Following the release of the financial reports of Tesla, Microsoft and Apple last week, the three members of the trillion club, and the basic smooth landing of all the staff, this week, Google, Meta, and Amazon all appeared. And obviously, this week's battle situation is much more exciting than last week's.

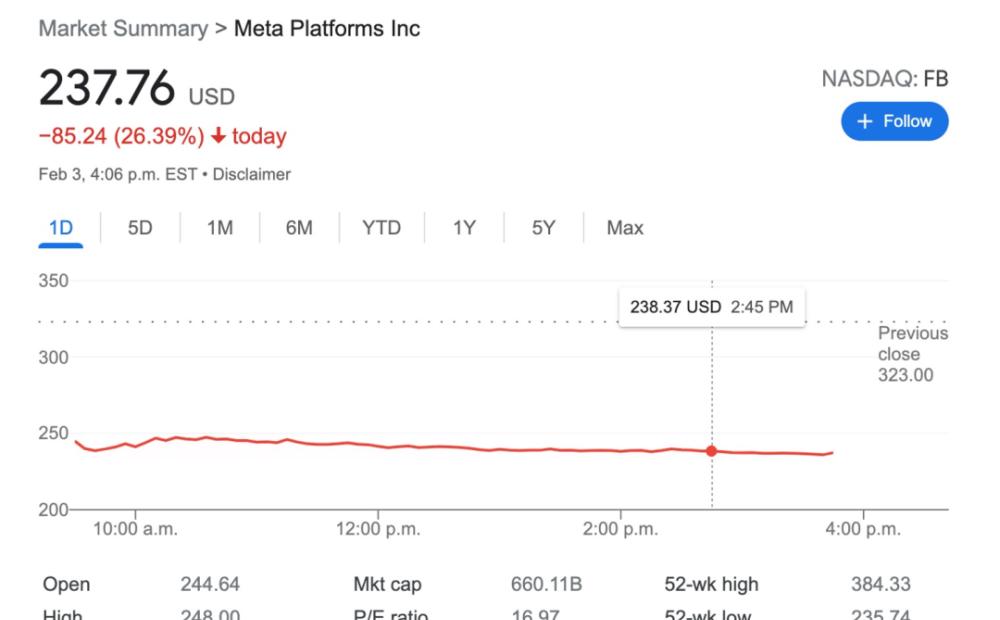

Among them, the most exciting financial report came from Meta. After U.S. stock market hours on Wednesday, Meta released its first earnings report since it changed its name from Facebook last October and fully transformed the meta-universe. The financial report, which was far below market expectations, directly threw a nuclear bomb at The Meta stock price, and after the release of the earnings report, Meta's stock price plunged more than 20% and fell to the trillion club. Today, the decline came even more violently, with Meta plunging more than 26 percent intraday, the biggest drop of the day in the company's 18 years of existence.

Overnight, Meta's nearly $300 billion market cap vanished. What is the concept of $300 billion? It is roughly equivalent to one-third Tesla, one-fourth Amazon, 10 Baidu, and 2 Meituan today.

And a few joys and a few sorrows. Today, under the extremely depressed market sentiment caused by Meta, e-commerce giant Amazon staged a jedi reversal: in the case of an intraday plunge of nearly 8%, it turned the tide with far more than expected financial performance, and the stock price once soared 18%, saving a number of technology stocks from fire and water. In addition, although and Meta are "eating" by advertising, Google's financial report is also unexpectedly good, and the after-hours market value has risen sharply to 2 trillion yuan.

This kind of heaven-into-earth operation of the technology giants directly stunned a large number of melon-eating masses. Since when did the rise and fall of the giants become so exciting?

| the Meta-Century Crash: earnings are full of lightning points, and the road ahead is full of fog

Meta's decline is so huge, I really can't blame the market for being surprised at first, but the problem reflected in the financial report is too obvious and too tricky. Let's first take a look at how "ugly" the data on these big metrics is this season.

Revenue: Revenue for the fourth quarter of 2021 was $33,671 million, up 20% year-over-year and slightly ahead of market expectations of $33.4 billion.

Profit: Net profit for the quarter was $10,285 million, down 8% from a net profit of $11,219 million in the year-ago quarter and the first decline in net profit since the second quarter of 2019.

Net income per share: Earnings per share were $3.67 compared to expectations of $3.84, lower than market expectations.

Active users: 1.93 billion daily active users in the quarter, the market is expected to be 1.95 billion, and the monthly active users are 2.91 billion, with the market expectation of 2.95 billion.

User growth: Only 2 million monthly active users increased in the quarter, with little change from the previous quarter. Last quarter, the platform added 15 million new monthly active users. In addition, the number of daily active users decreased by 1 million, which is also the first quarterly decline in the daily active user indicator since the establishment of the company.

