Written by Deng Xiaoxuan

Editor/Chen Jiying

2021 has come to an end, and this year's mobile phone market can be described as "like a flat lake, dark tide".

Plain pointing to the shipment of mobile phones, Canalys data shows that the cumulative shipment of domestic smartphones in 2021 is 333 million units, an increase of only 6.36% over the 330 million units shipped in 2020, which is flat.

The dark tide refers to the competition of brands, under the competition of stock, the industry is highly involuted, "Huawei falls, others are full", the pattern is reshaped, and the position is rearranged.

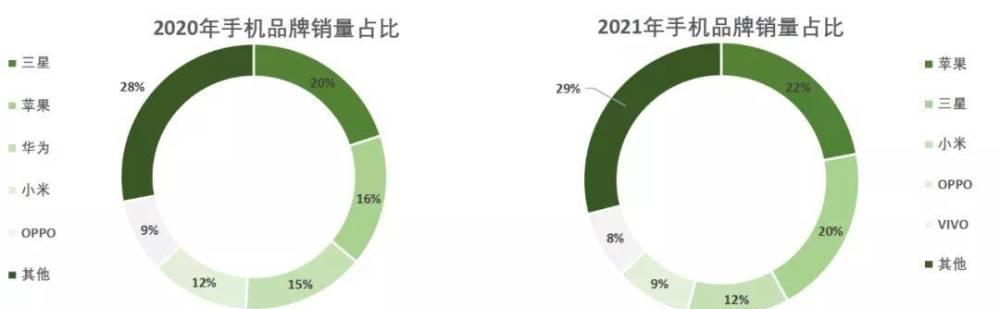

After Huawei gave up the global market because of the Sino-US dispute, Apple and Xiaomi worked hard to encroach on Huawei's share, OPPO and vivo were also dividing the soup, and Glory achieved a big reversal in the second half of 2021; the global mobile phone market share ranking changed from the previous "Samsung, Apple, Huawei, Xiaomi, OPPO" to "Apple, Samsung, Xiaomi, OPPO, vivo" top five competition.

In addition to the competition of the dragons, the old brands such as ZTE, Meizu and Coolpad have also made a comeback.

ZTE shipped more than 100 million units in 2021, an increase of 60% year-on-year; Meizu announced the return of its brand Meilan on September 10 and released 30+ new products; Coolpad, one of the former four domestic giants, also officially returned with a thousand yuan machine.

In the dark tide of the surging red sea of mobile phones, what changes have happened to the form and brand of mobile phones in 2021? What are the trends and developments in 2022? "Financial Story Club" will try to outline the whole picture from three angles: mobile phone form, brand position and industry challenges.

The multi-camera wind is suspended, it is difficult to break through the photo, and the folding screen is surging

In 2021, mobile phones show two major trends in form: the speed of multi-camera is slowing down, and folding screens are gradually becoming a trend.

With more and more application scenarios of mobile phone photography, a single lens is difficult to meet the user's photographic needs, and the improvement of the photographic effect, as a selling point of mobile phones, is easy to be perceived and favored by users, and the number of mobile phone cameras from single to dual cameras and then to multi-camera development, is also the main theme of mobile phone form changes in 2017-2020.

In 2017, the multi-camera penetration rate of mobile phones was 0, and by the end of 2020, the penetration rate of smart phone rear multi-camera has reached 78%, which means that nearly 8 out of 10 have more than 3 cameras in the rear.

At present, the average number of single smartphone cameras is 4.3, and according to Frost & Sullivan data, the average number of single mobile phone cameras will be 4.9 by 2024, and the number of cameras has grown near the ceiling.

After the number of cameras is approaching the upper limit and the significant improvement of mobile phone camera function is difficult, mobile phone manufacturers have found another innovation that is easy to be perceived and accepted by consumers - folding screens bear the brunt.

In 2021, folding screen mobile phones have emerged, with "Samsung plus code, Huawei power, millet OPPO into the game, glory suddenly" to describe the most appropriate, major mobile phone manufacturers have released folding screen new machines to seize the market, 2021, also known as folding screen mass production of the first year.

