Exchange proceeds subsidized 115 million profits, and Hanshow Technology's IPO fought with supplier Dongfang Kemai Xinphi data

Text/Leju Finance Cheng Mengyao

The remote management background can change the price with one click, and the shelf price tag will be refreshed synchronously. The Internet of Everything, as a price display tool, has basically become the standard configuration of new retail. The penetration rate of ESLs in the consumer market has increased, and Hanshow Technology Co., Ltd. (Hanshow Technology), a seller of ESL terminals built by former Huawei employees, has also sought to list on the GEM under the escort of capital.

In 2021, Hanshow Technology applied for listing on the Science and Technology Innovation Board, but was unsuccessful, and in 2023, it moved to the Growth Enterprise Market, and less than a month after submitting the form, the Shenzhen Stock Exchange accepted its application and issued a letter of inquiry.

According to the prospectus, Hanshow Technology's revenue has increased significantly in the past two years, but its profitability is not stable, and there are operational risks such as upstream dependence on outsourcing processing, downstream dependence on large customers, and continuous decline in R&D expense ratio.

In addition, Hanshow Technology also has an intellectual property dispute with SES, the No. 1 U.S. company in the industry. The case of SES-imagotag SA, SES-imagotag GmbH and SES-imagotag Inc. v. Defendants Hanshow Technology and Hanshow is still pending.

In this GEM IPO, Hanshow Technology plans to raise 1.182 billion yuan for the industrialization project of store digital solutions, AIoT R&D center and informatization construction project, and replenish working capital, of which 350 million yuan will be used for replenishment.

1. The luxury capital group escorted the listing valuation of 5.9 billion

Founded in 2012, Hanshow Technology Co., Ltd. has Hou Shiguo, Chairman and General Manager, and Li Liangyan, Director and Deputy General Manager, both of whom were previously Huawei technicians. Since its establishment, Hanshow Technology has been escorted by capital all the way.

From 2013 to 2019, Haijie Investment, Redstone Chengjin, Changrun Assets, Chuangda Capital, Legend Capital, Hongzhang Capital, Lightspeed Photosynthesis, Jingwei Venture Capital, and CICC Capital entered one after another. At the beginning of the reporting period, its shareholders included Hangzhou Chuangqian, Hongshi Chengjin, Junlian Huicheng, Chai Yuan Capital, Xiamen Qilu, Zhuji Mingming, etc.

During the reporting period, Hanshow Technology had 4 equity transfers and 2 capital increases, with shareholders such as Hangzhou Chuangqian and Zhuji Famous expanding their shareholdings through equity transfers, and Chuanqi Optoelectronics, Xingtou Preferred, Mingfeng No. 3, Changtou No. 1, Co-creation Zhiyuan, Hongtu Yuechuan, Shenzhen Venture Capital, Yimei Wireless, Hongnuo Investment, Silicon Valley Anchuang, Silicon Valley Xinyi, Silicon Valley Hechuang, Silicon Valley Lingxin, and Qingcheng Xingyuan became shareholders through capital increase. At the same time, Changrun Jiahe and Chaiyuan Capital chose to withdraw, and Hou Shiguo also cashed out 32 million yuan through two equity transfers.

In April 2023, Chayuan Capital will withdraw due to the expiration of the duration of the company, and the 1.93% equity will be valued at 87.8743 million yuan, which is 12 yuan per share. Compared with February 2022, Changrun Jiahe transferred 0.57% of the equity to Liaocheng Hechuang at a price of 30.0024 million yuan to 13.89 yuan per share, which is 86% off.

During the two transfers, Hanshow Technology did not increase its capital, and based on this calculation, when Chaiyuan Capital withdrew, Hanshow Technology was valued at about 4.55 billion yuan. In this IPO, Hanshow Technology plans to raise 1.182 billion yuan, with a listing valuation of 5.91 billion yuan, which is 1.3 times the valuation of Chayuan Capital when it withdrew seven months ago.

