Source: Content compiled by Semiconductor Industry Watch (ID: icbank) from Eetimes, Author: Takashi Yukami, thank you.

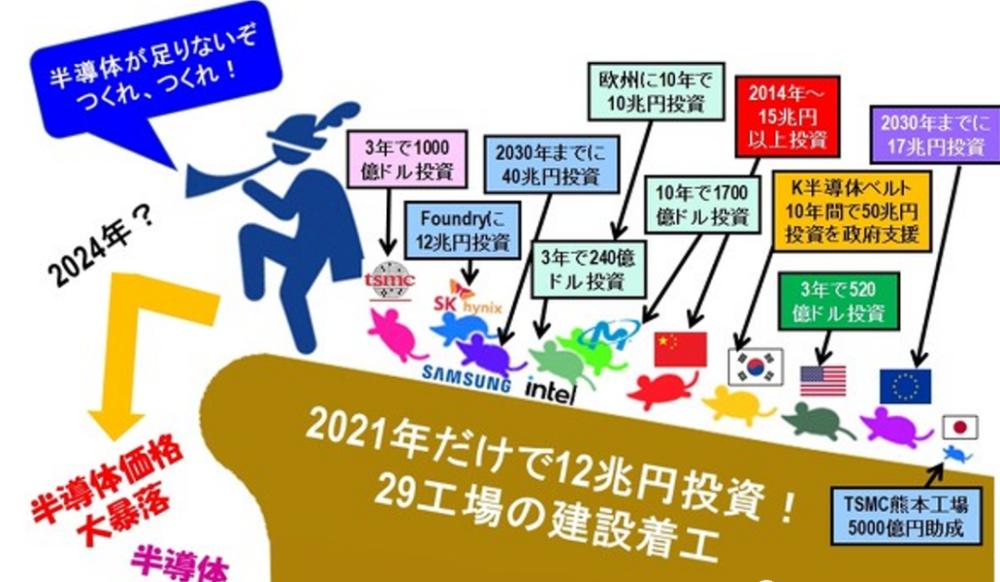

Seeing the crazy amount of equipment investment by semiconductor manufacturers in 2021 last year, as well as the extraordinary investment trend of subsidies in various countries and regions, the author feels a creepy fear. Last year alone, at least 12 trillion yen was invested and construction began on 29 factories.

The author can't help but think that if so many semiconductor factories are built, there will one day be an oversupply situation, which will eventually lead to a sharp price crash and a downturn in the semiconductor industry. Although the above 29 factories have not yet been put into production, shipments of various semiconductors, with the exception of Mos Memory, have set record highs.

It is worth noting that after 2020 ( that is, into the epidemic era ) , shipments of all kinds of semiconductors have increased in a different trend. If you add semiconductors from 29 factories that start construction in 2021, what will happen?

I am particularly concerned about Mos Memory's move. This is because the supply and demand balance of the DRAM contained in it can easily be broken, and there have been price plunges in the past, and its impact has spread to its own situation.

For example, in 1995, the price of DRAM soared in anticipation of Windows 95 sales, and the following year in 1996 plummeted. At that time, I was still working at Hitachi Manufacturing, and as a result, I was pushed from the Central Research Institute to the DRAM factory. In addition, the bubble economy of IT peaked in 2000 and burst in 2001. Hitachi Manufacturing advised all employees aged 40 and above to retire early, and the author, who had been seconded to ELPIDA memory and Selete (semiconductor advanced technology company), was forced to retire. And in 2008, when I was starting a wafer recycling company, there was a Lehman incident, the company I funded went bankrupt, the entrepreneurship was frustrated, and I fell into a situation of unemployment and no salary, and I had to work in a career guidance office.

When the memory bubble burst in 2018, the author was miraculously safe. However, the sluggishness in the memory industry bottomed out in 2019 and then increased shipments again with the same or greater trend as during the memory bubble period in 2016-2018. In the future, will there be another end to the peak of shipments and a sluggish memory market? At this thought, one feels an uneasiness that cannot be expressed in words.

