(Report Producer/Author: CITIC Securities, Shimin Hu)

1 Brands accelerate the layout of airport channels, and cagr 16%-18% is expected to be CAGR by 2025

The epidemic has accelerated the localization of consumption, and it is expected that by 2025, the scale of individual luxury repatriation WILL BE 13%-14%

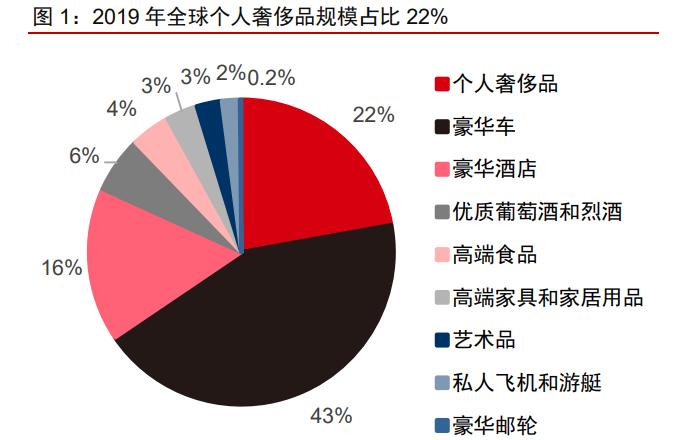

The epidemic has greatly accelerated the return of luxury goods consumption, and in 2020, China's personal luxury goods market has grown by 42% against the trend, and its market share has increased by 9pcts, and the only positive growth and bright performance in the global market. In 2019, the global luxury goods market size was 1.3 trillion euros, mainly composed of personal luxury goods, luxury cars and luxury hotels, of which the personal luxury goods market size of 281 billion euros, accounting for 21.6% ranked second. In 2020, the global luxury goods market fell by 20% to 22% due to the impact of the epidemic, of which the size of the personal luxury goods market fell by 22% year-on-year to 220 billion euros. China's epidemic control effect is leading the world, the economy took the lead in resuming the superimposed outbound policy restrictions to accelerate the return of consumption, and in 2020, personal luxury consumption increased significantly by about 42% to 44 billion euros, making it the only luxury consumer market with positive growth under the epidemic. Benefiting from the sharp growth of luxury consumption in China Against the trend, the share of Asia in 2020 increased by 7pcts to 33% year-on-year, surpassing Europe and the United States to become the largest luxury market, of which the proportion of China increased by 9pcts to 20% year-on-year.

The epidemic has greatly accelerated the return of luxury goods consumption, and by 2025, the global local consumer market will reach 215 billion to 260 billion euros, and airport channels with natural monopoly advantages are increasingly favored by brand owners. Luxury goods sales are highly dependent on the tourism scene, and in 2018, Chinese contributed duty-free income in China or only accounted for 25.6%, and the policy continued to promote the return of consumption. According to Bain & Company, 50% of the world's personal luxury consumption occurred in the travel scene in 2015, and in 2020, this value fell to 10% to 15% in 2020. According to the United Nations World Tourism Organization (UNWTO), the number of global outbound passengers fell by 73% year-on-year in 2020, of which the prevention and control policies in the Asia-Pacific region were more stringent, and international arrivals fell by 84% year-on-year. The epidemic has greatly accelerated the shift of luxury consumption to the local area, about 80% to 85% of personal luxury sales in 2020 will come from the local scene, bain & company expects the global local consumer market to reach 215 billion to 260 billion euros by 2025.

We estimate that the local proportion of China's luxury consumption will increase from 33% year-on-year to 37pcts to 71% in 2020, and it is expected that by 2025, the scale of China's luxury consumption will return to CAGR or 13% to 14%. Since March 29, 2020, China has strictly implemented the "Five Ones" flight and entry quarantine policy, and the number of outbound tourists in the country in 2020 has plummeted by 86.8% year-on-year to 20.33 million, and the number of outbound tourists is expected to be about 25.62 million in 2021, equivalent to 16.6% of the 2019 level. Strict immigration policies and consumer demand brought about by the first recovery of domestic economic activities may become an important support for the growth of China's local luxury market in 2020, and we estimate that the proportion of China's luxury goods consumption will increase from 33% year-on-year to about 37pcts to 71% in 2020. With the global epidemic under control, people's travel returns to normal, due to the high base reasons, the proportion of Local Consumption in China may temporarily decline, but the continuous return of consumption is expected to push up the proportion of Personal Luxury Consumption of Chinese residents in China by about 50% in 2025, that is, 750 to 90 billion euros, corresponding to 13% to 14% CAGR in 2020-25.

Brand owners are accelerating the layout of hub airports, and taxable commercial profitability is expected to meet the inflection point

Airport channel sales accounted for 6% of personal luxury sales in 2019, and are expected to achieve an average annual increase of 4 billion euros in 2019-25, which will be the fastest growing offline channels in the future. From the perspective of sales channels of personal luxury goods, according to Bain & Company statistics, single-brand stores, specialty stores and department stores in 2019 contributed a total of 69% of sales, but Outlets, online stores and airport channels have ushered in high growth rates in recent years, and the compound sales growth rate of the three from 2014 to 2019 reached 14%, 23% and 11% respectively. Among them, the global airport channel sales in 2019 is about 16.9 billion euros, accounting for 6% of the share, Bain & Company is expected to increase to 22 to 25 billion euros in 2025 (an average annual increase of about 4 billion euros), corresponding to CAGR of about 4.8% to 7.2%, or the fastest growing offline channels in the future.

