There are many netizens complaining, why can't our pension calculation be simple? Is it not well calculated according to the model of receiving a pension of 100 yuan per year of working age?

In fact, our pension is a social insurance system, which is jointly raised by the society to provide pension treatment for the retired elderly. The cost of the elderly for the elderly needs to be consistent with the level of social consumption.

People's incomes are high and low, and we also want to adjust the gap in social income distribution through the pension insurance system.

Under the social market economy system, people must also be given incentives to participate in insurance contributions, so as to effectively reduce the cost of social insurance premium collection.

Therefore, the basic principle of pension insurance determined by the state is to pay more and get more, and pay more for a long time.

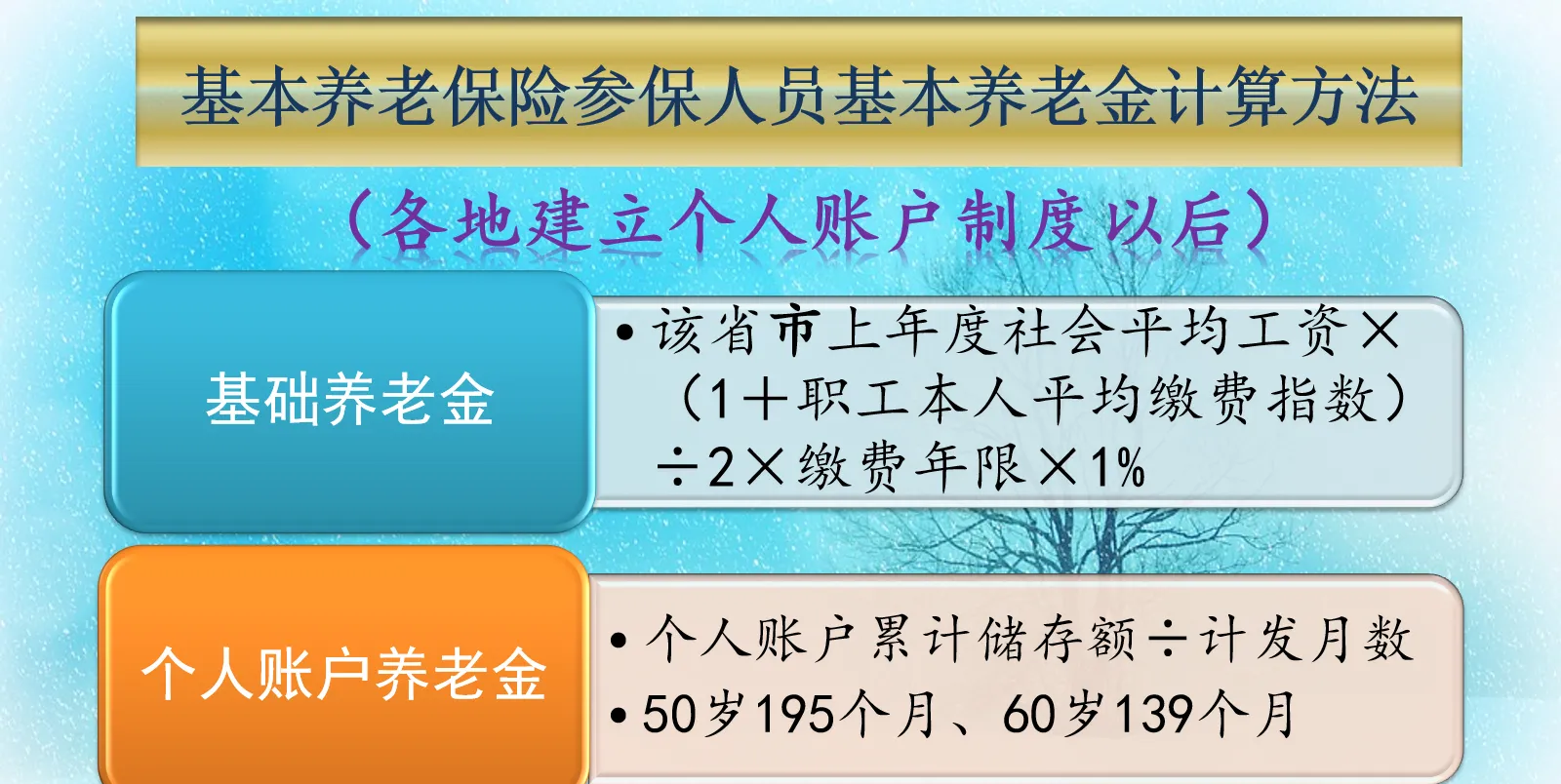

Our current pension calculation formula is actually formulated in 2005 by the "Decision on Improving the Basic Pension Insurance System for Urban Workers", which mainly includes the two parts of basic pension and personal account pension.

First, the basic pension calculation formula is equal to the average social wage × (1 + the average contribution index of the employee) in the previous year of retirement÷ 2× the payment period ×1%.

According to the calculation formula, it can be seen that the basic pension is related to three factors, the average social salary of the previous year of retirement, the average contribution index of the employee, and the number of years of payment.

The average salary of the previous year of retirement, which is now generally referred to as the pension calculation base of the current year, has been uniformly announced by the Ministry of Social Security. This wage ensures that the pension treatment level of the retired elderly can be connected with the wage level of the active workers, and there will be no relative depreciation of income. This is particularly applicable to our basic national conditions of rapid development of wage income in the past few decades.

The number of years of payment, in fact, includes the same number of years of payment and the actual years of payment, which actually reflects a factor of the length of time that the insured employees contribute to China's pension insurance system. This is also a factor that most elderly people can know, that is, working age. However, if the pension insurance contribution is not realized, it is useless to work only.

The average payment index of the employees themselves is mainly the level of the employees' payment. If employees always contribute according to the 60% base, the average contribution index of pension is 0.6. It can generally be expressed as the average of the monthly payment base ÷ the average monthly wage proportion of employees in the previous year.

