【Editor's Note】 Metaverse, the English name Metavrese, which originated from the concept of "Avalanche" in science fiction primary schools, shines in 2021: from NVIDIA's Lao Huang to Facebook's Xiaoza, to the domestic Baidu, NetEase, Tencent, Internet giants have laid out places. The first year of the metacosm?

Through interviews with industry experts, practitioners and analysts, the surging news reporter analyzed the "past and present lives" of the meta-universe, and first explored the meta-universe industrial chain and investment opportunities that Xiao he only revealed.

2021 is being regarded by more and more people as the first year of the "meta-universe".

This year, the meta-universe concept of the speed of light has become popular, and the market has begun to dig deep: how should we understand this popular industry that is still in concept? What are the core businesses included in the so-called element universe industry chain? Who is the top company in these chains? Who is the most noteworthy core target?

The meta-universe industry chain has basically taken shape, focusing on the terminal side and the infrastructure side

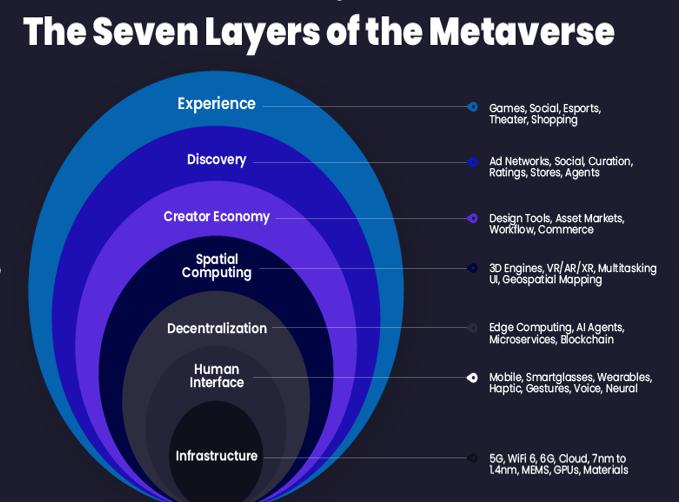

"At present, the meta-universe industrial chain has basically taken shape." Fang Guangzhao, an analyst at Open Source Securities, pointed out in the research report that the meta-universe industry chain can be divided into 7 levels or 4 major plates.

Specifically, Fang Guangzhao pointed out that the division of 7 levels, one is the experience layer, such as games, social networking, sports, movies, shopping, etc. The second is the discovery layer, such as advertising networks, social networks, curation, mutual evaluation, stores, agents, etc. The third is the creator economy, including design tools, asset markets, workflows, business trade, etc. The fourth is the spatial computing layer, including 3D engine, VR/AR/XR, multi-task interface, geospatial mapping, etc.

"The fifth is the decentralized layer, including edge computing, AI agents, microservices, blockchain, etc. The sixth is the human-computer interaction layer, including portable smart glasses, wearable devices, gesture interaction, voice-activated interaction, interactive neural network, etc. The seventh is the infrastructure layer, such as 5G, WIPI 6.6G, cloud computing, 7mm/11mm process, micro-electromechanical, graphics processing, basic materials, etc. Fang Guangzhao further pointed out.

If divided according to the four major sections, square light indication, can be divided into hardware, software, services, applications and content four aspects.

First of all, in terms of hardware content, it is to provide physical technology and facilities for developing, interacting with, or using meta-universe products. Such as network base stations, servers, VR glasses, etc.

In terms of software, it is to provide support and empowerment for hardware. Implement physical computing, rendering, data coordination, artificial intelligence and other functions.

The service sector is used to provide a platform that carries the user's online identity, distribute connected digital content, digital assets, and support corresponding digital financial services.

In terms of application and content, it refers to the provision of products in terminal application scenarios such as medical treatment, education, and games.

For the development path of the meta-universe, Ma Tianyi, chief analyst of Minsheng Securities Communications and Meta-universe, told the surging news reporter that there are four main aspects as a whole: First, the content side, mainly games. The second is the terminal side, such as the company that currently produces VR/AR equipment. The third is the platform side, such as Meta (Facebook), NVIDIA and other companies. The fourth is the infrastructure side, that is, the production providers of servers, switches, optical modules and other related servers, switches, optical modules and other related transportation and power supply.

"Among them, in the direction of investment logic, the current content side of the company, more is the development model of the traditional Internet, cultivating user activity, etc., so the possibility of short-term performance is relatively low." The opportunities on the terminal side and the infrastructure side are relatively certain. Ma Tianyi said.

However, Ma Tianyi reminded investors that in the past one or two years, due to the impact of the epidemic, the valuation of many cloud service-related companies has reached a historical high, so the valuation of these companies is currently in the digestion stage.

The VR/AR industry may be about to explode

In the meta-universe industry chain, the next development of the VR/AR industry has been optimistic about many industry experts.

Fang Guangzhao pointed out that although the development of the industry is tepid after the "first year of VR", VR/AR, as an important part of the metaverse, is expected to usher in an inflection point of rapid growth.