Considering the similarities and differences between luxury goods and airport duty-free categories, as well as the increase in the proportion of consumption in the Chinese market, we expect the total sales scale of China's airport tax-duty-free luxury goods in 2025 to be 75 billion to 80 billion, corresponding to a CAGR of 16% to 18% in 2019-25.

Compared with traditional channels such as department stores and specialty stores, airports with natural monopoly advantages will gain more favor from luxury brands in the future, and the epidemic will accelerate the inclination of brands to airport channels. The airport has a natural monopoly advantage, naturally screening the best passenger flow in the region, closed environment and waiting time are more likely to stimulate passengers' willingness to spend. As luxury brands have become more and more popular in recent years depending on brand image and channel management, airport channels are expected to be more favored. According to Savills, top luxury brands opened more than 33 airport stores between 2016 and 18, while expansion through other channels slowed. Kering, the global luxury leader, received 6% of its sales from the airport in 2019 and has steadily increased slightly since 2014, while the share of traditional department stores and specialty store channels fell by 9pcts and 5pcts in the same period.

The epidemic swept the world in 2020, seriously impacting economic activities and the flow of people around the world, changing the consumption patterns of luxury goods, and accelerating the adjustment of brand owners' layout strategies for various retail channels. Taking Louis Vitton (LV) as an example, according to The Moodie Davitt Report, LV is gradually withdrawing from the city duty-free shops in South Korea, which have declined in performance and have been hit hard by the epidemic, and plan to close its city duty-free shops in Hong Kong in cooperation with DFS, while increasing the brand's layout in the airport channel, planning to open new retail stores at Incheon Airport and Hong Kong Airport, and opening 6 airport stores in China by the end of 2022. Hermès, Chanel, Rolex and other luxury brands continue to favor airports under the epidemic, and actively deploy airports in Zurich, Sydney, Hong Kong, Seoul, Chengdu and other places. (Source: Future Think Tank)

2 Chinese people contribute 90% of the increase in consumption, and the supply pressure of hub airports may be alleviated

Demand for luxury goods is resilient, and the Growth Rate of the Chinese Market leads the world

The global luxury goods market is growing steadily, and it is expected that the size of the personal luxury goods market will quickly recover to the pre-epidemic level in 2021, and the MARKET CAGR may reach 2.7% to 4.7% in 2019-25. With the exception of the 2008 global financial crisis and the 2020 COVID-19 pandemic, the global luxury market has maintained solid growth over the years, but the growth engine has undergone many changes. Taking personal luxury goods as an example, the CAGR of the industry from 2001 to 19 was about 4.7%, and since 1996, it has experienced the stages of sortie du temple, democratization, crisis adjustment in 2008, Chinese consumption acceleration, new normal with deepening online and localization, the new normal, the new crown crisis and recovery. In 2020, hit by the epidemic, the global personal luxury goods market shrank by 22% to 220 billion euros, (according to Bain & Company forecast) in 2021, that is, a rapid rebound of 28.6% to 283 billion euros, returning to pre-epidemic levels, and Bain & Company expects that by 2025, with the continuous development of online and multi-channel layout, the market size is expected to rise to 330 billion to 370 billion euros.

The price elasticity of luxury demand is low, consumers pay more attention to intangible value, and the demand for personalized personality has become a new driving force for luxury consumption. Luxury goods are a type of consumer goods with a high ratio of value to quality, functional value and low price ratio, and consumers pay attention to its intangible value far higher than its tangible value. The value of luxury goods to the top 5 consumer rankings is respectively: high-end quality and materials, scarcity, craftsmanship, value preservation and rewards for themselves (we believe that the premium part of quality and materials and craftsmanship is much higher than the actual cost, and the underlying reason is still intangible value), so luxury goods have the characteristics of weak demand price elasticity, and can also stimulate consumption for value preservation purposes when the price of goods rises.

Taking the duty-free sales data before and after the epidemic at Incheon Airport as an example, the fashion category accounted for 28% of the duty-free sales in 2019 before the outbreak of the epidemic, of which luxury goods accounted for 67%, and the fashion category accounted for 39% of sales in 2020 after the epidemic, of which luxury products rose to 90% of the fashion category. In recent years, as the younger generation has gradually joined the consumer group of luxury goods, the demand for individuality has gradually been projected on luxury goods, and Chinese consumers have led this change from a global perspective.

The increased purchasing power of Chinese consumers has become a new engine of industry growth, contributing 90% of the global industry's growth in 2019. From 2015 to 20, the per capita disposable income of urban residents in China increased from 31,000 yuan to 44,000 yuan, with an average annual compound growth rate of 7.0% (if the impact of the epidemic is excluded, the CAGR was 7.9% in 2015-19). The main luxury consumption scenario before the epidemic is still overseas, and the proportion of global purchases by Chinese consumers has risen from about 15% in 2010 to 35% in 2019 (this proportion shrank to 27% to 29% in 2020, mainly due to the greater restrictions on overseas consumption of Chinese customers), of which Chinese customers contributed about 90% of the market increase in 2019.