It can be said that from the overall performance point of view, in addition to revenue, the rest of meta's other major indicators are almost all below market expectations. And when you take a closer look at meta's sub-business performance, you'll see that the problems are even bigger.

This quarter is Facebook's first earnings report after changing its name to Meta, and it is also the first time that Meta has conducted revenue statistics based on the advertising revenue of Family of Apps and Reality Labs, both of which are dismal.

Meta revenue by business, picture from Meta financial report

Advertising revenue: user interest shifts, deep in the swamp of various unfavorable factors

While overall revenue from social media including Facebook, Instagram, Whatsapp and Messenger grew significantly during the quarter. But at the earnings report, Meta made it clear that the company is being challenged in terms of the number of ads served and pricing, and expects revenue in the first quarter to be between $27 billion and $29 billion, up 3% to 11% year-on-year, far below the market's expectation of more than $30 billion.

Yahoo Finance data shows that The number of ad impressions in Meta North America fell by 6% year-on-year during the quarter, and the price of each ad increased by 6% year-on-year, much lower than the 22% growth in the third quarter. According to the explanation given by Meta at the earnings report, the decline in advertising revenue level is mainly caused by two reasons.

First, in terms of users, Meta said that people's social media habits have changed, and interest has shifted to short videos similar to Reels, and the monetization ability of short videos is far less than that of the mature Feed and Stories. In addition, it is also worth noting that Meta mentioned the problem of "people's time competition intensified", translating it to everyone, which means that "everyone blames TikTok for being too addictive to home, and our app is not used".

Second, in terms of advertising pricing, Apple's new privacy rules have brought a great negative impact on Meta, and this impact will continue to be reflected in the first quarter results. In addition, high inflation and macroeconomic environments such as supply chain and exchange rate fluctuations have also brought challenges to performance growth.

It is not difficult to see that the problems listed by Meta are very tricky to solve. The reversal of user habits requires a long period of accumulation and innovation, and the challenges encountered in advertising pricing currently seem to be all objective factors, and Meta itself is difficult to change.

Daily active users of Meta's social programs, image from Meta

Meta-universe: The road to transformation is difficult, burning money for at least 5 years

This quarter, Meta announced for the first time the highly anticipated Meta-Universe Strategy division's one-year results. Reality Labs' revenue in the fourth quarter of last year was $877 million, up 57% sequentially, but at the same time it lost $3.3 billion in operating, and the net loss in each quarter of last year gradually widened, according to the earnings report. At the same time, from the perspective of the past three years, the net loss in 2019 was 4.5 billion US dollars, the net loss in 2020 was 6.62 billion US dollars, and the net loss in 2021 was 10.19 billion US dollars, and the scale of losses was also expanding by more than 30% year-on-year.

At the earnings report, Meta said that the investment in meta-universe has reduced operating profit by about $10 billion in 2021, and also made it clear that Reality Labs will not be profitable in the short term. As you can see, Reality Labs is burning money like crazy.

When announcing a full transformation of the metacosm in July last year, Zuckerberg said that the metacosm was a long-term strategy for the company, and he hoped to build Facebook into a metacosmite company in about five years. This means that, if you calculate the level of investment this year, Meta will spend nearly ten billion dollars a year on the metacosm for the next five years.

Moreover, the realization of the metacosmity is not achieved by Meta alone, but also involves multiple constraints of transmission technology, interaction technology, and regulatory factors. Whether the vision of Meta can be realized in five years is still a big question mark.

As a single business company that relies on advertising for a living, the old business has not grown but declined, and the new business is crazy to burn money but the road ahead is ethereal. Meta doesn't give investors confidence, it's justified.

| Amazon multi-habitat development: non-e-commerce revenue accounts for more than 50%, and the Prime membership fee will increase

After Meta's bloodstorm, the morale of the entire tech stock dropped back to freezing. Pinterest, Snap and other social media companies of the same type as Meta were directly frightened to "fall first", and the decline of Amazon today's earnings report is rarely about 8%, after all, Amazon's performance in the last quarter was not very good.

However, after today's hours, Amazon resisted the pressure to hand over a financial report that exceeded expectations. The earnings report shows that although Amazon's revenue rose 9% in the fourth quarter to $137.4 billion, it was slightly lower than the market expectation of $137.72 billion. However, its operating profit for the quarter surged 98% to $3.5 billion, and net profit reached $14.3 billion, bringing earnings per share to $27.75 and market expectations of $3.54, nearly ten times more than market expectations.

Amazon's stock price rose more than 18 percent after the earnings report, and if Amazon maintains that rally on Friday, it will set the company's biggest one-day gain since 2009.

Although this time Amazon did, as highlighted last quarter, due to labor and supply chain shortages and inflationary pressures, it has led to an increase in operating costs and a slowdown in the growth rate of total revenue in its e-commerce sector. But this quarter, the strong performance from the cloud business and the optimistic expectations brought by the rise in Prime membership fees and the growth of the advertising business gave Amazon a lot of life.

