If Buffett's Berkshire is an insurmountable peak in the value investing world, Baillie Gifford (BG) from Edinburgh, Scotland, is another.

Invested in Amazon in 2004, Illumina in 2011, Tesla in 2013, Alibaba in 2014, Shopify in 2017, Modena in 2018... All of them have made BG an amazing return.

When BG first started investing in Amazon, Amazon's revenue was only $7 billion, and by 2021, that number has soared to nearly $470 billion, and the stock price has soared more than 60 times.

Tesla, one of BG's most successful investment projects, has soared more than 30 times since 2013, doubling its market value from less than $20 billion to more than $1,000 billion.

Over the past 20 years, BG's assets under management have grown 15-fold. As at the end of December 2021, BG had £336 billion in assets under management.

Looking back at its development history, it is not difficult to find that in addition to adhering to its ancient and unique governance structure of unlimited responsibility partnership, maintaining a diverse, optimistic and curious corporate culture, BG's ultra-long-term investment philosophy and style are the main reasons for its success.

01

100 years of practice: adapt to the times + layout globally

Founded in 1908 and with a long history of 114 years, BG is an established investment fund.

At first, BG had only two founders: Colonel Augustus Baillie and Lawyer Carlyle Gifford, neither of whom had a financial background.

In 1908, Ford's first "T-car" swept the United States, the two founders realized that the United States as an emerging market is about to usher in a big explosion, so they decided to transform the investment field, BG's first funds after the establishment of the British Malaya rubber plantation that provides raw materials for car tires. BG earned the "first pot of gold" through this investment.

At the end of World War I, BG continued to be bullish on the United States, focusing on the infrastructure industry, and merged into railroad companies such as the United Pacific Railway, eventually investing 20% of total assets in the United States. Once again, BG made the right choice.

After World War II, the depreciation of the pound sterling brought prosperity to the British financial industry, the trust industry was greatly boosted, and the BG, which relied on trusts, made a lot of money, but the company's second-generation management was gradually blinded by temporary glory.

During the stagflation period in the 1970s, the trust industry was greatly affected, but the company remained focused on the immediate customer base, and BG's capital end began to decline. Even more deadly, in 1978, BG's second-largest client, Edinburgh & Dundee Trust, was acquired, and the client brought in more commissions than the company's profits. BG was in crisis at one point.

Although it was finally safe to survive the crisis, BG decided to step out of his comfort zone.

In 1979, Thatcher's Conservative Party came to power and issued a series of stimulus policies that began a 20-year bull market in Britain. During this period, the U.S. and Japanese markets, where BG was heavily positioned, came out of the downturn of the 1970s and entered a period of rapid development.

It is worth mentioning that learning from the lessons of excessive concentration of trusts in the early stage, BG began to vigorously expand pension customers. The long-term stability of pension liabilities coincides with BG's investment philosophy, so BG has attracted a large number of institutional investors such as pensions, insurance, and charitable funds. To this day, pensions remain BG's most important customer group.

The bull effect combined with this key investment, and the assets under management of BG soared from £300 million in 1979 to £16.2 billion in 1998.

Fast forward to the millennium, the dot-com bubble, and the subprime mortgage crisis of 2007, which hit market confidence hard. In order to continue to maintain growth, BG actively deploys overseas emerging markets such as China, India and Brazil.

Especially the Chinese market. BG issued its first China-themed fund in 2008, which invests primarily in the consumer, healthcare, technology and other sectors. As of the end of March this year, the size of the fund was about 49 billion pounds, and it was heavily positioned in Tencent, Alibaba, CATL, JD.com, Meituan and other enterprises.

From the U.S. market, to the local market, to the overseas new market, BG's bets conform to the trend of the times, and the business gradually covers the global market.

After a century of precipitation, BG's core investment strategy has taken shape: long-term global growth strategy (Long Term, Globle Growth, LTGG), that is, to mine and invest in the most competitive, innovative and growth-efficient high-quality enterprises on a global scale, with a position holding period of more than five years.

02

Investment philosophy: adhere to long-term investment + not afraid of short-term fluctuations

"Real investors think on a ten-year basis, not quarterly," is BG's best-known investment philosophy.

The slogan "long-term investment" is often heard in the fund market, but it is difficult for investors to be undisturbed by short-term news.

The "efficient market theory" holds that the price of a stock fully reflects all the information available to the asset, that is, "information is valid", and once new news appears, the price of the stock will certainly change accordingly.

This theory shows that it is reasonable for investors to pay attention to corporate earnings announcements and macroeconomic news. The power to chase short-term returns, in turn, underscores the theory, with James Anderson, the BG ace fund manager of Tesla and Amazon, single-handedly mining tesla and Amazon, saying in a 2021 letter to investors.

But this information may not be a true indication of the future.

Take Tesla, for example. When BG took a stake in Tesla in 2013, BG realized that one day in the future, electric cars would have higher performance and cheaper prices than internal combustion engine cars. Given that only Tesla had such strength in the Western electric car field at that time, BG's investment decision was simple and clear.

