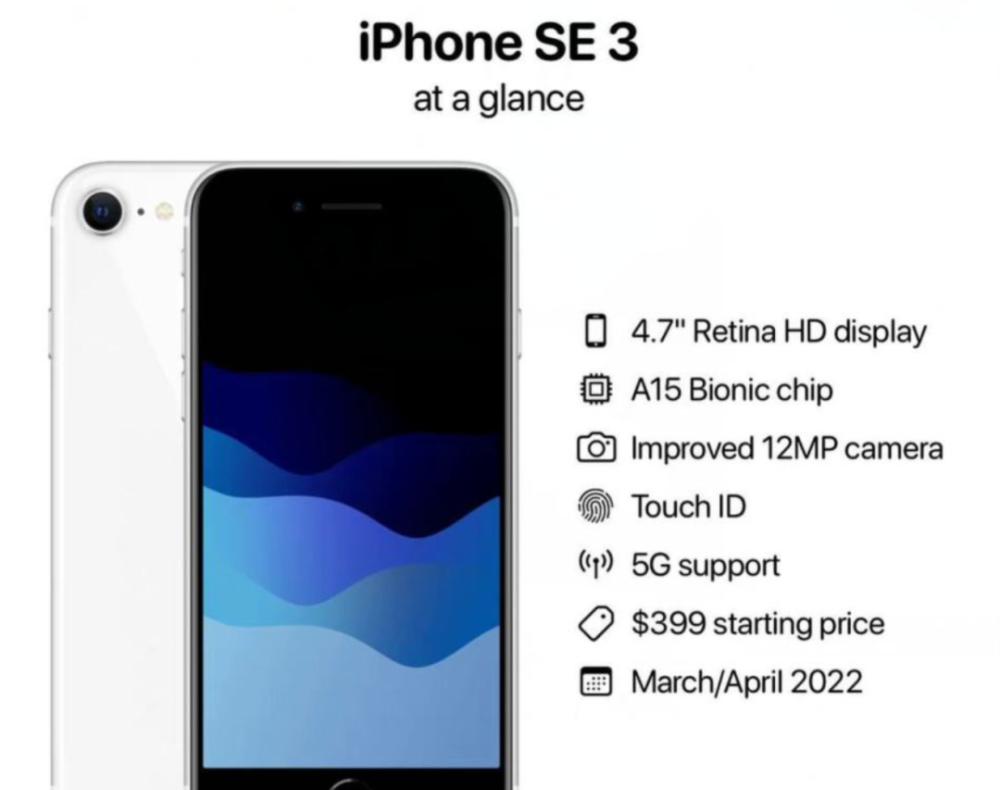

About the iPhone SE – priced from $429 to RMB3,499; powered by the A15 bionic chip of the iPhone 13 series; colors in midnight, starlight and red; 4.7-inch Retina HD display; the same glass as the iPhone 13 series backplane; support for TouchID; and support for 5G.

A bit of an unexpected update -

About the iPad Air 5 – priced from 599 yuan, starting from 4399 yuan; 64G and 256G capacity configurations; the colors are deep space gray, starry sky color, pink, purple and blue; equipped with a 12-megapixel ultra-wide-angle camera, supporting character centering; supporting 5G. It is worth noting that unlike the A15 chip that is speculated by the outside world, Apple directly devolved the iPad Pro chip M1 to the iPad Air.

Unexpected new -

About the M1 series of chips - unlike the media speculation about the launch of the M2 chip, the M1 series ushered in the launch of a doubled version of the M1 Ultra, with 114 billion transistors, which is 7 times that of the M1.

About the Mac - the new mac Studio, equipped with M1 Ultra; priced at $3999, the National Bank of China from 29999 yuan; 7.7 inches, 4 Thunderbolt ports, the performance is 3.4 times that of the current top iMac, 80% higher than the top Mac Pro.

Outside of the lively Apple launch, this article will try to answer the following three questions:

1. Why is this spring conference "mixed"?

2. Does Apple's "soft and hard" strategy have growth?

3. Where is Apple's new growth driver?

A "mixed" update

There were six new models, the first four of which took less than thirty minutes.

To sum up, there is really nothing to talk about.

You can see Cook repeating the story of "old bottle new wine". For example, when releasing the new color of the iPhone 13, it was repeatedly emphasized that "how good the iPhone 13 was bought." For example, when mentioning the iPad Air 5, it is once again combined with advanced productivity.

In the spotlight is the new iPhone SE 3, which Cook considers to be the cheapest iPhone, although it is equipped with A15 chips, 5G networks and iOS ecology and Apple services, and sells from 3499. This is certainly Apple's cheapest phone, but it's not the best option for users. If you know the history of the iPhone SE, it's been the story since its release in 2016 — with the latest chips, the lowest prices, and some feature updates that some don't.

