Over the past few years, chipmakers have shifted from hardware supply to more software services, automakers are still groping to develop their own software, and traditional Tier 1 suppliers like Bosch, Continental, and Aptiv are also accelerating software investment.

But the answer seems to be getting clearer. Today and in the future of the smart automotive industry, chips are becoming the top brand for car companies to market product technology for the C-end. New forces in China's automotive chips such as Qualcomm, NVIDIA and even Horizon are increasingly appearing on the big screen of the new car conference.

Chip manufacturers and traditional tier 1 suppliers are in a critical period of the game. In the past, chips mainly generated transaction relationships with automakers through Tier 1 suppliers, but this indirect partnership was completely broken by the shortage of chips and the opening of the era of "computing power defining the car".

For example, starting in 2024, the new generation of Mercedes-Benz models will use a computational architecture hardware and software (based on the NVIDIA DRIVE platform) program jointly developed with Nvidia, which involves a lot of software development.

On the one hand, the revenue of chip manufacturers from the automotive industry continues to rise. According to the data, the automotive industry contributed nearly $1 billion to Qualcomm's revenue in fiscal 2021, and although its share of overall revenue is still low (less than 5%), the upward momentum has been clear.

Traditional Tier 1 suppliers, on the other hand, are going through the most difficult times. Affected by the global pandemic and the ongoing shortage of automotive chips, Aptiv expects full-year 2021 sales to be 6% lower than expected, and operating margins have also declined due to operational inefficiencies, increased supply chain disruption costs and other uncertainties.

Industry change has always been the driving force for the birth of new business models and the reconstruction of industrial chain relations.

First, how to think from the perspective of the main engine factory

"Chips will play a key role in the autonomous driving revolution in the automotive industry." Nvidia CEO Jen-Hsun Huang predicts that selling new cars at cost prices will no longer be a "fantasy" in the coming years, because profits will come mainly from software.

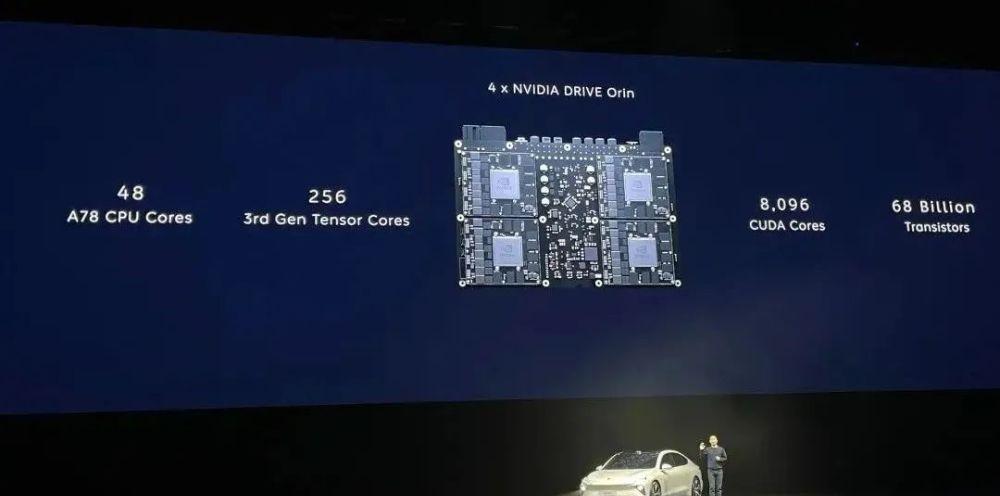

Taking the upcoming NIO ET7 and ET5 models as an example, on the basis of Tesla's previously launched "low-cost hardware embedding + software one-time payment" model, it is directly upgraded to "high-cost (including 8 million pixel cameras, lidar, 4 NVIDIA Orin, etc.) hardware embedding + software monthly payment model".

The more profound change behind it lies in the upgrading of the supply chain "sharing" model.

