Reporter 丨 Cui Liwen

Responsible editor 丨 Yang Jing

Editor 丨Zhu Jinbin

"Suffocation, just booked, the premium has risen so much."

In recent days, when talking with friends around me, I learned that I had just booked a Tesla standard endurance model Y in Shanghai, but when I paid for the lock order, I was notified of the docking sales, and the insurance cost increased significantly compared with before.

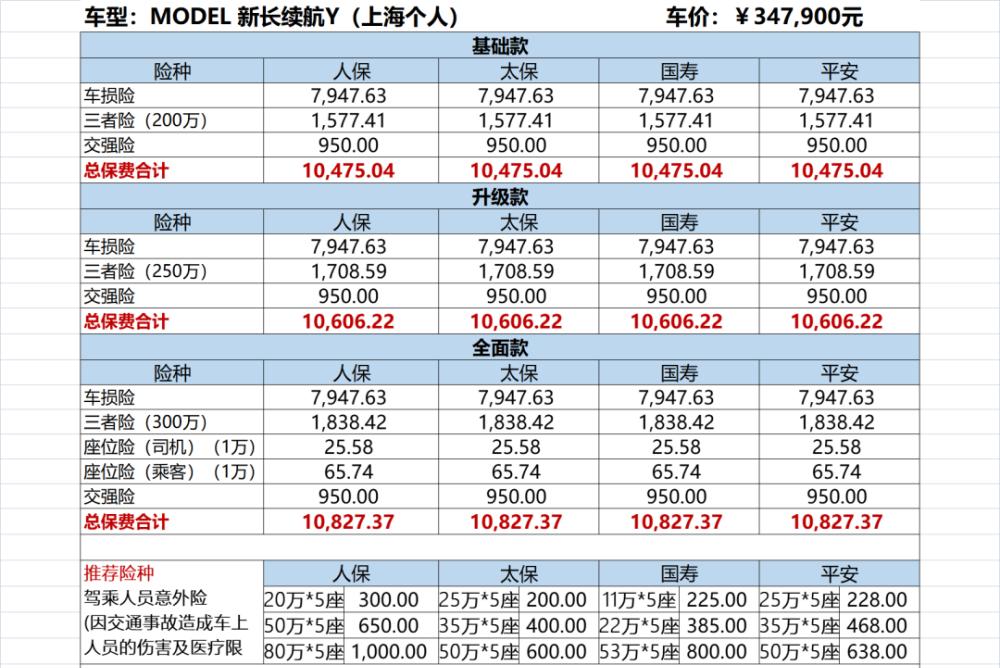

After specific understanding, it was learned that taking the Model Y long-endurance version model with a price of 347900 yuan as an example, the comprehensive premiums provided by Tesla to the four insurance companies selected by the owners of PICC, Taibao, Guoshou and Ping An have been updated to 10827.37 yuan.

Seeing this, there will inevitably be onlookers who will question: Suddenly raising the premium, does Tesla want to harvest the user's "leeks" by selling insurance?

This time, the answer is no. Although the AMERICAN new energy vehicle company is located in the Chinese market and unswervingly adopts a direct sales model, due to the restrictions of industry rules, it has to seek the help of the above insurance companies like other brands in the car insurance business. Therefore, even if the premium rises, the direct beneficiary is not Tesla itself.

So, I can't help but ask, what exactly gave birth to such a phenomenon? On December 27, Beijing time, the official launch of new energy vehicle captive insurance seems to have become a direct cause.

Probably, it's not a bad thing

In fact, as early as the middle of this month, the China Insurance Industry Association issued a notice on its official website of the "Exclusive Clauses of New Energy Vehicle Commercial Insurance of the China Insurance Industry Association (Trial)". At this point, the car insurance corresponding to traditional fuel vehicles and new energy vehicles has been completely separated.

It is undeniable that with the introduction of "new insurance", it is undoubtedly very beneficial for all new energy vehicle owners. After all, according to statistics released by the Ministry of Public Security, as of June 2021, the number of new energy vehicles in the country reached 6.03 million, and it is still expanding.

But the previous crux of the matter was that the Model Clauses for Motor Vehicle Commercial Insurance of the China Insurance Industry Association (2020 Edition) followed by car owners were actually "not friendly" to them.

In the clause, in order to reduce costs, insurance companies often exclude the exclusive parts and energy replenishment methods of new energy vehicles such as power batteries and charging piles from the scope of compensation.

From the perspective of the exclusive insurance for new energy vehicles that has been officially released, the clause not only provides protection for the "three electricity" system, but also covers the use scenarios of new energy vehicles driving, parking, charging and operation, including a total of 3 main insurance and 13 additional insurance.

The main insurance includes three independent types of insurance, including new energy vehicle loss insurance, new energy vehicle third-party liability insurance, and new energy vehicle occupant liability insurance, and the insured can choose to insure all the insurance types or some of them. The insurer shall bear the insurance liability separately according to the type of insurance in accordance with the provisions of the insurance contract.

Additional insurance includes 13 items, additional insurance for traditional cars, new energy vehicles can be insured as long as the conditions are met, including additional absolute deductible rate special clauses, additional wheel loss insurance, additional body scratch loss insurance, additional medical expenses liability insurance outside medical insurance, etc.

In addition, for the indispensable "supporting facilities" of new energy vehicles such as charging piles, the exclusive clause also designs additional external grid fault loss insurance, additional self-use charging pile loss insurance, additional self-use charging pile liability insurance, and additional special clauses for value-added services for new energy vehicles.

It is clear that the pain points that were once partially criticized have been successfully solved.

At the same time, it was learned from the Shanghai Insurance Exchange that the new energy vehicle insurance trading platform has been officially launched, and the first batch of new energy vehicle exclusive insurance products of 12 property insurance companies have been listed.