More importantly, the price of more than 3,000 Yuan Apple Entry Machine in Android is not low. In the era of domestic mobile phone screens and stacking materials such as Xiaomi and OV, how attractive the new iPhone SE can be, perhaps to mark a question mark. After all, the official performance comparison was made on the iPhone 8 five years ago.

Now the price of the new iPhone 8 (64G) is in the early thousand, and the second-hand model is less than a thousand.

Of course, if you're a fan of the iPhone SE retro design, the above statements can be ignored.

After four new products, Cook left more time for the latest chip M1 Ultra, and an average of three or four new products came out to introduce. Perhaps the most "surging" is this moment - when the camera begins to demonstrate the birth process of the M1 Ultra, two pieces of M1 Max "paste" composition.

The official description of this M1 series finalists leap forward: M1 Ultra through the polycrystalline silicon architecture Ultra Fusion, the grain density can reach 2 times the existing technology; 20-core CPU, 64-core GPU, 8 times faster than M1, media processor engine performance is 2 times that of M1; with 114 billion transistors, 7 times that of M1, the transmission speed is as high as 2.5TB/s, and the performance power consumption is 90% lower than that of today's 16-core computers.

In other words, the M1 Ultra requires only 1/3 of the energy consumption to achieve the same performance.

Obviously, this is the big flag that Apple made the year before pulling out, announcing the success of the self-developed chip to the outside world and showing the confidence to replace Intel. At the WWDC Developer Conference in mid-2020, Apple announced that it would abandon the X86 architecture and launch the Arm-based Mac chip M1.

This is a strategic shift for Apple, further differentiating itself from other companies in the PC industry, especially when Moore's Law is reaching its limits, and the advantages of customized self-developed chips are highlighted.

But in a number of "Apple killed crazy" evaluations, whether M1 Ultra is a subversive innovation is still debatable.

After all, stitching two chips together is just an upgrade of the physical connection level. In essence, the M1 Ultra has no new process process or new architecture, but is just a new physical connection method that combines the "super cup" of two M1 Max chips.

As for the official statement that "only 1/3 of the energy consumption can reach the same performance of 12900K", previously, the industry has also compared the running score test results of the Core i9-12900K and M1 Max series, the average running score of the geekbench 5 of the two is 18500 and 12500 points, combined with the peak power performance of 241W and less than 60W, it can be said that before the introduction of the M1 Ultra, 12900K and M1 Max has achieved the above "1/3" energy consumption ratio performance.

This also confirms that the M1 Ultra only continues the past advantages of the M1 series. Of course, objectively speaking, this is already very good. After all, in the hardware industry, the vast majority of cases are "1+1."

On the other hand, although Apple has made a way in the chip market dominated by Intel, the transformation of its self-developed chips is still bumpy. In January, Jeff Wilcox, the hero of Apple's M1 chip, left Apple for Intel. Earlier, three engineers also left Apple to start a new chip company called Nuvia, which was eventually acquired by Qualcomm.

But obviously, Apple relies not only on chips, through the "hardware + software" technology ecology, chip technology innovation can help Apple continue to improve the bargaining power of the upstream and downstream of the industrial chain, which is a win-win situation for Apple, which has a strong supply chain capability. As Wayne Lin, senior director of the Americas Research Department at CCS Insight, a global authoritative market research organization, said:

"Apple can use its dominance to squeeze more profits from consumers, or take away most of the value in the supply chain, giving industry players like Intel a smaller share of the industry's value pie."

Soft and hard, Apple's attack and defense

After entering the "Cook era", in recent years, Apple's overall strategy has been combined back and forth between hardware and software services.

The only landmark move can be traced back to 2018, when Apple announced that it would not announce the specific sales of hardware devices (iPhone, iPad and Mac), which was regarded by the outside world as an important symbol of Apple's "hard to soft".

Instead of telling wall street and friends the story of "selling more", Cook may want to show the "more profitable" side of Apple. The Apple operations guru used such an image metaphor to explain the doubts of the outside world:

"You'll fill your basket with stuff, and the camper might say, 'How much stuff is in it?' However, in terms of total value, the number of items in the shopping cart does not matter, and no one cares about this. ”

In fact, before the spring press conference, Apple and Cook handed over an answer sheet that exceeded market expectations - in the fourth quarter of 2021, Apple's revenue in the quarter was $123.945 billion, the highest quarterly record in Apple's history; net profit was $34.630 billion, an increase of 20% in the same period.

Based on this calculation, Apple net earns about $380 million per day.

