Cell Device Market Space Forecast

According to Trina Solar, global PERC cell production capacity will be around 120GW in 2020. According to our estimates, the global TOPCon capacity is approximately 3.7GW and the HJT capacity is approximately 2GW. From a cost perspective, TOPCon batteries have an advantage over PERC batteries in 2021, but the biggest reason for limiting their market share is capacity. Although the TOPCon battery production line can be upgraded by the PERC production line, the capacity formed before 2020 is basically only compatible with 166mm wafers, and the capacity potential of upgrading from the existing PERC production line is limited. Large silicon wafers of 182mm and 210mm will account for the main market share in the future.

The comprehensive cost of heterojunction batteries is currently about 25% higher than that of PERC batteries, and most of the existing production line capacity is below 500MW, mainly for trial production. Until the cost of heterojunction batteries does not form an advantage, companies are cautious about large-scale investment in heterojunction capacity. Different from the market view, we believe that even if heterojunction batteries form a cost advantage for PERC batteries in 2023, PERC batteries will still occupy a large market share due to capacity reasons.

The main assumption is one: 2021-2023, the market share of PERC batteries is 86%, 80%, 70%, the market share of TOPCon batteries is 6%, 12%, and 18%, and the market share of heterojunction batteries is 3%, 7%, and 11%.

The main assumption is two: TOPCon battery in the early stage of market introduction, capacity utilization rate will not be higher, there are two reasons: one is that the new production capacity will experience a capacity climbing period, and the other is that the company will carry out large-scale capacity construction in the early stage in order to strive for the market. Therefore, we predict that from 2021 to 2023, the capacity utilization rate of TOPCon will be 70%, 70%, and 80%, respectively. According to our estimates, from 2021 to 2023, the perc equipment market size was 6.151, 42.97 and 3.158 billion yuan, the TOPCon equipment market share was 2.578, 51.43 and 5.491 billion yuan, and the heterojunction equipment market share was 21.31, 69.20 and 9.000 billion yuan, respectively, and the total market size of the three was 10.891, 163.60 and 17.649 billion yuan.

Major manufacturers of cell equipment

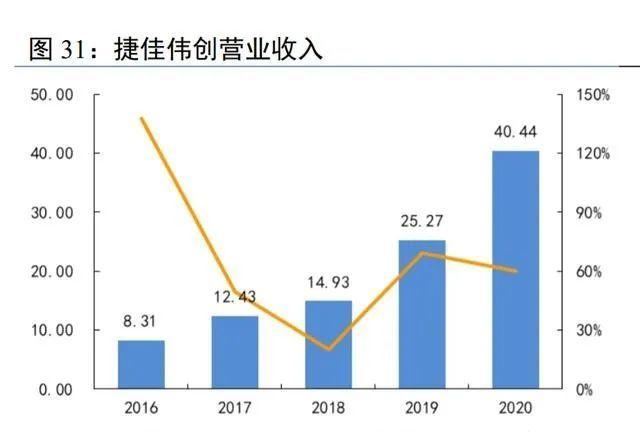

(1) Jiejia Weichuang (300724. SZ)

Doped deposition equipment faucet, multi-technical route comprehensive layout of the whole line equipment supplier. The company has the capability to provide turnkey engineering solutions for production lines of PERC, TOPCon and heterojunction batteries. At present, the largest proportion of the company's revenue is the diffusion annealing furnace and PECVD equipment in the diffusion and deposition process of monocrystalline silicon cell preparation.

According to the prospectus, the technical parameters of the company's PECVD equipment are the first in the industry. In the incremental phase of TOPCon batteries, the company realized the reserve of two technical routes: (1) LPCVD oxidation and deposition of polysilicon and doping in situ. The technology has now been tested. (2) PECVD deposition passivation film. In terms of the technical reserve of heterojunction batteries, Jiejia Weichuang is the world's first pool solution equipment provider to complete the full line of four processes completely independent development. In the amorphous silicon film deposition link, the company has developed a plate type PECVD equipment with the accumulation of PECVD equipment, and the coating uniformity reaches less than 5%, leading the industry level.

In the TCO membrane deposition process, the company was authorized by Sumitomo Of japan to develop RPD equipment. Due to the advantages of the design principle, heterojunction batteries using Jacques Victron RPD devices have higher conversion efficiency and electrical performance. According to the company, the company is conducting the research and development of CAT-CVD technology on the deposition of the most critical amorphous silicon film of heterojunction. On May 30, 2020, Jiejia Weichuang and iKang Technology officially signed a strategic cooperation framework agreement for iKang Changxing 2GW heterojunction battery project, mainly in the research and development of key process equipment technology and the procurement of a full line of battery equipment.

(2) Maiwei shares (300751)

Screen printing equipment faucet, heterojunction battery complete line equipment supplier. In the early years, China's photovoltaic cell screen printing equipment was monopolized by foreign manufacturers led by Baccini. Through technology, Maiwei Co., Ltd. has successively developed and produced single-ended single-track and double-ended shuanggui screen printing equipment, breaking the monopoly of foreign manufacturers. In 2019, the company began to develop heterojunction battery equipment and chose the technical route of PECVD+PVD. At present, the company has the ability to supply heterojunction battery equipment, and the core links of PECVD and PVD equipment have achieved mass production capabilities. In 2020, the company won the bid for the whole line of equipment and two PVD devices of Anhui Huasheng 500MW heterojunction battery. On March 18, 2021, Anhui Huasheng's 500MW heterojunction project was officially tape-out, and the average conversion efficiency of the first week of trial production of cells reached 23.8%. On June 8, 2021, Anhui Huasheng announced that the average efficiency of the production line's mass production batch reached 24.71%, and the maximum efficiency of single pieces reached 25.06%.

(3) Junshi Energy

Full-line equipment provider focused on heterojunction batteries. Founded in 2005, the company currently focuses on the research and development and production of a new generation of heterojunction battery equipment. According to the information on the official website, the company currently has the ability to supply heterojunction battery equipment. The technical route chosen by Junshi is PECVD+PVD equipment. PECVD, PVD, printing press, etc. are compatible with 166mm, 182mm, 210mm size silicon wafers. At present, the company's launch of PECVD and PVD have two models, corresponding to 350MW/year and 500MW/year production capacity, with a yield rate of more than 99.8%. At present, the company has made important technological breakthroughs in electrode printing equipment, and the sputtering coating method developed by Junshi Energy combined with the screen design and new slurry can reduce the consumption of single piece silver paste of G1 size heterojunction batteries from 150mg to 80mg.

(4) Ideal Wanlihui

The first echelon of domestic PECVD equipment has been verified by multiple production lines. Ideal Wanlihui was originally the PECVD business department of Ideal Energy. In October 2017, ideal Wanlihui's first SHJ was shipped with mass production PECVD products, breaking the monopoly of foreign suppliers. The company's PECVD equipment has been tested in Chengdu Tongwei heterojunction project and Anhui Huasheng heterojunction project.

Source: Future Think Tank