From the perspective of shipment data, the folding screen mobile phone volume is obvious, the market research institute Counterpoint data shows that in 2021, the global shipment of folding screen mobile phones will reach 9 million, accounting for 0.63% of the global smartphone shipments (1.4 billion units); compared with 2020, the global folding screen mobile phone shipments are only about 1.947 million units, accounting for only 0.15% of the overall shipments of smart phones.

Entering 2022, the beginning of the folding screen did not disappoint, honor released in mid-January released le 9999 yuan folding screen mobile phone Magic V (12GB / 256GB priced at 9999 yuan), the current mobile phone manufacturers, only Apple and vivo seem to be standing still.

But in fact, Apple has begun to recruit, as early as May 2021, it announced the latest list of 37 shortlisted suppliers, of which 11 companies Chinese mainland, and 2 of these 11 companies (Jingyan Technology, Fuchigao) are involved in the metal powder injection molding process (MIM).

MIM is a new manufacturing process technology that combines powder metallurgy and plastic molding process, which is the key technology of the hinge that must be used in the folding screen, and the hinge is the largest cost of the folding screen mobile phone, and the cost disassembly of the IT home found that the hinge cost can account for about 10% of the terminal retail price.

▲The circle drawing part is the hinge of the folding screen mobile phone, and the main technology is MIN

Guo Mingpei, a researcher at Tianfeng Securities, once proposed that in the consumer electronics industry, Apple is the vane of innovation, and xiaomi is the key to product promotion.

It is reported that Apple will launch folding screen products next year, and it can be predicted that when Apple launches folding products, or the starting point of folding mobile phones to really mainstream.

With the launch of OPPO FindN, the folding screen mobile phone really takes into account the high quality and low price, and now the price of this mobile phone has dropped to less than 8,000 yuan, and the folding screen mobile phone has gradually stepped over the biggest obstacle to mainstreaming " of "expensive price". Xiaomi, on the other hand, will lower the price of folding screen mobile phones to less than 7,000 yuan.

Therefore, with the launch of new models of major brands and the continuous decline in prices, the research institute Counterpoint optimistically predicts that the sales of folding screen smartphones in the global market are expected to reach 18.3 million in 2022, an increase of 103.33% year-on-year; by 2025, the global sales of folding screen smartphones are expected to reach 57.4 million units, with a compound growth rate of 58.92% in 4 years.

There are two reasons for the outbreak of folding mobile phones: first, for users, breaking through the limitations of screen size, meeting the needs of richer applicable scenarios, and solving the contradiction between screen size and one-handed operation convenience and portability; second, for mobile phone manufacturers, folding screens are rare innovations that can be perceived by consumers in time in addition to the development of mobile phone lenses to multi-camera, which helps to pull the tide of replacement.

At present, the folding screen mobile phone has not yet exploded on a large scale, the surface reason is subject to high prices, the depth of the reason lies in the supply chain - seemingly simple folding, but it requires the technology and production capacity of upstream manufacturers such as AMOLED flexible screens, flexible covers, hinges, etc., and the threshold is not low.

Also taking the hinge as an example, the hinge design of the Honor Magic V is composed of more than 200 parts, and the requirements for three-dimensional assembly accuracy have reached the level of 0.01mm, making it difficult to quickly break through the production cost and production capacity.

Only to solve the above pain points, is the folding screen really from the brand pile, to the critical point of mass popularization, in 2022, a certain trend is that the mainstream of the folding screen has sounded the trumpet.

Out of the sea to break the waves, the position is reversed

On the brand side, Transsion and Glory are the two brightest stars in 2021, not because their overall sales are the first, but with the strongest breakthrough, the former corresponding to the international market; the latter corresponding to the domestic market.

According to the global smartphone shipments released by Canalys, the top five are "Apple, Samsung, Xiaomi, OPPO, vivo", and the sixth place is squeezed into a new face - Transsion, whose parent company is Transsion Holding Group, which includes three brands of TECNO, Itel and Infinix.

Transsion was founded in 2006, not recognized by the mainstream public, is because its mobile phone products bypass the Chinese Red Sea, focus on the sea, with three sub-brands, with low prices (average unit price of less than 200 yuan) and functions (designed for Africans to take pictures, waterproof and other technologies), beat Samsung, Nokia, the achievement of "the king of African mobile phones".

