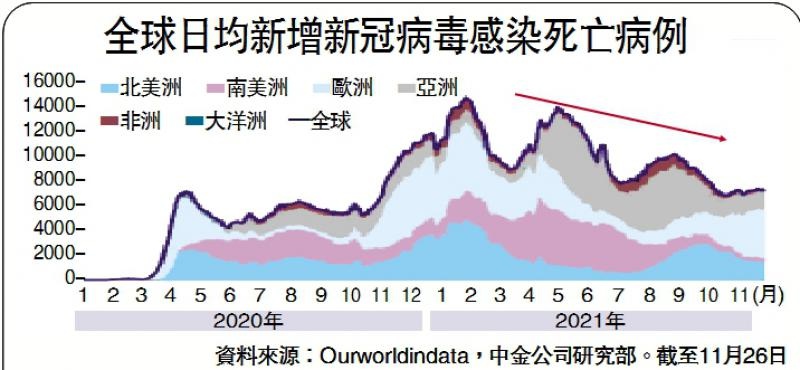

Last week South Africa discovered a new variant, Omicron, that broke the calm in the market. As of now, information about the new variants themselves is not sufficient, and further observation and official authoritative information remains to be seen. So, if you look at it from that point alone, the market's reaction to it so violently on Friday seems a bit overwhelming. The main reasons for market concerns are its high contagiousness and if the current vaccine is ineffective, countries will have to turn back to external or even internal lockdowns, which will disrupt production, demand and supply chains.

The author believes that the possible relatively favorable side of the current situation is that governments and pharmaceutical companies have responded more timely and accumulated more experience in response and vaccine research and development, higher vaccination rates, and the progress of specific drugs.

The relatively pessimistic scenario is that if more evidence follows up suggests that the virus has a higher fatality rate and that vaccines are more ineffective, then the combination of its high contagiousness may make global prevention and control more severe. In this case, a certain degree of external or even internal blockade in some countries is difficult to avoid, which may once again cast a shadow on economic repair, aggravate the pressure on supply chains that are already in a relatively tense state, and then put pressure on asset prices, which is the main reason why the market is most worried. Of course, due to the vaccine gap between different markets, there will also be a significant gap in the ability to respond to the epidemic and the intensity of the lockdown that needs to be adopted.

Considering that in the future, it is not excluded that the vaccine may not be effective and highly contagious at the time of the Delta mutation outbreak, the evolution path, impact characteristics, and asset price performance of the Delta outbreak can be compared to at least some references. We focused on the outbreak in India from March to May, and the Delta outbreak in the United States and Europe from July to September. Specifically:

Delta propagation path and response time

1) From the perspective of transmission time, from the first Delta sample in October 2020, the large-scale transmission in India from March to May, and further to the third wave of global epidemics in Europe, the United States and Southeast Asia in June and September, with an interval of about three months. 2) From the perspective of response time, from the widespread spread of the Delta variant virus, to the acceleration of vaccination, the adoption of certain prevention and control measures, and the development of new vaccines, the interval is about three months.

Asset performance during delta upgrades

1) The impact of the stock market is not large: whether it is India in March-May, or delta epidemic in the United States and Europe in July-September, it has caused a short one-time impact on the market, but it is limited to this. 2) Style shifts to growth: The escalation of the epidemic has hit the affected sectors of the epidemic, while the expected value and cycle of the recovery are also generally under pressure, compared with the continuous decline in interest rates in the same period, and the growth style is leading. 3) Bond interest rates continue to fall, policy tightening expectations cool down: 10-year US treasury interest rates fell back in the early stage of the epidemic escalation, once falling to a low of 1.1% in early August. However, after the beginning of August, although the epidemic situation is still escalating, it is basically flat at the bottom due to the full calculation of expectations. 4) Oil prices fell back and gold flattened in commodities: Oil prices continued to fall until late August due to the cooling of general aviation expectations, which in turn led to a decline in inflation expectations for 10-year US Treasuries, which combined with the still rise in stock markets, which suppressed gold's performance to some extent. 5) Overall strengthening of the US dollar: Although the epidemic in the United States has escalated, other emerging markets have been more affected by the lack of vaccine protection, thus widening the growth gap with the United States.

Delta's influence on different markets and supply and demand characteristics

In addition to the above impact of asset prices, in the long run, the delta variation has had some medium-term effects on the global supply and demand pattern and different markets, which is worth learning.

First of all, pay attention to the growth gap and capital flow gap caused by the vaccine gap, the delta mutation virus has widened the gap between developed and emerging markets, some emerging markets such as Vietnam have to take stricter prevention and control measures because of the lack of vaccine protection, which further affects production, while promoting China's export demand, it also widens the growth gap with the United States, which is also the main reason for the strength of the US dollar.

Second, the impact of the last round of epidemic escalation on both the supply and demand sides is completely different. The impact of the epidemic on the economy is not in the epidemic itself, but more in the policy response. Unlike emerging markets, the United States did not take any overall lockdown measures during the second round of the epidemic escalation in July and September, so from the perspective of practical effects, when the epidemic escalated in the United States, only the demand for travel was affected to a certain extent (such as the number of TSA security checks), but the local demand (such as eating out and entertainment retail, etc.) was basically not disturbed. In contrast, the impact of supply is obviously greater, such as the congestion of shipping and terminals, the shortage of some products such as automotive chips due to the escalation of the epidemic, the decline in capacity utilization in the United States, and the decline in employment, especially in service industries. This is also what needs to be paid attention to in the follow-up if the epidemic brought about by the Omicron variant escalates again.

(The authors Liu Gang and Li Yujie are researchers at CICC)

![The phoenix man did not listen to his wife's advice, and returned to his hometown to show off his wealth for the New Year with an annual salary of 500,000 yuan, and the result was tragic[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)