Affected by favorable policies, active price reductions by brand owners and the catalysis of the epidemic, the return of consumption has been deepening, and the market share of luxury goods in China has risen to 20% in 2020. In order to promote the return of consumption, since 2015, the import tariffs of clothing, cosmetics, jewelry and other consumer goods have been continuously adjusted, and the maximum one-time reduction is 30pcts. A number of luxury companies have followed suit to reduce domestic prices, and in 2015, top watches such as Piaget and Patek Philippe cut domestic prices by 5%-25%, and brands such as Burberry and Prada cut prices by up to 20%. In 2017, the overall average price spread of luxury goods in China and abroad narrowed from 68% in 2011 to 16%. The formal implementation of the 2019 E-Commerce Law strengthens the inspection and monitoring of daigou; China's luxury consumption is developing rapidly, and brand owners have also taken the initiative to adopt the strategy of narrowing the price difference to expand the Chinese domestic market.

The strict entry policy after the epidemic in 2020 further catalyzed the return of consumption, and the domestic personal luxury goods market grew rapidly from 17.2 billion euros in 2015 to 44 billion euros in 2020, during which the CAGR reached 20.7%, and the global proportion increased by 13pcts to 20%, leading the global market.

Airport channels have become a must-compete place, and production capacity is expected to break through the bottleneck

The airport has a natural monopoly advantage in the region, and its traffic monetization ability has been verified in the duty-free sales of Shanghai Airport. With its unique location and scarce resources, the airport has a monopoly advantage over the diversion of air passengers within its radiation range, that is, for commercial stores in the terminal, the availability of customers is extremely strong, and the traffic is continuous and stable, compared with the shops in the urban area, the possibility of customer loss or diversion is small. For example, Shanghai Airport has outstanding location advantages, radiating high-quality passengers in the Yangtze River Delta, monopolizing the relevant inbound and outbound passenger flow in the region by virtue of international route resources before the epidemic, and the international and regional passenger throughput in 2019 was 38.512 million passengers, accounting for 50.6%, and the duty-free sales reached 13.8 billion yuan in that year, an increase of 21% year-on-year, highlighting the liquidity brought about by the advantages of high-quality passenger flow under the natural monopoly advantage.

During the "14th Five-Year Plan" period, first-tier airports will usher in centralized production capacity investment, fully protect the main business of air transport, and bring opportunities for commercial upgrading. The demand potential of aviation market in first-tier cities such as Beijing, Shanghai, Guangzhou, and Shenzhen is large, and the first-tier airports will usher in concentrated expansion and production capacity launch during the "14th Five-Year Plan" period, and the planned capacity of Beijing Daxing, Shenzhen Bao'an and Guangzhou Baiyun in 2025 will be 72 million, 70 million and more than 100 million passengers. The expansion of the airport will better ensure the good operation of aviation business, while new terminals, satellite halls and other venues will provide the possibility of commercial upgrades.

For example, Baiyun Airport's T1 terminal is designed to have a capacity of 35 million passengers, but the passenger throughput in 2017 has reached 65.81 million passengers, which is seriously overloaded, which has a negative impact on passenger experience and airport management. In 2018, T2 was put into operation, the design capacity rose to 45 million passengers, the one-time tax-free area exceeded 4,000sqm, the capacity utilization rate of Baiyun Terminal in 2019 was 92%, and the overall taxable commercial area was 43,000 to 44,000 sqm, of which T2 still had resources to be developed. At present, the third phase of Baiyun project has started, with a total investment of 54.42 billion yuan, the construction of the fourth and fifth runways, the construction of new T3 terminals and related supporting settings, the space for commercial upgrading is large, and the continuous investment of production capacity is expected to promote the growth of non-aviation business.

BCG estimates that true-luxury customers accounted for only 0.24% of the global population in 2018, which is an optional consumption with a small audience, and the polarization within the industry is obvious, and the main consumers come from people with higher disposable incomes. Overall, luxury goods are still relatively niche optional consumption, according to BCG statistics, the global luxury consumer size in 2018 is about 425 million people, accounting for 5.6% of the global population, of which the annual consumption of more than 50,000 euros (BCG classifies such people as true-luxury customers) only 18.5 million people, accounting for 0.24% of the global population. But true-luxury customers contributed about 30% of the industry's size that year, and BCG expects this proportion to increase to 31% by 2025, indicating that the polarization within the luxury industry is relatively high, and shows a trend of strengthening year by year, and the main consumers come from people with higher disposable incomes.

The air travel penetration rate is highly correlated with economic development, the commercial scene of first-line airports is still high-end consumption, and airports can naturally screen out high-end audiences, and can also provide high-quality business scenarios, with outstanding channel advantages. As an optional consumption of air transport, demand and macroeconomics are highly correlated, and the increase in spending power has driven the increase in the number of flights per capita, and the per capita GDP of the mainland exceeded 10,000 US dollars in 2019, and the per capita number of flights was 0.47. According to TravelSky statistics, in 2018, China's civil aviation passenger population accounted for only 10.3%, the repeat purchase rate of 3.45, especially in the first-tier airports, the commercial, still belongs to the category of high consumption. First-tier airports naturally screen out people with strong purchasing power, and business travelers have a higher awareness and acceptance of luxury brands.