Image from Amazon Q4 earnings report

First, as Amazon's "second growth curve", the cloud business with the highest profit margin performed well. In the fourth quarter, the cloud computing business AWS revenue was $17.78 billion and operating profit was $5.29 billion, and the growth rate was further improved to 40%, both of which exceeded market expectations.

Second, Amazon announced an increase in the price of Prime membership. The monthly fee will be increased from $12.99 to $14.99, and the annual fee will be increased by 17% from $119 to $139. It's also amazon's first increase in Prime prices since 2018, which will be used to ease the pressure on inflation and increased operating costs.

In addition, Amazon's advertising business is on the rise. Advertising revenue, previously included in Amazon's "Other" business units, was reported separately for the first time this quarter, and advertising revenue reached $9.7 billion, up 32% year-over-year. While advertising has always been seen as an unrelated business for Amazon, can you imagine that Amazon is now the third largest advertising agency in the U.S. market, behind Google and Facebook.

It is worth noting that AWS, advertising and third-party seller services, subscription services and other businesses, Amazon's current non-retail revenue has exceeded more than 50% of the company's total revenue. That is to say, it is no longer accurate to use the e-commerce platform to describe Amazon, and Amazon has achieved a gorgeous turn of multi-habitat development, which is also the direct reason for the market confidence.

Amazon Q4 revenue of each sector, picture from Amazon financial report

But it's important to note that another major reason for Amazon's sharp profit surge in the quarter was to take into account the approximately $12 billion in revenue from investments in the electric car Rivian stock. At present, Rivian's stock price has cut from a high of about $130 to about $60 now. Therefore, in the next quarter, whether Amazon can still maintain such a high profit performance is still a question mark.

| Google: Revenue surge and record, will be split 20-1

Google, which was the first to release its earnings report this week, although it did not have such a big ups and downs as Meta and Amazon, took the lead in stopping the previous decline in technology stocks with ultra-stable performance. According to Google's fourth quarter 2021 financial report released on Tuesday, Google's parent company Alphabet had total revenue of $75.325 billion in the quarter, an increase of 32% year-on-year; net profit of $20.642 billion, up 36% year-on-year; earnings per share of $30.69, higher than expected $27.35, up 37.6% year-on-year. All indicators significantly exceeded market expectations and recorded sales for the third consecutive quarter.

The performance of its various sub-businesses is also very impressive, "total advertising revenue was $61.24 billion, up 33% year-on-year." Among them, search advertising increased by 35% year-on-year to achieve revenue of $43.3 billion, making it the biggest winner in the advertising business area this quarter. The reason for the significant growth comes from two aspects: one is that the impact of the epidemic has faded, and the recovery of retail and travel-related advertising has been obvious; the other is that due to the impact of Apple's new privacy regulations last quarter, many advertisers who relied on Apple's ecology in the past (such as Meta) have turned to Google, TikTok and other platforms, absorbing a large number of new customers.

In addition to advertising revenue, Google's cloud business also achieved a good performance in the quarter. In the quarter, Google Cloud achieved revenue of 5.5 billion, an increase of 44.6% year-on-year. The most important thing was the positive sequential growth and the significant increase in the number of new contracts, about 70%.

However, there are still fly in the ointment in this earnings report. First, Youtube's ad revenue growth was slightly struggling, and it was the only business that fell short of expectations in the quarter. In the fourth quarter, it increased by 25% year-on-year, and the growth rate continued to decline sharply. Short video business Shorts also had a flat response, with users basically the same as last quarter. In addition, the "other bets" business, including Waymo, DeepMind, and venture capital fund Google Capital, is still not improving. Revenue for the quarter was $181 million, down 7.7% year-over-year, and operating losses widened to $1.45 billion from $1.29 billion in the prior quarter. It can be seen that it is still burning money madly.

However, due to the excellent performance of this advertisement and Google Cloud, after the release of the earnings report, Google's stock price jumped by more than 6%. At the earnings report, Google's decision to split its stock by 1 to 20 on February 7 added another fire to the stock price, and Google's stock price soared nearly 10% at one point in the next trading day.

The day after the earnings report, Google's stock price performed

At this point, the financial report of this quarter's giants has basically come to an end. I have to say that at the moment when the market sentiment is turbulent, this time the earnings season is a bit fierce. The prestigious FAANG Silicon Valley's five technology giants folded Meta (Facebook) and Netflix in this quarter. Judging from the problems reflected in this financial report, the pattern of the technology giants that have been divided for many years may really usher in some changes.

Note: The cover image is from the Financial Times and the copyright belongs to the original author. If you do not agree to use, please contact us as soon as possible and we will delete it immediately.