In terms of business structure, except for the decline in iPad revenue, the rest have shown a state of growth. The iPhone, which accounted for more than 50% of the total, is still the "locomotive", with revenue of $71.63 billion in the quarter, up 9.2% year-on-year; Mac revenue of $10.85 billion, an increase of 25% year-on-year; revenue from other products of $14.701 billion, up 13% year-on-year; and services revenue of $19.516 billion, an increase of 24% year-on-year. iPad revenue of $7.25 billion, down 14% year-over-year,

On the earnings call, Cook acknowledged Apple's growth: "The market share of Apple products is also increasing, so we are very satisfied with the growth momentum of iPhone products." ”

Strictly speaking, in the past period of time, aside from the bright performance, Cook and Apple have not been moist. On the one hand, the supply chain shortage and lack of core in the field of consumer electronics are shrouded, and on the other hand, the clichéd "squeezed toothpaste" performance and improvement and "no surprise" conference.

It's an indisputable fact that Apple still sells well. According to a report released by Canalys, in terms of shipments, Apple regained the top spot in the global smartphone market in the fourth quarter of 2021, and the last "first" dates back to the fourth quarter of 2020.

In the fiercely competitive Chinese market, according to data from market research institute Counterpoint, Apple's market share rose from 11% to 16%, and the sales growth rate reached 47%, becoming the largest annual increase in mobile phone manufacturers.

The biggest hero is the "thirteen incense" that netizens complained about. After all, as the main source of revenue, if Apple wants to sell well, it must first make the iPhone sell well.

With the strategy of "increasing the amount without increasing the price", Apple has locked in the advantages of a group of domestic mobile phones in the collective encirclement and suppression of the high-end market. But in fact, pulling the long line to see - selling well is true, selling expensive is also true.

Image source: CITIC Securities

According to CITIC Securities data, the average selling price of the iPhone has risen slightly, from $660 / one in Q2 2015 to $866 / one in 2021Q2, and the average selling price of the iPhone has increased by about 31.2% in the past five years.

When the global smart phone enters the low-speed growth stage, in the stock market, the eyes of cook with accurate knife skills will of course always have only the interests of "Apple", after all, from the perspective of revenue structure, Apple is still a company that makes money by hardware.

That seems to be a different image than Apple executives want to present. Because, in recent years, whether on conference calls or in earnings reports, they have repeatedly mentioned the benefits of their software services. There is no doubt that behind the software service is Apple's independent ecological advantage, but in the short term, it is possible to rely on "ecological" storytelling, but it is not so easy to make money.

In the case of hardware growth, Apple's service sector has maintained double-digit year-on-year growth, and the three major revenue drivers of License, App Stroe and subscription services have grown considerably. At a macro level, the advantages of the software services business are obvious. On the one hand, the increase in the average selling price of the hardware-side superimposed single device can drive the continuous increase in software service revenue. On the other hand, since the services segment does not have a clear off-peak sales season, it is more profitable and sustainable.

Apple Services Section Content Source: CITIC Securities

But the reality is that software services have not brought significant growth to overall revenue, in fact, Apple did not disclose the specific revenue composition of its service sector in the financial report. According to CITIC Securities' calculations, in fiscal 2020, license, APP Store, subscription services & other business revenue was $11.1 billion, $20.3 billion and $22.3 billion, accounting for 20.7%, 37.8% and 41.5% of the overall revenue of the services segment, but for Apple, which earned $274.515 billion in fiscal 2020, the proportion of overall revenue was only 4.04%, 7.3% and 8.1%.

Therefore, Cook, who is attacking software services, wants to harvest a steady stream of recurring revenue from the Apple ecosystem, which cannot be achieved in the short term. Trying to become a service giant, with the huge and powerful purchasing power of subscribers behind Apple pulling out their pockets, is far less easy than it seems in the earnings report.

In a way, Apple seems to be born with no genes to do software services. Counting the failed works in Apple's history, whether it's Mobileme, which Jobs called "not the level Apple should be", or Apple Maps, which the New York Times rated as "the most embarrassing and impractical that Apple has ever released"... The core reasons for failure are not difficult to understand. Software services are a model of exchanging scale for business, but Apple's hardware entrance has a threshold, so the coverage of its software services is also limited.

To prop up a market value of three trillion, Apple needs to find new impetus

Since the hardware growth rate is weak, and the software service is not as profitable as imagined, where is Apple's new growth point?

Answering this question is like answering "How can Cook launch disruptive innovations", whether it is Apple or Cook, they urgently need a magical moment.

It wasn't just one person trying to get the answer out of Cook's mouth. In a recent conversation with a Reporter from The New York Times, Cook responded with his usual, restrained and calm response to rumors of product plans that represent Apple's future (Apple Cars, VR/AR, etc.):

"Apple doesn't like to talk about the future, and if we don't hide something, it won't be us."

