Ren Zeping: Get out of deflation and start a "new" round of economic stimulus

Zeping macro

2024-06-13 14:34Posted in Beijing Finance and Economics Creators

Text: Ren Zeping's team

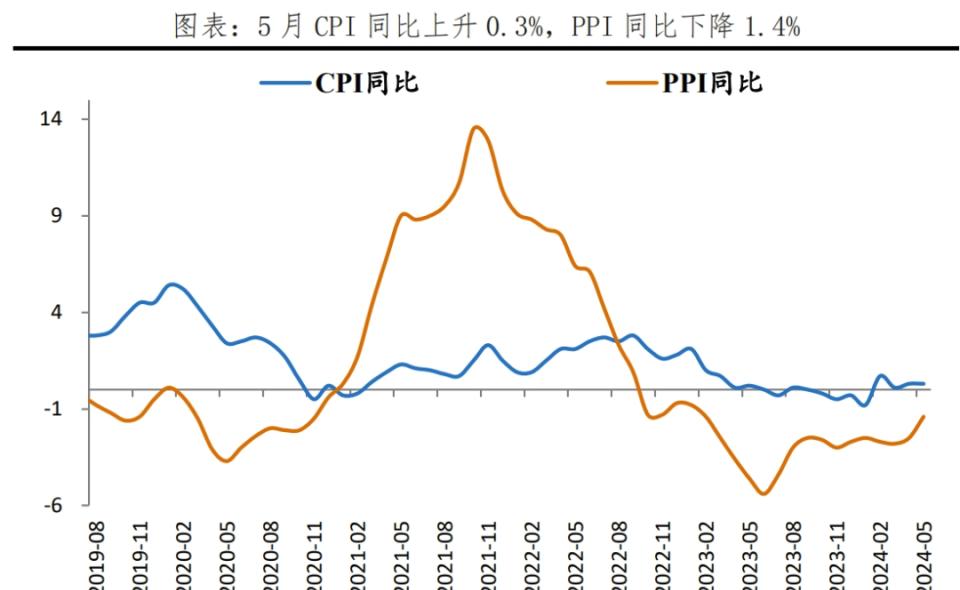

CPI rose 0.3% year-on-year in May, and the previous value rose 0.3%; PPI fell 1.4% year-on-year, and the previous value fell 2.5%.

1 Prices are low, out of deflation, and a "new" round of economic stimulus is launched

CPI and PPI continue to be sluggish, reflecting insufficient domestic demand. PPI has been negative for more than a year and a half, and corporate profits have been under pressure, affecting investment momentum. The CPI has been around 0% for a long time, indicating that household consumption is sluggish, which is still in the context of the recent start of the pig cycle, and the deflationary pressure after excluding pig prices is highlighted.

In May, CPI and core CPI fell back to negative growth month-on-month.

The decline in PPI narrowed, mainly due to the rise in upstream commodity prices such as non-ferrous black, which is an input factor, and the upstream manufacturing price has increased and the cost has increased, which has further squeezed the downstream profit margins.

Although the nominal interest rate on the mainland has continued to fall, the real interest rate after excluding inflation is at a high level, and the real interest rate is high in the world.

The time has come to prevent deflation and prevent a balance sheet recession. We usually know that hyperinflation is bad, income redistribution effects, market price signals are out of order. However, deflation is not good, such as the Great Depression of 1929, massive unemployment, bankruptcies, bank failures, and economic and social unrest. So mild inflation deleveraging is the best option, better than deflationary deleveraging and hyperinflation, which is why the Fed has set its monetary policy target at 2% of prices, not 0.

The way out of deflation, the "liquidity trap" and the "balance sheet recession" lies in a "new" round of economic stimulus, expanding aggregate demand through fiscal expansion, and at the same time increasing support for the new economy and new quality productivity. Bring inflation back to moderate levels as soon as possible and avoid deflationary deleveraging.

Historical experience shows that deleveraging from hyperinflation and deflation is not advisable.

