Wen | Dong Jie Editor| Qiao Qian

When the global stock market was wailing, JD.com resisted the pressure and sent a mixed four-quarter report.

According to the financial report, JD.com achieved a net income of 275.9 billion yuan in the fourth quarter, an increase of 23.0% year-on-year, and in the fourth quarter of the overall consumption downturn, the growth rate exceeded the consensus expectations of the outside world. In contrast, Ali's revenue growth rate in the fourth quarter was only 10%, while the growth rate of the online retail market in the whole society was only 8% in the fourth quarter.

Perhaps due to the geopolitical situation, the Fed's interest rate hikes and other multiple impacts, once the earnings report was released, the pre-market share price of JD.com's US stocks fell by more than 15% (as of this morning's close, down 15.83%), and the net loss of 5.2 billion yuan in the fourth quarter was considered to be the culprit. However, in detail, the operating loss of JD.com in the fourth quarter was only 390 million yuan, although it was slightly lower than the profit of 590 million yuan in the same period last year, but this was recorded under the premise that JD.com continued to increase investment in logistics and supply chain.

Excluding equity incentives, depreciation and amortization, and related fair value gains and losses, JD.com's operating profit under Non-GAAP reached RMB2.8 billion, far better than last year's RMB1.2 billion, which also proves jd.com's resilience to pressure to some extent.

Another point is worthy of surprise, in the financial report, JD.com revealed that its GMV for the whole year of 2021 was 3.29 trillion yuan, an increase of 26.2% year-on-year, which not only exceeded the growth rate of revenue, but also exceeded the growth rate of GMV of 25.7% in 2020. Under the strong impact of Douyin (according to people familiar with the matter, the GMV of Douyin e-commerce in 2021 under the wide caliber has reached trillions) and Kuaishou live e-commerce, JD.com's GMV growth rate has not only not declined sharply, but has made steady progress.

The stable performance has also made JD.com's stock price perform "steady" in the mournful stock market. According to Wind data, JD.com's stock price fell only about 20% last year, while Ali and Pinduoduo fell by about 50% and 70% respectively.

But there are also hidden worries. In the past few quarters, the rapid growth of new users and POP business are stalling in this quarter, and the outside world originally hoped that Jingdong could benefit from the "two choices" after the lifting, but in just a few quarters, the "dividend" began to disappear, which was inevitable to worry.

Self-operated flag carrying, POP stall

Dismantle in detail the four seasons of JD.com:

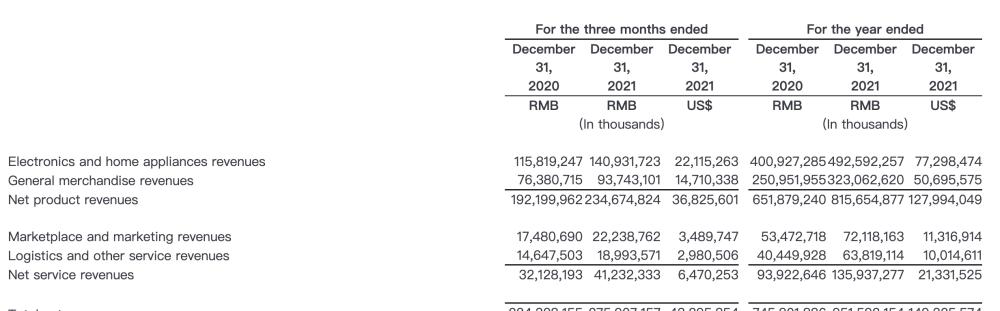

In the fourth quarter, Jingdong's commodity sales revenue reached 192.19 billion, an increase of 22.1% year-on-year. Among them, the revenue of electronic products and home appliances was 140.93 billion, an increase of 21.6% year-on-year, compared with the growth rate of 18.8% in the third quarter, rebounding significantly. Previously, the market was generally worried that the downturn in the real estate market and the curtailment of electricity and production would bring strong pressure on the sales of home appliances, but from the perspective of actual effects, home appliances performed quite well. In addition, the revenue of daily necessities was 93.74 billion, an increase of 22.7% year-on-year, slightly lower than the 29.4% growth rate in the third quarter.

JD.com's fourth-quarter revenue segmentation

Net service revenue remained stable, with the fourth quarter recording 41.23 billion, up 28.3% year-on-year, of which platform and advertising services revenue was 22.24 billion, up 27.2% year-on-year, and logistics and other services revenue was 18.99 billion, up 29.7% year-on-year. The growth rate of advertising revenue has declined significantly in this quarter, and the figure was 35.2% in the previous quarter.

Subject to the impact of the rise of new platforms on traffic dispersion, the competition for advertisers' budgets has become more intense, and JD.com does not have an advantage in platforms such as Douyin, Kuaishou, and Xiaohongshu, which may be one of the main reasons for the slowdown in advertising revenue.

