In the foreign exchange market in 2022, overseas investment by Japanese companies may become one of the factors leading to the depreciation of the yen. As the prosperity of Japanese companies improves, mergers and acquisitions (M&A) of overseas companies are expected to increase to the largest scale in three years. In Japan's current-account surplus, the majority of the gains from overseas investment have been maintained for a long time. "Investment nation" will incur the sale of the national currency (yen) in terms of both actual demand and expectations.

In the foreign exchange market on February 3, the yen-dollar exchange rate fluctuated up and down in the range of 114.5 to 115 yen per dollar. On the previous day, the employment indicators released by the United States were against market expectations and appeared to be sluggish, and the yen once appreciated to a range of 114 to 114.5 yen against 1 dollar, but the selling yen once again dominated.

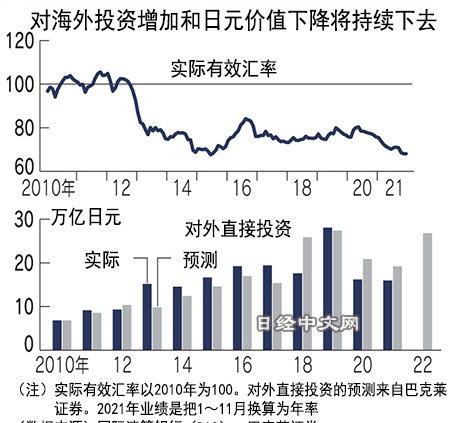

"In mid-2022, the exchange rate against the US dollar may depreciate to around 116 yen per dollar," said Shinichiro Motoda, chief foreign exchange strategist at Barclays Securities. One of the reasons for this is the increase in "outward direct investment" (OFDI) focusing on the mergers and acquisitions of overseas companies by Japanese companies.

Based on the company's estimation of corporate prosperity and cash deposit balances, the outward direct investment of Japanese companies will reach 26.9 trillion yen in 2022, which will increase after two years. This is expected to increase by 10.8 trillion yen compared to 2021. Most Japanese companies use U.S. dollars in outbound mergers and acquisitions, and Menda pointed out that "the increase in outward direct investment constitutes a pressure on the depreciation of the yen."

According to statistics from the Nihon M&A Center, which provides M&A intermediary services, "the majority of the company's M&A intermediary cases were raised after exchanging yen for foreign currency through banks." In this case, foreign investment will directly bring about the demand for selling yen.

If it is a large company to carry out mergers and acquisitions, although the means of raising foreign exchange are diversified, the possibility of selling yen to a certain extent is still very high. Panasonic announced the acquisition of a U.S. software company in April 2021, with approximately $3.5 billion of the $7.1 billion (approximately JPY770 billion at the then exchange rate) payable through cash deposits on hand, with the remainder temporarily raised using transitional financing. Domestic banks said that in this case, "when they obtain transitional financing, there may already be a demand for selling yen."

However, the fluctuations in the yen's exchange rate are not limited to real demand. Barclays' analysis shows that there is also a tendency to temporarily depreciate by about 0.5 to 1% before and after the merger of more than 500 billion yen. On the other hand, in the case of small-scale M&A cases, there is little volatility. Daisuke Tokatsu, chief market economist at Mizuho Bank, pointed out that the root of this trend is "the expectation that acquisitions may lead to a sell-off of this market participant in the yen.".

Looking at Japan's balance of payments in 2020, the trade surplus earned through trade in goods is 3 trillion yen, and if you add services, the trade and service balance is a deficit of 700 billion yen. On the other hand, the surplus of the first income and expenditure (which consists of income from overseas investment by Japanese companies, etc.) reached 19 trillion yen.

In the early 2010s, plagued by a severe appreciation of the yen by more than $1 to 80 yen, Japanese companies moved their bases overseas and made more money through investment than trade. Therefore, the status quo is that although the subsequent monetary policy has led to the depreciation of the yen, "the trend of investment targets choosing overseas to 'avoid Japan' has not stopped" (Tang Kamakura).

Looking at the real effective exchange rate calculated by the Bank for International Settlements (BIS) and showing the comprehensive strength of the currency, the strength of the yen has fallen to the level of 50 years ago. At that time, Japan's export industry accounted for a large proportion, and it fully benefited from the depreciation of the yen and gained benefits. In contrast, the sell-off of the yen brought about by the "founding of the investment country" is gradually reducing the purchasing power of the yen.

Nihon Keizai Shimbun (Chinese Edition: Nikkei Chinese.com) Gakuto Takako

Copyright Notice: All rights reserved by Nihon Keizai Shimbun, unauthorized reproduction or partial reproduction, violation will be investigated.

Nikkei Chinese.com https://cn.nikkei.com