China-Singapore Jingwei March 21 Title: Three issues in the relationship between banks and enterprises in the digital age are worth pondering

The author is Chen Daofu, Deputy Director of the Institute of Finance, Development Research Center of the State Council

Shengxi Cao is an assistant researcher at the Institute of Finance, Development Research Center of the State Council

The bank-enterprise relationship refers to a series of explicit and implicit contractual arrangements formed between banks and enterprises. As far as a country is concerned, due to its economic development level, financial supervision model, legal and cultural background, level of scientific and technological development and other factors, the relationship between banks and enterprises is relatively stable in the short and medium term. However, technological progress in the digital age has led to more convenient access to information, reduced processing costs, and the reconstruction of bank-enterprise relationships. This not only adapts to the needs of the times, but may also trigger some new risks, and it is necessary to actively promote transformation and guard against possible risks.

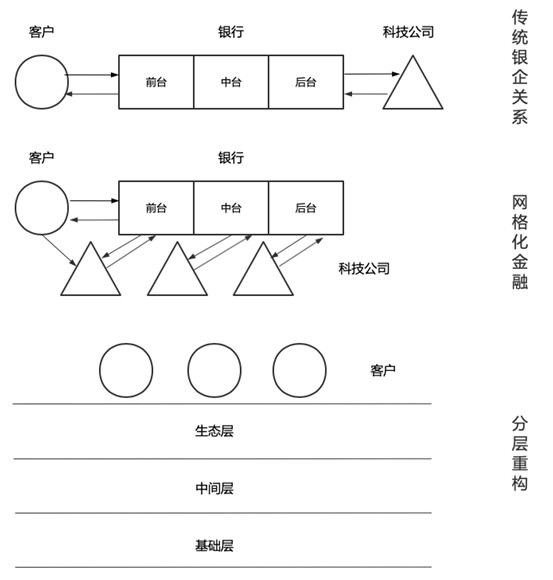

At present, the application of fintech in the banking industry is shifting from "external cooperation" to "internal embedding" and "platform reconstruction". Affected by the cross-border competition of technology companies and the guidance of government policies, banks have gradually opened their own business, trading systems and underlying account data to third parties in the process of balancing privacy, security and value creation. At the front of the business, banks cooperate extensively with third-party institutions in the fields of online lending, mobile payment, account opening, and fund depository. Especially in terms of customer drainage, many banks provide API interfaces on large third-party Internet platforms such as social networks, e-commerce platforms and search engines to attract customers to purchase banking financial products and services; in addition, through convenient payment practices such as open banking, banks also open basic data to third-party technology companies with customer consent. In the middle office, banks work with third-party institutions to improve their information sources and data analysis capabilities in customer identity verification, user portraits, risk control, service pricing, etc. In this process, technology companies have deepened their grasp of the core capabilities required for bank middle offices, and the applicability of models has continued to increase. In the business background, banks have introduced relatively mature technologies and products of third-party technology companies through technical cooperation, joint development, outsourcing services and other basic fields such as cloud computing capacity building, data security storage, big data analysis modeling, mobile Internet application development, and network security protection, which have improved their own scientific and technological capabilities and reduced construction costs.

The relationship between banks and third-party technology companies has changed, and the two sides are no longer relatively independent organizations connected only through limited business contacts. The constantly refined division of labor allows all kinds of cooperation to penetrate into the banking business chain, and technology companies and banks form a grid connection. With the advancement of digitalization and the deepening of mutual understanding, transaction costs will be further reduced. This will promote the blurring of traditional organizational boundaries and lead to organizational restructuring. The model of banking service enterprises has also changed, first from the original "vertical integration" to "grid", and then to the ecological layer (direct customer-facing service), the middle layer (application modules and data processing tools) and the basic layer (underlying data) layer of the "platform" model (see Figure 1).

Figure 1: Schematic diagram of the evolution of the customer-bank-technology company relationship

Fundamentally, the relationship between banks and enterprises is the connection between organizations, which explores the problem of organizational boundaries, and different bank-enterprise relationship models are determined by information characteristics and transaction costs. Therefore, in the digital age, the reconstruction of bank-enterprise relationships can be examined from this perspective. There are three major issues worth pondering at the moment.

First, how do you view the "bank demise theory"?