Despite this, JD.com still far surpassed Ali in two data (revenue from goods and services), whose customer management revenue (advertising expenses and commissions for Taoji e-commerce) in the fourth quarter fell slightly by 1% year-on-year (3% increase in Q3), showing negative growth for the first time.

However, it is undeniable that the weak consumption in the fourth quarter and the price increase in the upstream of the supply chain still affected the growth of JD's POP platform business, which increased by 27% year-on-year in Jingdong's self-operated business in this quarter, and the year-on-year growth rate of POP business slipped below 40%, lower than the 49% growth rate in the previous quarter.

At the earnings report meeting of the previous quarter, Xu Ran, CFO of JD.com, also said that "the growth of pop business has offset the downward trend of revenue growth of 1P business to a certain extent", but in this quarter, the situation has reversed, and the pressure resistance of self-operated business under the economic weakness cycle is quite obvious.

This can also be seen in Ali's recent actions. Not long ago, Ali has opened a Tmall self-operated flagship store, first from the 3C category to promote, which is considered to be a direct benchmark for JD.com's business type. Earlier, Ali disclosed its self-operated business (including Hema and Yintai, etc.) as a separate business item in the financial report, which proved its ambition to develop its own business, and after the platform business encountered policy suppression and growth ceiling, Ali also had to bow its head.

But in the long run, Jingdong's attractiveness to merchants is still getting stronger, and Xu Lei, CEO of Jingdong Group, revealed that more merchants settled in Jingdong in the fourth quarter than in the past three quarters. The minutes of the meeting obtained by 36Kr also show that due to the relatively higher unit price of merchants in JD.com, and the low rate of commissions and other rates drawn by JD.com, the profit margin of merchants in JD.com is the highest among all online platforms.

The earnings data also proves this. In the fourth quarter of the sluggish consumption, JD Retail's operating margin excluding unallocated items reached 2.1%, even better than the 1.9% in the same period last year. What JD.com needs to do is to try to drag this dividend for as long as possible.

New business dilemmas and new logistics issues

If you have to nitpick, the operating loss of 390 million yuan in the quarter, the addition of only 18 million (less than expected) and the stall of the FMCG category are all places that disappointed some investors.

The new business has once again become the main reason for JD.com's losses. In the quarter, JD.com's new business revenue reached 8.21 billion, although it increased by 44% year-on-year, but the loss also reached 3.22 billion, an increase of 230% year-on-year, according to CITIC Securities' estimates, Q3 Jingxi Spelling and Jingxi business single-quarter loss is likely to reach 20-2.5 billion yuan.

In the short term, the loss of new business will continue, especially after the sinking market Jingxi has already played a part of the world, and JD.com can no longer reduce its investment to give up the market to competitors.

Another major culprit in operating losses is overhead. In the quarter, JD.com's expense increased by 89% year-on-year to 3.7 billion, including more than 2.1 billion equity incentives, which is understandable for incentivizing management in such a turbulent environment, but for JD.com, which is a real cost drag for JD.com, which is at a breakeven point.

The new user increase of JD.com in the fourth quarter was also less than expected. Previously, we mentioned that at this year's investor conference, Jingdong had set the goal of "the new volume of annual active buyers to catch up with last year - one hundred million", although the 18 million new users in this quarter barely helped Jingdong complete the goal, but under the premise of double 11 promotion and significant increase in marketing expenses, the growth of the number of users was lower than 20.3 million in the third quarter, which was somewhat disappointing.

But fortunately, the performance of logistics improved in the quarter - achieving revenue of 30.47 billion, an increase of 27.7% year-on-year. Although the growth rate has slowed down, jd.com logistics' profit has finally turned positive to 730 million, with a profit margin of 2.4%, becoming JD.com's "most profitable" business - JD Retail's profit margin in the fourth quarter was 2.1%.

According to 36Kr, the news of JD Logistics's wholly-owned acquisition of Debon is about to be settled, and at the end of 2020, Wang Zhenhui, the former CEO of JD Logistics, who left jd.com, is reported to return to a low-key in the near future, and may take over the integration work after the acquisition of Debon.

Up to now, JD Logistics has covered six major logistics networks: warehousing network, comprehensive transportation network, last-mile distribution network, large-scale network, cold chain network and cross-border network. Among them, the large-scale network has always been the weak link of JD.com. After the completion of this acquisition, Debon's resources on the basis of aviation resources, trunk networks and customers will perfectly supplement jd.com Logistics' supply chain foundation, strengthen its competition in the B-end market, and help continue to extend its business upstream to the supply chain.

More importantly, this will further enhance the external revenue of JD Logistics. JD Logistics executives have said that in 2022, the foreign single business needs to occupy about 50% of JD.com's business, but in 2021, JD Logistics' fully socialized income (not external customer income) accounts for less than 35%, and there is still a lot of room for improvement.

On the whole, this quarter's JD.com in revenue, GMV and other growth rates are higher than the industry expectations, but the growth rate of POP business and the decline in new users is still worrying, as to whether this is short-term or long-term, JD.com needs to give answers in the next few quarters.