According to McKinsey statistics, the post-80s and post-90s are the main force of Luxury Consumption in China, with the number of customers and the proportion of consumption reaching 71% and 79% respectively, while the age distribution of civil aviation leisure and business travelers is 25 to 40 years old, which is in line with the portrait of luxury target customers. Airports offer naturally enclosed consumption environments, and Airport Council International estimates that each passenger waits at the airport for an average of about 2 to 3 hours, so airports can keep customers staying at almost no cost, while the lack of waiting stimulates the desire to buy. From the perspective of passenger portraits and business scenarios, airports can provide high-quality resources for high-end brand owners, and the channel advantages are outstanding.

The airport is an excellent place to highlight the brand power and is extremely valuable to maintaining the brand image. In the context of the continuous penetration of online shopping, luxury consumers are paying more and more attention to the shopping experience, according to McKinsey statistics, domestic brand stores are more popular with the main consumers after 80-90, accounting for 35% and 44% of their offline shopping stores in 2018. With luxury brands strengthening the maintenance of brand image and the management of various channels, the share of traditional department stores, specialty stores and other channels has gradually shrunk, and the sales scale of single-brand stores with better scenes has continued to expand, increasing by 12% year-on-year in 2019.

As a place to gather public business travelers and a monopoly airport gateway in the region, the airport is an excellent scene for luxury brands to highlight the power of the brand, and the airport store luxury store mostly adopts the form of a special brand store, which can have a better interaction with the target customer group in the terminal. Under the background of China's consumption return and the steady development of the aviation industry, the layout of airports can not only obtain the release of sustained traffic dividends, but also enhance the brand image, which is a "must-compete place" for high luxury. (Source: Future Think Tank)

3 The Stone of Mt. Ta: The Prospect of Airport Luxury from Incheon

Inaugurated in March 2001, Incheon International Airport undertakes international routes from the former Gimpo Airport, becoming the largest international airport hub in South Korea, including 2 terminals, 1 satellite hall and 3 runways, and has been opened to 173 cities in 52 countries by the end of 2019, with a capacity of 77 million passengers. In 2019, Incheon Airport handled 71.17 million passengers, ranking 14th in the world, of which 70.58 million were international passengers, ranking 5th in the world. Incheon Airport is one of the important international aviation hubs in Northeast Asia, located at the midpoint of the two metropolitan lines connecting Beijing and Tokyo, accounting for more than 98% of international passengers in 2020 and a transit rate of 17.4% in 2020, much higher than that of domestic hub airports.

With an extremely high proportion of international passengers, Incheon Airport's commercial development started earlier and its commercial development was more mature, with duty-free sales of US$2.43 billion in 2019, ranking first among the world's airports and being voted "World's Best Duty-Free Sales" by Business Traveler (Asia Pacifc). Incheon's luxury layout began earlier, with Louis Vuitton in Terminal 1 being the world's first airport duty-free shop, and its T2 terminal was put into operation with 20 high-end boutiques at a time, bringing a significant increase in unit price revenue. Although domestic luxury airport boutiques are mainly opened in tax zones, considering that in 2020, in which international passengers account for more than 98% of indyn airports, and the retail format is almost all tax-free, we believe that Incheon still has a greater reference role for domestic airports through the introduction of heavy luxury to enhance commercial value.

Benchmarking the layout of in-house luxury boutiques in Incheon, there is a large room for adjustment in the domestic hub

Incheon Airport's non-air revenue has remained above 60% all year round, the comprehensive deduction rate of tax-free commercial in 2019 is about 38%, and the non-air revenue of domestic aircraft and capital airports has grown rapidly since 2017, accounting for nearly Incheon in 2019. Incheon since 2010

The proportion of non-air revenue of airports has remained above 60%, of which non-air revenue in 2019 was 1.9 trillion won, accounting for 67%. Commercial revenue accounts for 80% of non-aviation revenue, mainly composed of tax-free income, with Incheon's tax-free income of 1.08 trillion won in 2019, accounting for 39% of total operating income. Incheon Airport surpassed Dubai Airport in duty-free sales since 2016 and ranked first in the world in terms of airport sales, achieving sales of US$2.43 billion in 2019, with a combined deduction rate of about 38%.

Compared with the major domestic airports, Pudong Airport and Capital Airport respectively after the tax-free contract was signed in 2017, the proportion of non-air revenue began to increase rapidly with the rapid growth of duty-free sales, reaching 62.7% and 62.2% respectively in 2019, close to Incheon Airport.

The Fashion category of Incheon Airport maintained a high CAGR of 13.8% in 2001-2019, and the luxury product sales in 2019 were 430 million US dollars, and the luxury industry continued to be rich, accounting for less than 5% of domestic airport boutique sales. Incheon Airport has long refined the layout of luxury goods, before 2010, Coach, Fendi, Chanel, Cartier and other brands have been introduced, and in 2011 Terminal 1 introduced the world's first Louis Vuitton airport duty-free shop (while among China's major first-tier airports, except for Hongqiao, which introduced Hermès in 2010, the rest of the heavy luxury was mainly after 2018). From 2001 to 2019, Incheon Airport's Fashion category sales (including luxury goods) rose from US$67 million to US$690 million, with an average annual compound growth rate of 13.8%, maintaining high growth since the start of the voyage.

According to Generation Research, boutique products account for a large proportion of the category structure of duty-free sales at overseas airports. In 2019, in 2019, the proportion of "boutique and other" in Incheon and Changi airports was 36% and 56%, while the proportion of high-quality goods in major domestic airports was less than 5%, and there was a large space for category adjustment and optimization. At present, Incheon Airport has a number of luxury brands such as Hermès and Louis Vuitton, chanel and rolex new stores entered Incheon Airport in October this year, opening new stores of 405 and 212 square meters respectively, and Louis Vuitton plans to open another boutique in Terminal 2 in 2023, and incheon's luxury industry continues to be encrypted.