But the reality is that soaring market capitalization (Apple's market value briefly exceeded $3 trillion) is demanding more responses from Apple, using a new growth curve to provide important support for long-cycle growth.

Bullish Wall Street analysts have found the answer for Apple. TFI Securities analyst Ming-Chi Kuo, after continuously tracking the research report of AR/VR helmets, expects Apple's AR/VR helmet sales to reach 1 billion in the next 10 years. He believes that such products will eventually replace the iPhone as the most important online experience for many people.

Morgan Stanley analyst Katy Huberty also wrote: "The new products to be released soon do not seem to be reflected in the stock price."

The new products are wearables (AR/VR headsets) and self-driving cars, two of Apple's undeleased lines of business.

While the Zuckerbergs are struggling to find an entrance to the Metaverse, the most profitable person may be Cook, who makes a fortune in a muffled voice. Combing through public information, Apple's exploration in the AR/VR field has been more than a decade.

Whether it is throwing money to do the headset, patent research and development and talent team formation that has lasted for many years, or the mergers and acquisitions in the upstream and downstream of the industrial chain, there are many signs that Apple is serious about doing VR/AR.

Back in 2016, Cook took the trouble to mention the AR outlook in public. In a public speech at Oxford University, Cook talked a lot about AR, and hinted at the linkage between AR and Apple's ecology:

"I can see the use of AR in education, consumption, entertainment, sports, I can see everything I know. In addition, it does not isolate people, which also makes me like it more. ”

Having said that, when it really entered the VR/AR track, Apple still followed Cook's "restraint." In 2017, ARKit was seen as a sign of Apple's entry into the AR space. But in essence, it is still a wedding dress for Apple's hardware products, continuing the strategy of the Jobs era, and strictly speaking, it is not Cook's innovation.

In 2022, after multiple "wolf coming" predictions, Apple is expected to launch AR glasses. Previously, Guo Mingji, an analyst at Tianfeng Securities, said that Apple's "computerized" smart glasses will be as powerful as Apple's Mac computer in performance, and the product will be released in 2022.

Guo Mingxi revealed that Apple's smart glasses will use a processor based on the M1 design, and in terms of product marketing, Apple will position smart glasses as an accessory for the iPhone, rather than an alternative tool for the iPhone.

This could be another innovation for Cook, trying to create an image of a "disruptive innovator." Although, Jobs has used the iPod, iPhone and iPad to set the overall tone of the story.

In Apple's "Cook era," despite the introduction of AirPods and Apple Watch, and in the eyes of Cook's unofficial biographer Leaner Kahney, the two products have become "Cook's legacy," the Cook writer is clearly indignant about the low-key Apple successor: "Cook is not getting the recognition he deserves."

The reality is that the VR/AR track will become more and more crowded, and the entry of the number one player will further harvest the few markets. According to Counterpoint data, in the 2020 global AR/VR mainstream vendor market share ranking, Facebook's Oculus has the highest market share, accounting for 53.5%; Sony's market share of 11.9%, ranking second in the world. The 3rd-5th places were HTC (5.7%), DPVR (5.5%) and Pico (4.8%), and the top 5 accounted for 81.4% of the total, with a high concentration.

Although people are not worried about Apple's ability to catch up later, for Cook, who has always prioritized profits, the era of VR/AR monks is approaching.

Another big growth point is in car building. Previously, in the article "Apple Car Making Time", Cai Wei wu jie combed the beginning and end of Apple car manufacturing in detail, and believed: "Although as a follower, Apple car manufacturing is not optimistic, but the 'catfish effect' it brings to the entire industry is bound to be far-reaching and huge." ”

According to Bloomberg, it is expected that in 2023-2025, Apple will launch its own self-driving vehicle iCar. In the long run, the story of "building cars" is an important attraction for Apple to Wall Street. But in the short term, Apple's entry into the field of smart cars, the biggest significance may only be to expand market share.

Regarding car building, Apple may need to think clearly, whether to replace it through imitation, or to create a new market with a subversive innovation strategy like jobs in the era of Jobs.

In short, the "Apple Car" that has been confused for many years should also have an appearance in recent years.

Of course, for Cook and Apple, it may no longer matter whether there are new highlights at the conference. After all, people with "verbal integrity" will still pay for Apple's strategy, staying up late again and again to listen to Cook tell old stories.

Not a product guru, but it must be a master of operations — the people who know Cook best may also be those who are most optimistic about Apple, such as Buffett, who is heavily positioned for Apple. "Tim may not be able to design a product like Jobs," Buffett said, "but he knows the world to a level that very few people can match." ”

He also used a comparison: "Very, very few CEOs I've met over the past 60 years can match [Tim]"