Text | Zheng Cancheng, Zhou Youhui

Edit | Peng Xiaoqiu

Suzhou Nanoxin Micro (688052. SH) will be listed on the Star Market today at a price of 230 yuan per share, which will also become the focus of market discussion.

On the one hand, the new gains are worrying. So far this year, 20 of the 37 companies listed on the Star Market have broken, accounting for more than half. Last week, the new stocks on the science and technology innovation board once again refreshed the lower limit. Weijie Chuangxin closed down 36% on the first day of listing, and the other two new stocks closed down nearly 30% and 23% on the first day of listing, respectively. On April 19, Jingwei Hengrun broke, and the sponsor CITIC Securities lost 80 million yuan a day, compared with the first day of The Yingji Core closed down less than 10%, which is already a good result.

On the other hand, Nanochip micro intends to raise only 750 million, and the announcement shows that Nanochip micro is expected to raise 5.8 billion yuan, exceeding 5 billion yuan. This amount is undoubtedly another challenge for Nanochip. According to the results of the offering, the amount of abandonment was 778 million yuan, accounting for 13.38%, and the amount of abandonment and the proportion of abandonment ranked first in A shares.

Nanochip Micro's main business revolves around signal chain chips. Depending on whether the processing signal is an analog signal or a digital signal, the chip can be divided into two types: analog chip and digital chip. Among them, analog chips can be further divided into three categories: RF chips, power management chips and signal chain chips.

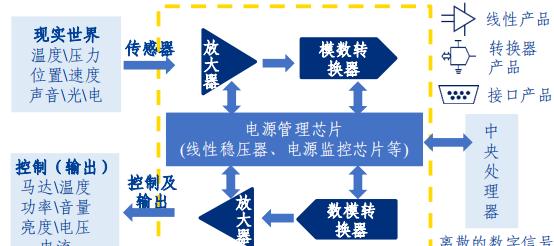

Most of the signals in the real world, such as temperature, pressure, sound, etc. are analog signals, and the role of the signal chain chip is to convert the physical quantities of the real world into understandable digital signals in the digital world.

(Source: Changjiang Securities Research Institute)

Different from digital chips, analog chip design is more complex, which also determines that the advanced level of analog chips depends to a large extent on the accumulation of experience in research and development. China started late in this field, none of the world's top ten analog chip companies are Chinese enterprises, and the two analog chip leaders TI and ADI occupy 19% and 9% of the market respectively.

(Data source: IC Insights, Nanochip Micro Prospectus)

According to IC insights, the global analog chip market is about $50 billion, and China accounts for half of the demand. Changes in the external environment have reshuffled the chip industry. As one of the enterprises, Nanochip Micro superimposed the outbreak of downstream applications, and its performance showed exponential growth.

From 2018 to 2021, the operating income of Nanocore Micro was 40.2233 million yuan, 92.1032 million yuan, 242 million yuan and 862 million yuan respectively, and the deducted non-net profit was 2.0184 million yuan, 6.7081 million yuan, 40.4928 million yuan and 216 million yuan.

(Data source: Nanocore Micro Announcement, 36Kr Drawing)

So, what changes have taken place in the downstream market? How does Nanochip micro grasp it? Is its 107 times price-to-earnings ratio a bubble sought after by the market or is it an investor's recognition of Nanocore? 36Kr will answer these questions from the development history of Nanocore micro and the capital operation in it.

Start with sensor supporting chips, layout automotive, industrial fields

From 2013 to 2017, although the overall revenue of nanocore micro showed an increase, the growth rate was getting lower and lower, and in 2017, due to the downstream expansion was less than expected, the revenue scale only expanded by about 2%.

(Data source: Nanocore Micro Transfer Manual, Nanocore Micro Annual Report, 36Kr Drawing)

The controlling shareholders and actual controllers of Naxin Micro are Wang Shengyang, Sheng Yun and Wang Yifeng. Among them, Wang Shengyang, the founder of Nanochip, graduated from Peking University with a master's degree in electronic and communication engineering, and joined ADI, the world's second-ranked analog chip manufacturer, as a design engineer after graduation. In May 2013, Wang Shengyang pulled his former colleague Sheng Yun to jointly establish Naxin Micro.

In September of the same year, Wang Shengyangla University classmate Wang Yifeng joined the company and transferred the registered capital of 15,000 yuan belonging to Wang Shengyang and Shengyun to Wang Yifeng at a parity. When Naxin Micro's new third board was listed, Wang Yifeng served as the secretary of the board of directors of Naxin Micro.

