Image source @ Visual China

Text | Market Capitalization Watch, author | Blue Danube, edited | Little City Sister

Robot penetration rate is an important criterion for measuring the level of industrial intelligence in a country, due to factors such as late start, China's robot market, especially the level of development of industrial robots is far behind the major developed countries, for which the country attaches great importance to and is committed to breaking through the technical bottleneck.

At this stage, what are the breakthrough opportunities in China's robot market?

Unbalanced development

When it comes to "robots", the public is most likely to think of various "humanoid robots", such as Pepper, who interacted with Son Zhengyi at the press conference in 2014, which is a robot that installs an "emotion engine" to recognize human emotions.

Later, a variety of humanoid robots appeared frequently, including last year's eye-catching "Waker X", a humanoid robot developed by the domestic manufacturer UBTECH, which can run on a treadmill, unscrew the lid of the thermos cup, give people a massage, and even sit down to play against people.

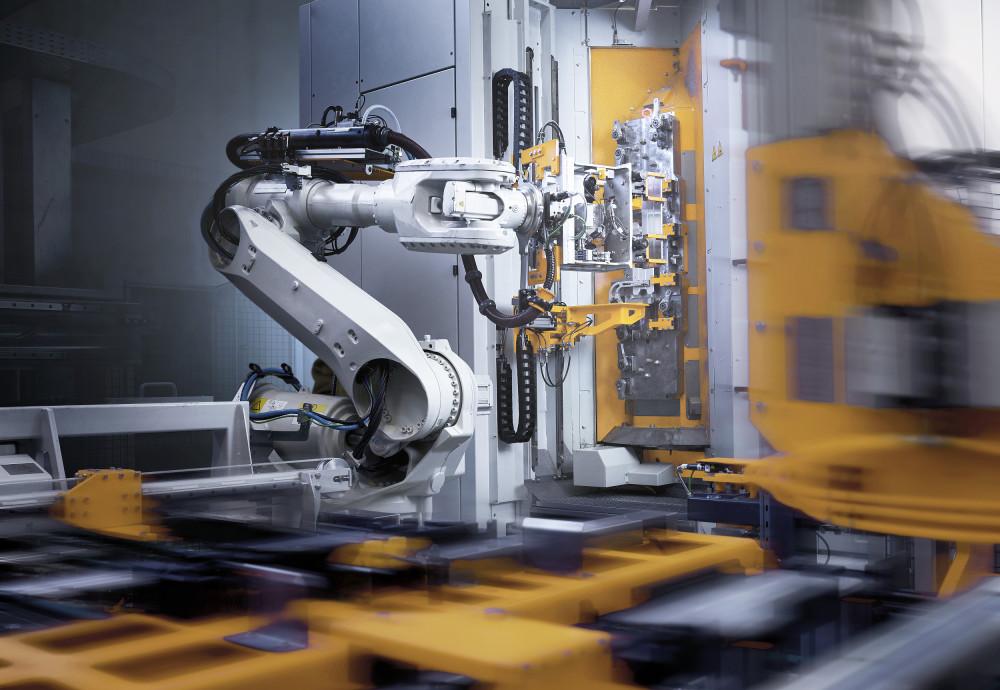

In fact, humanoid robots are only the tip of the iceberg of the huge robot industry, and those non-humanoid robots are the main body of the market, which are distributed in automotive smart factories, 3C electronic product precision processing production lines, and food and beverage packaging lines.

According to IFR (International Federation of Robotics) statistics, in 2021, China's robot market size is expected to reach 83.9 billion yuan, the average growth rate of 2016-2023 reached 18.3%, of which industrial robots 44.57 billion yuan, service robots 30.26 billion yuan, special robots 9.07 billion yuan.

▲China's robot market structure in 2021

Industrial robots are the robots with the highest market share in China, which are widely used in the assembly, handling, palletizing, welding and other aspects of automobiles and 3C electronics, and expand to metal processing, photovoltaics, lithium batteries, food and beverage industries.

In addition, China is also the world's largest industrial robot application market, accounting for nearly 30%.

However, a terrible reality is that more than 70% of the newly installed industrial robots in China come from foreign suppliers, and the self-sufficiency rate is amazingly low.

In 2020, the density of manufacturing robots in China is 246 units / 10,000 people, far less than the 932 units / 10,000 people in South Korea, the 390 units / 10,000 people in Japan, and the 371 units / 10,000 people in Germany.

This reality means that we are only an industrial power, and we are still far from being a real industrial power.

