After all, it is a dream of NanKe.

Source 丨The Information

Written by Josh Sisco, Stephen Nellis

Compilation 丨 Tech Walker

Nvidia has abandoned the $66 billion acquisition of chip designer ARM. After an 18-month regulatory review process, the wave of acquisitions that had been unpromising and even opposed by all parties in the semiconductor industry finally failed.

But after Nvidia and ARM holder SoftBank Group have confirmed the failure of the transaction, where should the various forces involved in the acquisition go next? More specifically, how can ARM, which continues its independent corporate identity, obtain sufficient cash flow to keep pace with competitors such as Intel and continue to meet the urgent needs of customers for subsequent chip open source technologies?

As a SoftBank Group that has always had a unique vision and dared to sell its wholly-owned subsidiaries, it is not clear whether they can find potential buyers for ARM that is comparable to NVIDIA's strength and is willing to take real money and silver such as banknotes and stocks. After all, even if the growth momentum has declined, the realization of Nvidia's trading price is still more than 70%. According to people familiar with the matter, SoftBank's current plan is to promote arm companies to go public in a public offering alone; but considering ARM's actual financial situation, SoftBank may have a hard time recovering the $31 billion it paid to acquire the company in 2016.

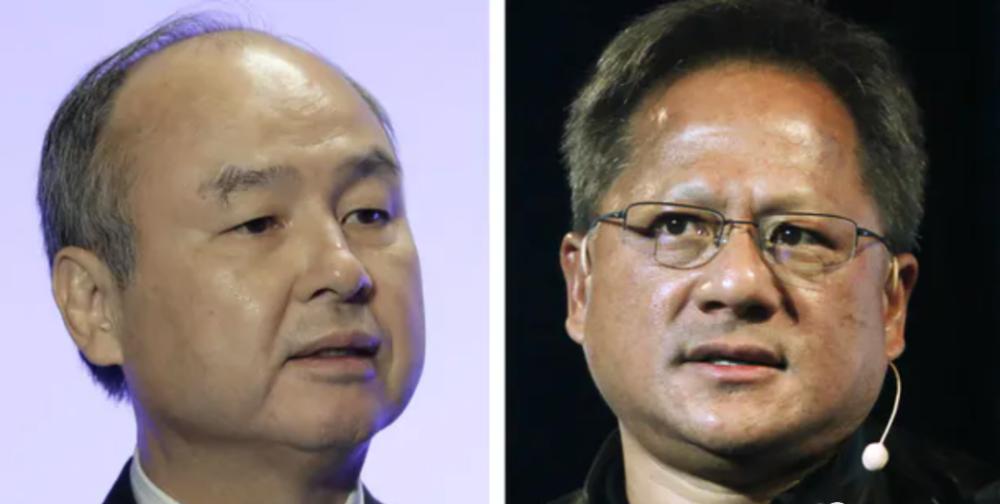

According to people familiar with the matter, under severe regulatory pressure, NVIDIA CEO Huang Jenxun and SoftBank CEO Son Zhengyi have been negotiating almost every day in recent weeks on "whether to cancel the transaction". The person familiar with the matter also said that the "hammer of the fixed tone" before Tuesday's earnings meeting was personally struck by Sun Zhengyi.

In a statement, SoftBank said that "this acquisition transaction is mainly hampered by major regulatory challenges."

ARM

Without this olive branch that NVIDIA extended, ARM has few other reliable options. As the regulator of ARM's headquarters, the UK regulator said that "the sale of a business like ARM to foreign buyers is likely to raise national security concerns". In other words, such a tone also makes Qualcomm CEO Cristiano Amon's proposal to make acquisitions by a consortium of arm's major customers, including Qualcomm, equally difficult to achieve.

The reason why ARM can occupy a unique position in the chip industry is because it has become a "neutral" supplier in this fierce intellectual property competition, so the UK and even local antitrust regulators at all levels naturally do not want ARM to be manipulated by a single chip manufacturer.

Rene Haas, who just became ARM's new CEO on Tuesday, said in an interview that he plans to push the company up and running by March 2023. Haas also mentioned that ARM has not yet determined exactly where to list, whether to list in its entirety or whether to accept other investors before going public.

Haas noted, "We have seen significant growth in our share of the cloud and infrastructure markets, as well as an increase in our share of the automotive market, while continuing to maintain our inherent strengths in the market. We are well prepared to maintain our market position. ”

But for ARM, an independent listing is bound to bring a series of serious challenges. While ARM has been steadily selling some key intellectual property to industry giants such as Apple, Google and Samsung Electronics, actual sales have been limited. In the six months ended September 30, 2021, ARM generated revenue of just $1.46 billion. Although this number has increased by 56% from the same period last year, and some analysts expect ARM's performance to grow further strongly in the next six months, all this is still pale in front of the traditional giants in the chip industry. For example, according to data released by Yahoo Finance, analysts expect Nvidia's sales to be close to $27 billion this fiscal year.

The problem is that ARM clearly needs a lot of cash to keep up with the pace of big competitors. Essentially, ARM's competitive advantage lies in its unique instruction set architecture, which defines what kind of software can run on the chip. ARM's ISA architecture needs to be in direct confrontation with Intel x86 and the open source ISA RISC-V (RISC means reduced instruction set computer) on the market.

Before taking over the headship from former CEO Simon Segars, Haas served as head of ARM's intellectual property division. He said ARM has had its own experience in income creation in recent years. In addition, ARM decided to abandon the development of commercial technologies involving "display and video chips" in favor of more profitable computing technologies in application scenarios such as "data centers".

