Author: Gao Wei, Yu Zeming

preface:

In order to fully implement the "double carbon" goal, the meeting of the Political Bureau of the CPC Central Committee on July 30, 2021 further proposed to "tap the potential of the domestic market and support the accelerated development of new energy vehicles". In line with this strategy, on December 14, the China Insurance Industry Association issued the "Exclusive Clauses for Commercial Insurance of New Energy Vehicles (Trial)". This clause solves the two "mismatches" of new energy vehicles in the current provisions: that is, in terms of insurance liability, it provides protection for scenarios such as "three electricity" systems, parking and charging, and realizes risk protection and risk matching; in terms of rates, establishes an exclusive rate table to match risk premiums with risk value.

As a leading data and analysis expert in the auto insurance industry, Jingli Lianxun and its parent company, Lexong Lianxun Risk Information Co., Ltd. (hereinafter referred to as "L&C Risk"), draw on the business philosophy of the international mature auto insurance market and the practical experience of china's auto insurance industry, and delve into the possible impact of new elements of auto risk on china's auto insurance market. This series of articles and the auto insurance industry share some of Jingli Lianxun's research experiences on new automotive technologies such as new energy technology, ADAS and driverless technology. On the basis of the analysis of one of the new elements of vehicle risk: pure electric vehicles, published in the BOC Insurance News No. 4893 on July 7, 2020, this article explores in depth the various important factors affecting the compensation risk of new energy vehicles.

On the occasion of the release of the exclusive terms of new energy vehicle insurance, Jingli Lianxun launched a database of new energy models to the auto insurance industry, as well as a "dynamic and static integration" risk score based on the static structure information of new energy vehicles and dynamic usage information. The solution has been recently validated by customers and can greatly improve the risk segmentation capability of new energy vehicles in the auto insurance industry.

The full text totals 4768 words and is expected to take 9 minutes to read

1

Overview of the current situation of the new energy vehicle market

Many countries around the world regard the development of new energy vehicles as an important strategic measure to cope with climate change and optimize the energy structure, and have promoted the development of the new energy vehicle industry from strategic planning, scientific and technological innovation, promotion and application. As an important part of the global new energy vehicle market, China's new energy vehicle market has also shown strong growth potential.

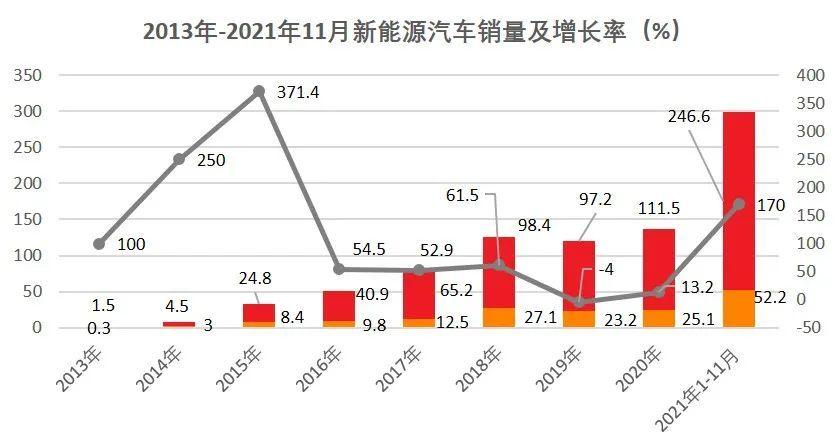

First of all, the production and sales of new energy vehicles in China showed a rapid growth trend, with sales of 1.367 million units in 2020, an increase of 10.9% year-on-year, ranking first in the world for six consecutive years. China's automobile manufacturing industry actively explores new energy vehicle technologies such as pure electric vehicles and hydrogen fuel cells.