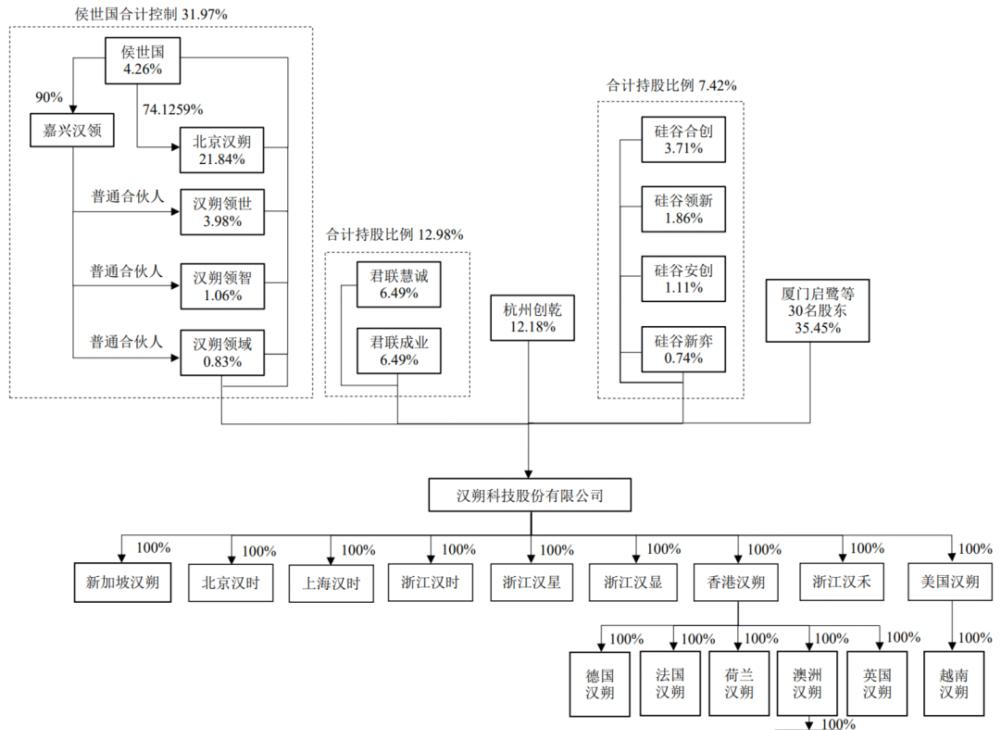

Hanshow Technology's shareholding structure is relatively dispersed, with 42 shareholders before the IPO, and the top 10 shareholders control a total of 85.83% of the total according to the same control and concerted action relationship.

As the largest shareholder and controlling shareholder, Beijing Hanshow holds 21.84% of the shares, and Hou Shiguo holds 4.26% of the shares, and controls a total of 31.97% of the shares through the actual control of Beijing Hanshow, Hanshow Lingshi, Hanshow Field and Hanshow Lingzhi, and is the actual controller.

Among the external shareholders, Legend Capital holds a total of 12.98% of the shares, making it the largest institutional investor; Hangzhou Chuangqian holds 12.18% of the shares, behind which there are the National Social Security Fund, China Merchants Wealth, Ping An Trust, Shougang Fund, Gopher Assets, Shenwan Hongyuan and other capitals; and Paradise Silicon Valley holds a total of 7.42% of the shares through four institutions.

In addition, CICC Capital, a wholly-owned subsidiary of CICC, the sponsor of Hanshow Technology's listing, indirectly holds 4.31% of the shares of Xiamen Qilu and 24.17% of the property shares of Shanghai Guangyi, the shareholder of Shanghai Guangyi, through its role as the executive partner of CICC Qiyuan, thereby indirectly holding 0.36% of the shares.