At the beginning of its establishment, Nanocore Micro focused on the signal conditioning ASIC chip, which is a supporting product for sensor-sensitive components, and the product of the combination of the two is the sensor.

Sensor-sensitive elements are capable of capturing weak analog signals in the real world, but these signals are generally not directly used in electronic devices and are subject to greater external influences. The signal conditioning chip assumes the role of intermediary, further processing the weak signal and converting it into a signal that the electronic device can process.

Based on the physical quantities measured by the sensors, Nanochip's products can be further subdivided. For example, the main business of Nanochip at that time was acceleration ASIC chips, the main role is to obtain the acceleration of the device, determine whether the electronic device has accidentally fallen, and start the self-protection mechanism of the device in a timely manner, mainly for consumer electronics products such as smart phones and wearable devices.

The first bucket of gold earned by Nanochip micro came from the downstream sensor company - Suzhou Minghao, which is the holding company of Suzhou Gutech, an A-share listed company. In 2011, Suzhou Gutech acquired the American Octavia Optoelectronics, officially cut into the field of high-end sensors, at that time Suzhou Minghao's acceleration sensor products, is the supporting nano-core micro-signal conditioning ASIC chip. At the same time, in order to expand the sales of such sensors in China, Suzhou Gutech invested 7 million yuan to set up Suzhou Minghao, and then increased its capital by 10 million yuan.

In 2014, Nanocore achieved sales revenue of 7.9 million yuan, of which Suzhou Minghao accounted for 6.8 million yuan, accounting for more than 80% of the proportion. In the following three years, Suzhou Minghao accounted for more than half of the sales revenue of Nanocore Micro.

With the continuous development of Nanochip micro and the expansion of more new customers, the dependence on Suzhou Minghao is getting smaller and smaller, and the scale of revenue is also showing an increasing trend. In 2015, the operating income doubled, the operating income reached 18 million yuan, and the proportion of Suzhou Ming hao decreased to 61%. In order to make the signal conditioning ASIC chip products better cooperate with sensitive components, Wang Shengyang recruited a senior marketing manager in Suzhou Minghao as the technical marketing manager of Nanochip Micro. Later, this early employee rose all the way to the director of the sensor product line of Nanocore.

(Data source: Nanocore Micro Transfer Manual, Nanocore Micro Annual Report, 36Kr Drawing)

In 2016, the development of Nanocore Micro is still rapid, achieving operating income of nearly 30 million yuan and net profit of more than 10 million yuan. But macroscopically, business in the consumer electronics sector is not easy to do. Due to the low barrier to entry, the homogenization competition of enterprises has become more and more intense. At this time, the demand in the industrial and automotive fields began to enter Wang Shengyang's vision, compared with the consumer electronics field, the industrial and automotive fields have higher requirements for the performance and reliability of chips, which also means that higher requirements are put forward for technology.

For example, one of the applications in the automotive sector is engine inlet pressure detection. Nanocore micro invested in ceramic capacitive pressure sensor manufacturer Xiangyang Zhenxin 3.7 million yuan, research and development of a conditioning chip suitable for Xiangyang Zhenxin pressure sensor, forming a pressure sensor solution. In 2017, Nanocore micro invested an additional 300,000 yuan, and the shareholding ratio rose to about 20%.

The new business line of Nanochip entered a painful period in 2017, which showed that the operating income had hardly changed from the previous year, and the net profit shrank by more than 40%. The reason is that from the perspective of the downstream application market, although the industrial and automotive fields have been opened up, the development of new products in these areas has greatly increased the cost.

In addition, revenue in the consumer electronics sector fell short of expectations. The main reason is that the smartphone market has begun to "roll in", and IDC data shows that global smartphone shipments fell for the first time in 2017.

From the front end to open up the second battlefield, won huawei, Huichuan two major customers

From the perspective of the development logic of the chip market, the needs of downstream customers are not limited to signal perception, but also in the field of isolation and interface chips for system interconnection, and power-driven drivers and sampling chips.

This is because after the real-world analog signals are preprocessed into digital signals, they need to be further processed with isolation and interface chips. Electronic devices require high voltages when running, and for safety reasons, manually operated parts require low voltages, and digital isolation chips assume the function of isolating high and low voltages.

(Source: Nanocore Micro Prospectus)

Further, after the preprocessed signal reaches the MCU (micro-control unit), it is also necessary to drive the chip to amplify the signal and then deliver it to the power device; the parameters of the power device need to be sampled by the chip to sample and feedback to the MCU.