However, Tesla at the time was plagued by negativity. Tesla stocks in just 6 weeks after three Model S spontaneous combustion accidents, the price fell nearly 37% in two months, the market value shrank by $8 billion, Tesla was once in crisis.

Now, investors at the time were confused by wall Street analysts and short-selling institutions that spread panic. Musk's unguarded mouth often leads to abnormal fluctuations in Tesla's stock price.

But the news is a market failure for BG, which believes Musk can lead electric vehicles to victory over internal combustion engine vehicles. Therefore, the BG option is to buy and then wait patiently. It was also this year that Tesla broke out for the first time in the US stock market.

In the 8 years since, the outside world has never stopped questioning Tesla, Tesla once became the hedge fund's favorite short stock, but no matter what storm Tesla encountered, BG insisted on long positions: from March 2015 to December 2016, BG also increased its position six times when Tesla's stock price was weak. By 2017, BG had jumped to Tesla's second-largest shareholder.

By the end of 2020, BG's flagship fund, the Scottish Mortgage (SMT) Fund, made $29 billion (more than 100 billion yuan) on Tesla, making a name for itself in the investment world.

BG's obsession with long-term investment philosophies is behind its promotion of predictability of the future, and it believes that Moore's Law has the ability to predict many things. According to Moore's Law, at the same cost, a computer's computing power doubles every 24 months. The law has successfully predicted computer trends over the past 50 years, and according to Martin van den Brink, chief technology officer of Dutch chip giant ASML, the validity of Moore's law can be extended for at least another 10 years.

In his letter to investors, Anderson said:

"The specific impact on investment judgments can be vague and imprecise. But just by keeping in mind the exponential growth model, investors will open their eyes to PCs, video games, mobile phones, the Internet and e-commerce, new energy, gene editing, and more. ”

Anderson, who will retire on April 30, joined BG in 1983, became a partner in 1987 and began managing SMT in 2000. He is good at capturing high-growth enterprises and accompanying them for a long time, Amazon, Tesla, Alibaba, and Modena are all heavy targets of SMT.

For more than 20 years under his management, SMT generated a 1371% return for shareholders, far exceeding the 343% return of the FTSE Global Index.

But in the past year, SMT-focused technology stocks have suffered a heavy setback due to fed interest rate hikes. The price of stocks managed by SMT fell nearly 10 percent, and the return it created fell to -13.1 percent, well below the FTSE Global Index's 12.8 percent.

SMT performance as of March 31, 2022, source: BG official website

This has left many pessimistic investors wondering if tech stocks have lost their momentum.

Anderson admits that in his career, whether it was the bursting of the dot-com bubble or the financial crisis of '08, he had never seen a sell-off in tech stocks like this, regardless of future potential. Factors that affect the long-term development of enterprises have been ignored.

He believes that black swan events are unavoidable and investors must withstand the impact of short-term volatility and focus on the long term.

"Ominous days are always there, but I think if you can afford it, your clients and savers can afford it, then finding extreme winners is the best way to invest."

03

Investment style: active investment + less win more + low turnover rate + strict control of positions

In investment and wealth management, investors are faced with two basic investment strategies: active investment and passive investment.

The so-called active investment is that investors will operate more actively in the market, take the initiative to select stocks, and take the initiative to choose the time. They believe that their investment ability can beat the market. Therefore, active investing requires investors to have the ability to study and analyze, obtain information and seize the opportunity over the long term.

For example, Buffett and Lynch, these investment masters are active investors and have the ability to actively manage assets.

Passive investing is a concept that has emerged in recent years, focusing on asset classes, investing in indexes, not actively seeking to surpass the market, but trying to replicate the performance of the index, which is simply a way of investing with the flow. Passive investment is less expensive than active investment, so it is increasingly favored by investors.

BG is clearly not a big investor. BG believes that since the 19th century, the original intention of equity investment has been to focus on real companies and real projects, but passive investment is only concerned with reducing transaction costs, ignoring the ability to judge the long-term competitiveness, financial situation and strategic ability of enterprises.

BG has always believed that real investment needs to find and accompany a very small number of great companies in the long term, because the return on investment is "asymmetrical" and the vast majority of returns come from a very small number.

According to a study by Hendrik Bessembinder, a professor at Arizona State University, from 1926 to 2019, U.S. public companies generated a total of $47.4 trillion in net wealth for shareholders, of which net wealth created by top 5 companies accounted for 11.9% of total net wealth, and 50% of net wealth was created by the top 83 companies (the proportion was only 0.3%). In addition, more than 57% of companies cause shareholders to lose their wealth.

The study also found that the concentration of wealth creation in the stock market has increased in recent years. From 2017 to 2019, the net wealth created by the TOP 5 companies accounted for 22.1% of the total net wealth.

Therefore, successful investment is to try to find as many new superstar companies as possible, and the biggest difficulty in investing is also this.