In fact, there is a hidden factor in calculating formulas. If the average contribution index is 0.6, no contribution, the one-year basic pension receives 0.8% of the retirement average social wage of the previous year. The average contribution index is 1, and 1% is received; the average payment index is 3, and 2% is received.

In other words, the basic pension has the function of narrowing the income gap, and the low-income population benefits. However, for high-income people, it cannot be said that it is a loss, after all, compared with the low society in the past, the average wage is still very cost-effective at 2% of the social average wage.

Second, the personal account pension, which is equal to the balance of the personal account at the time of retirement by the number of months of calculation determined by the retirement age.

The number of months to be calculated for the retirement age was determined in 2005 on the basis of factors such as the average urban life expectancy in 2000 and the rate of return of about 4%. Now that the personal account system has actually been revised a lot, it should be improved. According to the 14th Five-Year Plan, it will be revised and improved within 5 years.

In general, the earlier the retirement age and the greater the number of months to be counted, the lower the calculated personal account pension. But after all, retirement is early, pension early, it is still very cost-effective.

The balance of the individual account of the pension insurance actually reflects the part of the accumulation of individuals participating in the pension insurance. If this part of the treatment is not completed, it can be inherited by the heirs. That's why it's called a personal account.

Monthly payments are now credited to the individual account at 8% of the payment base. The bookkeeping interest rate is not based on the yield of bank deposits, but the Ministry of Human Resources and Social Security uniformly announced that it is 6.04% in 2020. It has been above 6% to 8% in the past few years, and it is still very cost-effective.

In summary, our pension calculation formula actually takes into account many, many factors, and it really can't be too simple.

However, there is one thing that is not taken into account in the pension calculation formula, that is, the factor of loss. Individuals who participate in endowment insurance are basically difficult to lose money. Some elderly people only pay a few tens of thousands of yuan of pension insurance, and now the pension received before and after has exceeded hundreds of thousands. I believe that in the end, the country will have a solution.