Text | Aries

The "Three Red Lines" that came out in August were meant to force the brakes on the unscrupulous leverage of highly indebted developers, but since the regulatory authorities showed the sword of Damocles, the scale of developers' bond issuance has not gone down, but has borrowed more fiercely.

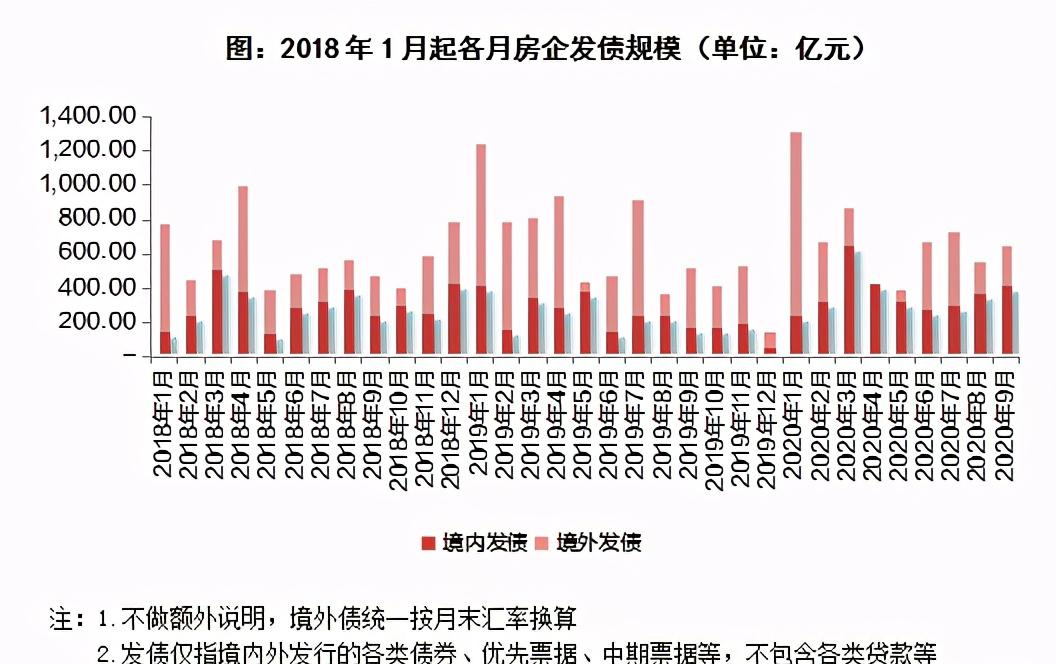

Wind data shows that since September, the domestic bond issuance scale of housing enterprises has reached 101.749 billion yuan, an increase of 56.9% year-on-year.

Kerry statistics also show that the total amount of financing and bond issuance of 95 typical housing enterprises in September was 65.144 billion yuan, up 16.6% month-on-month and 25.7% year-on-year, all of which achieved a large increase year-on-year.

Among them, domestic debt was 40.890 billion yuan, a new high since March, up 10.3% month-on-month and 140.8% year-on-year.

In March, the domestic debt financing of housing enterprises was extremely high, that is because the epidemic was severe at that time, out of the need to stabilize the property market and warm the property market, the above specially opened the floodgates and released water.

September was the first month after the "three red lines" were launched, and its domestic debt financing scale and large year-on-year increase after March were really unexpected.

From January to September, housing enterprises issued bonds of 628.917 billion yuan, an increase of 96.7% year-on-year, of which domestic bonds issued 328.344 billion yuan, an increase of 139.8% year-on-year, and overseas bonds issued 300.573 billion yuan, an increase of 72.4%. It's a spurt of growth.

Whether it is domestic debt or foreign debt, whether it is a cumulative increase or a 9-month increase, this year seems to be a big year for housing enterprise financing.

In the face of data, the so-called "three red lines" and "tightening of real estate financing" seem to be "grandmothers beating children" - just for example.

Is this really the case? Let's sort out the timeline first

On June 24, the China Banking and Insurance Regulatory Commission issued a document emphasizing "strict control of illegal funds flowing into the real estate market";

On July 24, Vice Premier Han Zheng presided over a symposium on real estate work, which proposed to "implement a prudent management system for real estate finance";

On August 20, the Ministry of Housing and Urban-Rural Development and the People's Bank of China held a symposium on key real estate enterprises, pointing out that the so-called key real estate enterprise capital monitoring and financing management rules were formed, that is, "three lines and four files".