Haas emphasized, "There is always a misconception about us that arm has become a member of the SoftBank Group, and naturally has an endless budget. We just need to throw money, throw money, throw money again, and don't have to think about the cost performance problem at all. This is certainly not the case, and arm now has the ability to make the right value trade-offs. ”

In addition, the RISC-V ecosystem is in the midst of a wave of investment, with venture capitalists and large tech companies funding startups using the technology, including SiFive, Andes Technology, and Ventana Micro Systems. Intel also said monday that it plans to allocate $1 billion to develop RISC-V and intends to use the architecture in conjunction with its proprietary x86 technology.

The biggest problem arm faces is, "How come I can't get such a generous investment?" "ARM used to get budgets from companies like SoftBank, but now they can only take responsibility for their own profits and losses, and this shift is undoubtedly a serious challenge." ”

Nonetheless, a number of ARM customers have informed the U.S. regulator responsible for reviewing the NVIDIA-ARM deal that the RISC-V structure is unlikely to make much of a splash in the market for at least the next 7-10 years.

Haas mentioned that ARM's main advantage in fighting RISC-V is "at the software level". For decades, most of the world's leading operating systems, including Linux, Android, and Windows, have had modified versions capable of running on ARM. However, the operating system options on RISC-V are limited, either just in the world or not yet complete with the architecture ported.

Haas said, "We have a very strong ecosystem and partner base, they are building chips for ARM, and they are willing to work with us and assist ARM in building products for the ecosystem." I'm not trying to belittle RISC-V, but we do have a greater chance of growth relative to RISC-V. ”

Nvidia

Nvidia should be at a lower risk than ARM, mainly because Nvidia has previously licensed the ARM architecture and recently launched a central data center processing unit based on the ARM architecture.

Stacy Rasgon, an analyst at Bernstein, a research firm, believes that "Nvidia doesn't need a whole acquisition at all" and that their stock "is still good currency, and Nvidia still has a lot of cash in its hands." ”

But the failure of the deal did give Nvidia a heavy blow. NVIDIA CEO Jen-Hsun Huang often stresses that the data center of the future will become a new computing infrastructure unit, and every data center will inevitably need a CPU. Nvidia has acquired Mellanox Technologies for $6.9 billion, and it is also strong in network chips, not to mention the "graphics processing unit" development capabilities that have always been a leader. As the last missing link in the chain, what NVIDIA needs is CPU design capabilities, and the "Grace" processor based on arm architecture can fill this gap. Nvidia has said it hopes to release the Grace CPU by next year; and Avidia has nothing else to expect from arm. Therefore, the failure of this transaction obviously greatly hindered the pace of NVIDIA's development of its own CPU chips.

Ben Bajarin, CEO and principal analyst at Creative Strategies, notes that "the only available and reliable source of CPU intellectual property on the market is ARM. ”

And in order to boost the confidence of Wall Street investors, Nvidia still needs to maintain business growth, which requires them to withstand the offensive of the "back waves" in the machine learning chip market. At present, Alphabet's Google and Amazon have launched competitive chips through their respective cloud computing divisions.

As the world's largest semiconductor developer, any future acquisitions by Nvidia may not escape strict scrutiny. An important intention of its acquisition is to expand its influence in driver assistance systems, and Nvidia's acquisition of ARM clearly takes this core demand into account. A person familiar with the assisted driving market once suggested that NVIDIA may wish to switch to the acquisition of German chip maker Infineon Technologies, after all, this will avoid a considerable part of the censorship pressure. However, considering the high dependence of the German domestic market on Infineon chips, it is believed that this transaction will also be strongly opposed by the German automotive industry.

SoftBank Group

The negative impact on SoftBank Group is mainly concentrated at the "financial" level. According to a source familiar with SoftBank's decision-making, SoftBank's internal decision-makers realized a few months ago that the deal was unlikely to close smoothly, but still did not want to give up the possibility of a huge return. And it wasn't until the Federal Trade Commission formally filed a lawsuit against the acquisition in November, and the Chinese side only started a lengthy review process last month, that the Japanese company finally accepted the reality that it was not happy to suffer the windfall.

At this point, almost no one has been able to buy ARM as a whole, so SoftBank's only "way to liquidate" is to promote ARM to complete the listing through public offerings. But even if the listing is successful, the returns that can be brought are far from SoftBank's expectations. ARM said in a filing last year that SoftBank had previously considered promoting ARM listings in 2019 and 2020, but ultimately gave up because "the stock market will not give SoftBank a return that meets investment expectations."

In addition, the helpless move to promote the listing of ARM is also the first heavy blow to SoftBank's Vision Fund. The Vision Fund, which belongs to SoftBank Group's technology investment arm, acquired a 25 percent stake in ARM in 2017. (The largest limited partner of the Vision Fund is Saudi Arabia)

SoftBank Group has been divesting assets in recent years, hoping to focus on the venture capital business of the Vision Fund, selecting excellent projects from it to make up for its huge investment losses. Just recently, SoftBank sold stakes in its U.S. mobile operator Sprint and asset management firm Fortress Investment Group, and may continue to sell a range of non-core businesses in the future.

-

This article is originally produced by Technology Walker, please do not reprint without permission

![There is no "neutral country" in the semiconductor world[fig]](data:image/gif;base64,R0lGODlhAQABAIAAAP///wAAACwAAAAAAQABAAACAkQBADs=)