Based on the accumulation of ASIC chips in signal conditioning, nanochip micro, which sees market changes, is beginning to seek a second growth curve for the business. This attempt is to extend the sensitive components with the signal conditioning ASIC chip to the front end, introduce the integrated sensor chip, and extend the isolation and interface chip to the back end.

The success of the sales of isolation and interface chips is inseparable from Huawei.

In 2018, Nanochip's isolation and interface chips entered Huawei's supply chain, achieving a small amount of sales revenue. In the middle of the following year, due to external reasons, the switch had to be made to domestic suppliers. As a result, Naxin Micro has changed from Huawei's three supplies to an exclusive supplier, and in 2019, the amount of Huawei's procurement from Naxin Micro exceeded 26 million yuan.

On the one hand, the construction of 5G base stations has led to a significant increase in Huawei's demand for such chips, and on the other hand, external factors have continued to deteriorate, resulting in limited procurement. In 2020, Huawei's purchase amount from Nanochip reached 55 million yuan.

More notably, in 2018 and 2019, Huawei still purchased chips from Nanochip micro through distributors Amerstone and Avnet Hong Kong, and in 2020, Naxin micro "turned positive", and sales to Huawei changed from distribution to direct sales. Until Q4 2020, due to changes in the operating environment, Huawei announced that it would suspend the purchase of chips from Nanocore Micro, and has not yet resumed procurement.

However, this news did not hit Nanochip. Because instead of selling goods to Huawei, it is more important to have been recognized by Huawei, which means that the products have been recognized by the most discerning suppliers in the field in China, and when they enter Huawei's supply chain, other suppliers will follow.

In 2020, the operating income of Nanocore Micro reached 242 million yuan. The surge in revenue made Naxin Micro take a bigger step towards the automotive field, choosing to spend nearly 40 million yuan in August of that year to acquire a 56.49% stake in holding company Xiangyang Zhenxin (valued at 60 million yuan). Superimposed on the early investment, Naxin micro accounted for 76% of the shares, and obtained the control of Xiangyang Zhenxin.

Selling products to Huawei is just a microcosm of Nanocore's micro-strategy, in fact, its products extended in front of and behind the back end have opened up the market in multiple lines. In Q3 2020, nanochip's third curve drive and sampling chips were shipped in batches, and the performance began to be gradually released. In 2021, the sales revenue of only the drive and sampling chip reached 264 million yuan, exceeding the sales revenue of the whole year of 2020.

(Source: Nanocore Micro Prospectus, 36Kr Chart)

Looking at Sriepu, which also focuses on analog chips, in 2019 and 2020, under the wave of localization substitution, Huawei, as the largest customer in two years, achieved sales revenue of about 170 million yuan and 310 million yuan respectively. In 2021, Huawei also suspended the purchase of Sripu, but Sripu also has high-quality customers such as Samsung and Mitsubishi Elevator, and more than 400 new trading customers will be added in 2021. Operating income still rose from 570 million to 1.33 billion, an increase of more than 130%. This confirms the competitive logic of the chip market from the side.

However, compared with the horizontal expansion of Sripu, Naxin Micro's playing style is more vertical. From the perspective of market size, according to IC Insights data, the global signal chain chip market size is about 10 billion US dollars in 2020, and the power management chip market size is about 30 billion US dollars. While the signal chain chip and power management chip technology have their similarities, Sripu has chosen to enter the larger market power management chip market. After the listing, power management chips have begun to take shape, accounting for 2%. In 2021, this proportion jumped to 22.49%, and the sales revenue was close to 300 million, which has exceeded the sales revenue of Nanochip in 2021.

The development route chosen by Nanochip Micro is to make the signal chain chip "fine". IDC predicts that from 2021 to 2025, the market demand in the automotive sector will grow at a growth rate of 13.2%, which is 4.5% in the industrial sector but only 2.1% in the communication sector. Although from the existing proportion, the communication field occupies one-third of the market, but from the perspective of growth, analog chips need to grasp the industrial and automotive fields, and the vehicle-grade chips have the highest requirements for chips, which is the long-term pursuit of quality goals in the chip field.

At present, nano-core micro's vehicle-grade chips have entered the domestic first-line automobile manufacturers. The revenue contribution of the automotive sector will account for about 13% in 2018-2020, and the revenue scale and total revenue growth will be basically the same, with a compound growth rate of more than 230%.

