(Text/Li Pengtao Editor/Yin Zhe) After young people drink the "first share of milk tea", the "first share of the tavern" will also go to Hong Kong for listing.

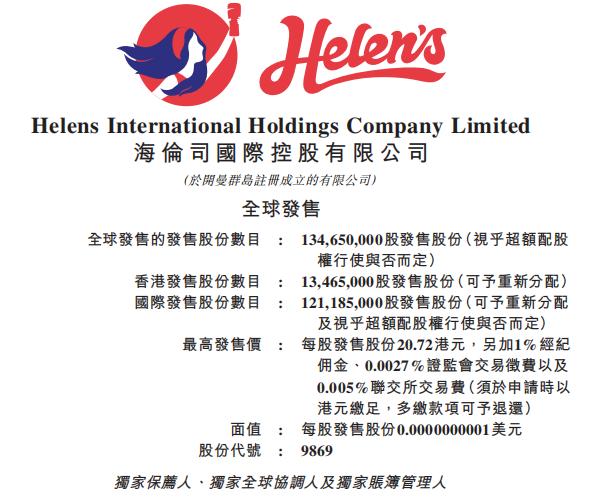

On August 31, the chain bistro Helens officially launched a prospectus to issue more than 134 million shares at an issue price of HK$18.82-20.72 per share and raise more than HK$2.5 billion.

(Image source: screenshot of prospectus, the same below)

According to the prospectus, about 70% of the funds raised by Helens will be used to open a new tavern and its expansion plan in the next three years; 15% will be used to further strengthen the talent building and basic capacity building of the pub; and the remaining 15% will be used to strengthen the brand awareness and operating funds and general corporate purposes.

Relying on young people and low-priced wine for less than 10 yuan a bottle, Helens, which earns 800 million yuan a year, aims to open 2,200 stores by the end of 2023. Can it rely on the beach capital market to become a fragrant feast by "low price"?

The number of stores has increased by more than 6 times in three years

With the prevalence of the night economy and the social needs of Generation Z's "wine friends", the bistro business has stood on the cusp of the new economy.

According to Frost & Sullivan data, China's nighttime consumption accounts for about 60% of the total retail sales, and continues to grow at a scale of about 17%, becoming an important driving force for China's domestic demand.

From 2015 to 2019, the total market volume of China's night economy grew from 10.9 trillion yuan to 16.8 trillion yuan, with a compound annual growth rate of 11.4%, and is expected to further grow to 2.82 billion yuan in 2025.

At the same time, the mainstream consumer base of the pub industry is generally younger. According to the data of the "2020 Young People's Alcohol Consumption Insight Report", 10% of the post-90s population has the habit of daily drinking, and young people have become the main force of alcohol consumption.

"Drinking friends" has also become an important way for young people to develop personal social networking. The data shows that young people's consumption purposes in pubs are mainly "social needs, personal interests and gatherings of friends" and pay more attention to emotional experience and price when consuming.

The huge night consumption scene and the rapid growth of Gen Z alcohol consumers have boosted the big business of the tavern. According to Frost & Sullivan data, the number of bistro stores in China was 35,000 by the end of 2020, and it is expected to exceed 50,000 by 2025, with a compound annual growth rate of 10.1%

The total revenue of China's pub industry has increased from 84.4 billion yuan in 2015 to 117.9 billion yuan in 2019, with a compound growth rate of 8.7%, and it is expected that from 2020 to 2025, the compound growth rate of China's pub industry will be 18.8%.

The tavern Helens is also taking advantage of the "night economy + wine friends" to meet friends, in less than two years, the number of stores has increased rapidly by nearly 200.

In 2009, the first store of Helens was born in Wudaokou, Beijing, known as the "Center of the Universe", targeting a group of international students, located near the university town, controlling the price of wine within 10 yuan, and soon attracted the attention of many student groups. Subsequently, it was laid out in many cities such as Shanghai.

In the early days, Helens rapidly expanded the market with the model of "direct operation + franchise", and after 2018, the company gradually converted the franchised pub into a directly operated pub. At present, the taverns under Helens are all directly operated stores.

From 2018 to the last practical date, the number of directly operated pubs under Helens increased from 84 to 528, and in just over three years, the number of stores increased by more than 6 times.

From the perspective of store opening logic, the main market of Helens is the second and third tier cities and below. From 2018 to the last practicable date, the number of stores in second-tier cities increased from 82 to 296; the number of stores in third-tier cities and below expanded from 53 to 165; and the number of pubs in first-tier cities increased from only 26 to 66.

This means that in the logic of opening a store, Helens is more inclined to sink the market. Under the relatively lower labor and rental costs, more profits are created.

Helens said in the prospectus that it will use about 70% of the proceeds to open new pubs and achieve expansion plans in the next three years, expecting to open 400, 630 and 900 pubs in 2021, 2022 and 2023 respectively, and increase the total number of pubs to about 2200 by the end of 2023.

For the rapid expansion of Helens, Jiang Han, a senior researcher at Pangu Think Tank, frankly told the Observer Network: "The excessively rapid expansion rate is actually still a little worrying. ”

"After all, such a rapidly expanding company, especially under the direct operation model, its own operating capabilities, especially the ability of employees (stores) to match its expansion speed, whether the high cost pressure caused by expansion can be effectively resolved, these problems Helens need to give the market more answers." he said.