The cooperation with Mercedes-Benz is regarded by NVIDIA as the "largest single business model transformation" in the company's development history, and through the deep binding cooperation with the main engine factory (more cooperation with Tier1 in the past), the previous single procurement and supply relationship has been changed, and the two sides can share the income of future users to purchase functions and subscription services.

The NVIDIA DRIVE platform, in addition to NVIDIA Orin and the next-generation Ampere supercomputing architecture, includes a complete system software stack that satisfies the full functionality of autonomous driving from L2 to L4, while supporting car companies in data-driven iterative development and deep neural network development.

Under the traditional business model, automakers emphasize "differentiated marketing" to meet different user needs and purchasing power through different model price points and function lists. In the future, Mercedes-Benz wants to make a radical change. "We plan to start in 2024, and all models of our brands will have the ability to run different software."

In Huang Jenxun's view, the most important purchasing factor for users in the future is software that is constantly iteratively upgraded and continuously enhanced in functionality. Whether it is possible to expect new software and be satisfied with it means that the automotive business model will fundamentally change.

As for the question of who will lead the software, Huang Jenxun said that the difference between cars and mobile phones is that the in-car software is customized for the car. "For a long time, automakers will largely dominate the software, which is fundamentally different from the mobile phone industry."

So, what will be the role of chip manufacturers? Hardware vendors, software vendors, or both? "We have to be flexible," Huang said, adding that different customers will have different needs, such as a single hardware computing power solution, or a full-stack rapid deployment solution for software and hardware.

The increase in the importance of software has given chip manufacturers greater initiative.

Arm announced last year that it would provide the automotive industry with a new software architecture and reference implementation, an embedded edge scalable open architecture (SOAFEE), and two new reference hardware platforms.

In the past, whether the performance of the chip could be fully utilized depended more on the tuning of Tier1 and even Tier2. In Arm's view, in order to quickly and seamlessly address the increasing demands of automotive software definition, a standardized framework must be provided and matched at scale with the real-time and safety features required for automotive applications.

As we all know, the ability of the chip to play comes from two parts: hardware and software. Among them, the hardware part involves chip design, manufacturing process, and maximum stacking super configuration. In terms of software, the global energy efficiency of different IP modules and the optimization of the underlying software engine are covered, so as to reduce the power consumption of the whole scenario.

Chet Babla, vice president of Arm's automotive business, said the current challenge facing the automotive industry is to develop, test and manage all software throughout the product lifecycle and on many different vehicle models. Software changes faster than hardware, which means that traditional proprietary software has become anachronistic.

Nvidia DRIVE' open source software stack, for example, helps developers efficiently build and deploy a variety of applications, including sensing, location and mapping, planning and control, driver monitoring, and natural language processing. In addition, the corresponding modular configuration tools are provided.

Another example is the Tiangong Kaiwu launched by Horizon, an AI full-life cycle development platform based on self-developed AI chips, including three functional modules of model warehouse, AI chip toolchain and AI application development middleware, providing chip partners with rich algorithm resources, flexible and efficient development tools and easy-to-use development frameworks.

Targeted user pain points, including masking hardware details, unified algorithm and application development framework, packaging basic components, lowering the development threshold; flexible adaptation to the industry's popular algorithm framework, open and flexible custom application development process; and out-of-the-box product algorithms, basic algorithms and product reference algorithms.

According to industry sources, at this stage, many automakers have begun to "spit" on the engineering development model of traditional first-tier parts suppliers, "some traditional automakers, including Ford, have been dissatisfied with the software development of traditional partners." ”

"We need to further simplify our customers' hardware design efforts, reduce functional safety verification requirements, and reduce the power consumption of the application." Naoki Yoshida, vice president of Renesas Electronics' Digital Product Marketing Division, said. Obviously, in the new track of software-defined cars, chip manufacturers have taken the initiative and have a stronger sense of customer service.

