A few days ago, the China Automobile Dealers Association released the 2021 National Automobile Dealers Survival Survey Report, which shows that nearly 30% of dealers completed sales targets last year, and 70% of dealers completed more than 80% of the annual task indicators. Moreover, the profitability of dealers has risen sharply. Dealers are more cautious about future investment and acquisitions, and the brands intended to invest or acquire are mainly concentrated in new energy brands, luxury/import brands and Japanese brands, and the investment intention of independent brands has increased significantly.

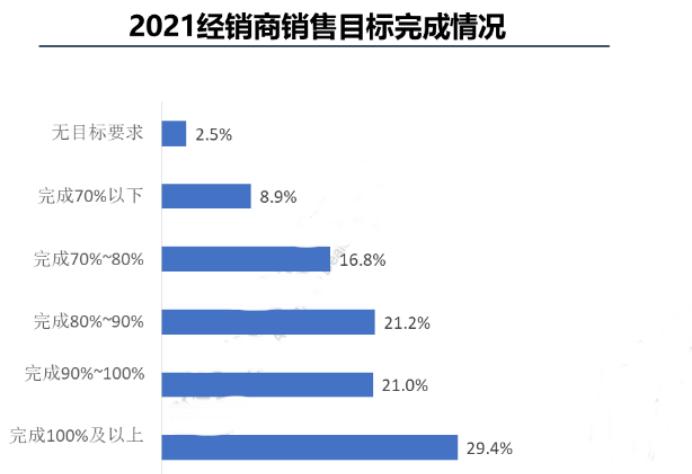

70% of dealers have completed more than 80% of the sales target

In the past year, due to the repeated epidemics, chip shortages and other issues on the domestic passenger car market exerted "braking force", through the industrial chain and supply chain to act in the field of automobile circulation, the operation of dealers has been affected. However, overall, car dealers' satisfaction with OEMs will increase significantly in 2021.

According to the survey, the overall satisfaction score of dealers in 2021 is 82.7 points, and the overall satisfaction of dealers with manufacturers has increased significantly. In terms of brand type, luxury/imported brands scored the highest at 84.8 points, joint venture brands scored 83.6 points, and independent brands scored 78.7 points. The survey results show that dealers have obviously improved their satisfaction with the market order and inventory management, and in 2021, due to insufficient chip supply, products are "in short supply", manufacturers optimize product production, dealer inventory pressure is slowed down, and terminal preferential margins are narrowed, making the overall profitability of dealers better.

The survey shows that despite the impact of chip shortages, 70% of dealers still completed more than 80% of the annual task indicators, while dealers who completed the annual sales target accounted for 29.4%. Among them, the annual target of luxury/import brand dealers is better, and nearly 40% of the dealers have completed the annual sales target. The survey found that the inversion of the sales price of new cars in dealers still exists, but it is significantly better than in 2020, and the proportion of dealers who have not experienced price inversion increased by 2.9 percentage points to 29.4%.

At the same time, the gross profit margin of dealers' new cars improved slightly, from 1.3% in 2020 to 1.5%. The gross profit margin of used cars increased significantly by 3.4 percentage points to 8.5%, and under the impetus of favorable policies in the used car market, dealer groups actively laid out the used car business and achieved initial results.

Dealer profitability has risen sharply

Due to the shortage of chips, the supply is insufficient, which is conducive to dealers digesting inventory and narrowing the profit margin. From the perspective of profitability, the profitability of dealers rose to 53.8% in 2021, and the loss surface fell to 17.5%. In contrast, the overall profitability of luxury/imported brands is better, with nearly 80% of dealers achieving profitability, and the proportion of profitable distributors of joint venture brands and independent brands is less than 50%.

In the profit structure of dealers, the proportion of new car sales profit has increased significantly. Although the repeated epidemic situation and economic downturn have affected the consumer market, the "short supply" of automotive products caused by the shortage of chips has narrowed the preferential range of terminals and increased the profit of new car sales of dealers. In addition, the proportion of profits in the dealer's financial insurance business has decreased significantly. After the 919 insurance premium reform, the insurance commission income of dealers decreased significantly, coupled with the tightening of insurance company policies, the profitability of insurance business declined.

Throughout 2021, multiple factors such as repeated local epidemics and untimely supply of vehicles caused by chip shortages have disrupted the pace of sales and increased the difficulty for dealers to cope with market changes. At the same time, the high cost of customer acquisition and the reduction of passenger flow are the core pain points of dealers. Dealers said that factors such as reduced supply, declining passenger flow, and increased cost of gathering customers are all affecting the conversion of potential customers. In addition, the high rate of after-sales customer churn and the reduction of accident cars entering the store are all challenges that dealers have to face. With the rapid development of the new energy market, the rise of new power brands, especially the substantial increase in sales of new energy passenger cars in 2021, has caused a great impact on the fuel vehicle dealer group.

New energy brands are still hot spots for investment in the future

However, for the future business prospects, nearly 90% of dealers are still optimistic, and the expectation of sales growth is obvious. In view of the different channel models of authorization, direct operation and agency, for investing in new stores, dealers are more inclined to the authorization model, mainly because they are more familiar with the authorized business model, and the autonomy is stronger, and they can independently carry out related businesses. For the agency model, the investor's investment is correspondingly reduced, without bearing inventory, and the operational risk is reduced, but the user maintenance and control of the channel will also be reduced.

Surveys of dealers' intentions to invest in brands show that dealers are more cautious about future investment and acquisitions. According to statistics, the brands intended to invest or acquire are mainly concentrated in new energy brands, luxury/imported brands and Japanese brands, and the investment intention for independent brands has also increased significantly.

Nandu reporter Liang Luozhe