But it is useless to be afraid. The author has conducted a thorough analysis of the data of the World Semiconductor Market Statistics (WSTS). The result is the conclusion that "the memory industry downturn will not come for the time being". Therefore, the results of this article will be described in this article. However, there are some worrying factors to this conclusion. One is whether the intel euv lithography (extreme ultraviolet) applicable process can hold, the other is whether the processor can ensure the use of a substrate, and then the other is where the impact of Russia's military aggression against Ukraine comes out. Especially the final suspense, I hope that the war will end as soon as possible.

Analysis of DRAM shipments and shipment quantities

As mentioned at the beginning, the supply and demand balance of DRAM in Mos Memory can easily be broken, causing price plunges many times in the past. As a result, the term "silicon cycle" has even appeared.

Let's take a look at the changes in DRAM shipments and shipment quantities from 1991 to 2021 (Figure 3). The shipment amount is affected by the price and fluctuates greatly up and down. Because of the change in shipments, the author's life has changed dramatically.

From the perspective of the number of shipments, it can be roughly divided into four periods.

1) 1991 to 2003: A period of slow shipment growth

This is mainly driven by the demand for PC and electrical products in developed countries in Japan, the United States and Europe.

2) 2003 to 2011: A period of sharp increase in shipments

In the 21st century, developing countries such as the BRIC countries (Brazil, Russia, India, and China) led by China have achieved rapid economic development. Because people in emerging countries buy mobile phones, PCs, and various electrical appliances, the absolute amount of DRAM carried by these products has also increased.

3) From 2011 to 2018, shipments remained at a period of about 15 billion units per year

DRAM manufacturers are gradually being phased out. In particular, after the bankruptcy of Erbida in 2012 and the acquisition of Micron Technology, the DRAM manufacturer essentially became Samsung Electronics, SK hynix and Micron. The three companies monopolized the DRAM market, and in order to prevent the price plunge caused by oversupply, tacit negotiations were held, and the companies made production adjustments. As a result, the number of speculative shipments was flat.

4) After 2018: A period when the number of DRAM shipments began to increase sharply again

The author believes that the reasons for this are as follows. The main battlefield of DRAM shifted from the PC to the mobile side, and gradually to the server side of the data center (Figure 4). As a result, three DRAM manufacturers competed again for supremacy over DrAM for Server. Moreover, due to the active investment in data centers, there is a need to increase the absolute amount of DRAM. It is speculated that these factors have led to a sharp increase in the number of shipments.

Memory requirements continue to expand

In addition, there is a popular word for people who are still alive, that is, "mix-and-match". At first I didn't quite understand what this meant, but it seemed to refer to a 3D virtual space built online. While I don't yet understand its structure, I understand that data centers are more important than ever. As a result, data centers require a large number of servers, and it is conceivable that the DRAM requirements used for this server will expand dramatically.

Moreover, this expansion of demand is not limited to DRAM, but also includes NAND flash memory and processors (MPUs). It will be quantified below.

NAND shipments and shipments

Figure 5 shows the change in shipments and shipments of NAND. If you pay attention to the number of shipments as dram, you can divide it into three periods.

1) 2000 to 2016: A period of straight-line shipment growth

As the NAND market expands to include music players "iPods", digital cameras, mobile phones, etc., the demand for NANDs has increased, and shipments have also increased.

2) 2016 to 2018: Shipments reached a fixed period of about 11 billion units per year

In 2016, the structure of NAND changed from two-dimensional to three-dimensional. In order to increase the storage capacity, the 3D NAND adopts the method of stacking storage units in longitudinal lengths. In two-dimensional technology, as the memory cells become thinner and the chip size becomes smaller, the number of chips available per wafer increases, resulting in an increase in shipments. However, in three-dimensional space, the chip size is basically unchanged. Therefore, although the number of shipments has increased, the number of shipments has not increased.