A classic example of hyperinflation, such as Argentina, was once labelled as a debt default and hyperinflation. The industrial structure is single, and the ability to generate export income is limited; Large-scale infrastructure construction for the development of the domestic economy, excessive and advanced high welfare spending, fiscal deficits; It can only rely on external debt and a large amount of money printing to make up for the deficit, the domestic hyperinflation, the inability of foreign exchange reserves to repay foreign debts, the default of debt on a total of nine times, and the continuous rise in the social poverty rate.

In the process of deflation and deleveraging, households and enterprises reduce spending and investment, forming a negative "consumption-production" cycle, which is painful and can easily lead to economic stagnation. For example, after the bursting of Japan's asset bubble in the 90s, the balance sheets of corporate households declined, the bad debt ratio of banks continued to rise, and the problem of non-performing loans continued to ferment. In 1997, the banking crisis led to the collapse of medium-sized institutions such as Sanyo Securities and Yamaichi Securities, and Japan has since fallen into long-term stagnation and chronic deflation. It took 15 years for the problem of non-performing loans to be resolved until Junichiro Koizumi came to power and the government injected capital on a large scale and relied on market forces to rectify the problem.

After the introduction of the 517 real estate portfolio, there are signs of bottoming out in first- and second-tier cities, but they are still at a low level. From May 17 to June 11, the number of units and area of commercial housing sales were -34.7% and -35.4% year-on-year respectively, and the decline was only slightly narrowed; The reason is that the demand side is subject to the lack of residents' purchasing power and expectations, and the supply side is subject to the inventory of new houses, and the listing of second-hand houses still needs to be destocked. Real estate has entered the era of stock, and the relationship between supply and demand and residents' expectations have changed.

On June 7, the National Standing Committee sent three major signals: the acceleration of the implementation of the collection and storage policy, the increase in inventory, and the new policy reserve.

The new reserve policy proposes housing banks and a "new" round of economic stimulus. Real estate and the economy should have a follow-up reserve policy to prevent another pullback from dampening market confidence. For example, the re-lending of storage housing has been gradually increased from 300 billion yuan to 1 trillion yuan, transaction taxes and fees and interest rates on existing housing loans have been reduced, new infrastructure projects have been launched to expand fiscal expenditure, green power stations and charging piles have been vigorously built, and birth subsidies have been encouraged. (See "Ideas for the Establishment of a Housing Bank", "Is It Time to Start a "New" Round of Economic Stimulus, "Current Economic Situation and Responses")

It is an important and correct step to collect and store inventory for affordable housing, and 300 billion refinancing is the first step, and more than 3 trillion housing banks will be needed in the future. At the same time, we will establish a large-scale housing security system, solve the liquidity of high-quality real estate enterprises and local finance, alleviate financial risks, and improve people's livelihood. Many places are actively exploring the combination of destocking and affordable housing and talent housing.

First-tier cities in Beijing, Shanghai, Guangzhou and Shenzhen can consider relaxing restrictions on the purchase of luxury homes. There is a market for the high-end, and there is a guarantee for the low-end. If you are willing to buy a luxury house, pay more taxes, and contribute more to the development of the city, there is no need to suppress it. Just protect what you need.

There is still room for the interest rate of the existing mortgage to be reduced. The interest rate of the existing mortgage is still high, although the lower limit of the interest rate of 5YLPR and the first home loan has been lowered many times, the "fixed markup" level of the existing mortgage is still high, and the lower limit of the incremental mortgage interest rate has been cancelled by the 517 policy, and the interest rate spread has further increased.

The property market can be regulated in more optimal ways such as linking people and land and increasing the supply of land in hot cities to achieve a balance between supply and demand.

China's economic development potential is huge, as long as substantial and effective measures are taken to develop new quality productivity, new infrastructure and new energy, boost confidence in the stock market and property market, protect the vitality of the private economy, and liberalize and encourage childbirth, confidence will be greatly boosted, and confidence is more important than gold. In this way, there is great hope for our economy.

2 The price data for May showed the following characteristics:

1) The CPI was the same year-on-year as the previous month, with a seasonal decline month-on-month. The CPI in May was 0.3% year-on-year, the same as the previous month; -0.1% month-on-month, higher than seasonal; The core CPI was 0.6% year-on-year, down 0.1 percentage points from the previous month, and the core CPI was -0.2% month-on-month, down 0.4 percentage points from the previous month.