2. Equity dispersion The stability of the control of the actual controller was questioned

During the Reporting Period, in order to ensure the control of Hanshow Technology by Beijing Hanshow and Hou Shiguo, Hanshow Technology also had voting rights entrustment arrangements. 16 institutional shares, including Legend Huicheng, Legend Chengye, Jiaxing Shanglin, Changrun Ice Wheel, Shanghai Guangyi, Chuangchuang No. 1, Zhuji Famous, Hangzhou Chuangqian, Ningbo Rongsong, Zhongtai Huasheng, Xiamen Qilu, Silicon Valley Anchuang, Silicon Valley Xinyi, Silicon Valley Hechuang, Silicon Valley Lingxin, and Qingcheng Xingyuan, entrusted their voting rights of the company to Beijing Hanshow and Hou Shiguo for exercise, but the above entrustment arrangement was terminated twice before the declaration.

Also in order to stabilize Hou Shiguo's control, in February 2021, Hanshow Technology set up special voting shares, that is, 99,220,800 shares directly held by Hou Shiguo and Beijing Hanshow are Class A shares, and the remaining 281 million shares are Class B shares, and the number of voting rights per Class A share is four times the number of voting rights per Class B share. However, on June 12, 2023, the establishment of the above-mentioned special voting shares will be cancelled.

With the release of the mandate and the cancellation of special voting rights, the stability of Hanshow's control has become the focus of regulation. The Shenzhen Stock Exchange not only requires Hanshow Technology to explain the reasons for the termination of the voting rights entrustment and the impact on the control of the actual controller. It is also required to explain the stability and safeguard measures of Hou Shiguo's control over the issuer in light of the fact that the termination of the above-mentioned arrangement before filing actually reduces the proportion of Hou Shiguo's voting rights.

According to the reply letter, after the capital increase in December 2016, the proportion of equity and voting rights of the company controlled by the actual controller Hou Shiguo was reduced to 43.88%, and in order to avoid the dilution of the proportion of voting rights of the company controlled by the actual controller through follow-up financing and enhance the control of the actual controller, Hou Shiguo and Beijing Hanshow required the investors to sign a voting rights entrustment agreement.

In 2017, 7 shareholders including Legend Huicheng, Legend Chengye, and Tianjin Qingzhe increased the capital of Hanshow Co., Ltd., and the equity ratio controlled by Hou Shiguo was diluted to 37.28%, and Legend Huicheng, Legend Chengye, Jiaxing Shanglin, Changrun Ice Wheel, Chuangchuang No. 1, and Shanghai Guangyi entrusted 24.07% of the voting rights held by Hanshow Co., Ltd. to Hou Shiguo.

With the subsequent capital increase and the transfer of part of Hou Shiguo's equity, its voting rights were further diluted. In December 2020, after Hanshow Co., Ltd. was transformed into a joint stock limited company, the proportion of voting rights controlled by Hou Shiguo was diluted to 33.76%, and in order to further strengthen the stability of the control of the issuer by the actual controller Hou Shiguo, in February 2021, Hanshow Technology set up special voting shares, and the voting rights of Hou Shiguo were increased to 63.74% through the special voting rights arrangement.

However, during the effective period of the relevant arrangements, there was no impact on the controlling position of the actual controller, and Hou Shiguo and Beijing Hanshow did not exercise such voting rights entrustment arrangements.

As of the date of issuance of the reply to the letter of inquiry, Hou Shiguo controlled 31.97% of the voting rights, and the total shareholding ratio of the remaining major shareholders alone or related to them did not exceed 13%, which was quite different from the proportion of shares controlled by Hou Shiguo with voting rights.

In addition, among the seven members of the Board of Directors, Hou Shiguo has been serving as the executive director/chairman of the company, and four directors have been nominated by Beijing Hanshow/Hou Shiguo, and other major shareholders who directly hold more than 5% of the company's shares individually or collectively have issued a "Commitment not to seek control of the company", "On the date of completion of Hanshow Technology's initial public offering and listing, the company will not increase the number of directors nominated by the board of directors of Hanshow Technology during the period when Hou Shiguo controls Hanshow Technology" Even after listing, Hou Shiguo still has a lasting influence on the board of directors.