Incheon Airport has stimulated duty-free sales under the epidemic with FtN, and the proportion of luxury goods in the sales structure has increased, which has become an important factor supporting the recovery of the airport's retail business. The pandemic has led to a sharp drop in duty-free sales at Incheon Airport, which was only $590 million in 2020, down 76.4% year-on-year, and the airport launched Flight to Nowhere (FtN) to stimulate duty-free sales. FtN takes off and lands in Incheon and does not depart to avoid travel bans and quarantines, but due to a brief flight over Japanese airspace and international flight conditions, passengers can make tax-free purchases and receive a cumulative tax exemption of up to $600. From December 2020 to October 2021, about 26,000 people in South Korea used FtN to achieve a total of about US$33 million in duty-free shopping, with a total of US$1,256 per capita (the part exceeding the us$600 limit bears passenger tax), and during the same period, Incheon Airport launched a total of 152 FtN flights with a total of 16,321 passengers.

From January to May 2021, Incheon Airport's FtN luxury goods duty-free sales increased by 8 times, which played a good role in pulling the duty-free business affected by the epidemic. From the perspective of the categories of goods sold, the fashion category is the mainstay, accounting for 61%, and we estimate that luxury goods account for 85% to 90%, an increase of 22 to 27pcts compared with the pre-epidemic level. FtN has partially "restored" the consumption scenario of Korean residents at airports in an innovative way under the epidemic, and its characteristics have certain guiding significance for predicting the commercial development of the airport in the future. As an effective symbol of personal status and personal value, the higher pricing level of luxury products and the stronger resilience of consumption are important factors supporting the recovery of airport retail business when factors such as the external epidemic fluctuate.

High luxury has led to the growth of passenger unit prices, airports have released traffic dividends, and bargaining power is expected to increase

When Incheon Airport Terminal 2 was put into operation, 20 high-luxury boutiques gathered, and the unit price of passengers in 2019 was 16.4% higher than that of T1, and the centralized luxury business format drove the improvement of single-passenger consumption level. Incheon Airport Terminal 2, which was formally commissioned in January 2018, covers an area of 397,000 sqm and will increase the airport's passenger capacity to 68 million passengers after its commissioning, with T2 outperforming T1 in terms of commercial development. At the start of the 2018 flight, the 9597sqm duty-free area (about 60% of the duty-free area of Terminal 1) jointly operated by Lotte, Silla and NWDS, covered a wide range of products such as aroma, tobacco and alcohol, and fine products. The T2's infrastructure is designed not only to improve traffic efficiency, but also to increase the time spent on shopping, such as two passageways leading to the boarding area, which lead passengers to the central duty-free zone. The central area is home to 20 luxury boutiques, including Gucci, Chanel, Hermès and Rolex.

With the commissioning of Terminal 2 and the excellent operation of commerce, in 2018, in 2018, in which duty-free sales at Incheon Airport increased by 16.5% year-on-year to US$2.40 billion, while international passengers increased by 10.0% year-on-year to 67.68 million passengers in the same period, a growth rate of 6.5pcts lower than that of duty-free sales. The unit price increased by 5.9%. According to the Moodie Davitt Report released by Moodie International, T2 passenger throughput accounted for 26% of in 2019 at Incheon Airport as a whole, but 29% of completed tax-free sales were completed, and considering that international passengers accounted for more than 98%, the impact of passenger structure can be ignored. Based on this, we estimate that the unit price of tax-free passengers in Terminal 2 is 38 US dollars, an increase of 16.4% over T1, and we believe that the high-luxury formats concentrated on T2 have a significant pulling effect on the unit price of customers.

From 2012 to 14, LV contributed 3.3 to 5.5% of inland airport duty-free sales, making it the largest store in terms of sales, with outstanding airport channel advantages and a higher level of ping efficiency than that of large stores in the city by 35%-65%. We believe that incheon Airport's advantage in gathering passenger traffic has greatly boosted sales of luxury brands. Take Louis Vuitton as an example: in September 2011, it entered Incheon Airport, which was the brand's first airport store in the world, with an area of 550sqm; the average daily sales volume was about 300,000 US dollars in the 4 to 5 months before the opening of the store, with daily sales of more than 500,000 US dollars in November of that year, and sales of 240,000 US dollars in 2012H1; louis Vuitton Incheon Airport store completed sales of 66.28 to 95.36 million US dollars in 2012-2014, accounting for 3.3% to 5.5% of the overall duty-free sales of the airport in the same period The highest-selling stores, other luxury brands also performed well, with Gucci, Chanel and Cartier completing sales of $42 million, $25 million and $21 million in 2010, respectively.

Lv stores in shopping malls in South Korea's Gangnam region can achieve sales of about 50 million yuan per month, but the area will generally be more than 1.5 to 2 times that of airport stores, if measured based on 2012 data, the incheon airport store's ping efficiency is about 35% to 65% higher than that of the city stores, and the airport's channel advantages are outstanding.