The "three red lines" are specifically: the asset-liability ratio after excluding advance receipts is greater than 70%,the net debt ratio is greater than 100%,and the cash short-term debt ratio is less than 1 times.

According to the situation of housing enterprises "stepping on the line", it is divided into four grades of "red, orange, yellow and green", and implements differentiated debt scale management:

If the three indicators exceed the threshold of "red file", the scale of interest-bearing liabilities of housing enterprises shall be capped at the end of June 2019 and shall not be increased; if the two indicators exceed the threshold of "orange file", the annual growth rate of interest-bearing liabilities shall not exceed 5%; if one indicator exceeds the threshold as "yellow file", the annual growth rate of interest-bearing liabilities shall not exceed 10%; the three indicators shall not exceed the threshold of "green file", and the annual growth rate of interest-bearing liabilities shall not exceed 15%.

It is also understood that for real estate enterprises that have a land sales ratio of more than 40% in the past year or whose net cash flow generated by activities has been continuously negative in the past three years, the regulator will also reduce the scale of their credit bond issuance according to the actual situation, and impose restrictions on trust financing, asset management products, overseas financing, etc.

This is also considered to be the most stringent debt control policy for housing enterprises in history, and the real estate industry itself is an industry with strong financial attributes, controlling the borrowing and leveraging behavior of housing enterprises, which is equivalent to taking away the control of "throttle" and "brake" from the feet of housing enterprises, and then blocking the possibility of housing enterprises achieving overtaking through counter-cyclical expansion of leverage.

Only when the housing enterprises are no longer aggressive and can no longer counter-cyclical operations to exacerbate the pro-cyclical push, can the property market avoid the frenzy of the momentum and truly achieve healthy and stable development.

As an important part of the long-term mechanism under the "housing and not speculation", the "three lines and four gears" for the financing of housing enterprises can be said to have done a major operation on the property market from the supply side, and its significance is worth affirming.

On September 14, Pan Gongsheng, deputy governor of the central bank, said at the State Council's regular policy briefing that the current capital monitoring and financing management rules for key real estate enterprises have started smoothly, and the social response has been positive; the rules will continue to improve and steadily expand the scope of application.

On October 14, Peng Lifeng, deputy director of the Financial Market Department of Chinese Min bank, said at the third quarter financial data conference that the capital monitoring and financing management rules of key real estate enterprises are an important part of the construction of a long-term mechanism in the real estate market, with the purpose of promoting real estate enterprises to form stable financial policy expectations, while also correcting the blind expansion of some enterprises.

It can be seen that the original intention and thinking of the regulatory authorities in controlling the borrowing and leveraging of housing enterprises are very clear and irreversible.

For the current "words and deeds", it is not difficult to explain, first, although the official has shown the sword of Damocles, it did not immediately sheath, but gave the housing enterprises a window period to adjust their own liabilities and leverage, so as to prevent enterprises from causing a crisis due to insufficient preparation. That is to say, there is a certain lag in the implementation of policies;

Second, the psychological impact of the three red lines on housing enterprises is still quite large, and now in addition to accelerating sales and repatriation of funds, it also forces more housing companies to rush to raise more grain and grass (borrowing) as much as possible before the financing window is tightened, and expand the margin of cash flow safety after entering the cold winter.

The most illustrative of this is to take land, although the scale of domestic bond issuance by housing enterprises hit a new high in September, but the amount and enthusiasm of housing enterprises to obtain land are falling sharply.

As shown in the figure below, after entering the second half of the year, the amount of land taken by top50 housing enterprises has declined significantly, especially in the second month (September) after the "three red lines" were released, which once again showed a cliff-like decline, which is in stark contrast to the first half of the year.

It shows that housing enterprises are stepping up financing at this moment to reserve winter grain.

Of course, in addition to grabbing the window period, there is also an advantage of stepping up at this time, that is, the financing cost is relatively low. The financing cost of domestic bonds in September was 4.33%, although it was higher than in the first half of the year, but it was still down nearly 1 percentage point from the whole of last year.

When the regulatory authorities close the door to financing, a real knockout game in the real estate industry will begin.

Housing enterprises can no longer fight the cycle through high debt and high leverage, and only by relying on real skills (financing ability, sales ability, cost control ability, product strength) can they grab more cakes. And those housing enterprises that will only rely on the sky (policy) to eat will take the lead in falling, or be swallowed up by other large housing enterprises.

Of course, the official will not sit idly by and watch a large number of housing enterprises cause systemic risks due to cash flow depletion, so the future will be loosened according to the specific situation, but the overall tightening situation is basically certain.

The current high bond issuance can be understood as the developer's final madness.