3. Overseas income accounts for more than 96%

Gross profit margin declined, net profit fluctuated sharply

Focusing on the offline retail application of IoT wireless communication technology, Hanshow Technology has built a business system with software and hardware products and services such as ESL system and SaaS cloud platform services as the core in the field of retail store digitalization, providing assistance for the digital transformation and upgrading of the retail industry. Branches have been set up in Singapore and other countries to serve more than 400 customers in more than 50 countries and regions around the world.

From 2020 to 2022, Hanshow Technology's operating income grew at a compound growth rate of 54.94%, and in 2021 and 2022, its ESL revenue scale ranked second among competitors of listed companies in the world, second only to SES in the United States, but in the first half of 2023, it was overtaken by South Korea's soluM and slipped to third in the ranking. Some analysts believe that the patent infringement dispute with SES has affected Hanshow's performance to a certain extent, but Hanshow Technology said that the patent dispute lawsuit with SES is less likely to lose the lawsuit and will not have a significant adverse impact on production and operation.

From 2020 to 2022 and the first half of 2023 (hereinafter referred to as the "reporting period"), Hanshow Technology's operating income was 1.190 billion yuan, 1.617 billion yuan, 2.858 billion yuan, and 1.875 billion yuan respectively, with a year-on-year increase of 35.86% and 76.70% in 2021 and 2022, and the net profit attributable to the parent company in the same period was 82 million yuan, -06 million yuan, 207 million yuan, and 324 million yuan, respectively, with a year-on-year increase of -107.66% in 2021 and 2022. 3383.71%, fluctuating violently.

During the reporting period, the average unit prices of ESL terminal products were 39.46 yuan/piece, 39.57 yuan/piece, 40.37 yuan/piece, and 41.63 yuan/piece, respectively, maintaining a steady and slight increase, bringing overall sales revenue of 977 million yuan, 1.431 billion yuan, 2.659 billion yuan, and 1.765 billion yuan, accounting for 90.58%, 88.51%, 93.06%, and 94.11% of the main business revenue, respectively.

Hanshow's ESL terminal products mainly include Nebular, Stellar, Nowa, and Lumina, which are mainly sold abroad and are mostly settled in foreign currencies such as euros, US dollars, and Australian dollars, but due to factors such as exchange rates and promotional incentives, sales revenue and gross profit margin fluctuate greatly. In each period of the reporting period, overseas revenue accounted for 79.01%, 76.10%, 93.04% and 96.47% of Hanshow's operating revenue, respectively.

Based on the average exchange rate in 2020, after excluding the impact of exchange rate, from 2021 to June 2023, Hanshow Technology's operating income was 1.673 billion yuan, 3.083 billion yuan, and 1.962 billion yuan, respectively, and decreased by 55.5285 million yuan, 226 million yuan, and 86.5149 million yuan respectively due to the impact of exchange rate.

In terms of gross profit margin, during the reporting period, the gross profit margin of Hanshow's main business was 30.70%, 22.70%, 20.05% and 29.62% respectively, and showed a downward trend from 2020 to 2022, with gross profit margins of 30.70%, 24.36%, 25.44% and 32.72% respectively after excluding the impact of exchange rates.

In terms of product series, exchange rate changes during the reporting period led to a decline in the gross profit margin of Nebular, Stellar, and Nowa series products, which accounted for a high proportion of overseas sales, with an impact of about 0-3 percentage points in 2021, 4-7 percentage points in 2022, and 2-4 percentage points from January to June 2023.

However, the exchange gains and losses arising from exchange rate changes helped Hanshow Technology subsidize its net profit of 78.08 million yuan and 115 million yuan in 2022 and the first half of 2023.