The 12 property insurance companies are Chinese Insurance, Sunshine Property & Casualty, China Insurance, Chinese Life, Dadi Insurance, Ping An Property & Casualty, CPIC Property & Casualty, Taiping Property & Casualty, Tianan Property & Casualty, Zhongcheng Insurance, Asia Pacific Property & Casualty, and Samsung Property & Casualty.

At present, the trading platform has issued a standard interface and completed the docking line with the first batch of institutions such as PICC Property & Casualty, Ping An Property & Casualty, and CPIC Property & Casualty, and is expected to cover more than 90% of the market share.

In terms of price that end consumers are most concerned about, the benchmark premiums of the three insurances and car damage insurance of new energy vehicles have dropped by about 0.8% compared with the current benchmark premiums of traditional car insurance.

Among them, the benchmark premium of the three insurances fell by 0.1%, and the benchmark premium of the car damage insurance fell by 1.2%. According to the "Explanation on the Adjustment of the Pure Risk Premium Table of the Benchmark Pure Risk Premium Table for Exclusive Products of New Energy Vehicle Commercial Insurance" previously issued by the China Association of Actuaries, the car damage insurance for new energy vehicles with a price of less than 250,000 yuan does not increase the fee, and the threshold for the increase and decrease of the rate is narrowed.

In other words, the new energy vehicle models below 250,000 yuan only fell and did not rise, and the models above 250,000 yuan rose partially, and the overall maintenance was within an acceptable controllable range.

As for the other dimensions of tesla model Y's substantial increase in premiums mentioned at the beginning of the article, after consulting with insurance industry professionals, it is more that insurance companies are in order to share costs and ensure profitability.

"The premium of new energy vehicles is basically the same as before, but the premium of more than 300,000 yuan has increased slightly." And taking PICC as an example, it is also necessary to look at a comprehensive score of this model in the PICC system, it is possible that this person has a high insurance score (the insurance is due at the end of this month, and it is insured at the end of the month), so that the system will control (the insurance company will adjust the control in the last few days at the end of the month according to the amount of the month), the preferential coefficient will be adjusted accordingly, and the premium will increase together. ”

However, with the introduction of new energy vehicle captive insurance, from the perspective of users, the car purchase budget is still inevitably fluctuating, and the annual cost of using the car will rise accordingly. But from the perspective of safety and practicality, it is not a bad thing after all.

Endgame, or self-employment?

It must be admitted that by never following the rules, anything can subvert innovation, overturn and start again, and be firmly engraved in the DNA of Tesla as a company. Every operation link pursues the ultimate cost control and efficiency. It is also based on this background that once it is found that the final stage of achievement is not as expected, a rapid adjustment will come as expected.

At the same time, after years of development in the automotive industry, the entire car purchase process faced by consumers has become a stereotype. OEMs, distributors, insurance companies, all of them are performing their duties according to their fixed roles.

However, in Tesla's eyes, so many participants docking each other will inevitably cause corresponding delays and waste of resources, and even the profits they can make will be reduced accordingly. Obviously, such a situation does not conform to the logic of its development. Eventually, disruption and change followed.

If it is said that since the first mass-produced model Model S was put on sale, it has been adhering to the direct operation model, proving that Tesla can fully assume the "drama" of dealers, then from the various measures it has shown this year, its long-cherished wish to also want to include the business of insurance companies has become a reality.

In the past October, Musk has said on his personal social platform: "Tesla car insurance will be launched in Texas this week, and hope that tesla insurance will be available in most parts of the United States next year." "Tesla Motor Insurance provides owners with more comprehensive insurance and claims management services, and the price is cheaper, with discounts of up to 20-30%. ”

What can differentiate it from traditional insurance companies is that according to the premium calculation method, Tesla launched UBI car insurance, that is, car insurance based on the user's real-time driving behavior.

For example, the frequency of the driver's sharp braking and the distance from the car in front of it can be collected in real time through Tesla's in-car sensors, which scores the driver's safety factor and formulates the most reasonable premium amount, that is, the "thousands of people" premium personalized customization model.

According to Tesla officials, the average car owner can save about 20% to 40% of the premium, and the driver with the safest driving behavior can save 30% to 60%.

Taking this approach is undoubtedly fairer to car owners, and at the same time, it can obtain more profits and positive cash flow, thus feeding back the car manufacturing sector. In other words, this time Tesla will use technology and big data to subvert the traditional insurance industry.

Therefore, when the domestic new energy vehicle captive insurance is officially launched, there is always a feeling: at a certain node in the future, Tesla will abandon the assistance of these companies and operate its own insurance business.

After all, it is facing a huge and attractive "cake".

From the relevant data, the total number of new energy vehicles in 2021 will reach 7.23 million, calculated with an average premium of 6,000 yuan per vehicle, then, the annual new energy vehicle insurance market size will reach about 43.4 billion yuan. As the world's largest and most important new energy vehicle market, China's auto insurance market will reach trillions in the near future.

Because of this, Tesla has been located in China on August 6 this year, has been located in the country formally established insurance brokerage co., LTD., the registered capital of 50 million yuan, the legal representative is Tesla global vice president, Greater China head Zhu Xiaotong, the scope of business for insurance brokerage business.

The company's registered address is: the second floor of No. 5000 Jiangshan Road, Lingang New Area, China (Shanghai) Pilot Free Trade Zone, where Tesla's Shanghai Gigafactory is located, and is 100% owned by Tesla Motors Hong Kong Co., Ltd.

Obviously, this American car company is ready to further "harvest" in the insurance market. And this also makes us start to wake up to the fact that for many capable new energy vehicle companies in China, perhaps the realization of insurance business self-operation will be a path where the advantages outweigh the disadvantages.