"In 2018, with the exposure of technical and content problems, the VR industry that once stood on the cusp of the wind once declined, and although it returned to the development track, the development of the entire industry has been tepid in recent years. The reason is mainly three aspects: First, the price factor, the high price is the main reason that hinders consumers from buying VR/AR equipment, and the price of VR headsets with good convenience is generally more than several thousand yuan. The second is the technical problem, the dizziness still exists. The third is the lack of content market, from the perspective of the entire VR market, virtual reality-related content products, especially phenomenal masterpieces, are very lacking. The lack of content makes VR lack sufficient appeal to users. Fang Guangzhao pointed out.

However, Fang Guangzhao stressed that with the application of content, high-quality VR products are constantly enriched, and the content ecology that can be self-sufficient and profitable has begun to take shape. In terms of network platforms, the popularity of 5G is expected to break the bottleneck of the niche of stand-alone VR. Superimposed manufacturers have accelerated the layout of the metaverse, in the technical side and the content side to promote the development of virtual reality, VR/AR, an important part of the metaverse, is expected to usher in a rapid growth inflection point.

CITIC Construction Investment Securities Research Report also believes that the VR/AR hardware industry chain is maturing day by day, the product experience has been greatly improved, and the industry is about to explode.

Among them, in terms of VR, CITIC Construction Investment Securities said that in the cost of VR hardware, processors, storage, and optical display devices account for more than 80%. Among them, the optical display device technology is mature, and the future will be developed to the next generation of short-throw optical solutions. Under the condition of fully meeting the needs of consumer use, the experience of related products has been significantly enhanced.

In terms of AR, CITIC Construction Investment Securities pointed out that optical display accounts for 40% of the hardware cost. Optical machine design is the technical difficulty of AR equipment that urgently needs to break through, the current industry mainly focuses on optical waveguide technology, although the development and mass production of high-performance optical waveguides still need a certain amount of time, but it is expected that apple and other manufacturers will drive the rapid growth of the industrial chain.

Ma Tianyi also pointed out that vr/AR is constantly evolving as a "bridge" linking reality and the online virtual world. For example, in the past, VR needed to link a high-performance computer to achieve good results, but now it is relatively separate.

"It can be seen that many VR/AR manufacturing companies, compared with the previous manufacturing business of mobile phones and car displays, the manufacturing technology difficulty of meta-universe terminals has been reduced, so the future terminal supporting equipment products will do better, and the next step should be performance." Ma Tianyi judged.

In terms of targets, CITIC Construction Investment Securities recommends that investors pay attention to high-quality companies in the VR/AR industry chain, such as Goertek (002241), Sunny Optical Technology (02382. HK), Crystal Optoelectronics (002273).

The metacosm brings long-term industrial logic to the game industry

In addition to VR/AR, the game industry is another investment line that is optimistic about many institutions.

CITIC Construction Investment Securities pointed out that the meta-universe is the long-term industrial logic of the media Internet industry in the future, and games are expected to become the first widely promoted applications in various pan-entertainment applications with their more comprehensive entertainment experience.

Specifically, CITIC Construction Investment Securities said that overseas manufacturers represented by Facebook have accelerated the layout of the metacosm. Among them, Facebook changed its name to "Meta" and fully shifted to the metacosm, with the goal of reaching 1 billion people and creating hundreds of billions of digital economies in the next decade. At the same time, Microsoft and NVIDIA are also working on the metacosm.

"On the domestic side, ByteDance previously acquired VR hardware Pico and launched the meta-universe game "Restart the World", while Tencent proposed a 'super digital scene' and invested in the meta-universe game Roblox." CITIC Construction Investment Securities further pointed out.

CITIC Construction Investment believes that a series of domestic and foreign manufacturers have significantly accelerated the layout of the meta-universe, and the game sector has ushered in a long-term new industrial logic.

In addition, CITIC Construction Investment pointed out that with the rapid growth of game overseas revenue, the industry space is still large. According to the data, in the first three quarters of this year, the revenue of domestic games going abroad was 4.064 billion US dollars, 4.404 billion US dollars and 4.966 billion US dollars, respectively, and the growth rate in the third quarter reached 28%.

Fang Guangzhao also pointed out that as the product form closest to the metaverse, especially MMORPG (massively multiplayer online role-playing game), it is in line with the stable economic system, strong virtual identity, strong sociality, and immersive experience of the metaverse.

"Under the trend of open world and UGC elements constantly merging with MMORPG, MMORPG may be the earliest to give birth to the prototype of the metaverse like sandbox games, and manufacturers who have accumulated leading development experience and underlying logic in the field of MMORPGs may take the lead in the exploration of metaverse games, such as Perfect World (002624)." Fang Guangzhao pointed out.

CITIC Construction Investment Securities recommends that investors pay attention to Tencent (00700. HK), 37 Interactive Entertainment (002555), Gigabit (603444), etc.