Through intensive pushing in 60 african countries, TRANSSION has won more than 50% of the market share in Africa; in the first half of 2021, TRANSSION ranked first in the African mobile phone market for four consecutive years with 96 million mobile phone shipments, and is a veritable invisible leader. Compared with anchoring developed countries such as Europe and the United States, Transsion anchors Africa's dimensionality reduction strike, and the odds of winning are higher.

In addition to Transsion, other brands are also following the trend, and OPPO also uses the brand matrix to quickly attack globalization:

OPPO's sub-brand realme was officially released in India in May 2018, the growth momentum of the three years since its establishment is quite rapid, Counterpoint data shows that in 2021, realme ranks fourth in India with a market share of 14%; OPPO's other independent brand hit the Indian mid-to-high-end market, Counterpoint data shows that its market share in the indian mid-to-high-end market is about 27%, one plus, Realme, OPPO has a cumulative market share of 32.8% in India.

In addition to the Indian market, realme also performed prominently in other markets: the Philippines ranked No. 1, the Czech Republic, Greece and other mobile phone market shares entered the top 4, and the Russian market ranked No. 3.

It is predicted that in 2022, emerging market countries are still in the "functional machine to smart machine switching" upgrade tide, the development of 5G construction in developed countries is in full swing, the 5G replacement tide will bring new opportunities, a new round of global market fighting has been fully launched, and domestic brands are also accelerating.

Focusing on the domestic market competition from the brand to the sea, Glory made a strong comeback in the second half of 2021.

After Huawei divested Honor in November 2020, Honor's market share has been declining all the way, from 14% in the third quarter of 2020 to 5% in the first quarter of 2021.

In the third quarter, with 14.2 million units of shipments, Honor's market share reached 18.3%, surpassing vivo and OPPO, ranking third in China, deducing an unprecedented V-shaped reversal; in 2021, Glory shipped 0.4 billion units, becoming the fourth largest smartphone shipping manufacturer in China.

The counterattack of Honor in the third and fourth quarters is the joint effort of the two ends of the channel and the product:

On the channel side, Glory takes the dealer level cooperation and is widely spread in large, medium, and small cities: one, although Honor Huawei has separated, offline Huawei and Honor share channels in many places; second, when Glory Huawei is separated, there are multiple offline channel providers in glory acquirers, and the interests are deeply bundled, so Glory quickly completed the construction of offline channels.

On the product side, Honor has successively released three key products: the Honor 50 series released in June 2021, the Honor Magic3 series released in August, and the Honor Play5 Vitality Edition, honor X30i and Honor X30Max in October, and the new machines released are priced between 2000-3000 yuan, which helps Honor maintain its advantage.

2000-3000 yuan model is the advantage of the glory of the price, in many brands, to maintain the highest or second market share, the new model positioning is clear, strengthen the price advantage.

Looking to the future, even if the crisis is fraught, glory is still full of hope, and there is still enough sinking space for offline channels; overseas, online channels, high-end markets, there are still high ceilings on these three paths:

In overseas channels, Honor 50 in Malaysia, Europe, Africa and other markets synchronous release, intensive appearance; online channels have not yet been forced, the core task of Glory independence at the beginning is to stabilize offline channels, to be alleviated by the lack of core, Glory online there is still a lot of room for power; in the high-end market, try folding screens, etc., to launch a tough battle to the high-end.

Therefore, domestic mobile phone brands such as the endless beast, carry out a long march of market competition without end, are launching a fierce attack at both ends at home and abroad, and the high and low ends are comprehensively laid out.

The pain of lack of core, strive to self-research

The wave of lack of core in the mobile phone industry began at the end of 2020 and intensified throughout 2021.

Chips are highly dependent on the global industrial chain. The fuse for the lack of cores is the Sino-US trade war, and then because of the intensification of the epidemic, the chip supply chain shutdown and the decline in production capacity have led to the already tight chip supply, which in turn has triggered the malicious hoarding of goods by channel providers, which has aggravated the supply shortage and price increase in the chip industry.

Shipments are less, prices are rising, and delivery cycles are all manifestations of the lack of cores in the field of mobile phones in 2021.