3) After 2018: Nand shipments began to increase again

This is due to the increasing volume of DRAM shipments over the same period. In other words, due to the expansion of data center demand, the demand for the server used has also increased sharply, so the demand for SSDs carried by the server has also increased, and the result is that the number of shipments of three-dimensional NANDs, the core components of the SSD, has begun to increase.

In summary, shipments of DRAM and NAND increased dramatically after 2018. This can be speculated to be due to the expanding demand for Servers in data centers. So, what is the shipment trend of server brain MPU?

MPU shipments and shipments

Figure 6 shows the amount of MPU shipped and the number of shipments. Judging by the number of shipments, it is not clear why there was a peak in 2011. However, the peak decline in 2016 was due to Intel's failure to advance the micro-process from 14nm to 10nm.

From 2016 to 2018, we ushered in the real era of big data, and cloud manufacturers such as Amazon, Microsoft, and Google began to build data centers. In that data center, it was necessary to line up the most advanced servers.

However, as mentioned earlier, Intel failed to mass-produce a 10nm MPU. The stagnation of 10nm technology lasted for 5 years, Intel was forced into a desperate situation, and the seventh CEO, Bob Swan, even mentioned that in 2020, "Intel may achieve Fabless".

Not long ago, Ibm-born Lisa Su became amd's CEO. The production commission for mpus was changed from GlobalFoundries to TSMC, and the most cutting-edge miniaturization process began to release high-performance MPUs (Humble report "Director of the Processor Market?"). Intel Catches Up with the Two Protagonists Who Made Amd Leap Forward" / May 15, 2020).

In order to improve the performance of the MPU, Intel, which had to compete with it, adopted the method of increasing the number of MPU cores while extending the 14nm process. However, the increase in the number of cores led to a decrease in the number of chips available to 1 wafer, which worsened the production speed.

Due to Intel's poor performance, shipments of MPUs in 2016 were 518 million units, which fell to 383 million units in 2019, 135 million fewer than in 2016, resulting in a global MPU shortage. As a result, DRAM and NAND for mass production of data center servers flooded the market, causing prices to plummet. In fact, the 8gbit product of the representative DRAM DDR4 fell from $8.2 to $2.8. In addition, the representative NAND MLC's 128gbit product fell from $5.6 to $3.9 (Figure 7).

That is to say, the memory depression in 2019, the root cause, can be said to be caused by Intel's lack of energy production of 10nm MPU (humble article "Memory Depression Caused by Intel 10nm Process Delay" / December 7, 2018). Will there be a similar memory slump in the future?

Will the memory industry be sluggish for the time being?

Figure 8 shows the change in the number of shipments of MPU, DRAM, and NAND. Shipments of MPUs fell to 383 million in 2019 and began to recover gradually. By 2021, it is only 19 million units away from the peak in 2016, and shipments will reach 499 million.

The reason for the increase in MPU shipments is twofold, one is that Intel's 10nm process has barely started, and the other is the increase in the number of AMD MPU shipments commissioned by TSMC. And, if MPUs continue to grow in the future, the memory market will not be sluggish (which we are desperate to do).

However, there are also worrying factors. As mentioned at the beginning, one is Intel's establishment of an EUV, one is a lack of packaging substrates, and the other is war.

Can Intel be proficient in USINGEVs?

Intel's eighth CEO, Pat Gelsinger, unveiled a new roadmap in January 2021 (related report: "Intel will change the name of the process to get rid of the "nm" process" / August 3, 2021). We have written a comparison of the year when mass production began with TSMC's technical nodes into this roadmap (Figure 9).

Intel will mass-produce the "Intel7" in 2021 and will be available this year through 2022. This is the same generation as the 10nm that failed mass production in 2016 (although the structure, materials, and process have changed), and it is the same as TSMC's N7 (ArF liquid dip). Moreover, with the start of mass production, the supply of MPUs in the world will also increase. However, the conundrum ahead is piling up.