Secondly, China's new energy vehicle market maintained a double increase in ownership and penetration. By the end of 2020, there were 4.92 million new energy vehicles in China, accounting for 1.75% of the total number of vehicles. There are 4 million pure electric vehicles, accounting for 81.32% of the total number of new energy vehicles. Between January and November 2021, new energy vehicle sales were 2.99 million units, up 1.7 times year-on-year. Among them, the sales of pure electric vehicles were 2.466 million units, an increase of 1.7 times year-on-year; plug-in hybrid vehicles were sold 522,000 units, an increase of 1.4 times; and the sales of fuel cell vehicles were 0.1 million units, an increase of 16.0% year-on-year. The market penetration rate of new energy vehicles in November was 17.8%, of which the market penetration rate of new energy passenger vehicles reached 19.5%.

Source: China Association of Automobile Manufacturers

Finally, the category of new energy vehicles in China's market will still be dominated by pure electric vehicles in the near future, supplemented by plug-in hybrid vehicles, and a small number of extended-range hybrid vehicles and hydrogen energy vehicles. The chart below shows the significant difference in the payout performance of the pure electric and plug-in hybrid businesses after the comprehensive reform.

Data source: Historical application data of New Energy Vehicle Solutions

In new energy vehicles, the battery is the basic energy and power source, the drive motor converts this on-board energy into driving power, and the electronic control system controls and monitors the operation and component status of the vehicle, referred to as the "three electricity" system of the new energy vehicle. The power battery system is usually composed of the following parts: battery part, battery management system, high and low voltage wiring harness, thermal management part and structural parts. The core part of the power battery system is the power battery. At present, the mainstream power battery on the market, according to the different cathode materials, can be divided into lithium iron phosphate, ternary materials, and lithium manganate, which is gradually eliminated due to too short cycle life. Of course, the development of power battery technology is changing rapidly, Tesla's introduction of electrodeless ear and dry electrode technology 4860 battery and Toyota's solid-state battery, although it has not yet been installed on a large scale, are worth looking forward to.

The drive motor of new energy vehicles mainly includes three categories: DC motor, AC motor and switched reluctance motor, of which the motors that are widely used in the field of passenger cars and commercial vehicles include DC (brushless) motors, AC induction (asynchronous) motors, permanent magnet synchronous motors, switched reluctance motors, etc. The motors used in today's new energy vehicles are mainly AC induction motors and permanent magnet synchronous motors. Among them, The Japanese and Korean car series currently use permanent magnet motors, the speed range and efficiency are relatively high, but the use of expensive system permanent magnet material NdFeB; European and American car series mostly use AC induction motors, mainly for the lack of rare earth resources, as well as the consideration of reducing motor costs. The disadvantages are mainly the small speed range, low efficiency, and the need for a higher performance governor to match the performance.

The new energy vehicle electronic control system is a device that controls the automobile drive motor, and the new energy vehicle electronic control system can be divided into the main controller and the auxiliary controller:

1) Main controller: control the drive motor of the car, that is, by receiving the control information transmitted by the vehicle controller and the brake pedal, accelerator pedal, shift mechanism and other control mechanisms, the motor torque, speed and steering of the driving motor are controlled, and the voltage and current output of the power battery can be controlled accordingly;

2) Auxiliary controller: Controls the power steering pump motor, air conditioning motor, and BSG (all-in-one machine that uses belt drive to take into account both start-up and power generation) motor.

Inverters, drives and controllers are the core components of the electronic control system.

In summary, although new energy vehicles have "three electricity" systems, different brands have their own different battery types, motor types and electronic control systems. Therefore, on the basis of understanding its technical principles, mature multi-party data collection and standardized processing capabilities are required to lay the foundation for refining valuable analysis results.