Huawei bore the brunt of the attack, due to sanctions, processor chip production and shipments were severely restricted, and the global market share fell from the third in 2020 to the seventh in 2021, resulting in Huawei's mobile phone being difficult to find and users waiting to be fed.

Samsung, the world's largest smartphone manufacturer, was also affected by chip shortages, with mobile phone shipments falling by 20% in the second quarter compared to the previous quarter.

Apple revealed at its July 2021 earnings report that the chip shortage spread to the mobile phone business in 2021Q3, and the capacity limit in the third quarter was further aggravated from the second quarter.

Xiaomi's flagship machine, the Redmi Note 10, launched in India in March 2021, cost about $161, but by July, due to the shortage of production capacity, the retail price had risen to $174, an increase of about 8%, and the Xiaomi 11 Ultra launched by Xiaomi in India in April was also delayed until July due to lack of cores.

Yu Xiaohui, president of the China Academy of Information and Communications Technology, disclosed that the lack of cores has led to an extension of the supply cycle of mobile phone chips from 3 months to 12 months, and the extreme situation of delaying for 9 months mainly affects small mobile phone manufacturers with weak voice.

Generally speaking, mobile phone manufacturers have three ways to obtain chips: directly buy chips, buy IP chips, and develop self-developed chips.

Buying chips is to buy chips from chip manufacturers such as MediaTek and Qualcomm, the advantage is that there is no need to invest a large number of research and development costs, and the disadvantage is that it cannot meet special needs and is easy to be stuck neck.

Buying IP chips refers to the pre-designed and verified function modules in the chip, and the chip design company then purchases IP through a similar way to build blocks to achieve a specific function, which can be understood as a chip semi-finished product, the advantage is to shorten the chip development time and save the research and development costs of infrastructure, but in fact, this way still needs to be handed over to the cooperative manufacturers to manufacture and test, and it is also difficult to escape the dilemma of the card neck.

Self-developed chips, as the name suggests, is to invest a lot of manpower and material resources for chip self-research.

After experiencing the pain of Huawei chip suppression, the difficulty of lack of cores, and the lack of core technology, there is no future, domestic mobile phone manufacturers have raised the banner of core manufacturing, and have tried to launch self-developed chips in 2021.

Xiaomi's Xiaomi 12 Pro, which was launched in December 2021, is equipped with the first self-developed fast-charging chip "Surging P1".

OPPO launched its first self-developed chip, Mariana Marisilicon X, on December 14, 2021, achieving a breakthrough in energy consumption ratio, camera HDR, AI processing of images, and sensor customization, which will be installed on the Find X4 released this year.

Vivo launched its own V1 image chip in September 2021, which is specially designed to process image functions such as mobile phone photography and video.

Huawei is the first to embark on the road to the core of the enterprise, in October 2004 established HiSilicon Semiconductor Co., Ltd., has launched a number of chips such as Kirin, Balong, Lingxiao, Kunpeng and Shengteng; after being sanctioned by the United States, Huawei accelerated the pace of chip self-development, at the end of December, Huawei European executives revealed that Huawei's Shanghai R & D center has begun to study the entire set of 5G chips, is expected to be as soon as 2023 after successful research and development with new flagship mobile phone products, officially breaking through US sanctions.

Honor CEO Zhao Ming said that it is already possible to launch a chip for power management, or Bluetooth, Wi-Fi chips. However, "in the short term, we have no plans to do baseband chips or SoC chips", Zhao Ming believes that Honor can optimize the underlying capabilities of supplier chip hardware based on its own research and development capabilities, "so that the combined energy efficiency can be better."

A mobile phone is composed of many chips, self-developed chips are not achieved overnight, must make up their minds and continue to invest, because this is a long-term battle, domestic mobile phone manufacturers are still far from attacking chips.

In 2022, the competition in the mobile phone market will only become more intense: high-end is the must for mainstream brands, folding screen is a must for high-end breakthroughs, it will become a river of spring water that disturbs the innovation of smart phones; brands going to sea is also the focus of contention, using domestic supply chain, brand, price advantages to conquer the new blue ocean; self-developed chips are the trend of the times, grasp the core technology, break through layers of barriers, improve the industrial chain, even if the pace is alarming.