Global investment institutions on the "green theme" flock, all walks of life expect global electric vehicle sales will rise another 30% to 40% next year, the whole year reached 8 million to 9 million vehicles, and China and the United States will become the main force, China's electric vehicle sales are expected to reach 4 million.

As China's stock market has gathered a large number of relevant listed companies, international investors have also continued to increase their allocation. However, rising raw material prices and technological innovations have brought uncertainty to the industry. How will foreign investment lay out China's green theme in 2022?

Zhang Wei, a senior equity analyst at Temasek's Fullerton Investment Management (Shanghai) Co., Ltd., told first financial reporters that if Tesla's German factory is successfully put into operation and the United States passes the "BuildBackBetter" stimulus bill, the sales of new energy vehicles in 2022 are expected to reach about 8.5 million, and the future is especially optimistic about the development of domestic independent brands. In the midstream, investing in battery faucets is still the best strategy to resist technological uncertainty in the early stages. In terms of the four main materials, the diaphragm is expected to remain the most scarce link next year.

Tesla's German factory and U.S. sales are key

This year, the global electric vehicle shows a trend of "rising more and more buying", which shows the fierce momentum of the "green revolution".

Major institutions believe that the cost problem will be digested by the longer automotive industry chain and end consumers. Wang Bin, co-director of automotive industry research at Credit Suisse Asia Pacific, told reporters that the epidemic situation in Malaysia, one of the main chip packaging bases, tends to ease, and it is expected that the supply of chips will recover significantly. Although there have been signs of price increases in the vehicle recently, the price has still dropped sharply compared with previous years. Taking Ideal Car as an example, there were only 20 stores at the end of last year, and at the end of this year, it has approached 200, an increase of 10 times, and the establishment of a large number of new stores has contributed to sales expansion. Credit Suisse expects new energy vehicles to reach a penetration rate of 25 percent by 2025 and 50 percent by 2030.

The U.S. market is a key variable in the development of new energy vehicles. The U.S. House of Representatives recently passed the "Building a Better Future" proposed to invest $555 billion to support clean energy development and deal with climate change, including the tax credit bill for new energy vehicles, which will subsequently enter the Senate voting process. "Because the sales volume of new energy in the United States this year is less than expected, only a few hundred thousand vehicles, and the expectations of Chinese sales from all walks of life are very full, the United States will become the main source of poor expectations next year." Zhang Wei said.

In addition, when Tesla's German factory will be put into production is also key. Zhang Wei mentioned that if the plant is delayed due to ecological or environmental protection issues, it may have an impact on the output of China and Europe, and there are still variables in the event. He expects that with the gradual reduction of subsidies, the sales of new energy vehicles in Europe next year may reach 2.4 million to 2.5 million, an increase of 14% to 20% over this year. Coupled with 30% to 40% growth in China and the United States, global sales may reach 8.5 million units next year.

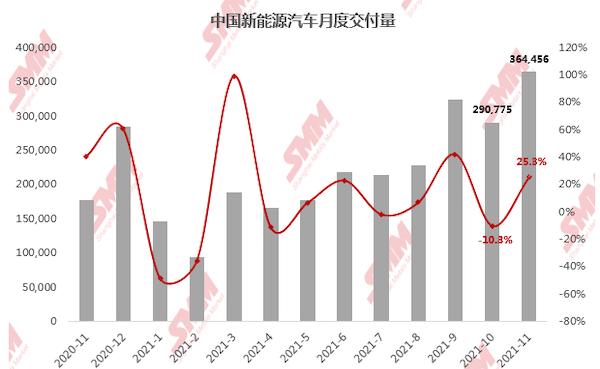

According to public information, due to complaints from environmental protection organizations in Germany, the start of operation of the factory was again postponed to the end of December, and it was originally planned to be put into operation by the end of 2019, with an expected production capacity of 500,000 units. The ModelY will become the main model, but the delay in the production of the factory has directly affected the global capacity distribution and given the veteran car companies room to catch up. According to the information disclosed in Tesla's second-quarter earnings report, the total production capacity of the California factory is 600,000 vehicles, and the capacity of the Shanghai factory is greater than 450,000 vehicles. The Promotion Time of the Berlin Gigafactory is less than a year behind the Shanghai plant, which has begun mass production as early as 2019, and the output of the Shanghai plant rose to about 40,000 units in the second half of this year, and the delivery volume in October was 54,391 units, of which 13,725 units were sold domestically and 40,666 units were exported.

Increase the size of Chinese local car companies

In addition to China's "new car-making forces" that are already very powerful and highly priced, the institution is also optimistic about the development prospects of other Chinese local brands.

"This round is obviously a slow joint venture brand, with very few models launched this year and a network of sales channels not in place." Zhang Wei said that due to the early start of local brands, the brand image is deeply rooted in the hearts of the people, and many of the electric vehicles launched by the joint venture brand are "oil to electricity" platforms, the models are almost the same as earlier, the level of intelligence also needs to be improved, and the response to the needs of end consumers is slow.

A number of institutional sources told reporters that if you want to sort by advantage, it should be China's private car companies (such as BYD, Geely), state-owned car companies, and joint venture car companies.

