Recently, Baidu Group released unaudited financial results for the fourth quarter ended December 31, 2021 and the full year 2021. Judging from the financial report data, although the quarterly and annual revenue has increased, the operating profit margin and net profit margin have both declined, and it has contracted for several consecutive quarters.

Nandu reporter combed the company's quarterly performance data since 2020 and found that its online marketing revenue part began to decline from the first quarter of 2021, and fell from double-digit growth to only 1% year-on-year growth in four quarters; the non-advertising revenue part also showed a slowdown in growth.

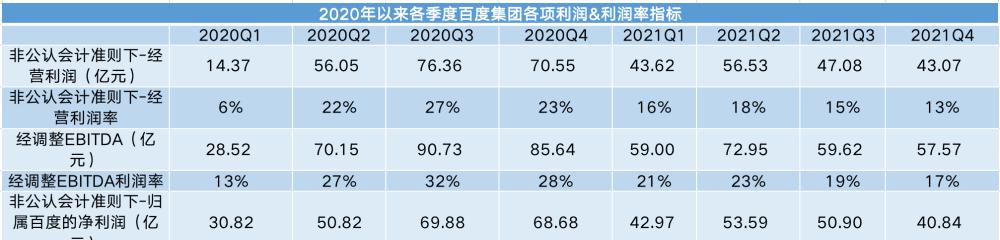

Multiple profit indicators declined for 6 consecutive quarters

From the financial report data, in the fourth quarter of 2021, Baidu achieved an operating profit of 1.958 billion yuan, down 61% year-on-year, and the operating profit under non-GAAP reached 4.307 billion yuan, down 39% year-on-year; the net profit attributable to Baidu was 1.715 billion yuan, down 67% year-on-year, and the indicator under non-GAAP was 4.084 billion yuan, down 41% year-on-year. Adjusted EBITDA margin was 17 percent, compared to 28 percent in the year-ago quarter.

From the perspective of the whole year of 2021, Baidu achieved an operating profit of 10.518 billion yuan, down 27% year-on-year, Non-GAAP operating profit of 19.03 billion yuan, down 12% year-on-year; net profit attributable to Baidu was 10.226 billion yuan, down 54% year-on-year, and the indicator under non-GAAP was 18.83 billion yuan, down 14% year-on-year. Adjusted EBITDA margin was 20 percent, compared to 26 percent in the year-ago quarter.

Data source: Baidu quarterly financial reports

Nandu reporter counted the profit and profit margin indicator data disclosed by Baidu Group and Baidu Core in the 8 quarters since 2020. The comparison found that Baidu Group's Non-GAAP operating profit has declined for 6 consecutive quarters from the third quarter of 2020, while the Non-GAAP operating profit margin has also fallen from 22% in the third quarter of 2020 to 13% in the fourth quarter of 2021. Non-GAAP net profit also declined for six consecutive quarters, shrinking from nearly $7 billion in the third quarter of 2020 to the latest $4.1 billion.

Baidu's core revenue growth slowed down advertising revenue under pressure

As in previous quarterly earnings reports, Baidu's presentation of the financial report emphasized the growth of non-online marketing revenue and highlighted the main impetus from the cloud and other AI-driven businesses. Over the past few years, Baidu has been emphasizing the opening of the second and even third growth curves, trying to break the single model of advertising as the main source of revenue, and vigorously developing new technology-driven businesses such as AI, cloud computing, and autonomous driving. Advertising (the "Baidu Core Online Marketing Section") and the cloud and other AI-driven businesses (the "Baidu Core Non-Online Marketing Portion") are recorded together in Baidu's financial statements as the "Baidu Core" section.

The revenue growth rate of Baidu's core non-online marketing part since 2021 is higher than that in 2020, and it is also higher than the growth rate of the advertising business that has experienced obvious decline. The data shows that its online marketing revenue segment began to decline from the first quarter of 2021, and in 4 quarters, the growth rate fell from double digits to only 1% of the latest.

In fact, due to the environmental impact, many industries have been affected to varying degrees, and they have adjusted or reduced their advertising budgets. The loss of large customers in many industries has been clearly reflected in their financial data.

The low growth of Baidu's advertising business actually affected the growth rate of Baidu's core revenue. Throughout 2021, Baidu's core's overall revenue showed a slowdown in growth, from a continuous decline of 34% in the first quarter to a year-on-year growth rate of only 12% in the fourth quarter.

It is worth noting that at present, advertising revenue is still the bulk of Baidu's core revenue, accounting for up to 74%. Stretching the observation dimension to the first quarter of 2018, it will be found that its proportion of advertising revenue has indeed been shrinking, and the proportion of AI-driven business has also been increasing, from 6% to 26.5%, but in the context of slowing growth, the expansion of this proportion still needs a lot of time, and it also takes time to promote the overall revenue growth. While Baidu's first growth engine is shrinking, the second engine is far from offsetting the decline of the advertising business, which is considered by some analysts to be the key point of Baidu's transformation breakthrough and the hidden worry behind the data. A number of brokerage research reports also highlighted the pressure on Baidu's advertising business. CITIC Securities Research Report believes that considering that the domestic epidemic scatter outbreak in the first quarter delayed the recovery of demand, it is expected that Baidu's core advertising revenue growth will still face certain pressure in the first half of the year.

Continued high cost inputs, free cash flow continued to decline

It is worth mentioning that Baidu's expenditure on AI-driven new business is very large. In 2021, Baidu's core R&D expenses were 22.1 billion yuan, accounting for 23% of core revenue, an increase of 2.6 billion yuan compared with the 19.5 billion yuan invested in 2020, and Baidu's core R&D expenses accounted for 21.4% of core revenue in 2020. Baidu explained that this is mainly due to the increase in traffic acquisition costs, bandwidth costs, sales costs and other costs related to the newly expanded AI business.

In fact, compared with the data of multiple quarters, the growth rate of its sales costs and research and development expenses has exceeded the growth rate of revenue, which may also be a major reason for the year-on-year decline in net profit. For example, in the fourth quarter of 2021, Baidu's core sales costs increased by 42% year-on-year, and research and development expenses increased by 37% year-on-year, far exceeding the growth rate of Baidu's core revenue. It remains to be seen whether a large amount of capital investment can make Baidu continue to maintain its competitive advantage in the new track.

In addition, as the advertising business as a "cash cow" will continue to be under pressure, Baidu's sustainability is also worth paying attention to. As of December 31, 2021, Baidu's free cash flow excluding iQiyi was 1.596 billion yuan, a decrease from 2.9 billion yuan in the third quarter and a long way from 6.9 billion yuan in the second quarter.

Written by: Nandu reporter Xiong Runmiao