2) The year-on-year growth of food items has been negative for 11 consecutive months since July last year; The decline narrowed this month, with prices of most food items falling and rising prices of pork and fresh vegetables. Food items decreased by 2.0% year-on-year, 0.7 percentage points narrower than the previous month, and increased from -1.0% to 0 month-on-month.

3) The growth momentum of service consumption weakened slightly, and the price of durable goods continued to fall for 8 months year-on-year. Non-food products were 0.8% year-on-year, down 0.1 percentage points from the previous month. In 2023, the average consumer price of services will be around 1.0%, and in 2024, the price of services has been 0.8% year-on-year for three consecutive months; -0.1% month-on-month, weaker than seasonal; Household appliances, vehicles and communication tools fell by 0.9%, 4.7% and 2.5% respectively year-on-year.

4) Pig prices rebounded month-on-month, and the "pig cycle" entered an upward period, with little room for growth in this round. In May, the pig price was 4.6% year-on-year, up 3.2 percentage points from the previous month, and 1.1% month-on-month, up 1.1 percentage points from the previous month. It has been 13 months since the production capacity was degraded; The pig feed ratio has risen significantly; The production capacity stock is close to the equilibrium point, and the situation of oversupply is about to be reversed; However, the concentration of the industry has increased, and the price fluctuations of the new pig cycle may be smaller than that of the traditional pig cycle. The proportion of large-scale farms with more than 500 heads slaughtered has increased from 36.6% in 2011 to 65% in 2022.

5) Since 2024, the overall PPI has shown that it is difficult for upstream price increases to be transmitted to the middle and lower reaches, and the prices of domestic and foreign priced commodities are differentiated; PPI improved slightly in May, ending six months of negative growth month-on-month, and narrowing the year-on-year decline. price improvement in the ferrous metal industry chain; The overall price of the petrochemical industry chain has fallen; The price of non-ferrous metal industry chain continues to rise; Prices of high-tech-related industries fell; Glass manufacturing, cement manufacturing and other infrastructure and real estate-related industries continued to decline; Manufacturing prices for consumer goods continued to decline. For example, the price of crude oil rose in the first four months, but the price of the middle and lower reaches of the petrochemical industry chain fell; Crude oil and copper priced overseas have risen in turn, while the price of ferrous metal industry chain priced domestically is weak. PPI rose from -0.2% to 0.2% month-on-month in May; PPI fell by 1.4% year-on-year, 1.1 percentage points narrower than the previous month.

3 CPI is low, and service momentum is weakening

The CPI in May was 0.3% year-on-year, the same as the previous month; -0.1% month-on-month, higher than seasonal. The core CPI, excluding food and energy prices, was 0.6% year-on-year, down 0.1 percentage points from the previous month, and the core CPI was -0.2% month-on-month, down 0.4 percentage points from the previous month. In the year-on-year change in CPI in May, the carryover effect was about 0, and the new price increase factor was about 0.3 percentage points.

The year-on-year growth of food items has been negative for 11 consecutive months since July last year; The decline narrowed this month, with prices for most food items falling and pork and fresh vegetables rising. In May, food items fell by 2.0% year-on-year, 0.7 percentage points narrower than the previous month, affecting the CPI by about 0.37 percentage points year-on-year, and the month-on-month increase from -1.0% to 0. In May, fresh vegetables and pork were 2.3% and 4.6% year-on-year respectively, up 1.0 and 3.2 percentage points from the previous month.

Non-food items drove the CPI up by nearly 70% year-on-year, the growth momentum of service consumption weakened slightly, and the prices of durable goods continued to fall. Non-food products were 0.8% year-on-year, down 0.1 percentage points from the previous month, and non-food products were -0.2% month-on-month, down 0.5 percentage points from the previous month.