First of all, compared with Intel and TSMC, "Intel4" is equivalent to 5nm of TSMC, "Intel3" is equivalent to 3nm of TSMC, and "Intel20a" is equivalent to 2nm of TSMC. Assuming this comparison is correct, Intel must mass-produce the "Intel4" of about 15 layers of EUV in the second half of 2022.

However, Intel only has about 3 EIVs, and it is speculated that it is not the mass production machine NXE3400, but the research and development machine NEX3300. In this case, in the second half of 2022, TSMC's 5nm "Intel4" will be difficult to rise. As a result, the foothold of "Intel3" in the second half of 2023 and "Intel20a" in 2024 seems hopeless.

If Intel is not proficient in using EUV, "Intel4" and "Intel3" can not be mass-produced, it may cause MPU shortages. In order to avoid the shortage of MPU, Intel fully entrusted the "Intel4" and "Intel3" to TSMC production, and AMD hoped that TSMC would produce MPU sufficient to fill Intel's vacancy.

What exactly will Intel do (can it not stubbornly rely on TSMC?).

The Server is running out of footprints

Another worrying material is that even if Intel and AMD are able to produce MPUs by commissioning TSMC production, etc., the MPU-equipped FCBGA (Flip Chip-Ball Grid Array) substrate is insufficient.

The FCBGA substrate is exclusively owned by Japan's IIDDEN and Shin Kong Electric. (Co-authored article "Semiconductor Manufacturing Equipment and Materials, Why Is Japan's Market Share So High? ~ Competitiveness Generated by the "Japanese Unique Temperament"," December 14, 2021).) However, due to the high demand for servers around the world, the problem of insufficient FCBGA substrates has become significant (Figure 10).

According to the co-author of the aforementioned report, Former Intel's Mr. Tadaoji Kamewada, the shortage of FCBGA substrates is expected to continue into 2024. If the substrate shortage continues, it may become a bottleneck causing the server to run out of MPU. This is a problem that Intel and AMD cannot solve, and can only be solved by the efforts of IBIDEN and Shin Kong Electric.

I hope the war will end soon

The problem with IntelEUV and the shortage of FCBGA substrates are the problems of technology and production capacity in ordinary times (whether it can be called "usual" due to the impact of the epidemic).

However, Russia's military offensive against Ukraine is clearly an "extraordinary period". On March 10, 2022, Prime Minister Kishida of Japan said: "As events unfold, the world and Japan will be plunged into the biggest crisis after the war." (Nikkei Shimbun, March 10). However, this statement is used in the context of "high energy prices (in Japan)". I can't help but think, "Does this still need to be said?"

Taking the semiconductor industry as an example, in this "extraordinary period", it is difficult to predict where, what supply chains will break, and what kind of impact will occur in what fields. In semiconductor manufacturing, first-tier suppliers, second-tier suppliers, third-tier suppliers, etc., a very complex supply network is formed in the world, so any arrears of raw materials may lead to the complete inability to manufacture semiconductor chips. That said, this war is likely to lead to a Great Depression in the semiconductor industry. Note)

Note) According to the "Impact of Russia's Invasion of Ukraine on the Semiconductor Market", Ukraine is the main supplier of rare gases such as neon, argon, krypton and xenon, as well as semiconductor raw gases such as C4F6. First, the stagnation of the supply of noble gases will affect the production of KrF and ArF exposure devices and the maintenance of light sources. In addition, argon, xenon, and C4F6 are important gases used for insulation film etching, and if their supply stagnates, all semiconductors cannot be manufactured. If the war is prolonged, or if the gas plants cannot function even if the war is over, it will have a huge impact on the world semiconductor industry. Hope it doesn't turn out that way.

Finally, I will end with the author's wishes.

1. I hope that the war will end as soon as possible

2. Hope that there will be no memory depression caused by insufficient MPU (or war).