The benchmark customer in the industrial field is Huichuan Technology. Nanochip's products have been verified by Huichuan technology testing and will start mass production and delivery in 2020. In addition to the old customer Suzhou Minghao, Wuxi Weigan also landed on the list of the top five customers of Nanochip Micro in 2021 H1 and officially entered the Supply System of Weier shares.

The valuation tripled in half a year, and the actual controller cashed out to buy a house

The valuation of Naxin Micro has soared, bringing huge investment returns to the capital behind it.

The earliest external investor was Guorun Ruiqi. Behind it is also Suzhou Gutechnium, accounting for 10%. In 2013, it invested 3.45 million yuan in Nanochip Micro, accounting for 49%. With the continuous financing of Naxin Micro, the old shareholder Guorun Ruiqi has cashed out wildly, the amount has exceeded 40 million yuan, as of the listing, it holds 8.6274 million shares, accounting for 8.54% after listing.

Even with reference to the transfer price of the last financing before the listing of 27.27 yuan / share, the shares held by Guorun Ruiqi can cash out 230 million yuan, that is, 80 times the investment income; if calculated at the issue price of 230 yuan / share, the market value of the shares held by Guorun Ruiqi is about 2 billion.

In September 2018, Qufu Tianbo entered the market, and the microvaluation of Naxin reached 300 million yuan, and the valuation of 300 million yuan continued until February 2019, which was the slowest period of valuation growth.

On May 16, 2019, changes in the external environment made localization substitution quickly become an investment hotspot. In November 2019, Qian multiplication Capital subscribed for 347,000 shares at a price of 72 yuan per share, and it was estimated that Qianzao Capital invested about 25 million yuan in this round, accounting for 4.82%, and the microvaluation of Nanocore exceeded 500 million yuan.

(Source: Nanocore Micro Prospectus)

The continuous influx of peripheral capital in a short period of time makes Nanocore micro more and more expensive. Only a month later, the old shareholder Guorun Ruiqi sold part of the shares, and the transfer price rose to 77.50 yuan / share.

This speed is far from enough, in May 2020, Naxin micro opened a new round of financing, Thousand Multiplier Capital added 10 million yuan of investment, at this time the transfer price came to 194 yuan / share, the valuation came to 1.5 billion yuan, compared with half a year ago the valuation has doubled 3 times; after another month, the transfer price to 200 yuan / share.

Huawei and Huichuan Technology entered the game in September 2020, with an investment of 40 million yuan and 15 million yuan respectively.

It is worth noting that in May 2019, Huawei Hubble had subscribed for 6% of the equity of Siriphol at a price of 72 million yuan, and it is estimated that the valuation has reached 1.2 billion yuan, and in 2020, Hubble will reduce its holdings, according to the stock price at that time, the income on Sreip has reached 36 times. In December of the same year, Siripu doubled its valuation for half a year, and its valuation reached 2.5 billion yuan.

With the help of two rounds of financing in 2020, the controlling shareholder and the actual controller cashed out a total of 93 million yuan. Among them, Wang Shengyang, Sheng Yun and Wang Yifeng cashed out 46 million yuan, 30 million yuan and 17 million yuan respectively. Wang Shengyang and Wang Yifeng used most of them to buy real estate.

In January 2021, Xiaomi Changjiang purchased 696,800 shares at a price of 27.27 yuan per share (corresponding to the price of 245.43 yuan per share before the capital reserve was converted to increase in November 2020), at which point the valuation reached 2 billion yuan.

(Naxin Micro Equity Structure Chart, Source: Nanochip Micro Prospectus)

On the eve of listing, The forecast revenue of Nanochip's 2021Q1 performance forecast was 250 million to 350 million yuan, corresponding to an increase of 84.23% to 157.92% year-on-year. An industry insider also gave the expectation of 1.5 billion yuan in revenue in 2022, and the high performance growth is gradually digesting the valuation of Nanocore.

Nowadays, Nanochip micro-pricing is 230 yuan, high stock price, high valuation superimposed on high underwriting caused by high abandonment, eating nearly 800 million abandoned shares of Everbright Securities, has become the seventh largest shareholder of Nanochip Micro, facing the listing of Nanochip Micro all high-level receivers feel pressure.

(Source: Nanochip Micro Listing Announcement)

Endnotes:

[1] The full name of ASIC is Application Specific Integrated Circuit, that is, an application-specific integrated circuit.