Based on the above analysis, the role of banks in the financing chain will change, and there are four possible forms. First, the relationship between banks and enterprises has been strengthened. Banks strengthen the relationship between existing banks and enterprises through the construction of their own financial technology platforms, and even participate in corporate management in part, and rescue enterprises in times of crisis. Second, the relationship between banks and enterprises is loose, and the service is modular. Banks adhere to the financial links such as payment, financing and loans, and strengthen cooperation with third-party technology platforms. The third is the platform-led "bank-platform-enterprise" relationship. Banks are solely responsible for balance sheet management and regulatory compliance obligations as funders. Large Internet platform companies have become integrated integrators of corporate financial services. The fourth is financial disintermediation. Platform companies become the infrastructure for matching supply and demand for financial services, fulfilling financial functions entirely through direct financing and intermediary organizations. In reality, large banks and small and medium-sized banks may move towards different models. Large banks have a good market foundation, strong capital and strong technical capabilities, which will strengthen the relationship between banks and enterprises and transform them into important nodes and comprehensive platforms for digital financial services. The market foundation of small and medium-sized banks is relatively weak, and the capital and technology capabilities are insufficient, and they are more inclined to choose a looser bank-enterprise relationship of service modularization and focus on serving specific industries.

Second, can information be fully made public?

In the digital age, data has become a factor of production, the information industry chain has been extended and socialized, and data has been effectively used in a wider range. But to produce effective data, autonomous behavior of market players is required. Considering the inherent incentive and constraint mechanism requirements of the information industry chain and the individuality of soft information, information in the digital age will have stronger public attributes, but it is still necessary to retain the necessary privateness, and it is necessary to achieve reasonable publicization of information through a reasonable distribution mechanism that balances information security, privacy, value sharing technology and benefit distribution mechanism. The publicization of information may lead to insufficient incentives for information collectors. Theoretically, the shared information belongs to the public goods of the whole industry, the information collection behavior is positive externalities are high, the cost needs to be borne by the information collector, but the benefits are shared by the whole industry. In particular, the non-standardized information of some enterprises needs to pay a higher cost to obtain. Banks could have covered the previous information collection costs with long-term rental income, but after information sharing, banks lost the possibility of charging relatively long-term high rents, and they lacked the motivation to collect corresponding non-standardized information. According to scholars' research on the impact of credit score sharing, information sharing does reduce the cost of switching loan banks, especially for small and medium-sized enterprises with short credit histories. However, information sharing does reduce banks' willingness to provide long-term loans to enterprises, suggesting that banks have less incentive to collect proprietary information after information sharing.

In addition, the important role of soft information is difficult to replace, especially in the economic downturn. The information used for corporate loan decisions can be divided into two categories, one is public information (balance sheet, rating, and even more detailed transaction behavior, etc.), which is called hard information because it can be quantified; the other is internal information that needs to be obtained through repeated interaction between the loan commissioner and the company manager, such as industry prospects, employee mentality, etc., which is mainly based on the subjective evaluation of the loan commissioner, known as soft information (Soft Information)。 Over the past few decades, due to regulatory pressures and the development of fintech, the scope of hard information has expanded and its role has also increased. However, for SMEs, soft information remains an important determinant of corporate lending. In a crisis, hard information that reflects a company's risk profile loses its predictive power; but soft information about the future of the company is constantly being updated, and banks can rely on this soft information to reduce uncertainty.

Third, is supervision "penetrating reduction" or "node-based" reconstruction?

After the financial industry has realized the refinement and grid of the division of labor, the traditional model of taking a single institution as the core and comprehensively assuming the risks of the financial chain is no longer established. Financial regulators have two options. First, with the current regulatory structure as the cornerstone, in accordance with the principle of "penetrating and restoring", financial institutions are required to carry out consolidated statements of various types of business, off-balance sheet return to the table, etc., to maintain institution-based supervision. The second is to innovate the way of supervision, understand the goals of financial supervision from the essence, grasp the principles of supervision, and create a new regulatory framework and technology according to the changes in the form of financial business.

Financial supervision is essentially to ensure that the rights and responsibilities of each participant are equal, and to internalize externalities as much as possible. Or rather, to ensure that the right people and institutions offer the right products and services in the right form for the right customers. Among them, the qualification review of shareholders, executives, marketing and professionals constitutes the way to ensure "the right person"; the requirements for license management, capital, professionalism and integrity constitute the way to ensure the "right body". Similarly, accredited investors are required to have professional knowledge, risk tolerance and civil capacity; appropriate forms mean conduct supervision, including related party transactions, monopolistic behavior, information disclosure, etc.

Therefore, for the gridded financial industry, the financial supervision can be "node-type" reconstructed. Implement the above-mentioned regulatory spirit into each link of the chain to ensure that the behavior of each node follows these regulatory concepts. Nodes, on the other hand, are subjects that bear the full consequences of their actions.

In short, the digital economy maps the relationship between man and nature and between people to the digital space, and the logic of the rights and obligations of human beings to manage these relations also needs to be mapped to the digital space, so as to fully inherit the existing human cognition and exploration of nature and society in the digital space. (Zhongxin Jingwei APP)

Zhongxin Jingwei copyright, without written authorization, any unit and individual shall not reprint, excerpt or otherwise use. This article does not represent the views of Sino-Singapore Jingwei.

Editor-in-Charge: Lei Wang

![Who are the 50 most active CVCs in the hardcore era?[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)