The tender rent of luxury boutiques at Incheon Airport has increased significantly, and it is expected that with the release of traffic dividends, the bargaining power of the airport may be improved, bringing about an increase in the level of income. When Louis Vuitton moved into Incheon Airport in 2011, the contract with Shilla Duty Free and Airport was a guaranteed rent of 5.5 billion won/year (about US$5.1 million at the 2012 exchange rate, and 10 million won/year for Hedanping) and a 7% sales deduction rate, while other duty-free shops generally had a deduction rate of about 20% in the same period. Incheon Airport took the initiative to make profits to stimulate Louis Vuitton's business momentum, and with the increase in luxury brand sales, the value of the airport channel gathering passenger flow has become increasingly prominent, which provides a premium for a new round of bidding. According to moodie Daviitt Report, in 2015, the bidding single floor guarantee of Incheon Airport boutique rose to 33.88 million won/sqm, an increase of more than 2 times compared with the level of LV stores opened in 2011, at this level, LV, Hermès and other top luxury may indeed enjoy preferential treatment in rent, but overall, with the continuous release of airport dividends, the preferential margins they give to brands may gradually narrow.

At present, the domestic airport for the introduction of high luxury generally does not adopt the ordinary bidding model, but the airport takes the initiative to invite, sign a contract different from the ordinary taxable business, we expect that the contract is also the use of guaranteed rent + deduction point commission, but considering the high efficiency of high luxury, the brand will enjoy a large degree of preferential treatment in the early stage. However, we believe that as airports and brands cooperate to increase sales, airports may usher in an increase in bargaining power, which will lead to an increase in the level of revenue.

Incheon Airport has been actively laying out luxury sales since the early days, with T2-intensive boutiques bringing an increase in unit prices, and the airport enjoying the rent benefits brought by high sales, while also increasing its bargaining power. From the perspective of domestic airports, with the launch of production capacity ushered in the opportunity of commercial upgrading, in addition to the basic retail catering, if we can learn from overseas experience, actively seek changes and optimize various formats, it is expected to increase the unit price level of customers and realize the upgrading of traffic realization logic.

4 Taking the two sessions in Shanghai as an example, luxury goods opened the second growth curve of commerce

Hongqiao, Bao'an and Daxing airports are more preferential in bidding for luxury goods, and the newly opened Aerospace Airport fully taps the value of traffic realization with high-end brands and innovative layouts. Compared with South Korea, Singapore and other places, China's domestic airports have opened their luxury layouts late. At present, among the domestic airports, Hongqiao Airport, Shenzhen Bao'an Airport, Daxing Airport and the newly opened Chengdu Tianfu Airport have more prominent performance in terms of luxury investment in tax areas, and Hermès has settled in Hongqiao and Daxing in 2010 and 2019 respectively, and plans to enter Chengdu Tianfu Airport this year. Among them, Chengdu Tianfu International Airport opened in June 2021, and set up a famous product area covering an area of about 2700 square meters in the tax area of Terminal 2, and 14 luxury goods such as Louis Vuitton, Dior, Gucci, Hermès have been settled, and Dior (non-fragrant) and Balenciaga are the brand's first airport tax stores in China. "Jin Luxury Hui" is set up in Tianfu Airport after the T2 security check, enjoying full "exposure", and Tianfu Airport adopts the mode of departure and arrival mixed flow, which increases the traffic of commercial crowds and fully taps the value of traffic monetization with high-end brands and innovative layouts.

Hongqiao Airport has a leading location advantage and a well-known commercial operation ability in the industry, and in 2020, it was selected by Skytrax as "the best airport for passenger experience in the airport with 40 million to 50 million passenger throughput". According to the statistics of Winshang Network, Hongqiao has 4.89 stores per 10,000 square meters, ranking first among the major airports in first-tier cities, and the number of shopping shops accounts for about 72% of the highest, which is the "most commercial" airport, the number of luxury stores accounts for 7.4%, and it is also the "most expensive" airport. We believe that among the major airports in first-tier cities, Hongqiao is the most competitive airport for the development of luxury goods, and we will take Hongqiao as an example to explore the driving effect of heavy luxury accommodation on domestic airport business.

Asset restructuring will bring about resource optimization and promote the two-way development of Shanghai's two non-aviation businesses

Asset restructuring is about to land, the transaction valuation is reasonable, the problem of competition in the same industry has been fundamentally resolved, the advantages of the core airport in the Yangtze River Delta have been strengthened, and the two resource allocations are expected to usher in substantial optimization. On November 30, 2021, Shanghai Airport issued the Report on the Issuance of Shares to Purchase Assets and Raise Supporting Funds and Related Party Transactions (Draft) and Asset Appraisal Report, in which the Company intends to issue shares to purchase the following assets: 100% equity of Hongqiao Company, 100% equity of Logistics Company and Pudong Fourth Runway, with transaction prices of 14.516 billion, 3.119 billion and 1.497 billion yuan respectively, with total assets of 19.13 billion yuan and corresponding to the number of issued shares of 434 million shares and 22.5% of the current share capital.

Among them, the appraisal value of Hongqiao Aviation and supporting assets is 9.949 billion yuan, corresponding to about 1.3 times the PB; the appraisal value of the right to use the advertising position is 3.655 billion yuan, and the PE is 13.77 times; the equity appraisal value of 49% of the domestic advertising company is 912 million yuan, and the PE is 9.3 times. After the completion of the transaction, the shareholding ratio of Shanghai Airport Group in the joint-stock company will increase by 12.1pcts to 58.4%, the two formal mergers in Shanghai, the problem of competition in the same industry has been fundamentally solved, the allocation of resources in the two fields is expected to usher in a substantial optimization, and the competitiveness of Shanghai International Airport will be further strengthened. We expect to increase throughput to 180 million passengers in 2025, creating a world-class aviation hub with leading quality."