Chen Qing, an analyst in the new energy industry at bocom International, told reporters that the penetration of new energy vehicles, the development of intelligent vehicles and the rise of independent brands will continue to be the main theme in the future. Independent brands will launch more A-class new energy vehicles and plug-in hybrid vehicles, driving the overall penetration rate to approach or even exceed 20%, and achieve China's 2025 target ahead of schedule. After years of investment and technology research and development, it is expected that independent brands will enter the harvest period in 2022. Optimistic about the new model cycle of strong independent brands, especially in the field of new energy vehicles. The agency gave buy ratings to Great Wall Motors, Geely Motors, GUANGZHOU Automobile Group, Zhongsheng Holdings and others.

Credit Suisse expects china's third- and fourth-level autonomous driving penetration to increase by about 17 percent in 2025 and even higher growth by 2030, supported by a significant drop in costs and China's evolving infrastructure, including roadside smart terminal construction, 5G communication networks, and high-precision maps, all of which contribute to the development of autonomous driving.

Hold the battery faucet tightly

The cost of batteries accounts for about one-third of electric vehicles, and other costs come from the chassis, internal and external, electric, electric motors, body, etc. The investment in the battery link is crucial.

The reporter learned that Morgan Stanley had previously established a global battery portfolio and gathered 25 stock analysts from North America, Europe and Asia to conduct research.

In the Chinese market, CATL is undoubtedly the battery king, although the high valuation has always been controversial, but international investors are still willing to adopt a "tight leader" strategy. Zhang Wei told reporters that in the early stage of penetration, as far as the battery link is concerned, although the valuation of Dragon Two and Dragon Three seems to be cheaper, in fact, it seems that more expensive dragon heads are safer. In terms of cost control, the cost of raw materials soared this year, and the cost of batteries rose by nearly 40%, but leading enterprises have the ability to perceive the price increase trend and supply shortage in the market, and will purchase a lot of materials nearly half a year in advance, and even buy half of the entire market materials, or sign long-term agreements with suppliers such as electrolyte to lock in prices.

In addition, the current battery technology is still rapidly iterating, "the head battery enterprise r & D investment is far ahead, up to 5 billion to 6 billion yuan per year, while dragon two, dragon three may be less than one billion yuan." Once the future sodium-ion battery is launched, the overall battery cost will be reduced by 20% to 30%. After that, semi-solid-state batteries and solid-state batteries will be introduced. Leading R&D investment will enable them to better grasp the new opportunities brought about by technological change. He said.

According to the financial report data, although the upstream raw material prices continued to rise sharply in the third quarter, the Ningde era seems to have been little affected, and the gross profit margin reached 27.9%. Compared with similar companies: the net profit attributable to the mother of Ewell Lithium Energy in the third quarter fell by 14.98% month-on-month, and the gross profit margin was 21.55%, down 2.4 percentage points from the second quarter; the net profit attributable to the mother in the third quarter of Sunwoda fell by 88.81% year-on-year, down 89.36% month-on-month, and the gross profit margin was 21.55%, down 1.89 percentage points from the second quarter.

Pay attention to raw material price changes and technological developments

In addition to the battery itself, the price change and technological innovation of the main material of lithium batteries in the future are the focus of investment institutions.

The four main materials of lithium batteries are positive electrode, negative electrode, electrolyte, diaphragm, this year due to short supply, energy consumption double control, equipment shortage and other issues and prices soared, but the supply and demand pattern in 2022 will change greatly. The tightening of layout and supply is still the core.

The tightest link is still the diaphragm. Zhang Wei said that limited by the production capacity of equipment (diaphragm equipment mainly from Japan, Germany, France), a large number of Japanese companies' production capacity has been booked in advance by China's diaphragm faucet, and other companies have not expanded production so fast, so the diaphragm is still the most missing link in the four main materials, and the positive and negative supply and demand will slowly return to a balanced level, and the electrolyte may appear excessive.

The biggest change is the negative electrode. Since the graphitization of anode materials is a high-energy-consuming industry, under the background of dual control of energy consumption, local government approval is slow and production expansion is limited, resulting in a tightening of the supply of negative electrodes. However, Zhang Wei said that the recent Central Economic Work Conference pointed out that it is necessary to scientifically assess that the new renewable energy and raw material energy use are not included in the total energy consumption control to prevent simple layers of decomposition. From the perspective of new energy vehicles, the previous ranking that was strictly controlled by the assessment and control of energy consumption indicators was negative electrode (graphitization) > positive electrode (ternary & lithium iron) > copper foil.

In addition, technological changes in the next few years are also closely watched, such as the development prospects of semi-solid-state and solid-state batteries, technological changes will not only affect battery costs and energy density, etc., but also affect the vehicle mileage, but also affect the supply and demand pattern of major main materials.

For example, Avant-Garde Blue New Energy has promised to purchase a total of no less than 25,000 tons of solid-state lithium battery materials from Dangsheng Technology (cathode enterprises) from 2022 to 2025. The two sides agreed to strengthen exchanges and cooperation in the frontier technologies of lithium batteries such as high nickel multi-materials, lithium-rich manganese-based materials, lithium cobalt oxide, lithium iron phosphate, and lithium iron manganese phosphate. This is an important step in the development of semi-solid-state batteries.

Zhang Wei said that the development of semi-solid-state batteries will greatly improve energy density and safety. "In the ternary system, China's square battery enterprises can use it to counter the cylindrical 4680 battery, its positive electrode does not change much, the separator will use new materials, currently only the Chinese diaphragm faucet can be mass-produced; the negative electrode is relatively large, will use silicon carbon anode to add lithium, or directly use the full lithium metal anode; the electrolyte will be basically unnecessary."