The chip war of smart cars has started?

Author | Home scale from the planet Magnesia

52.4 billion.

This is the global shipment of automotive chips in 2021, an increase of 30% year-on-year compared with 2020, far faster than other chips of the same type.

In the face of this huge market cake, all kinds of haoxiong have also come out, including many consumer electronics chip giants with strong technical strength, there are also OEMs that are plagued by lack of cores, and even terminal car manufacturers as the last link of the industrial chain have not been able to withstand the temptation.

Core "New Force"

If you use the noun analogy in the field of smart cars, then consumer electronics giants such as Intel, Qualcomm, Nvidia, and Huawei are undoubtedly the "new forces" of automotive chips.

They have their own technical advantages, and after the crossover car, they are "hanging" a number of traditional Tier 1s. In fact, these new forces do not play the role of "challengers" - they have targeted high-performance computing chips from the beginning, this choice is based on the computing power requirements brought by the "new four modernizations" of automobiles, similar to automatic driving, intelligent cockpits need the support of high-performance computing platforms, which is the advantage that the traditional Tier 1 does not have.

In the case of almost "monopoly", chip giants began to develop autonomous driving chips at their own pace, which can be summarized in two aspects: spelling power and spelling technology.

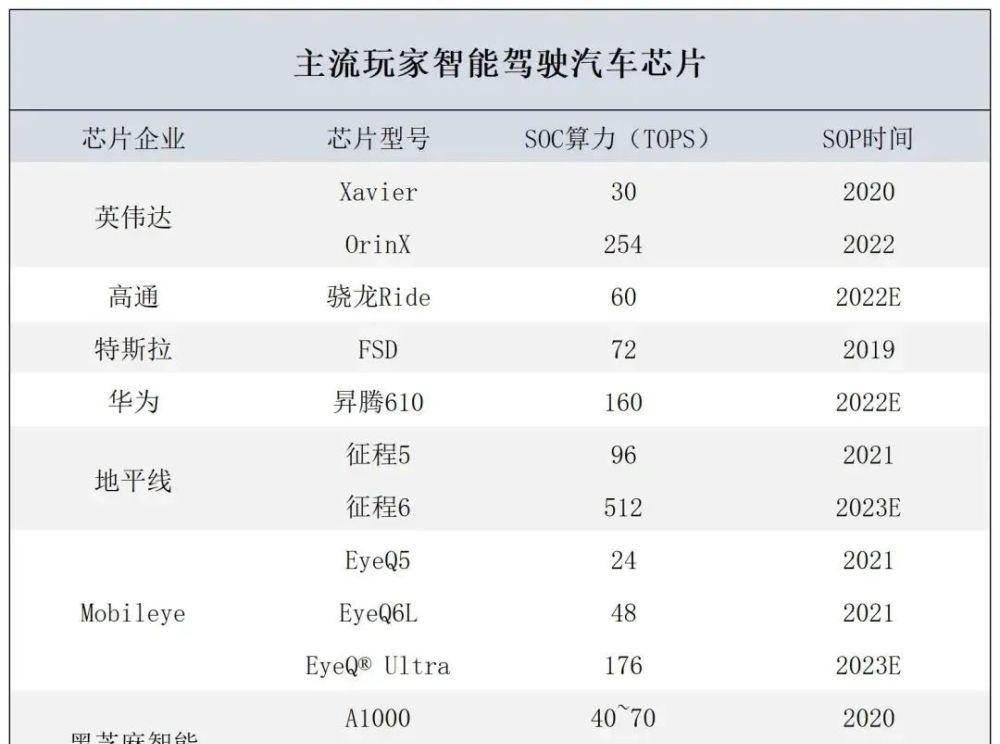

At this year's GTC conference, NVIDIA presented a list of vendor customers of the DRIVE Orin platform, which includes almost all mainstream car companies. The reason why these customers choose the DRIVE Orin platform is also very simple: the Orin chip with a computing power of up to 254TOPS has no opponent. In contrast, mobileye and Qualcomm's mainstream autonomous driving chips have less than 100 TOPS, of course, for the current mainstream L2 level autonomous driving, 100TOPS chips are also completely sufficient.

In terms of advanced technology, Qualcomm has brought advanced processes such as 7nm and 5nm to the automotive industry. The focus of this round of chip shortage tide MCU is still faltering, staying at the mature process stage of 28nm. Advanced processes deliver excellent performance, power consumption, and lucrative profits. In the context of the decline of consumer electronics such as mobile phones, automotive chips will become a new growth point for these manufacturers.