Pudong Airport's tax-free dividend has been postponed rather than disappeared, and we expect its sales to be close to 50 billion yuan in 2025, and its bargaining power will be significantly improved when the contract is re-signed. Pudong Airport's post-epidemic duty-free sales are expected to hit the level of nearly 50 billion yuan, and the original contract under the epidemic has been re-signed due to the force majeure factor of the sharp reduction of the international line, and the guarantee has been cancelled and the mode of confirming the income by international passenger flow has been adopted. Under the epidemic situation, the dividends of new channels such as Hainan outlying islands and online direct mail have continued to escalate, while airport channels are almost absent, and the domestic tax exemption pattern has undergone major changes, but we believe that the channel dividend of Shanghai Airport has only been postponed and has not disappeared. Although there has been a disturbance of Omicron strain recently, but the confirmed cases are mostly mild, we do not think it is necessary to be too pessimistic, it is expected that from 2022Q2, the opening of the international line is still a high probability event, it is estimated that the passenger throughput of Pudong Airport International + Region in 2025 is expected to exceed 53 million person-times, if the unit price of consumption upgrades is increased to 938 yuan, the corresponding tax-free sales or close to 50 billion yuan, the corresponding comprehensive deduction rate under the framework of the supplementary agreement is only 15%.

The two have the advantage of in-depth cooperation to make the port channel cake bigger, and the sales of 50 billion yuan are extremely attractive to duty-free operators, and under the background of the opening of tax-free licenses and the gradual decentralization of the operator pattern, it is expected that the premium capacity of the machine will be significantly improved when the contract is re-signed. Assuming that the comprehensive deduction rate in 2026 is increased to 25% to 30%, it is expected that the tax-free income of Shanghai Airport will increase significantly by 95% to 135% year-on-year to 14.6 to 17.6 billion yuan, and the performance will usher in greater flexibility.

The policy positioning upgrade superposition and Pudong open resource sharing, the Hongqiao route structure is expected to usher in optimization, traffic monetization capacity or further enhanced. According to the "Overall Plan for the Construction of Hongqiao International Open Hub" issued by the National Development and Reform Commission, Hongqiao Airport will strengthen the function of international air transport, apply for the expansion of duty-free shopping venues, and carry out the pilot project of "buy and refund" for departure tax rebate. At present, the tax-free area of Hongqiao Airport is about 2000sqm. Previously, Hongqiao was constrained by competition in the same industry and its development was restricted, in 2019, the international passenger throughput of Hongqiao Airport was 3.421 million passengers, accounting for 7.5%, which was 42.5% lower than the international passenger proportion of Pudong Airport in the same period.

With the relocation of Dachang Airport, Hongqiao Airport is expected to usher in peak hour expansion during the "14th Five-Year Plan" period, policy upgrades and resource optimization, and it is expected that Hongqiao Airport will be further encrypted in the express line, and the international line moment may usher in an increase. Hongqiao aims at the positioning of fine business, and if it creates high-quality international flights after the opening of the national gate, it is expected that the passenger structure will be further optimized and the traffic realization ability will be enhanced. At the same time, the advertising position of Hongqiao Airport is operated by JCDecaux Momentum, and the media quality is leading the domestic airport, and it is expected to increase the media space in the future, and coordinate with the boutique business within the airport to improve the quality of resources.

Shanghai's two future differentiated advantages are expected to develop a network of characteristic routes. Pudong maintains its position in the duty-free market after the opening of the international line, taps the value of international passenger traffic realization, Hongqiao captures traffic hotspots, enhances the upgrading of taxed businesses, and improves the level of income. Through the two-way development of non-aviation business, the company may realize the "internal and external repair" and "attack and defense" in the post-epidemic era.

In the future, high luxury is expected to increase net profit by 60 million to 70 million, and the commercial value of Hongqiao will be further improved

Hongqiao Airport's first-line inter-flight flights and express flights account for a relatively high proportion, accounting for 60% of business passengers in 2019, and passenger flow resources provide advantages for commercial development. Hongqiao Airport is positioned as a boutique airport with distinctive business characteristics, and the proportion of commercial routes is leading among domestic airports, and the number of first-line inter-flight commercial routes from Hongqiao to Beijing and Guangzhou-Shenzhen in the new season of winter and spring 2021 is 35.8%, leading daxing, Baiyun and other first-tier city airports, and the proportion of express lines is high, accounting for 75.8% of the outbound flights. According to the company's statistics, about 60% of hongqiao airport passengers in 2019 are business travelers, and the resource advantages of high-quality passenger flow provide fertile soil for the commercial operation and development of Hongqiao Airport, and its commercial facilities, introduced retail, catering brands, etc. are ahead of other first-tier airports in terms of fashion trends and pricing levels.