Among the seven categories, the price of transportation and communication decreased year-on-year, and the price of the rest increased. In May, clothing, housing, transportation and communications, education, culture and entertainment, medical care, daily necessities and services, and other goods and services were 1.6%, 0.2%, -0.2%, 1.7%, 1.5%, 0.8%, and 3.6% year-on-year, respectively, with changes of 0, 0, -0.3, -0.1, -0.1, -0.6 and -0.2 percentage points from the previous month.

From the perspective of breakdowns, 1) the trend of consumer prices for services is declining. In 2023, the average consumer price of services will be around 1.0%, and in 2024, the price of services has been 0.8% year-on-year for three consecutive months; -0.1% month-on-month, weaker than seasonal. 2) The price of durable consumer goods has fallen year-on-year for 8 consecutive months. In May, household appliances, transportation and communication tools fell by 0.9%, 4.7% and 2.5% year-on-year respectively, with changes of -0.6, -0.4 and 0.4 percentage points from the previous month.

4 Pig cycle: year-on-year and month-on-month continued to rise

In May, pig prices rebounded year-on-year and month-on-month. In May, the pig price was 4.6% year-on-year, up 3.2 percentage points from the previous month, and 1.1% month-on-month, up 1.1 percentage points from the previous month. As of June 11, 2024, the average wholesale price of pork was 24.6 yuan/kg.

We judge that the "pig cycle" has entered an upward period, and there is little room for upside in this round.

First, it has been 13 months since the production capacity was reduced. According to the law of history, the continuous reduction of production capacity for about 10 months will be transmitted to the pig price. In March 2023, the number of fertile sows was 2.9% year-on-year, and in April 2024, the inventory of fertile sows was -7.0% year-on-year, which has been depleted for 13 months.

Second, the production capacity is close to the equilibrium point, and the situation of oversupply is about to be reversed. At present, there are 39.86 million sows in the herd, and the normal number of sows is 39 million, which is still slightly more than the normal number. Under the current deregulation rate, it may decline rapidly until it breaks through the lower limit of 35.88 million heads.

From the perspective of the historical pig cycle, the two rounds of pig cycles that began in 2014 and 2018 both experienced 2-3 quarters of rapid production capacity decline before the price rose sharply. Among them, the year-on-year decline in the production capacity of fertile sows has remained above -20% for many months, and the rapid reduction of production capacity has also created space for pig prices to rise.

Third, the pig food ratio has risen significantly. As of May 31, the pig-to-food ratio has reached 7.21, accelerating upwards since March 15, when it first broke out of the excessive decline range (the pig-to-food ratio was below 6). Historically, the pig-to-food ratio is expected to see a rapid upward movement in the pig cycle after breaking through 7.

The concentration of the industry has increased, and the price fluctuations of the new pig cycle may be smaller than that of the traditional pig cycle. Many small-scale farms were out of the market in 2018 in swine fever, accelerating the process of increasing industry concentration. After African swine fever in 2018, the proportion of 13 listed companies in the country increased by about double to 14.3% in 2021; The proportion of large-scale farms with more than 500 heads slaughtered has increased from 36.6% in 2011 to 65% in 2022. The increase in industry concentration may bring economies of scale, the production capacity of large-scale breeding institutions will continue to increase, and the irrational behavior of "chasing up and killing down" will decrease.

5 PPI ended six months of negative growth month-on-month

Since 2024, the overall presentation of PPI has shown that it is difficult for upstream price increases to be transmitted to the middle and lower reaches, and the prices of domestic and foreign priced commodities are differentiated. For example, in the first four months, the price of crude oil rose, but the price of the middle and lower reaches of the petrochemical industry chain fell; Crude oil and copper priced overseas have risen in turn, while the price of ferrous metal industry chain priced domestically is weak.

PPI improved slightly in May, ending six months of negative growth month-on-month, and narrowing the year-on-year decline. PPI rose from -0.2% to 0.2% month-on-month in May; PPI fell by 1.4% year-on-year, 1.1 percentage points narrower than the previous month. In the year-on-year change in PPI in May, the carryover effect was about -0.9 percentage points, and the new impact of this year's price changes was about -0.5 percentage points.