Second, chip companies should make more money

In the past decade or so, Mobileye has pioneered a "black box" business model for chip + software binding in the automotive industry. In the past few years, other peers have "lobbied" automakers to open up market gaps through the chip white box development model.

In particular, the open, rapidly iterative and differentiated intelligent driving system has become the main theme of the head car manufacturer seeking brand technology breakthrough, and the black box model has begun to be unpopular. But business interests are driving these "white box" model seekers to rethink the future.

Two months ago, Tier 1 component supplier Veoneer disclosed that the Extraordinary General Meeting of Shareholders formally approved and adopted the merger agreement, SSW will acquire Veoneer in a cash transaction of $37 per share, and after the completion of the transaction, the company's Arriver business (perception and software part) will be sold by SSW to Qualcomm.

Prior to the deal, Qualcomm and Veoneer had jointly developed driver assistance and autonomous driving systems, and deeply integrated Veoneer's perception technology and software stack with Qualcomm chips. "Part of the reason is that the same chip may not play at a completely different level of performance because of different solution providers."

Two years ago, Qualcomm launched the Snapdragon Ride platform, which offers different levels of hash rates, from 10 TOPS of hashrate for smart ADAS cameras at less than 5 watts of power to more than 700 TOPS for fully autonomous driving solutions.

"The deep integration of Arriver means that Qualcomm will be able to provide customers with full-stack, fully integrated hardware and software solutions; in this regard, similar to the solutions offered by Mobileye." Industry insiders said.

Unlike this, Snapdragon Ride offers an open programmable architecture that allows automakers and Tier 1 suppliers to customize the platform to their different needs for camera perception, sensor fusion, driving strategies, automated parking, and driver monitoring, allowing customers to choose one or more software stack combinations.

For example, an integrated development board support package, as well as software frameworks such as adaptive AUTOSAR. In addition, Qualcomm has a large number of hardware and software IP (including those developed for mobile platforms), Arriver is undoubtedly through software to enhance Qualcomm's hardware capabilities.

According to the plan, Qualcomm's mass production system with Veoneer's Arriver will be delivered in mass production in 2024, and the combination will cover the full range of solutions developed from L1 to L4 autonomous driving systems, while automakers and Tier 1 suppliers can expand and upgrade the solutions on the platform.

Qualcomm wants to expand its "business." For example, arriver's fifth-generation 8-megapixel visual perception software is scalable and will be available to automakers and Tier 1 suppliers as part of Qualcomm's future delivery computing platform.

According to the judgment of Qualcomm CEO Cristiano Amon, the revenue potential of each smart car equipped with a chip in the future will increase by more than ten times. On the one hand, Qualcomm hopes to gain a larger market share, and on the other hand, it is to increase the software revenue of the computing platform.

At the same time, after the acquisition of Arriver, Qualcomm's Snapdragon Ride will be able to compete head-on with NVIDIA's DRIVE platform, as well as Mobileye's SuperVision (for example, the domestic first mass production is Extreme Kr 001) and Mobileye Drive platform.

The competition for the comprehensive strength of chip manufacturers has begun.

A month ago, Qualcomm secured a production cooperation agreement from BMW, which said in a statement that Qualcomm's "breadth and depth of business portfolio, as well as expertise in computing, connectivity, vision and driver assistance technologies," was the main reason for the partnership.

A year ago, investment institutions were surprised to find that NVIDIA's business model had undergone significant changes. While semiconductor design remains the company's day-to-day core business, software revenue is also growing. In the long run, this means greater profit margins and more reliable revenue streams.

NVIDIA's DRIVE AGX Orin platform, for example, is designed in a manner similar to a modular software product. Upgrades, bug fixes, and new features can be added through OTA updates, and many features can be activated in subscription mode.

"NVIDIA is now a software company," Huang believes, "with a wealth of software and corresponding update services, will increase the company's sustainable business model to continue to generate software revenue." ”