Fourth, sixty percent of the revenue comes from the top five customers

99% of the revenue of the main products depends on outsourcing

While its revenue is dependent on overseas markets, Hanshow Technology also has a dual concentration of customers and suppliers. In each period of the reporting period, the sales revenue from the top five customers was 863 million yuan, 632 million yuan, 1.613 billion yuan and 1.233 billion yuan respectively, accounting for 72.47%, 39.07%, 56.46% and 65.73% of the operating income respectively, and the purchase amount of the top five suppliers was 627 million yuan, 883 million yuan, 1.654 billion yuan and 776 million yuan respectively, accounting for 62.51%, 67.69% and 62.88% of the total procurement value respectively. 59.59%。

However, Hanshow Technology has inconsistencies with the data disclosure of its main supplier, Dongfang Kemai. From 2020 to 2022, Dongfang Kemai was its first, first, and second largest supplier, with a purchase amount of 315.2879 million yuan, 293.2381 million yuan, and 327.6626 million yuan.

In the same IPO, the sales revenue from Hanshow Technology from 2020 to 2022 disclosed by Dongfang Kemai was 314.2353 million yuan, 293.9699 million yuan, and 327.3545 million yuan, respectively, and the difference between the disclosed amounts of the two companies was 1.0526 million yuan, 731,800 yuan, and 308,100 yuan, respectively. The two IPO companies that have been accepted by the Shanghai Stock Exchange and the Shenzhen Stock Exchange have disclosed transaction data with tens or millions of differences. Hanshow Technology said that the main reason was that there was a difference in the exchange rate selected by the two parties when carrying out the translation and accounting treatment of foreign currency business, resulting in a difference in the amount of the translated accounting base currency, RMB. Solum, one of Hanshow's main competitors, is also the largest customer of Oriental Kemai.

Most of Hanshow's main business products rely on outsourcing processing, which has also attracted the attention of the exchange to its business model and competitiveness.

In the outsourcing mode, the components of the ESL terminal are assembled by the outsourcing processing factory, including the production process of patching, product assembly, functional testing, packaging and shipment, and Hanshow directly purchases the finished products from the outsourcing manufacturers.

During the reporting period, the sales revenue of Hanshow Technology's ESL outsourcing products were 721 million yuan, 983 million yuan, 2.416 billion yuan, and 1.264 billion yuan, accounting for 87.83%, 81.31%, 97.15%, and 99.64% of the main business income respectively, and the proportion of outsourced processing products continued to increase, and in the first half of 2023, its self-produced products accounted for less than 1%, bringing sales revenue of 1.3705 million yuan, accounting for 0.11% of the main business income.

According to Hanshow, the main reason for outsourcing processing is that the production process of ESL terminals is relatively mature, and through outsourcing production, the abundant equipment and human resources of the outsourcing processing plant can be flexibly used to reduce the risks brought by market fluctuations to the company's operation.

In terms of competitiveness, Hanshow Technology said, "The core technology and core competitiveness are mainly reflected in the high performance of the Internet of Things system, not in the production of core components and complete machines." "Focusing on the wireless communication protocol of the Internet of Things, a comprehensive core technology system has been built, and the advantages of its ESL system are mainly reflected in the system capacity, large data throughput, strong anti-interference ability, fast update speed, ultra-low power consumption, long service life of equipment, high-precision autonomous positioning, and rich application functions.

At the time of submission, Hanshow Technology has five core technologies. During the reporting period, the R&D expenses were 102 million yuan, 122 million yuan, 124 million yuan and 71.5516 million yuan respectively, and the R&D expense rates were 8.56%, 7.55%, 4.33% and 3.82% respectively. Compared with comparable companies in the same industry, Hanshow's R&D expense ratio in 2020-2021 far exceeded that of its peers, but it gradually fell behind in 2022 and the first half of 2023.

Attached: List of intermediaries for listing and issuance of Hanshow Technology

Sponsor: China International Capital Corporation Limited

Lead underwriter: China International Capital Corporation Limited

Issuer's lawyer: Beijing Zhong Lun Law Firm

Auditor: KPMG Huazhen Certified Public Accountants (Special General Partnership)

Appraisal agency: Beijing CEA Asset Appraisal Co., Ltd