In this regard, the fifteenth department on the issuance of the "14th Five-Year" robot industry development plan notice (hereinafter referred to as the 14th Five-Year Plan) clearly mentioned: we must seize the opportunity, face the challenge, accelerate the solution of insufficient technology accumulation, weak industrial base, lack of high-end supply and other issues, and promote the robot industry to move towards the middle and high-end.

However, unlike industrial robots facing a serious card neck situation, China's service robots have little gap with foreign companies in terms of technology and industrialization level, and even some product market-oriented applications have been ahead of the world and have a first-mover advantage.

Judging from the financing distribution results of the primary market in the field of robotics in 2021, service robots are far ahead, special robots such as medical robots are relatively secondary, industrial robots are lagging behind, and the increase in the primary market for robots focuses on the advantages of no baggage.

The gap is huge

Although it is the world's largest robot consumer market, the supply side is highly dependent on imports, which has become an urgent problem to be solved in China's industrial automation.

From the perspective of the industrial chain link, where is the specific backwardness of China's industrial robots?

An industrial robot is separated, and its components include three parts: upstream core components, midstream robot body, and downstream system integration.

Among them, the upstream core components not only account for up to 70% of the cost, but also have the greatest technical difficulty; the technical difficulty of the midstream robot body follows the upstream core components, accounting for about 20%; the downstream system integration technology is less difficult, mainly depending on the landing scenario.

The technical difficulty of the industrial chain determines that the core components are the commanding heights for industrial robots to win.

However, unfortunately, at present, the domestic robot companies in the three core components of industrial robots, including "controller", "servo system" and "reducer", are not highly vocal.

The first is the controller, which is known as the robot brain device, mainly composed of software and hardware, hardware including fuselage, operation interface, etc., the gap between domestic and foreign is not large; but in terms of software, foreign capital in software algorithms, reaction speed, compatibility and other aspects of the performance is obviously better than domestic.

As a result, the four major families of robots, including Fanuc, KUKA, ABB, and Yaskawa Electric, occupy 53% of the share of China's controllers, plus other second-tier foreign investment, the total proportion of foreign capital in this field is more than 80%, while domestic manufacturers account for about 16% in the controller field.

▲The domestic controller market pattern in 2019

The second is the servo system, as the cerebellum of the industrial robot, the servo system drives the robot body to accurately execute by receiving the motion instructions issued by the controller.

Servo system is mainly composed of servo drive, servo motor two parts, the current AC servo drive design is generally used based on vector control of current, speed, position three closed-loop control algorithm, the design of closed-loop system, debugging requirements are very high, which is also the core difficulty in the servo system.

This difficulty also determines the advantage of foreign investment with a long history of research and development. According to statistics, in 2019, in the field of domestic servo systems, foreign-funded enterprises such as Panasonic, Yaskawa and Europe's Siemens and Schneider accounted for more than 52%, and domestic enterprises accounted for only about 26%, ranking high in Huichuan Technology (10.7%) and Leisai Intelligence (2.3%).

At present, the domestic servo system and the international advanced level are roughly the same in terms of power output power, there is no obvious gap, the gap is mainly reflected in the response speed, size and stability, etc., and the breakthrough of technology continues.

Finally, there is the reducer, which acts as a partner to the servo system, which is equivalent to a brake installed between the servo motor and the actuator.

The core difficulty of the reducer lies mainly in precision machining, tooth surface heat treatment, assembly accuracy, large-scale production and testing and other process links, which is precisely the weakest part of China's manufacturing basic supporting system, which requires long-term experience accumulation.

At present, the accelerators on the market include RV reducers and harmonic reducers, two mainstream reducers and Spinea special reducers, accounting for 4:4:2 respectively. Among them, the RV reducer and the harmonic reducer are complementary in application, the former is mainly used in robot joints above 20KG, and the latter is within 20KG robot joints.

At present, the domestic reducer is mainly concentrated in the field of harmonic reducer, while the sound volume of RV reducer is insufficient. In terms of market share, at present, the RV reducer and the field of harmonic reducer are monopolized by Nabotsk and Hamonak respectively. Foreign capital accounts for more than 70%, and the share of domestic reducers accounts for less than 30%.

In general, among the three core components of the robot, the proportion of the reducer and the servo system domestically has relatively improved, and the controller is lagging behind. In this context, the opportunity for the localization of robots not only requires breakthroughs in hard-core technology in the neck of foreign cards, but also other ways in other advantageous areas.

Three major breakout directions

Although the gap between domestic robot companies and foreign investment is huge, it cannot stop us from struggling to catch up.

