The global automotive industry is undergoing a full range of dramatic changes. Increasingly stringent emissions regulations, combined with higher requirements for business average fuel economy, have exacerbated this challenge, leading to increased demand and supply of electric vehicles. According to the IHS Markit Supply Chain and Technology Department, the global new energy vehicle motor market will produce more than 10 million units in 2020, and it is expected to produce more than 90 million units in 2032, with a compound annual growth rate (CAGR) of 17%.

Depending on the position of the motor in the powertrain architecture, it can be summarized into four different areas. It is not sufficient to classify the propulsion system design or the type of motor, because the same motor type can meet two completely different propulsion system applications. For a given propulsion system design, the choice of motor is not limited to the type of motor, other factors such as performance, thermal management and cost are all considerations. The resulting new energy vehicle motors include: engine-mounted motors, transmission-connected motors, e-axle motors and hub motors.

Engine-mounted motor

Engine-mounted motor technology is primarily based on belt starter generator (BSG) technology. Belt starter generator (BSG) technology replaces the traditional starter motor and generator (alternator) of an engine and fulfills their functionality. Engine replacement functions including stop-start, coasting, electric torque and power boost are also implemented. The demand for this technology solution has exploded, and it offers a more cost-effective approach than conventional cars, achieving significant fuel savings with minimal changes to the powertrain architecture. Engine-mounted motors account for approximately 30% of the overall propulsion motor market in 2020, and by 2032, their market is expected to grow at a COMPOUND annual growth rate of 13%. Together, the world's top three suppliers supplied more than 75% of demand in 2020 and are expected to maintain most of their market share in the future.

Transmission-connected motor

Transfer-connected motors alleviate some of the limitations of the belt start-up generator (BSG) architecture, provide more power, complement traditional powertrains, and increase the flexibility of the power system. This series of motors is mainly suitable for all-electric or plug-in hybrid vehicles, depending on the powertrain architecture, the motor position can be before or after the transmission. Transmission-connected motors account for 45% of the propulsion motor market by 2020, according to IHS Markit's Supply Chain & Technology division, which is expected to grow at a CAGR of 16.7% by 2032.

Unlike other types of motors, in the transfer-connected motor market, Japan and South Korea alone will account for about 50% of production in 2020. In this proportion, considering the concern of these countries on all-hybrid and plug-in hybrid vehicles, this data is actually not difficult to understand. In addition, the leading OEMs that use transfer-connected motors in the production of electrified vehicles and their key suppliers are mostly located in Japan and South Korea.

E-axle motor

The third motor series is e-axle motors, which combine individual electrified powertrain components in a single component package, creating a compact, lightweight and efficient solution that delivers superior performance and greater efficiency. In the e-axle motor configuration, the motor is placed on the transaxle.

According to IHS Markit's Supply Chain & Technology Department, e-axle motors will account for about 25% of the propulsion motor market by 2020, and it is expected that by 2032, the market will grow at a compound annual growth rate of 20.1%, making it the fastest growing category of all propulsion motors. This is a significant market opportunity for all areas of the motor supply chain, such as electrical steel producers, copper winding producers and aluminum casters producers. Europe and Greater China are leading the e-axle motor market and are expected to account for more than 60% of global production in the 2020-26 forecast period.

Hub motor

The fourth type of motor is the hub motor, which allows the motor to be placed in the center of the wheel, reducing the components required for transmission and energy losses associated with gears, bearings and gimbal connections.

The in-wheel motors, classified as the P5 architecture, look like an attractive alternative to traditional powertrain architectures, but they have significant drawbacks. In addition to the increase in costs brought about by technological progress, the problem of increasing the unsprung load of vehicles has been detrimental to the popularity of hub motors. IHS Markit said in-wheel motors will remain a segment of the global light vehicle market, with annual sales remaining below 100,000 for most of the next decade.

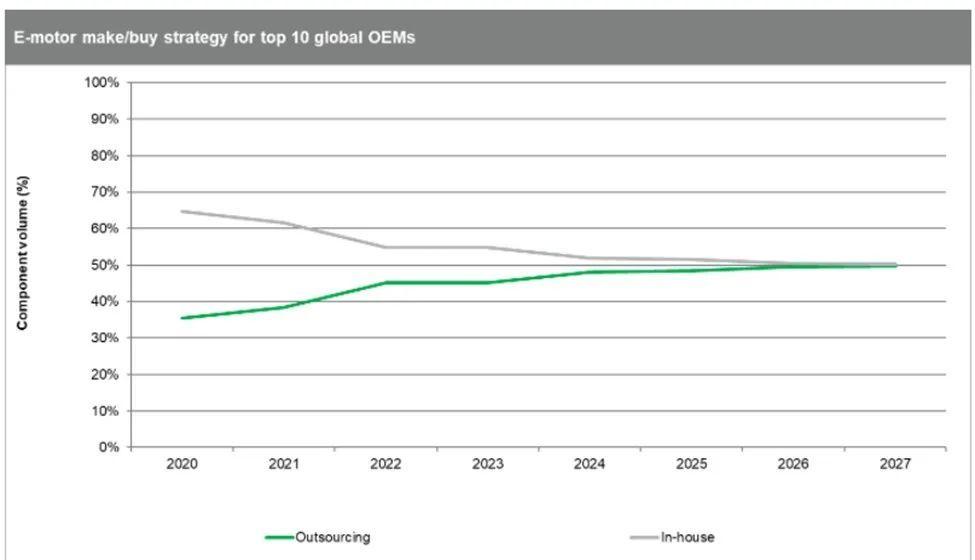

Homemade or outsourced strategies

In the global motor supply chain market, an important trend is the in-house manufacturing and outsourcing of motors. The chart below outlines the trends in the world's top ten OEMs producing or purchasing propulsion motors. It is expected that by 2022, global OEMs will be more inclined to outsource rather than produce motors in-house. This period is often considered a "technical requirement" and most OEMs worldwide will rely heavily on motor suppliers, given the latter's excellent understanding of the underlying technology, as well as the limited but ever-changing component needs of OEMs.

From 2022 to 2026, the so-called "supportive growth" phase, the share of in-house manufactured motors will gradually increase. About 50% of the motors produced in 2026 will be domestically produced. During this time, OEMs will develop technologies in-house with the help of partner and supplier mergers. IHS Markit predicts that after 2026, OEMs will be in the lead and the share of in-house motor manufacturing will increase significantly.

As the vanguard of the promotion of new energy vehicle cities, the application of Shanghai's charging supporting infrastructure or a microcosm of the development of new energy vehicles, which shows that power exchange is not the only mode, and charging also has its own scenes and necessities.

Wang Zidong pointed out that power exchange and charging are not completely opposite, this is a new choice, and has considerable social benefits. "When the life of the battery pack increases and the safety is improved, the passenger car in the power exchange mode will be widely used in the market, and not only the B-end car, but also the C-end car (private car) will gradually catch up with this demand."

Huang Chunhua believes that in the future, new energy vehicle users have time to charge, no time to change the power, but also can upgrade the battery by changing the power station, so that users have a variety of choices, more convenient use is the focus of industrial development. In addition, the Ministry of Industry and Information Technology recently announced that in 2022, the pilot project of fully electrified vehicles in the public domain will be launched. Behind this must be the combination of charging and power exchange, together to promote the full electrification of public domain vehicles. "In the next two to three years, in the field of public transportation, transportation and other segments, the popularization of the power exchange model will accelerate."