2

Integration and processing of data from new energy vehicles

New energy vehicle data collection

Traditional fuel vehicles, customers can regularly inspect the vehicle on a daily basis, and when a fault occurs, go to a professional maintenance service agency for maintenance. However, the new "handicraft" of new energy vehicles has the characteristics of high integration of spare parts, high electronics, especially the high complexity of the three-electric system. If insurance companies lack sufficient historical compensation data, fail to effectively introduce new factors for risk identification, or simply apply the traditional fuel vehicle risk model, it will lead to prudent underwriting, non-underwriting, or resource misallocation underwriting, resulting in loss of market share or underwriting losses. Focusing on new energy vehicles, Jingli Lianxun has a variety of compliance data sources, as a partner, to help insurance companies achieve the dual goals of development and profitability.

Standardization of new energy vehicle data

With the help of the world's leading big data technology and product concept, Jingli Lianxun has been honored to become a long-term partner of 99% of auto insurance companies in the Chinese market, with rich experience and high-quality service level. In accordance with the requirements of model related standards and vehicle insurance business specifications, the model standard information database of Jingli Lianxun has formed a proprietary model data product after the construction of the standardization system, including coding, parameters, classification, price information, etc., which are widely used by various car insurance companies in the underwriting, underwriting and claims process in the business process of car insurance. The database covers passenger cars, commercial vehicles, new energy vehicles, ADAS and other fields, with more than 350,000 model data, supporting automatic update of new car data.

Under the national policy to vigorously support the rapid development of new energy vehicles, new energy spare parts manufacturers have also mushroomed rapidly, and the manufacturing level of various manufacturers is uneven, resulting in different quality levels of new energy vehicle parts on the market, and the important components of new energy vehicles, such as batteries, electronic controls, motors and other data play a decisive role in the underwriting pricing of new vehicles. How to standardize the dynamic data generated with the commissioning of new cars, such as driving behavior data, mileage, battery safety, charging facilities, etc., and how to apply it to the auto insurance industry will also become a problem that insurance companies need to consider.

With the promulgation of the "Exclusive Clauses for Commercial Insurance for New Energy Vehicles (Trial)", On the basis of the exclusive data of new energy and the traditional data of models, vehicles and vulnerable spare parts information data, Jingli Lianxun uses the internationally leading multi-data standardization and consistency processing capabilities to lay a solid data foundation for insurance companies to achieve intelligent decision-making in the marketing, underwriting and pricing of new energy vehicles. The following figure shows an example of the standardized processing of battery type data.

3

The compensation risk of new energy vehicles after comprehensive reform is subdivided

In line with the trend of refined risk management in the industry after the comprehensive reform, Jingli Lianxun made in-depth research and quantitative analysis on the impact of dynamic and static information of new energy vehicles on the underwriting risks of the comprehensive reform of the automobile insurance industry.

Some traditional slave vehicle variables still have a strong explanatory effect on the risks of new energy vehicles

Insurers' existing pricing models are generally based on underwriting claims data from historical fuel vehicles. The traditional slave car factor covers various physical properties of the vehicle. For example, the larger and heavier the vehicle, the higher the difficulty of braking; the longer the body, the larger the blind spot area; the larger the zero-to-whole ratio, the higher the claim cost. These traditional factors are equally applicable to both new energy vehicles and fuel vehicles. Below we have selected 3 traditional slave factors to show. We found that both the number of seats, the total mass, and the front wheelbase have a good ability to distinguish the payout rate of new energy vehicles.

Of course, the physical structure of new energy vehicles, especially pure electric vehicles and fuel vehicles, is fundamentally different. The physical properties and spare parts price information of various types of batteries, motors, and electronic controls can better portray the risks of new energy vehicles. Only by combining the traditional slave factor, the static and dynamic factors of new energy can we achieve better results. Next, we will delve into the underwriting risk factors unique to new energy vehicles.

New energy vehicle underwriting risk factor

Static information:

The difference between the physical structure of new energy vehicles and fuel vehicles is obvious. But if the focus is on comparing new energy vehicles. We found that different "three-electric systems" will have different payout differences. The following is an example of a one-factor analysis conducted by Jingli Lianxun combined with the physical characteristics and insurance data of some new energy vehicles.