Hongqiao has significant location advantages, which is suitable for the development of high-luxury formats to achieve the upgrading of traffic realization. As an important airport in the Yangtze River Delta region, Hongqiao Airport has obvious location advantages and many potential target customers in the radiation area. The per capita income of urban residents in Shanghai has always been at the forefront of the country, with 76,000 yuan in 2020 (the national average of 32,000 yuan), and the Mob Research Institute report shows that Shanghai's luxury consumers accounted for 8.4% in 2019, ranking second in the country's first- and second-tier cities (Beijing accounted for 9.7%), much higher than the third-place Chongqing's 3.7%. At the same time, the awareness and consumption ability of public merchants on luxury goods are higher, Hongqiao Airport screens out the target customer groups for brand owners, which is an ideal scene for luxury stores, and the airport relies on the brand power of international brands to upgrade the logic of traffic realization.

Hongqiao Airport adjusted the structure of taxed businesses through the introduction of luxury goods, catering "first stores", etc., and the retail revenue of single-passenger catering in 2021 increased by 29.4pcts compared with 2019. In 2019, Hongqiao Airport's non-aviation revenue accounted for about 48%, and under the epidemic situation, it actively captured traffic hotspots and mined commercial value in terms of taxes, and improved the income level of non-aviation business through the optimization and adjustment of the structure of the settled business format. In 2020, Terminal 2 ushered in lv, Zumalong (the first airport store in China) and other brands to settle in, as of July 2021, the "first-line brand avenue" has gathered 18 international first-line brands, and the two terminals have a total of 23 "first stores" of well-known domestic and foreign catering brands, including shake shack, Yanyue Mountain, etc. In 2020 and 2021H1 Hongqiao Airport,021,000,000,000,000,000,2021,2021,2021,102,2021,100,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,000,

In "Logistics and Mobility Services 2022 Investment Strategy – Finally Crossing the Mountain, Going with the Flow" (2021-11-05), we benchmarked the revenue generation capacity of Hongqiao's luxury stores with Shanghai Plaza 66, and if measured at a 15% deduction rate, the rental efficiency level of luxury business formats is about 3.2 times that of other taxable retail restaurants. At present, there are about 300 to 400 square meters of high-end luxury boutiques in Hongqiao Airport, considering that it is constantly optimizing the non-aviation revenue in the tax area by adjusting the business structure and innovating the business model, we do a flexible calculation of the impact of the introduction of luxury goods on the company's revenue, the basic assumptions are as follows:

1. Ping efficiency level, considering that the Lui Vuitton store at Incheon Airport is 135% to 165% of the city's largest stores, from pessimism to optimism, we assume that the ping efficiency of Hongqiao Airport Store can reach 80%, 100%, 120% and 150% of Shanghai Plaza 66 respectively.

2. High luxury area, since Hongqiao Airport has no expansion plan in the short term, it is expected that the adjustment of business formats will be mainly based on the mutual transformation of the stock area. The penetration rates of T1, T2 and Chengdu Tianfu Airport were 12.1%, 18.4% and 9.3% respectively. At present, Hongqiao Airport has a tax area of about 23,000 square meters of commercial area, considering the operating conditions, from pessimism to optimism, we assume that Hongqiao Airport has 5%, 8%, 12%, 15% of the area can be used for the layout of luxury goods.

3. Rent deduction rate, the average rent deduction rate of Hongqiao Airport in the tax area is about 20%, considering that Incheon Airport is actively giving profits in the introduction of heavy luxury formats, giving preferential treatment to brands with lower deduction points, domestic airports may be able to imitate, so from pessimism to optimism, we assume that the sales deduction rate of heavy luxury shops at Hongqiao Airport is 10%, 15%, 20%.

According to the calculation results, the driving center of heavy luxury formats on Hongqiao's retail catering revenue is roughly 22% to 26%, considering that almost all of the marginal benefits brought about by the adjustment of business formats, we expect to bring about 60 million to 70 million yuan of hongqiao net profit improvement.

We expect Hongqiao to make a profit of 740 million yuan in 2025, and the total of the three assets will bring about 1.05 billion yuan in net profit. Based on the above calculations, superimposed on the speculation of Hongqiao's future passenger flow, we predict that Hongqiao Airport may achieve a net profit of about 740 million yuan in 2025, corresponding to a CAGR of 6.3% in 2019-2025; referring to the logistics asset performance commitment given by the company, we expect that the logistics company may achieve a net profit of about 230 million yuan in 2025; in 2019, Shanghai Airport will pay the fourth runway of the group of 160 million yuan, and the annualized depreciation after incorporation into the listed company is about 40 million, that is, the cost savings of 1.2 About 100 million yuan. Therefore, it is expected that the three assets will bring a net profit increase of 1.05 billion yuan to the company in 2025.

If the deduction point is re-signed to 25% to 30%, it is expected that the profit on the machine in 2025 will increase to 15 billion to 18 billion yuan. If you do not consider asset restructuring, Shanghai Airport is expected to achieve a net profit of 7 billion to 7.5 billion yuan in 2025, and the overall profit of the aircraft after the assets are merged may exceed 8 billion to 8.5 billion yuan. In 2026, the tax-free contract will be re-signed, and with the expansion of sales, the bargaining power of the airport will rebound, and if the deduction rate in the re-signed contract is 30%, it is expected that the profit on the aircraft will rise to 16 billion to 18 billion yuan, and the performance is expected to usher in greater flexibility.

(This article is for informational purposes only and does not represent any of our investment advice.) For usage information, see the original report. )

Featured report source: [Future Think Tank]. Future Think Tank - Official website