In addition, with the intelligent upgrading of domestic car companies, the huge demand for autonomous driving chips has provided new opportunities for domestic chip manufacturers. Taking Nvidia as an example, although the DRIVE Orin platform is good enough, the shortcomings of the solution are also very obvious: the cost is too high, and the current models equipped with the Orin platform are basically more than 400,000 yuan. Domestic chip manufacturers have attracted the attention of many OEMs with cost-effective large computing power products.

At present, there are intelligent driving products developed by Huawei, Horizon, Black Sesame Intelligence, Xinchi Technology, etc. in China, among which the first local chip company Horizon has occupied the first-mover advantage, and has won a number of OEMs such as SAIC, BYD, and Nezha.

The Tier 1 giant seeks transformation

As mentioned earlier, due to the shortcomings in algorithm capabilities, the international giants such as Bosch, Continental, Delphi, ZF and other international giants such as Bosch, Continental, Delphi, and ZF in the era of traditional fuel vehicles are significantly slower than the chip giants in the progress of intelligence.

In L1/L2-level low-level ADAS, Mobileye single-handedly occupies more than 70% of the entire market share, and the Tier 1 giants' own algorithms can only compete for less than 30% of the remaining. In the L2+ autonomous driving level, the Tier 1 giants are even more helpless, basically abandoning the plan of self-developed algorithms, and mostly choose to cooperate with mature algorithm companies.

Fortunately, the Tier 1 giants also hold the right to speak of vehicle chips such as MCUs, which are in high demand but have low profit margins and high technical requirements.

In fact, the Tier 1 giants and the chip giants have the same approach: lower their posture to join the industrial chain cooperation of car companies, no longer hand over ready-made products to car companies as in the past, but jointly develop autonomous driving software and hardware.

Of course, under the big changes of the transformation of the international giant Tier 1, domestic MCU companies have also ushered in opportunities for development, but not compared with the aforementioned automatic driving chips, OEMs are still biased towards Tier1 suppliers, and domestic MCUs are currently mainly used in the low-end market.

No chips, make your own?

Since the veteran Tier 1 can change the way of life, it is not surprising that the OEMs choose to make the core themselves. The representative companies are Tesla and BYD.

Tesla's plan for self-developed chips began in 2014, and in 2015, a chip self-research team was secretly formed. At that time, Tesla's first generation of Autopilot used Mobileye's chip, and then the second generation was changed to NVIDIA. Until April 2019, Tesla's self-developed FSD chip was officially installed on the mass production car. In terms of AI, Tesla is also unambiguous, the D1 chip released in August last year, the computing power is as high as 362TOPS, in contrast, Nvidia's Orin chip is also willing to bow to the wind.

Seeing that Tesla has used self-developed chips, the new domestic car-making forces have also acted quickly, and zero-run cars have also said that "car companies that do not make chips are not a good technology company", of course, zero-run cars really use the self-developed "Lingxin 01" intelligent driving chip on the zero-run C11 performance version. Although the hash rate is only 4.2 TOPS, it is also a good start for the new forces.

Compared with the new car-making forces, BYD, which has laid out the semiconductor field for more than fifteen years in advance, is more pragmatic. Since the establishment of BYD Semiconductor in 2004, BYD has first broken the monopoly of foreign IGBT chips, and at the same time, the first domestic production of vehicle regulation MCU chips. So far, BYD Semiconductor has loaded more than 5 million vehicle-grade MCUs and carried more than 500,000 vehicles. Because of this, BYD was able to survive the lack of cores and avoid the impact of production suspension.

Although it seems that personally making cores can reduce the risks caused by "lack of cores", the production capacity problems encountered by The Tier 1 giants are more difficult to solve by car companies that lack the right to speak. In addition, the cycle of self-developed chips is very long, and the probability of failure is very large, far from quenching the thirst, especially for high-end chips such as autonomous driving chips, it is difficult to obtain results without long-term accumulation. In this case, it is wiser to choose to work with Tier 1.

epilogue

Under the window period of lack of cores, the entire automotive chip industry is surging undercurrents, the growing demand of the market has given new opportunities to entrants, OEMs, chip giants do not want to miss this opportunity, and traditional Tier 1 manufacturers do not want to lose their voice in this round of competition.

But the core needs the accumulation of time and technology, the consumer electronics industry, the automotive industry is the same, the out of the game is destined to be the majority, only a few will stick to it.

At the same time, in order to explore the automotive chip industry chain in more depth, at the World Semiconductor Conference held in May, Magnesium will also hold a concurrent forum "2022 World Semiconductor Conference - IC Design Chip Developer Conference", at which time we will invite automotive chip designers, host manufacturers, etc., to explore the current and future trends of automotive chips with the audience.