Battery risk factor

From the perspective of development trends, pure electric vehicles will dominate China's new energy vehicle market in the future. There are many types of batteries for pure electric vehicles and the positive and negative electrode materials used are also diverse, such as: multi-component composite lithium, nickel cobalt manganese oxide, ternary materials, lithium iron phosphate and so on. The following figure proves through practical data that the car insurance compensation using multi-compound lithium and nickel-cobalt lithium manganese oxide materials as assembly battery materials is lower than the industry average.

Data analysis shows that the greater the battery quality, the greater the risk.

The analysis shows that in the classification of battery thermal management cooling devices, "direct cooling" is 40% higher than "free cooling" and air cooling designs.

In addition, the battery price difference also has a particularly significant difference in the risk of compensation, the data shows that from group 1 to group 5, as the average price of batteries rises, the risk also shows an upward trend.

The first year of the new energy vehicle retention rate is seriously damaged, and the second-hand car retention rate is low, and its average retention rate is about 15% lower than that of fuel vehicles, mainly due to battery performance attenuation.

At the same time, similar to the analysis results of the main components of the fuel vehicle, the zero-to-integer ratio difference in battery prices also has a significant difference in the loss risk, and the data shows that from group 1 to group 4, as the zero-to-integer ratio rises, the risk also shows an upward trend.

Motor risk factor

The types and efficiency of motors that keep pace with battery technology also affect the underwriting risks of new energy vehicles, and data analysis shows that the prices of different motors directly affect the results of car insurance claims.

Similar to batteries, the replacement price information of the motor is also a particularly important risk discriminator, and the risk also shows an upward trend as the average replacement price of the motor rises.

The zero-to-integer ratio information of the motor is also a particularly important risk discriminator, that is, from group 1 to group 3, as the ratio rises, the risk also shows an upward trend.

Electronically controlled risk factors

In addition to batteries and motors, the electronic control system in "three electricity" has become an indispensable element in the risk control component of new energy vehicles with the development of science and technology. Data analysis shows that as the price of electronic control systems increases (group 1 to group 4) and the zero-to-piece ratio increases (group 1 to group 5), the car insurance payout ratio also increases.

Dynamic information

On the basis of the difference in the risk interpretation of the static information, the dynamic information after the noise reduction processing of the big data information can add to the risk difference of different vehicles under the model.

Data analysis shows that the longer the average daily mileage, the greater the proportion of night driving time, and the higher the proportion of fast charging times, the higher the frequency of insurance and the higher the loss rate.

Through the multi-dimensional research of static data, dynamic data and dynamic plus static comprehensive data, it is found that the combination of dynamic and static data can maximize the difference in underwriting risk of new energy vehicles under the condition of reasonable information noise reduction. As shown in the figure below, the risk modeling of new energy vehicles is carried out by using static data, dynamic data and dynamic + static data. The risk estimates of 1-10 were divided into 10 groups of the model (the estimated risk was increased from 1 to 10), and the difference in actual risk was 4.2 times, 5.3 times and 6.5 times, respectively.

summary

The development of the new energy automobile industry is in line with the development trend of "electrification, intelligence, networking and sharing" in the future automotive industry, and pure electric vehicles will dominate China's new energy vehicle market in the future. The captive insurance of New Energy Vehicles in China, whether it is based on the difference and pricing of the underwriting risk of the new car based on the traditional physical information of the new vehicle and the exclusive static information of the new energy at the time of leaving the factory, or the use of vehicle dynamic information such as mileage and real-time power consumption to further distinguish the risk, it provides important assistance for the risk segmentation of new energy vehicles and the decision-making of insurance sales.

Only by having a deep understanding and quantification of the risk factors of new energy vehicles can we promote the healthy development of new energy vehicle captive insurance and cultivate and help the benign development of the new energy vehicle industry chain.

END