From the perspective of ex-factory prices of industrial producers, the prices of means of production turned from negative to positive month-on-month, and the prices of means of subsistence continued to decline month-on-month; Prices of food and durable items fell. In May, the prices of means of production and means of living were 0.4% and -0.1% month-on-month, respectively, up 0.6 and 0 percentage points from the previous month.

In terms of sub-items, the prices of extractive industries, raw materials and processing industries were 0.2%, 0.9% and 0.1% month-on-month, respectively, an increase of 1.2, 0.6 and 0.5 percentage points from the previous month, and the prices of food, clothing, general daily necessities and durable consumer goods were -0.2%, 0.1%, 0% and -0.3% month-on-month, respectively, a change of -0.1, 0.1, -0.3 and 0.2 percentage points from the previous month.

From the perspective of the industry, the price of the petrochemical industry chain fell as a whole; The price of the ferrous metal industry chain has improved, and the price of the non-ferrous metal industry chain has continued to rise; Prices of high-tech-related industries fell; Glass manufacturing, cement manufacturing and other infrastructure and real estate-related industries continued to decline; Manufacturing prices for consumer goods continued to decline.

1) The overall price of the petrochemical industry chain has fallen. In May, the oil and gas extraction industry, rubber and plastic products industry, non-metallic mineral products industry, chemical fiber manufacturing and pharmaceutical manufacturing industry decreased by 2.1%, 0.2%, 0.8%, 0.2% and 0.1% month-on-month respectively, with changes of -5.5, 0, 0.2, 0 and 0 percentage points from the previous month.

2) The price of ferrous metals and non-ferrous metals industry chain has risen, of which the ferrous metal industry may be related to the acceleration of local bonds in May and the high demand for high temperature in summer; The non-ferrous metals industry is mainly due to the increase in the price of copper and other products priced overseas. In May, the coal mining and washing industry, ferrous metal mining and dressing, non-ferrous metal mining and dressing, petroleum, coal and other fuel processing industry, ferrous metal smelting and rolling processing industry, and non-ferrous metal smelting and rolling processing industry were 0.5%, -0.1%, 4.4%, 1.0%, 0.8% and 3.9% month-on-month, respectively, an increase of 3.5, 5.7, 1.0, 0, 3.3 and 0.7 percentage points from the previous month.

3) The price of high-tech industries fell, mainly due to overcapacity. The manufacturing prices of lithium-ion batteries and new energy vehicles decreased by 0.5% and 0.2% respectively; Computer, communication and other electronic equipment manufacturing, general equipment manufacturing and automobile manufacturing decreased by 0.2 percent, 0.1 percent and 0.3 percent month-on-month, an increase of 0, 0.2 and 0.3 percentage points from the previous month, and the manufacturing of railways, ships, aerospace and other transportation equipment increased by 0.1 percent month-on-month, an increase of 0.1 percentage points from the previous month.

4) Glass manufacturing, cement manufacturing and other infrastructure and real estate-related industries continued to decline. The price of building materials continued to decline, and the prices of glass manufacturing and cement manufacturing fell by 1.2% and 0.8% respectively.

5) The price decline in the consumer manufacturing industry is mainly due to the lack of downstream demand, and the CPI food item price is negative. In May, the agricultural and sideline food processing industry, food manufacturing, wine, beverage and refined tea manufacturing industry decreased by 0.5%, 0.2% and 0.1% month-on-month, with a change of -0.1, 0 and 0 percentage points from the previous month.

The purchase price rose and fell, the price of ferrous and non-ferrous metals, and petrochemicals increased, and the rest of the prices fell. In May, fuel power, ferrous metals, non-ferrous metals, chemical raw materials, wood pulp, building materials, agricultural and sideline products, and textile raw materials were 0.2%, 0.2%, 3.6%, 0.1%, 0.2%, -0.5%, -0.4%, and -0.1% month-on-month, respectively, with changes of 1.6, 2.0, 0.8, 0.0, 0.3, 0.7, -0.1, and -0.1 percentage points from the previous month.

View original image 214K

-

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus -

Ren Zeping: Get out of deflation and start a "new" round of economic stimulus