Recently, the 14th Five-Year Plan put forward two goals for the development of robots: by 2025, China will become the source of global robot technology innovation, a high-end manufacturing agglomeration and a new highland for integrated applications; by 2035, the comprehensive strength of China's robot industry will reach the international leading level.

Based on the current industry pattern and development trend, we sort out the following three breakthrough directions. The first is the research of core technology, the second is the layout of high-growth segments, and the third is to expand the big cake of service robots.

The first is the research of core technology.

In terms of the three core components of the card neck, in addition to the controller, there are signs of domestic manufacturers catching up in the field of servo systems and reducers.

Among them, in the field of servo system, the domestic manufacturer Eston servo drive products and Yaskawa Motor "Σ series" products have no tuning function, the maximum speed is basically the same, the company is also one of the few domestic enterprises with the whole industry chain of robots.

Some of the servo technology of Leisai Intelligent has reached the world-class level, and has established long-term cooperative relations with BYD, Han's Laser, Luxshare Precision and other enterprises. In 2020, the company took advantage of the high demand for photovoltaic, lithium battery, logistics, epidemic prevention and other industries, and the servo system business increased by 22.6%, recording revenue of 166 million yuan, which was the second largest business of the company.

Huichuan technology servo system in China's market share in the top five, ranking first in the domestic brand. In the first half of 2021, the company relied on supply chain supply, chip inventory strategy, and seized the opportunity of foreign capital lack of cores, significantly seized market share, general servo business revenue increased by 133%, and the market share increased from 10% in the same period last year to 15.4%, continuing to lead the domestic servo market.

In the field of reducers, green harmonics have obvious advantages in the field of harmonic reducers, with a share of about 60% in domestic robot brands, providing services for Eston, Eft, GSK, Siasun and other enterprises.

In addition, the company's business focus, harmonic reducer and metal parts business revenue accounted for about 95%, by the epidemic catalyzed "machine substitution" demand, the company's revenue growth rate in the first three quarters of last year exceeded 115%, some brokers expect that only the domestic CNC machine tool field, 2021-2025 harmonic reducer market size annual compound growth rate of 45%, the ceiling is high.

Secondly, the segmentation of high growth mainly includes two parts:

First, some robots with relatively low technical barriers, such as AGV robots, because the core technology threshold of AGV robots is not high, and there is no obvious gap between domestic and foreign technical water products, so domestic AGV robots have become the mainstream of the domestic market.

However, the market segment is growing rapidly, and the data shows that the average annual compound growth rate of the market in 2015-2019 reached 57.7%, and in the future, with the increase in e-commerce penetration and the development of smart logistics, such robots are expected to continue to maintain a high growth rate.

Second, some long-tail markets with faster growth rates. The focus of industrial robots has always been the automotive and 3C electronics fields, but in recent years, these two markets have gradually saturated, and the growth rate has slowed down seriously. Segments including food and beverage, photovoltaics and lithium batteries ushered in high growth.

In 2019, in the downstream industry application of industrial robots in China, the proportion of food and beverage, photovoltaic and lithium batteries increased by 127%, 55% and 24% respectively year-on-year, and the cumulative installed capacity of photovoltaic power generation in China still ranks first in the world for 6 consecutive years, and the penetration rate of new energy vehicles is about 7%, which is still far from the target of 20% in 2025.

Betting on these high-growth subdivision application scenarios will give domestic industrial robot manufacturers some shortcuts to break through.

In the end, the service robot will be the big cake that flips the plate.

According to IFR forecasts, by 2023, the domestic service robot market size will exceed 60 billion yuan, surpassing industrial robots to become the largest robot market.

Different from the passive situation of industrial robots being suppressed by foreign capital, service robots are completely lightly loaded, and at present, domestic service robots are not only not inferior to foreign brands in terms of technology and industrialization level, but even some product market-oriented applications have led the world.

The application of domestic service robots in the fields of cleaning, catering, hotels, medical treatment, delivery and other fields tends to mature, but in addition to the cleaning robot field with Coworth, Stone Technology and other listings, the rest of the service robot companies are in the primary market.

It should be known that at present, the market value (120 billion US dollars) of the medical service robot intuitive surgery (the parent company of da Vinci surgical system) is almost more than the sum of the four major families of industrial robots, from the investment point of view, we must pay attention to the IPO opportunities of service robot companies.

For the breakthrough of robots, domestic brands must not only dare to charge forward and face difficulties, but also focus on service robots in some high-growth areas, and combine the two aspects to improve the level of intelligence and create an industrialized power.