Anderson argues that companies with unlimited potential should have the following characteristics: never set limits on themselves, no historical baggage; a founder who leads the company (almost so); and a unique business philosophy (usually originally created from the "first principles"). Except for the second one, Tesla fits Anderson's description perfectly.

BG has designed a "due diligence ten questions" for Tesla's core competitiveness, business model and long-term geometric growth logic. Later, BG will follow the law for large-scale investment projects, including NVIDIA and Nio.

Source: BG official website

BG began to vigorously reduce tesla holdings in 2020, a move that once pulled tesla stock price. Anderson said Tesla's stock price has soared beyond the weight limit of customer portfolios, which means that it needs to reduce its holdings, but it is still very optimistic about the company itself.

But his successor, Tom Slater, pointed the finger directly at Musk: "Tesla has become more and more dependent on Musk, a talented leader in recent years, but the operational execution is insufficient, limiting Tesla's growth space and expanding production capacity has become stretched, so we have reduced our holdings." ”

As of now, BG has reduced its stake in Tesla to 1%. However, from the perspective of the proportion of BG positions, Tesla is still the object of BG's heavy position. By the end of 2021, Tesla still accounts for 6.3% of its holdings.

Source: Whalewisdom

In BG's portfolio, in addition to Tesla, Amazon, Tencent and other successful cases, there are also many failure cases, such as Brazil's former richest oil company OGX and German solar panel manufacturer Q-CELLS (both companies have filed for bankruptcy), Lending Club, whose stock price has been in a slump for a long time due to founder violations, and Airbnb, which is in trouble due to the impact of the epidemic. However, BG did not put the entire portfolio in trouble because of the volatility of one of the companies.

The reason is that BG will strictly control the position, ensuring relative dispersion and no leverage.

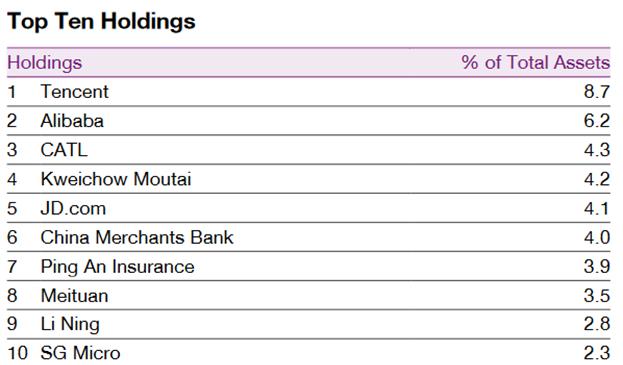

Taking the SMT fund as an example, as of March 31, 2022, its portfolio covers 53 listed companies and 49 unlisted companies, with a concentration of 44.3% in the top ten heavy positions, and the highest proportion of a single position does not exceed 10% in principle.

Top 10 SMT positions as of March 31, 2022, source: BG official website

In addition, the combination of diversified and heavy growth companies, if only one or two of them are successful, is enough to make up for other unavoidable losses.

BG's long-term investment philosophy and fascination with super-growth companies have resulted in a much lower turnover rate than its peers.

In the past three years, the average holding time of BG funds has exceeded 7 years, and the average holding time of similar institutions in the world is about 2 years. BG's turnover rate has been low for a long time, with the 2021Q3 report disclosing that its average turnover rate over the past decade is about 4%.

The data also tells us that even active investors, in the case of active trading volume, are still likely to perform worse than the broader-cap index. Biggest winner = active investment + low turnover rate.

Between 1995 and 2013, the most active and high-turnover fund managers performed 1.9% lower than the broad-cap weighted index after cost, and the most active and low-turnover fund managers performed 2.3% higher than the large-cap weighted index after deducting costs.

As a century-old store, BG has the acumen, curiosity and creativity that is not common at this age, and the patience and confidence that should be at this age. In fact, whether it is long-termism, active investment, less than more, diversification, BG is essentially concerned with the development prospects of the company for the next decade, this simple investment philosophy makes them fundamentally different from the modern financial market obsessed with complex models of investors.

Resources:

1、Wealth Creation in the U.S. Public Stock Markets 1926 to 2019, Hendrik Bessembinder

2、TheScottish Fund Manager That’s One of the Biggest Winners on Tesla, The Wall Street Journal

3、Stayon the road less travelled, James Anderson

4、Collecting Thoughts, James Anderson

5、What Others Teach Us, Lessons in Investing, Lawrence Burns

6、https://www.bailliegifford.com

7. What is a real investment? The BG fund, which made 20 billion yuan at Tesla, said so, Happy Fortune Pass

8, smashed Tesla's BG, what's the beginning?, Happy Fortune Pass

9. Overseas asset management profit model from Baillie Gifford, Huatai Securities

Star Wall Street sees, good content is not missed

This article does not constitute personal investment advice and does not take into account the specific investment objectives, financial situation or needs of individual users. Users should consider whether any opinions, opinions or conclusions in this article are appropriate for their particular situation. The market is risky, investment needs to be cautious, please judge and make decisions independently.

Buffett bet on Apple, BG on Tesla