After the annual income of 800 million, only 2.78 million are left in the pocket

While Helens accelerated its expansion, its operating performance was also growing at a high rate.

According to the prospectus, from 2018 to 2020, Helens' revenue increased from 115 million yuan (unit: RMB, the same below) to 564 million yuan, and increased to 818 million yuan last year.

Although revenue has increased year by year, Helens' net profit performance has been unstable. In the same period, the company's net profit was 9.734 million yuan, 79.136 million yuan and 70.072 million yuan, respectively.

Helens, which sat on the revenue rocket, lost 76.332 million yuan in the first quarter of this year, down 360.69% year-on-year.

Looking back at the development of Helens in recent years, it can be found that rising labor costs have caused great pressure on profitability.

From 2019 to 2020, the company's employee welfare and human service expenditure was 92.271 million yuan and 179 million yuan, respectively, an increase of 267.95% and 93.92% year-on-year; in the first quarter of 2021, the growth rate of this part of the expenditure reached 845.97% year-on-year.

It is worth noting that Helens did not pay all the social security and housing provident fund contributions for some employees.

According to the relevant Chinese laws and regulations, if the company is unable to pay the required social insurance contributions in full, it may be ordered to pay the unpaid social insurance contributions within the prescribed time limit and pay the corresponding late fees, otherwise it will be fined one to three times.

According to Helens' estimates, the company may face a total of $2,003,500 in fines from 2018 to the end of March 2020.

At the same time, Helens' marketing expenses are also increasing day by day, which also brings a lot of pressure to profitability.

According to the prospectus, from 2018 to 2020, the company's publicity and promotion expenses were 5.2 million yuan, 12.1 million yuan and 15.4 million yuan, respectively. In the first quarter of this year, the expenditure reached 6 million yuan.

In addition, the asset-liability ratio of Helens division is high, reaching 95.4%, 84.48% and 81.37% from 2018 to 2020, respectively, and the company's asset-liability ratio in the first quarter of this year is 86.04%. It can be seen that Helens is not rich.

From the perspective of cash flow data, at the end of 2020, Helens' cash and cash equivalents were once only 2.781 million yuan.

Due to the $328,000 preferred equity financing from CICC Jiacheng and Black Ant Capital, Helens' cash has rebounded. As of the end of the first quarter of 2021, the company's cash and cash equivalents were 153 million yuan, so listing and fundraising has become an inevitable choice for the expansion of Helens.

The "low price" model is easy to be replaced by imitation

Known as the "Ten Dollar Tavern", the core customers of Helens are young people aged 18 to 28. The company said in the prospectus that it plans to expand the age distribution of its major customers to 18 to 38 years old in the future.

At present, Helens attracts traffic through low prices and drives profits with small profits and high sales.

Bottled beers from Helens, including Budweiser, Corona and private labels, do not exceed 10 yuan. For example, a 275ml bottle of Budweiser costs 9.8 yuan. According to Frost & Sullivan, the average selling price of this Budweiser beer in the same industry is 15 yuan to 30 yuan / bottle.

With "own products + external products" as the product matrix, Helens' own alcohol accounts for nearly 70% of the total revenue. According to the prospectus, from 2018 to the first quarter of 2021, the proportion of Helens' own liquor revenue to total revenue was 68.4%, 64.2%, 69.8% and 74.8%, respectively.

In general, the gross profit margin of private label liquor is higher than that of third-party purchases. From 2018 to 2020, the gross profit margin of the former was 71.4%, 75.3% and 78.4%, respectively, which was higher than the gross profit margin of 39.2%, 52.8% and 51.5% in the corresponding period.

It should be pointed out that the gross profit contributed by Helens' own bottled beer is lower than that of third-party brands. In 2018, the company's gross revenue per liter of bottled beer was only $2, and it didn't rise to $10.5 until 2020.

The gross income contributed per liter of third-party brand beer has always been more than 10 yuan, and as of the first quarter of this year, the gross income per liter has reached 13.8 yuan.

In recent years, although "super cost-effective" has become the killer of Helens, it has also affected the gross profit of its own products.

In addition, there are always catch-ups on this track.

On the day of the hearing of Helens through the Hong Kong Stock Exchange, the chain pub brand "Cat Yuanwai" announced the completion of Pre-A and A rounds of financing totaling more than 100 million yuan.

Similar to Helen Division, "Cat Staff Outside" provides craft beer, wine snacks, all self-developed and self-supplied, per capita consumption in the range of 50-70 yuan, there are currently more than 50 stores in Shenzhen, all of which have achieved profitability.

Back in 2019, Nesher's tea made its way into the bar industry. At present, the company's Nesher House has begun rapid expansion; in 2020, Starbucks opened its first bar on the Bund in Shanghai.

As the beverage giants covet this huge market cake, the "low-priced volume" model of the tavern Helens seems to be easily imitated and replaced.

For the risks faced by Helens after its listing, Jiang Han told the Observer Network: "Its business model is actually not exclusive enough, which is a very easy to imitate, and it is also a relatively low cost business model. ”

He added: "Due to the lack of sufficient market entry barriers, Helens' business model is extremely easy to learn from other companies, and once Helens is listed, other companies see Helens' business model clearly, then joining the battle group is actually very simple." ”

This article is an exclusive manuscript of the Observer Network and may not be reproduced without authorization.